Programmatic Display Advertising Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

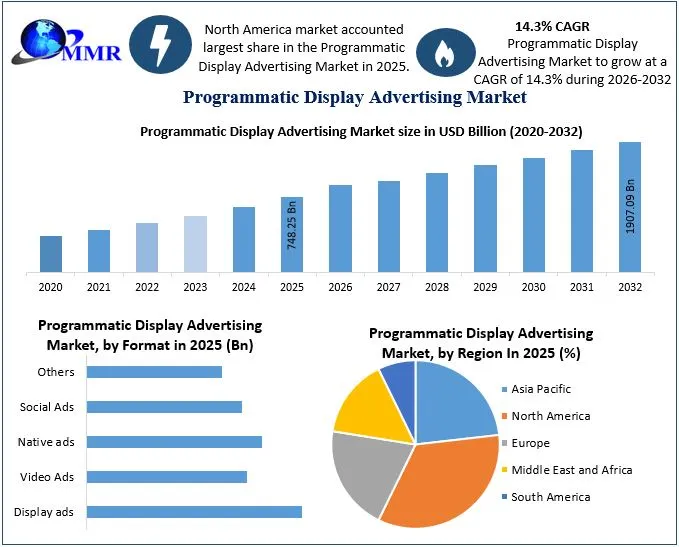

The Programmatic Display Advertising Market was valued at USD 748.25 Bn in 2025, and the total revenue of the Programmatic Display Advertising Market is expected to grow at a CAGR of 14.3% from 2026 to 2032, reaching nearly USD 1907.09 Bn by 2032.

Programmatic Display Advertising Market Overview:

The practice of automatically purchasing and selling digital advertising space is known as programmatic advertising. The use of automation distinguishes programmatic advertising from more conventional media purchase strategies. Before programmatic advertising, all ad ordering, setup, and reporting had to be done manually. Programmatic advertising streamlines the process, making it more successful and efficient.

Because programmatic platforms have built up their ad inventory and database, all formats and channels may be accessed programmatically. Since publishers have enabled native advertisements on their websites, programmatic advertising has reached unprecedented heights. The major reason publishers are adopting programmatic native advertising is that it is less susceptible to ad blockers than other ad formats and platforms.

Despite persistent ambiguity as third-party identifiers are gradually phased away, programmatic display advertising demand is growing, with marketers increasing their expenditure. Programmatic ads continue to gain traction as marketers, ad tech platforms, and publishers collaborate to create a new normal. Retail media networks are poised to be the third wave of digital advertising. This implies greater ad supply near the point of purchase, with the added benefit of customer data. Several retail media networks have formed in the past few years, with nearly every leading online marketplace, mass merchandiser, supermarket chain, category-specific store, and delivery company involved.

Programmatic Display Advertising Market Report Scope:

The Programmatic Display Advertising market is segmented based on Format, Organization Size, Platform, Display, and Region. The growth of various segments helps report users in acquiring knowledge of the many growth factors expected to be prevalent throughout the market and develop different strategies to help identify core application areas and the gap in the target market. The report provides an in-depth analysis of the market and contains meaningful insights, facts, historical data, and statistically supported and industry-validated market statistics. It also includes estimates based on an appropriate set of assumptions and methodologies.

A bottom-up approach has been used to estimate the market size. Key Players in the Programmatic Display Advertising market are identified through secondary research and their market revenues are determined through primary and secondary research. Secondary research included a review of annual and financial reports of leading manufacturers, while primary research included interviews with important opinion leaders and industry experts such as skilled front-line personnel, entrepreneurs, and marketing professionals. Some of the leading key players in the global Programmatic Display Advertising market include AppNexus Inc., AOL Inc., Yahoo! Inc., DataXu Inc., and Google Inc.

The report is not only a representation of global players but also covers the market holding of local players in each country. Market structure by country with market holding by market leaders, market followers, and local players make this report a comprehensive and insightful industry outlook. The report has covered the mergers and acquisitions, strategic alliances, joint ventures, and partnerships happening in the market by region, by investment, and their strategic intent.

To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

Programmatic Display Advertising Market Dynamics:

The impact of programmatic advertising on digital marketing frameworks:

As digital media technology and cell phones have advanced, online advertising has become increasingly personalized and engagement driven. The development of digital marketing systems has influenced advertising firms to create a system that can assist in ad automation. This field is becoming more inventive, competitive, and demanding with the introduction of immensely improved and advanced technology.

In the competitive environment of digital advertising, more effective methods and frameworks have been established that are applied by various ad agencies in obtaining correct output and profits through online promotions and networking techniques. The digital advertising industry is currently the most affordable method for customers, ad agencies, and advertisers all over the world to complete daily work activities, purchase goods, and invest in these products.

Rapid changes in digital marketing assist in converting accurate information through various modes of systems that can support digital users’ information. Companies are constantly going to improve in enhancing the efficiency and profits of online strategies to increase the marginal return on financial expenditure of automated promotional media.

Retail media networks and their competitive strategies:

Retailers have taken considerable measures to embrace the commerce-media trend by building RMNs, supported by their vast and steady user bases, new real estate for ad placements, and the abundance of privileged first-party data. What was once thought to be a side business producing extra cash from "sponsored items" is now a strategic approach for retailers to create consumer loyalty. By 2026, the growth of RMNs in the United States might account for up to $100 billion in ad expenditure.

Companies throughout the retail spectrum are well aware of the financial possibilities, with RMNs' overall operating margins ranging from 50 to 70 percent. Amazon, for example, has pioneered the use of its e-commerce data collection to build an advertising and technology company that now extends well beyond sponsored commercials on its shopping site. Retailers with low margins and those new to e-commerce may want to investigate selling off- and on-site sponsored adverts as a feasible approach.

| Retail Media Networks | Owned By | Type | Average Monthly Unique Visitors | Offerings |

| Amazon Advertising | Amazon | General RMN | 213 Million+ | Sponsored products onsite and offsite display |

| Walmart Connect | Walmart | General RMN | 100 Million+ | Sponsored products, onsite and offsite display, and in-store advertising |

| Roundel | Target | General RMN | 120 Million+ | Sponsored products, Google search display, onsite and offsite display, connected TV |

| Retail Media+ | Home Depot | Niche RMN | 183 Million+ | Onsite and offsite advertising, email advertising |

| Wayfair | Wayfair | Niche RMN | 39 Million+ | Sponsored products, onsite and offsite advertising, and promotions |

| Criteo Retail Media | Criteo | Connected RMN | N/A | Onsite, offsite, and commerce display advertising |

| CitrusAd | CitrusAd | Connected RMN | N/A | Sponsored products, banner advertising, branded landing pages, and fixed tenancy |

The dearth of skilled professionals in the programmatic advertisement sector:

The inability of trained individuals in advertising and marketing firms to adopt new technological tools to build programmatic display adverts on digital platforms limits the market's growth. In addition, the limited adoption of smart devices in numerous nations inhibits digitization in various regions and also hinders overall market growth. In core industries, high attrition rates can raise human resource management expenses. It can also have a direct influence on an organization's long-term strategy. Even though technologies are automated, creative content, and marketing strategy, as well as platform strategy, are heavily influenced by humans. As a consequence, it is critical to understand how to put up digital campaigns on multiple platforms to get the most outcomes from them. The absence of such kind of expertise can result in ad fraud and, in some cases, a lack of transparency in complicated algorithms.

Programmatic Display Advertising Market Segment Analysis:

Based on Format, the video ad segment dominated the programmatic display advertising market in 2025 with a total share of xx%. This is because of faster network access, the introduction of 5G technology, and the desire for brief material as people's attention spans shrink. Video advertisements are typically a few minutes long with appealing visual and auditory elements that outperform traditional ads. With the rise of social media, a new kind of video advertising has emerged: vertical video. People are more likely to remember video marketing because of the high recall power and the strong pull of audio and video combinations.

The need for patchwork data solutions by advertisers and publishers is expected to be a benefit for some platform providers and a burden for others, but the larger providers, with their massive pools of first-party data, would be positioned to gain disproportionate shares of the market. Demand-side platforms (DSPs), which allow marketers to buy video and display advertising from many sources through a single interface, may have to revise their value proposition if they have invested in assets and capabilities that rely on third-party data. However, DSPs with their consumer ID maps, particularly walled gardens and large-scale platforms, are expected to have an edge over their competitors.

Based on Display, the mobile devices segment dominated the market in 2025 with a total share of xx%. This is because of the low cost of smartphones, increased screen time, and the increasing rate of network access. As a result, smartphone advertising has become an essential component of brand marketing strategies. Smartphones have grown into massive databanks of personal inclinations and preferences. This meant that advertisers and marketers could be considerably more precise in their advertising and marketing initiatives. It may also gather data such as location, customer profiles, demographics, and so on.

They have a variety of advertising channels, including web-based, app-based, and third-party platforms. According to a forecast by PwC and the Online Advertising Bureau, mobile advertising accounted for nearly xx% of all internet advertising sales in 2025. In other words, mobile advertisements received $7 out of every $10 spent on advertising. As a result, rising mobile device engagement is driving the programmatic display advertising market growth.

Programmatic Display Advertising Market Recent Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 23 April 2026 | Vereigen Media LLC | The company launched its Revenue-First Demand Generation Programs, incorporating VM Engage to deliver intelligence-driven programmatic display advertising targeted at real-time decision-makers. | This integration bridges the gap between account-based marketing and automated media buying, significantly increasing conversion rates and pipeline visibility for B2B marketers. |

| 04 March 2026 | Orange 142, LLC | The company officially launched Ignition+, a unified, AI-enabled programmatic media solution designed to integrate buy-side and sell-side capabilities within a single stack. | The platform improves cost efficiency for enterprise advertisers by maximizing working media margins and eliminating hidden middleman markups through transparent gross CPM reporting. |

| 10 February 2026 | Growth Channel | The firm partnered with Speedeon to enable direct consumer and predictive audience data activation natively inside its automated media execution workflow. | This alliance scales target precision and cross-channel consistency across programmatic display, digital out-of-home (DOOH), and connected TV (CTV) by eliminating manual onboarding friction. |

| 19 August 2025 | AdCellerant LLC | The digital advertising technology firm expanded its strategic partnership with Vendasta to deploy AI-driven programmatic display solutions alongside automated business tools to over 250,000 SMBs. | The unified architecture empowers local businesses to seamlessly coordinate lead generation and customer conversion operations under a single agile software platform. |

| 17 July 2025 | PubMatic | The independent adtech provider launched an AI-powered Live Sports Marketplace, selecting FanServ as its premier premium digital media inventory partner. | This innovation delivers event-level precision, allowing brands to programmatically scale real-time ad placements during high-attention broadcast moments on streaming platforms. |

Programmatic Display Advertising Market Regional Insights:

This is because of the surge in E-commerce and social media usage, as well as an increase in marketing software solutions and 5G network connectivity. The increased use of connected television (CTV) and digital-out-of-home (DooH) is driving the regional market growth. According to a July 2020 research from the United States Interactive Advertising Bureau (IAB), programmatic advertising is on the rise and is expected to reach over US$ 100 billion in ad spending by 2023, accounting for nearly 70% of digital media advertising. Mobile is expected to account for more than 80% of programmatic digital display ad expenditure across devices. Thus, the enormous diversity of platforms and digital consumers drives North America Programmatic Display Advertising market growth. Consumer privacy rules, notably the California Consumer Privacy Act, and major technology enterprises would demand explicit consent from consumers to share and utilize data created through digital interactions by the end of FY2023. The $150 billion US digital advertising industry will lose access to most third-party data, which has driven programmatic advertising because consumers are often uninformed of how their data is used and are unlikely to consent to provide their data. The advertising sector is facing a confrontation as a result of the reform. With little or no first-party data (data straight from consumers who agreed to share it) and no third-party data, marketing teams, ad agencies, and the publishing and media vehicles where advertising appears would be in the dark about behavioral and demographic perspectives that currently allow them to create targeted customers and segments.

Consumer privacy rules, notably the California Consumer Privacy Act, and major technology enterprises would demand explicit consent from consumers to share and utilize data created through digital interactions by the end of FY2023. The $150 billion US digital advertising industry will lose access to most third-party data, which has driven programmatic advertising because consumers are often uninformed of how their data is used and are unlikely to consent to provide their data. The advertising sector is facing a confrontation as a result of the reform. With little or no first-party data (data straight from consumers who agreed to share it) and no third-party data, marketing teams, ad agencies, and the publishing and media vehicles where advertising appears would be in the dark about behavioral and demographic perspectives that currently allow them to create targeted customers and segments.

Programmatic Display Advertising Market Scope: Inquire before buying

| Global Programmatic Display Advertising Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 748.25 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 14.3% | Market Size in 2032: | USD 1907.09 Bn. |

| Segments Covered: | by Format | Display ads Video Ads Native ads Social Ads Others |

|

| by Organisation Size | Small and medium enterprises (SME) Large enterprises |

||

| by Platform | Demand-Side Platforms (DSPs) Supply-Side Platforms (SSPs) Data Management Platforms (DMPs) Ad Exchanges Ad servers Ad networks |

||

| by Display | Mobile devices Tablets & Laptops Desktops Connected television (CTV) Digital-out-of-home (DooH) Others |

||

| by Industry Vertical | Retail & E-Commerce BFSI IT & Telecom Healthcare & Pharmaceuticals Automotive Media & Entertainment Others |

||

Programmatic Display Advertising Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Programmatic Display Advertising Market, Key Players are

North America

1. Google

2. Facebook

3. Amazon Advertising

4. Verizon Media

5. Microsoft Advertising

6. Adobe Advertising Cloud

7. AppNexus

8. PubMatic

9. OpenX

10. Rubicon Project

11. Xandr

12. MediaMath

13. Sizmek by Amazon

14. Taboola

Europe

15. Criteo

16. Adform

17. Yieldbird

18. Dentsu Aegis Network

19. Teads

20. BidTheatre

21. Mediatool World W AB.

APAC

22. Adimo

23. Baidu

24. FreakOut

FAQs:

1. Which region is expected to dominate the Programmatic Display Advertising Market at the end of the forecast period?

Ans. North America is expected to dominate the Programmatic Display Advertising Market at the end of the forecast period.

2. What was the market share by format in the Programmatic Display Advertising Market in 2025?

Ans. The video ad segment dominated the programmatic display advertising market in 2025 with a total share of 748.25%.

3. What is expected to drive the growth of the Programmatic Display Advertising Market in the forecast period?

Ans. Retail media networks and their competitive strategies.

4. What is the projected market size & growth rate of the Programmatic Display Advertising Market?

Ans. The Programmatic Display Advertising Market was valued at USD 748.25 Bn. in 2025, and the total Programmatic Display Advertising revenue is expected to grow at 14.3% from 2026 to 2032, reaching nearly USD 1907.09 Bn.

5. What segments are covered in the Programmatic Display Advertising Market report?

Ans. The segments covered are Format, Organization Size, Platform, Display, Industry verticals and Region.