Nanomedicine Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

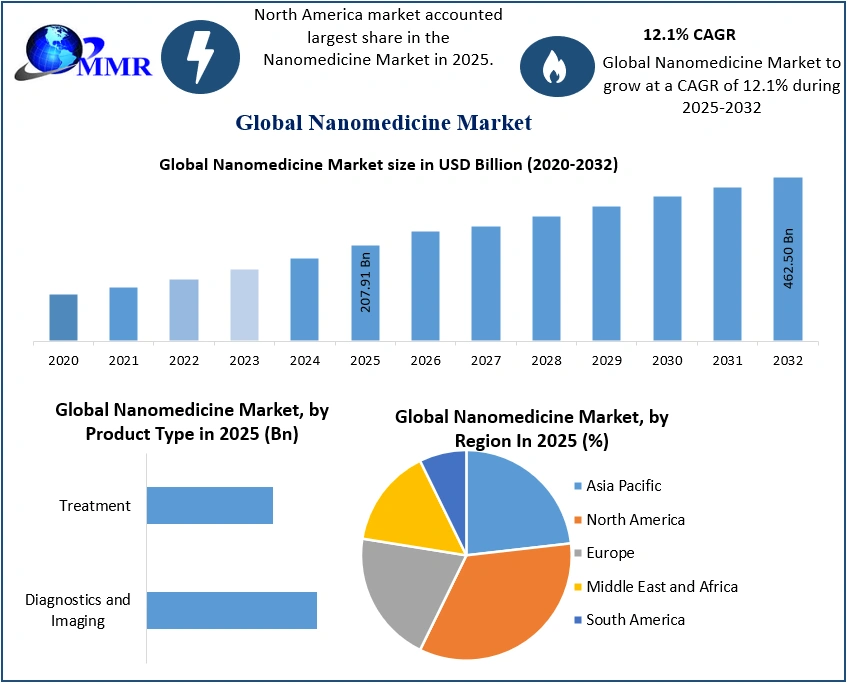

The Nanomedicine Market size was valued at USD 207.91 Billion in 2025 and the total Nanomedicine revenue is expected to grow at a CAGR of 12.1% from 2025 to 2032, reaching nearly USD 462.50 Billion by 2032.

Nanomedicine Market Overview:

The nanomedicine market has witnessed significant growth in recent years driven by the compelling advancements in nanotechnology for healthcare applications. This surge in demand stems from the wide array of opportunities offered by nanotechnology in preventing, diagnosing, and treating diseases like COVID-19 and various viral infections. Nanotechnology has enabled the development of innovative materials such as disinfectants, diagnostic systems, and nanocarrier systems for vaccines and treatments, offering novel strategies to manage health crises. Furthermore, nanomedicine has revolutionized disease management for critical conditions like cancer, Parkinson's, Alzheimer's, diabetes, and cardiovascular ailments. The rise in prevalence rates of diseases like dementia, forecasted to double every 20 years globally, highlights the escalating need for effective nanomedicine-based therapeutics, propelling the nanomedicine market growth.

The growing prevalence of diseases like cancer, coupled with advancements in nanoscale technologies, are expected to be the primary factors driving the global nanomedicine industry growth. In oncology, nanomedicine is heralding transformative treatments and diagnostic methods, offering personalized and efficient solutions. This burgeoning field has seen remarkable progress in engineered nanomaterials and nanoplatforms, diversifying cancer therapies and enhancing sensitive detection methods. Numerous product launches, such as Medtronic PLC's Adaptix Interbody System with Titan nanoLOCK Surface Technology, have further strengthened the nanomedicine market's landscape.

However, challenges persist, with stringent regulatory hurdles and higher costs of nanoparticle-assisted medicines compared to traditional counterparts posing a significant threat to the nanomedicine market. Despite these barriers, the market is expected to continue to grow significantly, fueled by ongoing technological advancements and heightened demand, notably driven by the COVID-19 pandemic's influence. The major players like Sanofi SA, Pfizer Inc., Celgene Corporation, and innovative startups like Nanobiotix, actively launching nanotechnology-based medicines and diagnostic tools, further increase the competitiveness of the global nanomedicine market. The collective efforts of these entities are opening up lucrative avenues, attracting new players, and encouraging novel solutions, such as Innovasis Inc.'s FDA-cleared 3D-printed implants employing Promimic's HAnano Surface Technology. This dynamic landscape showcases the growing importance of nanomedicine in revolutionizing healthcare, promising transformative solutions for various medical challenges. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

China's dominance in nanotechnology indicates a Western threat

China has emerged as a formidable force in nanotechnology, propelled by substantial funding, a burgeoning talent pool, and robust global collaborations. As a result, china has stood out as a major epicenter in the global nanomedicine market in recent years. The Chinese government's staunch commitment to support this scientific domain has positioned the country as a competitor against established forces like the US, EU, Japan, and Russia. Strategically embedded within China's 13th Five-Year Plan, nanotechnology enjoys prioritized state funding and regulatory backing, fostering an environment ripe for innovation. Leveraging the influx of foreign-trained Chinese researchers and scientists, drawn by competitive salaries and ample research funding, has significantly contributed to China's rapid advancements. The synergy between public-private partnerships has yielded substantial success across various nanoscience sectors, notably showcased in Suzhou's 'Nanopolis,' housing multinational corporations and indigenous startups at the forefront of nanotech innovation.

This ascendancy in nanotechnology aligns with China's overarching strategy outlined in the "863 Program," catalyzing the development of pioneering materials and manufacturing technologies. Enhanced by subsequent initiatives like the "973 Program," focused on nanomaterial research, these government-led efforts have fostered a thriving ecosystem. Renowned academic institutions and state-sponsored research centers like the Chinese Academy of Science (CAS) and the National Center for Nanoscience and Technology (NCNST) spearhead cutting-edge research, fostering a surge in private nanotech companies like Array Nano and Nano Medtech.

China's strides in nanotech have birthed groundbreaking innovations with profound implications for various sectors, including medicine. Breakthroughs like synthetic nanoparticle development for precise gene editing and laser-enabled nanobots open vistas for advanced medical treatments. Moreover, CAS's revolutionary nanomaterial designed to mitigate liquid pollution holds promise for eco-friendly solutions in industries like printing. The convergence of China's talent pool, state-backed ambition, and burgeoning private sector indicates a paradigm shift in global nanoscience leadership and supports the nanomedicine market size in recent years.

This burgeoning prowess in nanotechnology by China reverberates profoundly within the global nanomedicine market, introducing disruptive innovations poised to redefine medical treatments and diagnostics. The precision and efficacy promised by nanotech-driven advancements hold the potential to revolutionize drug delivery systems, diagnostic tools, and therapeutic interventions, reshaping the landscape of healthcare and pharmaceutical industries all across the world.

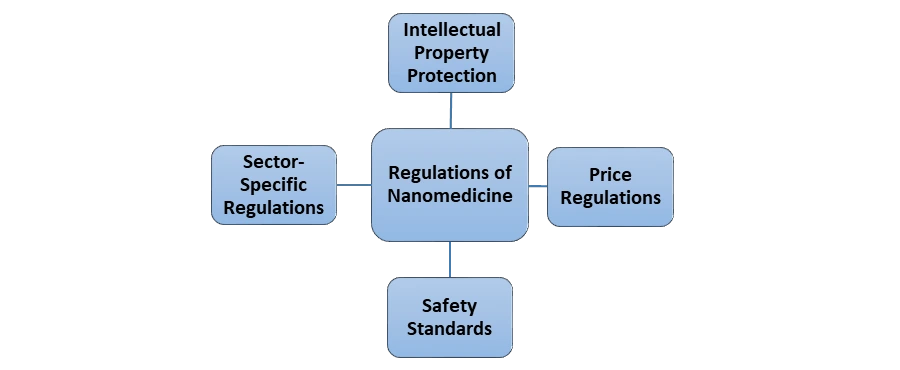

Current Regulatory Framework for Nanomedicine

Under the present laws, a nanomedicine application is expected to be regulated as a drug, medical device, or biologic. However, the absence of a specific definition for nanomedicine poses challenges in regulation, categorizing it based on its application specifics. In terms of drug regulation, the primary statutes governing drugs in India (DCA and DCR) oversee the manufacture, import, distribution, and sale of drugs, but they don't explicitly define or regulate nanomedicine. The CDSCO implements these regulations, requiring licenses for both manufacturing premises and the drugs themselves. Importing nanopharmaceuticals involves specific licensing and registration procedures, with additional India-specific labeling requirements.

For medical devices, the MDR under the DCA governs their regulation. Notified medical devices fall into four risk-based classes, determining the regulatory requirements for approvals and licenses. Clinical investigations and performance evaluations are mandated for certain devices, depending on their categorization. Biologics, including genetically engineered biologics, are regulated under specific guidelines like the Biosimilar Guidelines and Genetically Engineered Microorganisms Rules, in addition to DCA provisions. Marketing approval for nanomedicine involves compliance with various regulations, clinical trial requirements, stability testing, and pharmacovigilance studies. Price regulation under the Drug Price Control Order (DPCO) categorizes nanomedicines as scheduled or non-scheduled formulations, impacting their pricing and permissible price increments.

For medical devices, the MDR under the DCA governs their regulation. Notified medical devices fall into four risk-based classes, determining the regulatory requirements for approvals and licenses. Clinical investigations and performance evaluations are mandated for certain devices, depending on their categorization. Biologics, including genetically engineered biologics, are regulated under specific guidelines like the Biosimilar Guidelines and Genetically Engineered Microorganisms Rules, in addition to DCA provisions. Marketing approval for nanomedicine involves compliance with various regulations, clinical trial requirements, stability testing, and pharmacovigilance studies. Price regulation under the Drug Price Control Order (DPCO) categorizes nanomedicines as scheduled or non-scheduled formulations, impacting their pricing and permissible price increments.

Safety standards are managed under the broad framework of the Environmental Protection Act, including Hazardous Waste Rules. Additionally, guidelines for safe handling of nanomaterials in research laboratories and industries have been proposed. Intellectual property protection for nanomedicines involves patents, copyrights for software components, and trademark protection, aligning with India's intellectual property regime. Regulations on machine-to-machine (M2M) communications are evolving, impacting nanomedicine applications using M2M technologies, such as sensors or continuous monitoring devices. This regulatory landscape affects the nanomedicine market by dictating approval processes, pricing structures, safety standards, and intellectual property protection. Clarity in defining nanomedicine and developing specific regulations tailored to its unique characteristics is expected to facilitate streamlined and effective governance.

The COVID-19 pandemic Impact on the Global Nanomedicine Market:

The COVID-19 pandemic has significantly influenced the global nanomedicine market, particularly in leveraging nanomaterials' unique properties for combating the virus. Nanomaterials, ranging from nanoparticles to graphene and carbon nanotubes, played crucial roles in various aspects of pandemic management, including diagnostics, therapeutics, wearables, and personal protective equipment (PPE). These materials showcased their antimicrobial, biocompatible, and low cytotoxic characteristics, driving their use in immune engineering, nano vaccine production, surface disinfectants, and base materials for PPE manufacturing.

In diagnostics, nanotechnology-based solutions, such as rapid antigen testing using nanoparticles and nano biosensors for detecting SARS-CoV-2 antibodies, experienced heightened demand. Therapeutically, nanomaterials became integral in COVID-19 vaccinations (e.g., BNT162b2 mRNA vaccine by BioNTech and Pfizer) and drug delivery systems, capitalizing on their unique delivery capabilities and antiviral effects against various viruses. As a result, the diagnostics segment generated the maximum revenue share in the nanomedicine market during the pandemic. Moreover, nanotechnology's role in producing antiviral coatings, airborne virus filters, and enhanced facemasks significantly impacted the wearables and PPE sectors. These materials, particularly when combined with substances like graphene oxide and metallic nanoparticles, exhibited increased antiviral activity, offering smarter antimicrobial surfaces and long-lasting disinfection properties upon heat application.

Despite short-term setbacks caused by lockdowns and supply chain disruptions, the pandemic's long-term impact fostered the nanomedicine market growth. The urgency to develop COVID-19-related products laid the groundwork for sustained demand, not just limited to pandemic management but also expanding into broader applications, such as improved diagnostics, hygiene products, and medical devices. The pandemic's aftermath positions nanotechnology as a pivotal tool in managing future viral outbreaks, and driving research and development toward improved vaccines, antivirals, and early detection systems. This trajectory points to an increased demand for nanomaterials in healthcare, underscoring their continued significance in global healthcare strategies beyond the COVID-19 era.

Nanomedicine Market Dynamics:

Increasing Use Of Nanotechnology In Drug Delivery

The rapidly increasing adoption of nanotechnology in drug delivery is expected to be the major factor driving the nanomedicine market growth. Nanoparticles' unique properties offer precise drug targeting, enhanced therapeutic efficacy, and reduced side effects, revolutionizing conventional drug delivery systems. This shift has accelerated due to the ability of nanoparticles to traverse biological barriers, delivering drugs directly to specific cells or tissues. The nanomedicine market's growth is propelled by this innovative approach, attracting substantial investments globally.

This factor significantly influences the nanomedicine market by fostering advancements in drug development and treatment strategies. The increased precision and efficiency in drug delivery achieved through nanotechnology pave the way for more effective therapies, opening new avenues for treating complex diseases. Moreover, the potential for minimizing adverse effects and improving patient outcomes strengthens the market's appeal to both pharmaceutical companies and healthcare providers, driving further research and development initiatives.

Countries exhibiting the highest demand for nanomedicine solutions include the United States, European nations such as Germany, the United Kingdom, and France, and rapidly emerging markets in Asia, especially China and Japan. These regions witness robust investments in nanotechnology and healthcare infrastructure, leading to increased adoption of nanomedicine in drug delivery and therapeutics.

High Adoption Rate Of Nanomedicine For The Treatment Of Ocular Diseases

The high adoption rate of nanomedicine for treating ocular diseases has emerged as a significant driver propelling the growth of the nanomedicine market. Ophthalmology, in particular, has witnessed a surge in demand for advanced treatments due to the limitations faced by conventional eyedrops and sprays. The challenges of poor bioavailability and short-term effectiveness associated with traditional formulations have spurred the development and utilization of nanoparticle-based eyedrops. Nanotechnology-based formulations, like lipid-based nanoparticles and micellar preparations, have notably enhanced drug retention on the ocular surface and improved corneal penetration, significantly boosting drug bioavailability. This advancement has been particularly impactful in addressing chronic ocular diseases, such as dry eye syndrome, infections, and inflammatory conditions, where conventional therapies fell short in providing efficient and sustained relief.

The demand for nanomedicine in ophthalmology has surged due to the compelling need for more effective and patient-friendly treatments in a domain that traditionally faced challenges of poor drug retention and limited bioavailability. Ophthalmic preparations like eyedrops and sprays have been vital in providing relief for common eye conditions and serious diseases affecting the anterior segment of the eye, such as cataracts and chronic dry eye disease. However, the inefficiency of conventional formulations in delivering drugs to the target ocular compartments propelled the exploration and utilization of nanotechnology. Nanoparticle-based formulations, including lipid-based nanoparticles, micellar preparations, and liposomal formulations, have revolutionized ocular drug delivery by significantly enhancing drug bioavailability and offering sustained therapeutic effects, thus contributing to the burgeoning demand for nanomedicine in ophthalmology and supporting the nanomedicine market growth during the forecast period.

The demand for nanomedicine in ophthalmology has surged due to the compelling need for more effective and patient-friendly treatments in a domain that traditionally faced challenges of poor drug retention and limited bioavailability. Ophthalmic preparations like eyedrops and sprays have been vital in providing relief for common eye conditions and serious diseases affecting the anterior segment of the eye, such as cataracts and chronic dry eye disease. However, the inefficiency of conventional formulations in delivering drugs to the target ocular compartments propelled the exploration and utilization of nanotechnology. Nanoparticle-based formulations, including lipid-based nanoparticles, micellar preparations, and liposomal formulations, have revolutionized ocular drug delivery by significantly enhancing drug bioavailability and offering sustained therapeutic effects, thus contributing to the burgeoning demand for nanomedicine in ophthalmology and supporting the nanomedicine market growth during the forecast period.

Economic Challenges Of The Nanomedicine Market

The economic landscape presents substantial challenges for the nanomedicine market. Commercializing nanodrugs from concept to reality involves extensive validation and navigating through costly clinical trials, a process mainly shouldered by small and medium-sized enterprises (SMEs). Surprisingly, major pharmaceutical companies often maintain a subdued interest until SMEs validate a concept, prompting increased interest through acquisition. Collaboration between SMEs, academia, and larger pharmaceutical entities is crucial, leveraging each partner's strengths. While public funding supports initial risky projects, industrial investment typically emerges once significant risks are mitigated, shifting the focus toward commercially viable projects.

Cost inefficiencies pose a significant hurdle for nanotherapeutics, thereby further restraining the nanomedicine market growth potential. The manufacturing expenses for nanodrugs far exceed those of conventional medicines, leading to higher acquisition costs for hospitals or end consumers. Despite potential cost-effectiveness, excessively high prices hinder market success and reimbursement. Limited expertise in nanomedical technology and constrained manufacturing capabilities further compound these challenges. Particularly in regions where medicines are publicly funded based on rational selection, high acquisition costs become prohibitive, impeding market access and patient availability.

In for-profit healthcare systems like the USA, intermediaries control healthcare expenditures, often resisting the reimbursement of expensive yet highly effective nanomedicines. Moreover, soaring healthcare costs globally, fueled by chronic diseases and epidemic rates, exert immense pressure to optimize healthcare efficiency. These challenges underscore the critical need for an efficient allocation of healthcare resources to contain rising costs while ensuring access to novel and impactful nanodrugs at reasonable prices. These factors are expected to support the global nanomedicine market growth during the forecast period.

Nanomedicine Market Regional Insights:

North America led the global nanomedicine market with the highest market share of 43.78% and is expected to maintain its dominance throughout the forecast period. The growth is attributed to the technological advancements applied in early disease detection, preventive interventions, and managing chronic disorders. In the United States, conditions like heart disease and stroke drive the demand for specialized nano vectors, nanostructured implants, and stents for tissue regeneration, thereby supporting the nanomedicine market growth in North America. Ongoing R&D endeavors focus on nanotech-based drugs and diagnostics, exemplified by Stanford University's nanoparticle-coated drug inhibiting atherosclerosis in mice without adverse effects.

Market players within the nanomedicine industry are actively innovating, partnering, or acquiring companies to compete or introduce novel technologies to remain competitive. For instance, Nano-X Imaging and SPI Medical's collaboration on Nanox ARC, a nanotech-driven X-ray system, typifies this trend, replacing traditional cathode-ray tubes with semiconductor-based technology. The COVID-19 pandemic accelerated nanomedicine's role, as seen in research efforts for effective therapeutics and vaccines. The Canadian government's substantial funding to Precision NanoSystems in October 2020 reflects this, supporting the development of a lipid-based RNA vaccine for COVID-19. Thus, this factor is expected to boost the nanomedicine market growth in Canada.

However, the stringent approval process and regulatory framework set by the US Food and Drug Administration (FDA) for nanomedicine products distinguish them from other industries using nanotechnologies. The extensive and costly approval procedures compel pharmaceutical and biotechnology industries to focus predominantly on blockbuster products to satisfy shareholder expectations. Nanoparticles, while not inherently hazardous, possess unique properties that raise safety concerns, necessitating comprehensive safety evaluations due to their novelty. Federal agencies like the FDA and the US Patent and Trade Mark Office (PTO) aim to safeguard public safety while fostering product development. However, the emergence of nanomedicine has introduced significant regulatory challenges, primarily concerning product classification and the FDA's limited scientific expertise in this domain.

The FDA categorizes nanoproducts based on their primary mode of action, labeling them as drugs, devices, or a combination of both. Yet, defining nano-based drug delivery devices becomes intricate as they straddle the line between being carriers (devices) or effectors (drugs), creating ambiguity in their regulatory classification. This ambiguity poses substantial challenges for the FDA in effectively regulating these products. Overcoming these challenges requires a robust scientific understanding of nanomedicine and a nuanced grasp of the potential risks associated with patient exposure to such products. This regulatory landscape significantly impacts the nanomedicine market. The arduous approval process and ambiguity in product classification lead pharmaceutical and biotech industries to focus predominantly on high-return, blockbuster products to navigate the rigorous regulatory pathway.

China is expected to be the lucrative region in the Asia Pacific nanomedicine Market during the forecast period. The China Nano conference, which was held in Beijing from 26–28 Augusta, 2023, a hallmark event in nanoscience and technology, reflects significant shifts in the landscape since its last edition was canceled due to the pandemic. This gathering, renowned as the largest of its kind, witnessed a surge in focus on nanobiotechnology and nanomedicine, aligning with the global success story of mRNA vaccines. The success of mRNA vaccines revitalized funding for nanomedicine, particularly lipid nanoparticles for delivery purposes, reigniting optimism around nanomedicine's clinical potential. The heightened interest in these sessions underscores a pivotal moment for the field, drawing attention and funding to fundamental nanobiotechnology aspects.

China is expected to be the lucrative region in the Asia Pacific nanomedicine Market during the forecast period. The China Nano conference, which was held in Beijing from 26–28 Augusta, 2023, a hallmark event in nanoscience and technology, reflects significant shifts in the landscape since its last edition was canceled due to the pandemic. This gathering, renowned as the largest of its kind, witnessed a surge in focus on nanobiotechnology and nanomedicine, aligning with the global success story of mRNA vaccines. The success of mRNA vaccines revitalized funding for nanomedicine, particularly lipid nanoparticles for delivery purposes, reigniting optimism around nanomedicine's clinical potential. The heightened interest in these sessions underscores a pivotal moment for the field, drawing attention and funding to fundamental nanobiotechnology aspects.

Nanomedicine Market Scope: Inquire before buying

| Global Nanomedicine Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 207.91 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 12.1% | Market Size in 2032: | USD 462.50 Bn. |

| Segments Covered: | By Product Type | Diagnostics and Imaging Treatment |

|

| By Application | Drug Delivery Diagnostic and Imaging Vaccines Regenerative Medicine Implants Others |

||

| By Indication | Clinical Oncology Infectious Diseases Clinical Cardiology Orthopedics Neurology Urology Ophthalmology Immunology Others |

||

Global Nanomedicine Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Nanomedicine Market, Key Players

Global Nanomedicine Market Major Players:

1. Elan Corporation (Ireland)

2. Taiwan Liposome Company Ltd (Taiwan)

3. NanoCarrier Co. Ltd (Japan)

4. LiPlasome Pharma ApS (Denmark)

5. Starpharma Holdings Limited (Australia)

6. Sanofi SA (France)

7. Bristol-Myers Squibb Company (U.S.)

8. Teva Pharmaceutical Industries Ltd. (Israel)

9. Spago Nanomedical AB (Sweden)

Leading Nanomedicines Providers in North America:

1. BIND Therapeutics (U.S.)

2. Ensysce Biosciences (U.S.)

3. Genzyme Corporation (U.S.)

4. Gilead Sciences (U.S.)

5. Insys Therapeutics (U.S.)

6. Intarcia Therapeutics (U.S.)

7. Nanoprobes (U.S.)

8. Nanosphere Health Sciences (U.S.)

9. Abbott Laboratories (U.S.)

10. CombiMatrix Corporation (U.S.)

11. Celgene Corporation (U.S.)

12. GE Healthcare (U.S.)

13. Johnson & Johnson Services, Inc. (U.S.)

14. Mallinckrodt Pharmaceuticals (U.S.)

15. Merck & Co., Inc. (U.S.)

16. Pfizer, Inc. (U.S.)

17. Arrowhead Pharmaceuticals, Inc. (U.S.)

18. CytImmune Sciences Inc. (U.S.)

19. Luminex Corporation (U.S.)

20. Copernicus Therapeutics Inc. (U.S.)

21. Ocuphire Pharma Inc. (U.S.)

22. Name Therapeutics Corp. (U.S.)

23. Genetic Immunity (U.S.)

Major Nanomedicine Providers in Europe:

1. Ablynx (Belgium)

2. Nanobiotix (France)

3. Nanospectra Biosciences (France)

4. Stealth BioTherapeutics (U.S. & Europe - headquarters in Ireland)

FAQs:

1. What are the growth drivers for the Nanomedicine market?

Ans. The increasing prevalence of diseases, technological advancements in nanoscale technologies for diagnostics and therapies, and a rising preference for personalized medicine are expected to be the major drivers for the Nanomedicine market.

2. What is the major restraint for the Nanomedicine market growth?

Ans. Stringent regulatory issues and the comparatively high cost of nanoparticle-based medicines compared to traditional alternatives are expected to be the major restraining factors for the Nanomedicine market growth.

3. Which region is expected to lead the global Nanomedicine market during the forecast period?

Ans. North America is expected to lead the global Nanomedicine market during the forecast period due to its advanced healthcare infrastructure, extensive R&D activities, and significant investments in nanotechnology.

4. What is the projected market size and growth rate of the Nanomedicine Market?

Ans. The Nanomedicine Market size was valued at USD 207.91 Billion in 2025 and the total Nanomedicine revenue is expected to grow at a CAGR of 12.1% from 2025 to 2032, reaching nearly USD 462.50 Billion by 2032.

5. What segments are covered in the Nanomedicine Market report?

Ans. The segments covered in the Nanomedicine market report are Product Type, Applications, Indication, and Region.