Surgical Wound Closure Device Market Size by Product, Wound Type, End-use, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

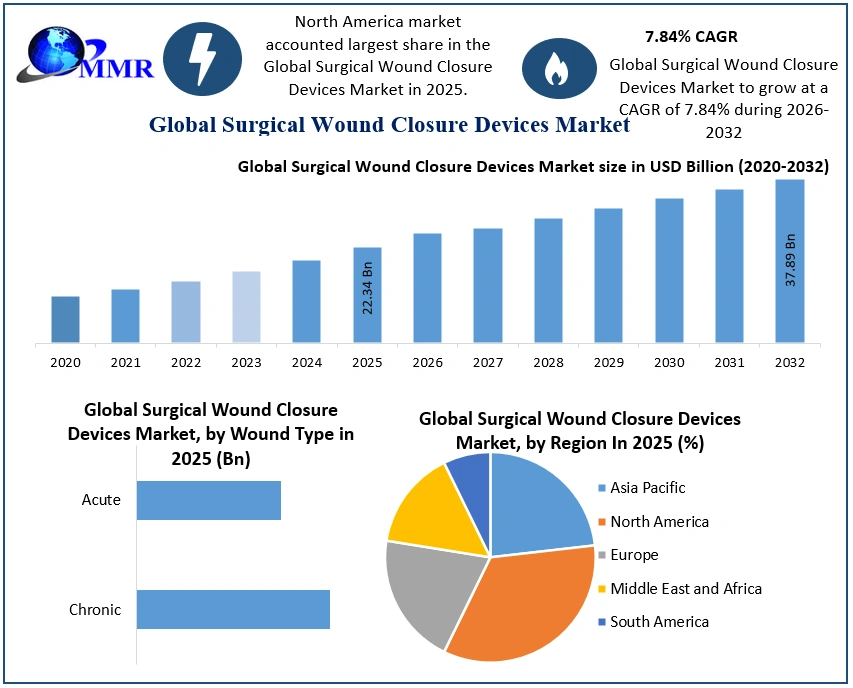

The Surgical Wound Closure Devices Market size was valued at USD 22.34 Billion in 2025 and the total Surgical Wound Closure Devices revenue is expected to grow at a CAGR of 7.84% from 2026 to 2032, reaching nearly USD 37.89 Billion by 2032.

Surgical wound closure devices are medical tools used to close wounds and incisions following surgical procedures or injuries. These devices play a crucial role in facilitating wound healing by securing tissue and promoting proper alignment for optimal recovery. Common types of surgical wound closure devices include sutures, staples, adhesive tapes, and hemostats, each serving specific purposes based on the nature and location of the wound. Sutures, for example, are threads or wires used to stitch tissues together, while staples are metal clips applied externally to hold wound edges in place. Advanced closure devices may incorporate innovative materials such as bioresorbable polymers, enhancing biocompatibility and reducing the need for device removal.

The global surgical wound closure devices market is experiencing robust growth driven by several factors. The market encompasses a wide range of products designed to meet diverse surgical needs, including traditional closure methods and innovative technologies. Currently valued at billions of dollars, the market is expected to continue expanding at a steady pace, propelled by increasing surgical procedures worldwide, advancements in medical technology, and growing healthcare expenditures. Key players in the market are continuously innovating to introduce novel products with enhanced efficacy, safety, and patient comfort, further driving market growth and competitiveness.

The rising number of surgical procedures globally is driven by factors such as the aging population, the increasing prevalence of chronic diseases, and advancements in surgical techniques. This surge in surgical interventions creates a substantial demand for effective wound closure solutions, boosting Surgical Wound Closure Devices Market growth. Technological advancements in wound closure devices, including the development of bioabsorbable sutures, surgical adhesives, and minimally invasive closure techniques, contribute to market growth by improving patient outcomes and reducing post-operative complications. The increasing adoption of advanced materials and techniques, such as bioresorbable sutures and minimally invasive closure methods, stands out. These innovations offer advantages such as improved biocompatibility, reduced tissue trauma, and faster recovery, driving market growth.

The growing demand for outpatient surgical procedures and ambulatory care settings fosters the development of portable and disposable closure devices, catering to the need for convenient and cost-effective solutions. Furthermore, strategic collaborations and partnerships among key market players and healthcare institutions accelerate product development and Surgical Wound Closure Devices Market penetration, driving innovation and competitiveness. Recent developments in the market include the introduction of advanced closure techniques such as non-invasive wound closure technologies and the development of smart wound closure devices equipped with sensors and connectivity features. These innovations aim to enhance the efficiency, accuracy, and patient experience in wound management, driving market growth and differentiation.

To know about the Research Methodology :- Request Free Sample Report

Market Dynamics:

Advancements in Surgical Wound Closure Technologies:

Continuous advancements in surgical wound closure devices, such as the introduction of innovative materials and techniques like bioabsorbable sutures and surgical adhesives, are driving Surgical Wound Closure Devices Market growth. For example, the development of 3D-printed surgical meshes allows for customized wound closure solutions, enhancing patient outcomes and reducing complications. The increasing number of surgical procedures globally, driven by factors like the aging population and the prevalence of chronic diseases, creates a growing demand for surgical wound closure devices.

For instance, the rising incidence of cardiovascular surgeries necessitates the use of specialized closure devices like vascular clips and staplers to ensure effective wound closure and patient safety. The surge in traumatic injuries due to accidents, sports injuries, and natural disasters fuels the demand for advanced wound closure devices in emergency and trauma care settings. For example, trauma surgeons rely on hemostatic agents and wound closure strips to manage lacerations and control bleeding efficiently, driving Surgical Wound Closure Devices Market growth in trauma care applications.

The preference for minimally invasive surgical procedures over traditional open surgeries is driving the adoption of specialized closure devices such as trocars, suturing devices, and surgical staples. For instance, the growing demand for laparoscopic cholecystectomy procedures necessitates the use of trocars and specialized staplers for effective wound closure and faster recovery, boosting market growth in minimally invasive surgery applications. The escalating prevalence of chronic wounds, including diabetic ulcers, pressure ulcers, and venous leg ulcers, propels the demand for advanced wound closure solutions like negative pressure wound therapy systems and skin closure devices. For example, the use of skin adhesive products in diabetic foot ulcer management facilitates faster wound healing and reduces the risk of infections, driving Surgical Wound Closure Devices Market growth in wound care applications.

Robotic-Assisted Surgery Drives Specialized Wound Closure Devices:

The increasing adoption of advanced materials such as bioresorbable polymers and synthetic grafts in surgical wound closure devices enhances their biocompatibility, durability, and performance, driving Surgical Wound Closure Devices Market growth. For instance, the use of synthetic mesh implants in hernia repair surgeries offers superior strength and reduces the risk of postoperative complications, leading to increased adoption and market growth in the surgical hernia repair segment. The shift towards value-based healthcare models emphasizes the importance of efficient wound management and reduced hospital stays, driving the adoption of advanced wound closure devices that promote faster healing and minimize post-operative complications.

For instance, the use of absorbable sutures with antimicrobial coatings reduces the risk of surgical site infections, leading to improved patient outcomes and cost savings, driving market growth in value-based healthcare settings. Rising healthcare expenditure worldwide, coupled with investments in healthcare infrastructure development, create opportunities for Surgical Wound Closure Devices Market growth in both developed and emerging economies. For example, government initiatives to enhance surgical care facilities and access to quality healthcare services in developing countries drive the demand for surgical wound closure devices, leading to market growth in these regions.

The proliferation of ambulatory surgical centers as cost-effective alternatives to traditional hospital settings creates a significant demand for portable and disposable wound closure devices that streamline surgical procedures and promote patient convenience. For example, the use of disposable skin staplers and adhesive strips in ASCs facilitates efficient wound closure and reduces the risk of cross-contamination, driving Surgical Wound Closure Devices Market growth in ambulatory surgical settings. The increasing adoption of robotic-assisted surgical techniques in various specialties, including general surgery, urology, and gynecology, drives the demand for specialized wound closure devices compatible with robotic platforms. For instance, the integration of robotic stapling systems in robotic-assisted laparoscopic surgeries ensures precise tissue approximation and secure wound closure, leading to improved surgical outcomes and driving Surgical Wound Closure Devices Market growth in robotic surgery applications.

Regulatory Hurdles Impeding Market Growth for Surgical Wound Closure Devices:

Stringent regulatory requirements for the approval and commercialization of surgical wound closure devices impede Surgical Wound Closure Devices Market growth. For example, the lengthy and rigorous FDA approval process for new medical devices delays product launches and hinders market penetration, limiting revenue generation for manufacturers and constraining market growth. The high initial investment and ongoing maintenance costs associated with advanced surgical wound closure technologies act as a barrier to adoption.

For instance, robotic-assisted surgical systems require significant capital investment, limiting their accessibility to healthcare facilities with constrained budgets and hindering Surgical Wound Closure Devices Market growth in certain regions. Inadequate reimbursement policies for surgical wound closure devices deter healthcare providers from investing in advanced solutions. For example, if reimbursement rates do not adequately cover the cost of innovative closure devices, hospitals, and clinics will opt for more cost-effective alternatives, constraining Surgical Wound Closure Devices Market demand and revenue potential for manufacturers.

The potential risk of adverse events and complications associated with certain surgical wound closure devices, such as infections, tissue damage, or allergic reactions, deters healthcare professionals from adopting new technologies. For example, concerns about the safety profile of bioabsorbable sutures lead surgeons to prefer traditional non-absorbable sutures, limiting market acceptance and adoption of innovative products. Established clinical practices and preferences among healthcare professionals present a barrier to the adoption of new surgical wound closure devices. For instance, surgeons accustomed to using conventional techniques and materials are hesitant to switch to newer, more advanced closure technologies, leading to slower market uptake and longer adoption timelines.

Surgical Wound Closure Devices Market Segment Analysis:

Based on Product, The Sutures segment dominates the Surgical Wound Closure Devices Market in 2025. Sutures play a pivotal role, with both absorbable and non-absorbable categories contributing significantly. Historically, non-absorbable sutures have dominated due to their widespread use in various surgical procedures where long-term wound support is required. However, the demand for absorbable sutures is rapidly growing, driven by advancements in material technology and the preference for materials that degrade over time, eliminating the need for suture removal.

Absorbable sutures are increasingly favored in procedures where minimizing tissue trauma and post-operative complications is paramount, such as in delicate surgeries or in pediatric and geriatric patients. While non-absorbable sutures continue to maintain their dominance in specific applications like skin closure and cardiovascular surgeries, absorbable sutures are expected to further dominate the Surgical Wound Closure Devices Market in the forecast period, fueled by their advantages in reducing infection risk and enhancing patient comfort. Both segments cater to diverse surgical needs, with absorbable sutures gaining traction due to their convenience and superior outcomes in certain applications.

Surgical Wound Closure Devices Market Regional Insights:

North America holds a dominant position in the market due to several factors such as advanced healthcare infrastructure, high healthcare expenditure, and an increasing prevalence of chronic diseases requiring surgical interventions. For instance, in the United States, the growing number of surgical procedures, coupled with the emphasis on improving patient outcomes and reducing hospital stays, drives the demand for innovative wound closure devices.

Moreover, the presence of key market players and extensive research and development activities contribute to the region's Surgical Wound Closure Devices Market dominance. However, the Asia-Pacific region is expected to witness significant growth in the coming years. Countries like China and India are experiencing rapid urbanization, rising healthcare investments, and increasing accessibility to advanced healthcare services, leading to a surge in surgical procedures. For example, India's medical tourism industry is booming, attracting patients from around the world for various surgeries, thereby driving the demand for surgical wound closure devices.

Initiatives by governments and healthcare organizations to improve healthcare infrastructure and enhance patient care further propel market growth in the region. With the increasing adoption of next-generation wound closure devices, such as bioresorbable sutures and surgical adhesives, the Asia-Pacific market is poised for substantial growth, offering lucrative opportunities for market players. Europe also holds a significant market share, driven by the presence of a well-established healthcare system, high healthcare expenditure, and an increasing geriatric population.

Countries like Germany, France, and the United Kingdom are witnessing a rise in surgical procedures, particularly orthopedic and cardiovascular surgeries, driving the demand for advanced wound closure devices. However, stringent regulatory requirements and pricing pressures pose challenges to market growth in the region. While North America currently dominates the surgical wound closure devices market, the Asia-Pacific region is expected to emerge as a key growth engine in the forecast period, presenting significant opportunities for Surgical Wound Closure Devices Market players to expand their presence and capitalize on the growing demand for advanced wound closure solutions.

Competitive Landscape

The competitive landscape of the surgical wound closure devices market is characterized by intense competition among key players striving to maintain or enhance their market position through various strategies such as mergers and acquisitions, product innovations, partnerships, and geographical growth. Leading market players such as Johnson & Johnson, Medtronic plc, B. Braun Melsungen AG, and Ethicon Inc. dominate the global market with their extensive product portfolios and strong distribution networks. These companies focus on continuous research and development activities to introduce advanced wound closure solutions, including bioresorbable sutures, surgical adhesives, and hemostatic agents, to address evolving patient needs and surgical requirements.

Additionally, strategic collaborations with healthcare providers and academic institutions enable companies to leverage clinical expertise and accelerate product development cycles. Mergers and acquisitions play a significant role in reshaping the competitive landscape, as companies seek to expand their product offerings and geographical presence. For instance, in 2025, B. Braun Melsungen AG acquired Osseon LLC, a US-based provider of minimally invasive vertebral compression fracture solutions, to strengthen its position in the orthopedic surgery segment.

Furthermore, the entry of new players and startups focusing on innovative wound closure technologies intensifies competition, compelling established companies to enhance their product differentiation and Surgical Wound Closure Devices Market penetration strategies. Overall, the competitive landscape of the surgical wound closure devices market is dynamic and evolving, driven by technological advancements, changing healthcare dynamics, and shifting consumer preferences. Companies that can adapt quickly to Surgical Wound Closure Devices Market trends, leverage strategic partnerships, and invest in product innovation are poised to thrive in this highly competitive market environment.

Surgical Wound Closure Device Market Scope: Inquire before buying

| Global Surgical Wound Closure Device Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 22.34 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 7.84 % | Market Size in 2032: | USD 37.89 Bn. |

| Segments Covered: | by Product | Sutures Absorbable Non-absorbable Strips Sterile Non-Sterile Sealants Synthetic Non-synthetic Collagen-based Staples Adhesives Mechanical wound closure devices |

|

| by Wound Type | Chronic Acute |

||

| by End-use | Hospital Clinics Trauma centers Others |

||

Surgical Wound Closure Device Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Surgical Wound Closure Device Market, Key Players

Key Players in North America:

1. Johnson & Johnson Services, Inc. (New Jersey, United States)

2. 3M - (Minnesota, United States)

3. Cryolife (Georgia, United States)

4. Medtronic (North America)

5. Stryker (Michigan, United States)

Key Players in Europe:

6. B. Braun Melsungen AG (Melsungen, Germany)

7. Arthrex GmbH (Munich, Germany)

8. DACH Medical Group (Zug, Switzerland)

9. Smith & Nephew (Watford, United Kingdom)

10. Gecko Biomedical (Paris, France)

11. BSN Medical Inc. (Hamburg, Germany)

12. ConvaTec (United Kingdom)

FAQs:

1. What are the growth drivers for the Surgical Wound Closure Devices Market?

Ans. Advancements in Surgical Wound Closure Technologies are expected to be the major driver for the Market.

2. What is the major Opportunity for the Surgical Wound Closure Devices Market growth?

Ans. Robotic-Assisted Surgery Drives Specialized Wound Closure Devices is expected to be the major Opportunity in the Market.

3. Which country is expected to lead the global Market during the forecast period?

Ans. North America is expected to lead the Market during the forecast period.

4. What is the projected market size and growth rate of the Market?

Ans. The Surgical Wound Closure Devices Market size was valued at USD 22.34 Billion in 2025 and the total Surgical Wound Closure Devices revenue is expected to grow at a CAGR of 7.84% from 2026 to 2032, reaching nearly USD 37.89 Billion by 2032.

5. What segments are covered in the Market report?

Ans. The segments covered in the Market report are by Product, Wound Type, End User, and Region.