In-Vitro Diagnostics Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

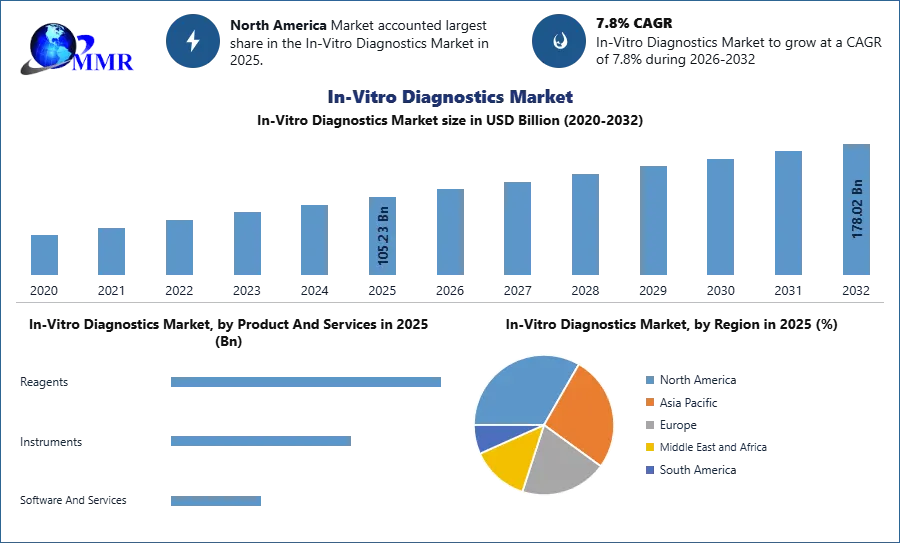

The In-Vitro Diagnostics Market size was valued at USD 105.23 Billion in 2025 and the total In-Vitro Diagnostics revenue is expected to grow at a CAGR of 7.8% from 2026 to 2032, reaching nearly USD 178.02 Billion.

In-Vitro Diagnostics (IVD) are diagnostic tests that are used to diagnose infections and disease, diagnose medical condition, and monitor drug therapies. Such tests are carried out on samples including tissues, blood, and urine.

The development of condition-specific markers and tests, the increasing importance of companion diagnostics, and point-of-care (POC) tests with multiplexing capabilities are the factors that are anticipated to provide significant growth opportunities in the upcoming years, according to primary and secondary research. For a wide range of medical and medicinal applications, manufacturers in the in-vitro diagnostics market are developing and marketing affordable kits and reagents.

The clinical laboratory is well-equipped with assay and instrument systems used for the detection and categorization of many disease types, including cancer, the risk of cancer progression, cardiovascular disease, and testing the efficacy of medications, among others.

As per the World Health Organization, an expected 23.6 million new cases of cancer would be diagnosed globally by 2032, driving up government healthcare spending in the US. The substrates for in vitro diagnostics are utilised in diagnostic kits, assays, tools for diagnostic laboratories, facilities for research and development, and more. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

In-Vitro Diagnostics Market Dynamics:

Globally Increasing Rates of Infectious and Chronic Disorders

Increased prevalence of infectious and chronic diseases globally has led to an increase in in-vitro diagnostics. Heart disease, cancer, diabetes, respiratory issues, Alzheimer's, kidney problems, malaria, jaundice, dengue, TB, and other illnesses are among these. For example, the Centres for Disease Control and Prevention (CDC) estimates that 5.9 million Americans will have Alzheimer's disease in . Additionally, over 241 million cases of malaria were found worldwide in .

In the US, roughly 2,000 cases of malaria are identified annually. Additionally, the use of cutting-edge diagnostic equipment in pathological labs and services will increase demand for in-vitro diagnostics, benefiting the growth of the industry as a whole.

Point-of-care (POC) Testing to Take Precedence over Centralised Laboratory Testing

Testing used to be done nearly entirely in centralised laboratories. For the diagnostic processes to operate as effectively and consistently as possible, centralised laboratory testing is crucial. In recent years, there has been a steady shift away from centralised laboratories to point-of-care testing services or decentralised clinical laboratory testing.

This shift is primarily attributable to point-of-care testing's (POC) lower costs, convenience for patients and clinicians, shorter wait times for results, higher quality, and widespread use. POC tests can enhance patient care in situations involving infectious illnesses. Physicians can better manage clinical operations and keep an eye on patients receiving treatment for infectious diseases thanks to the decentralised.

Increasing R&D Spending to Open up New Opportunities for Major Players in In-Vitro Diagnostics Market

In-vitro diagnostics are now more appealing thanks to a significant advancement in IVD research. For example, pregnancy tests have become very useful and are frequently used at home. In a similar vein, point-of-care monitoring technologies have helped the market for at-home blood glucose monitors grow. This feature also provides prospects for the sector given the growing demand for such technologies. Additionally, the anticipated increase of the IVD market in developed nations is very encouraging and is expected to happen in the forthcoming years.

Regulatory Procedures for Tests of High/Moderate Complexity Probable to Restrict In-Vitro Diagnostics Market Growth

The procedures for diagnostic test and device regulatory approval are time-consuming. To assure the reproducibility and safety of the devices, regulatory approval comprises a review of the clinical data, calibration, manufacturing processes, quality control, risk assessment, and other elements. Despite this, the complexity is the main regulatory roadblock for molecular diagnostic equipment. However, due to their great complexity in POC settings, many institutions around the world decline to conduct these tests.

It is required under the U.S. Clinical Laboratory Improvement Amendments of 1988 (CLIA) to classify molecular diagnostic tests as low-complexity tests or CLIA waived, that is, tests with a low risk of inaccurate results, in order to employ them in POC settings. These tests can be utilised in home healthcare settings, thus they should be extremely contaminant resistant and produce results that are simple to understand quickly, even if they are used by patients without extensive training in that specific assay.

In-Vitro Diagnostics Market Segment Analysis:

By Technique, in 2025, the molecular diagnostics market segment held the highest market share of 37.95% thanks to the launch of new products and continuous development in technology. Whereas complex equipment is often required for PCR, research efforts in this field have led to advancements such postage stamp-sized plasmofluidic chips. According to the ACS Nano Journal in May , plasmofluidic chips are efficient and incredibly quick; they can complete a PCR test in just 8 minutes, and as a result, are anticipated to speed up diagnosis in both current and upcoming pandemics.

The introduction of cutting-edge products that could identify both the flu and SARS-CoV-2 satisfied this unmet demand. To meet the demand, businesses like Roche have released the SARS-CoV-2 & Flu A/B Rapid Antigen Test on the market. For the purpose of identifying infectious microorganisms, tests and assays are included in the microbiology sector.

By Application, the Infectious Diseases segment held the largest market share of 2025 and is projected to grow at the highest CAGR of 4.15% during forecast period. Rising prevalence of diseases including hepatitis, pneumonia, HIV/AIDS, tuberculosis, and others, the infectious disease sector is expected to dominate the market throughout the forecast period. To combat the rising frequency of infectious diseases, key firms are creating cutting-edge diagnostic methods.

Cobas MTB-RIF/INH, which supports clinicians in speeding tuberculosis tests, was introduced by Roche Diagnostics in . The availability of automated in vitro diagnostic tests and the rising incidence of cancer fuel the oncology market's expansion. For example, Roche Diagnostics introduced the Ventana pan-TRK (ERP17341) assay in as an automated in vitro diagnostics immunohistochemistry assay to identify tropomyosin receptor kinase proteins in cancer.

Based on end user, Hospital segment is projected to dominate the market over 2026-2032, thanks to increasing use of modern diagnostic equipment. With the development of technology, new developments of intelligent tools and gadgets have made it simple to detect viruses with better results. In-vitro diagnostics are used more frequently in hospitals due to rising patient visits for medical difficulties, illness diagnosis, and testing. The aforementioned elements will accelerate market growth.

In-Vitro Diagnostics Market Trends:

1.Government support and EU funds: Government support is a major growth factor for the IVD market in the near future because increased government funding enables research institutions to create quick analyser systems beneficial for the diagnosis of a variety of diseases using a variety of samples.

2. Increasing adoption of rapid diagnostic: The need for faster, more accurate, more informative, more inexpensive, and less invasive diagnostic procedures was brought on by the rise in healthcare costs associated with the ageing of the population, the rise in chronic and infectious disease, and particularly the spread of the Covid-19 pandemic.

3.Innovation and technological advancements: Automating laboratory functions can solve the lack of manpower in managing big laboratories that are involved in processing many tests, leading to an increase in the use of automated platforms.

4.Rise of point-of-care testing (POCT): The rise of point-of-care testing (POCT), which is done at or close to the patient's location, such as the doctor's office or the patient's home, is a significant trend in the field of in-vitro diagnostics. POCT has far lower costs and offers significantly quicker turnaround times than central or satellite laboratory testing.

In-Vitro Diagnostics Market Regional Insights:

North America is the global leader in In-vitro diagnostics market. In 2025, it accounted for around 38% of the market share. Thanks to the region's established healthcare sector and the increased frequency of chronic diseases, it is anticipated that this region would enhance its market share in the future. Owing to increase healthcare costs and the quick uptake of point-of-care testing, the United States currently controls the majority of the North American market.

The American Cancer Society estimates that there were nearly 1.8 million new cancer diagnoses and 606,520 cancer-related deaths in the United States in . In addition, Americans who have chronic diseases use healthcare facilities the most frequently. They are mostly responsible for hospital admissions and prescription filling, which propels the market's growth.

Europe: In terms of market share, Region is expected to be the second-most dominating region. Europe has a considerable market share because of its developed infrastructure, rising healthcare costs, and big population of people with cancer and infectious diseases.

Asia Pacific: The market in the Asia Pacific region is anticipated to expand at the highest CAGR, driven by emerging nations like China, South Korea, Australia, and India. The Asia Pacific market is anticipated to increase from 2025 to 2032 as a result of better approval and reimbursement rules and rising per capita healthcare spending in this region.

Asian manufacturing capacity growth and a shift in supply: Leading manufacturers, particularly those in China, have hastened to build capacity for the molecular test components as demand has skyrocketed. As a result, between 70 and 90 % of the world's capacity for key molecular-assay components is now accounted for by China. China may someday become the world's top supplier of diagnostics as a result of this.

The Production Linked Incentive Scheme (PLI 2.0), recently introduced by the Indian government, aims to improve India's manufacturing capabilities by boosting investment and production in the IVD sector. It also seeks to develop Indian companies into global leaders with the potential to scale up using cutting-edge technology and thus enter global value chains.

In-Vitro Diagnostics Market Scope: Inquire before buying

| Global Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 105.23 USD Billion |

| Forecast Period 2026-2032 CAGR: | 7.8% | Market Size in 2032: | 178.02 USD Billion |

| Segments Covered: | by Product And Services | Reagents Instruments Software And Services |

|

| by Technique | Immunodiagnostics Hematology Molecular Diagnostics Tissue Diagnostics Clinical Chemistry Others |

||

| by Application | Infectious Diseases Cancer Cardiac Diseases Immune System Disorders Nephrological Diseases Gastrointestinal Diseases Others |

||

| by End-User | Standalone Laboratories Hospitals Academic And Medical Schools Point Of Care Others |

||

In-Vitro Diagnostics Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitores Proflies Coverd In-Vitro Diagnostics Market Report in Strategic Perspective

1. Danaher Corporation (US)

2. Carlyle Investment Management L.L.C. (US)

3. Beckman Coulter (US)

4. Alere, Inc. (US)

5. Ortho Clinical Diagnostics (US)

6. Agilent Technologies (US)

7. Bio-Rad Laboratories (US)

8. Becton, Dickinson, and Company (US)

9. Thermo Fisher Scientific Inc. (US)

10. Abbott (US)

11. Johnson & Johnson (US)

12. QIAGEN (Germany)

13. Siemens AG (Germany)

14. Roche Diagnostics (Switzerland)

15. F. Hoffmann-La Roche Ltd (Switzerland)

16. BioMérieux SA (France)

17. DiaSorin (Italy)

18. Sysmex Corporation (Japan)

19. Arkray (Japan)