1.1. Study Assumption and Market Definition

1.2. Scope of the Study

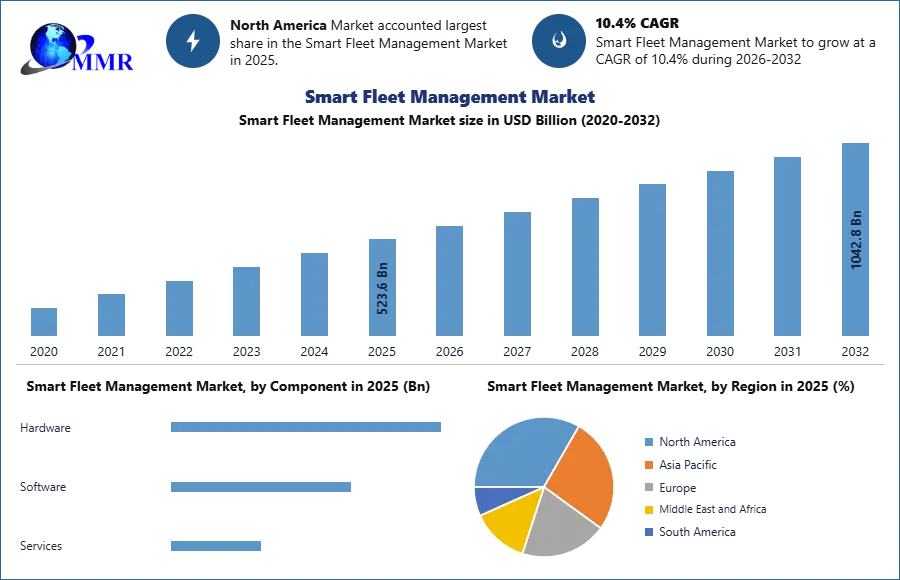

1.3. Executive Summary

2. Global Smart Fleet Management Market: Competitive Landscape

2.1. MMR Competition Matrix

2.2. Competitive Landscape

2.3. Key Players Benchmarking

2.3.1. Company Name

2.3.2. Business Segment

2.3.3. End-user Segment

2.3.4. Revenue (2025)

2.3.5. Company Locations

2.4. Leading Smart Fleet Management Market Companies, by market capitalization

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Smart Fleet Management Market: Dynamics

3.1. Smart Fleet Management Market Trends by Region

3.1.1. North America Smart Fleet Management Market Trends

3.1.2. Europe Smart Fleet Management Market Trends

3.1.3. Asia Pacific Smart Fleet Management Market Trends

3.1.4. Middle East and Africa Smart Fleet Management Market Trends

3.1.5. South America Smart Fleet Management Market Trends

3.2. Smart Fleet Management Market Dynamics by Region

3.2.1. North America

3.2.1.1. North America Smart Fleet Management Market Drivers

3.2.1.2. North America Smart Fleet Management Market Restraints

3.2.1.3. North America Smart Fleet Management Market Opportunities

3.2.1.4. North America Smart Fleet Management Market Challenges

3.2.2. Europe

3.2.2.1. Europe Smart Fleet Management Market Drivers

3.2.2.2. Europe Smart Fleet Management Market Restraints

3.2.2.3. Europe Smart Fleet Management Market Opportunities

3.2.2.4. Europe Smart Fleet Management Market Challenges

3.2.3. Asia Pacific

3.2.3.1. Asia Pacific Smart Fleet Management Market Drivers

3.2.3.2. Asia Pacific Smart Fleet Management Market Restraints

3.2.3.3. Asia Pacific Smart Fleet Management Market Opportunities

3.2.3.4. Asia Pacific Smart Fleet Management Market Challenges

3.2.4. Middle East and Africa

3.2.4.1. Middle East and Africa Smart Fleet Management Market Drivers

3.2.4.2. Middle East and Africa Smart Fleet Management Market Restraints

3.2.4.3. Middle East and Africa Smart Fleet Management Market Opportunities

3.2.4.4. Middle East and Africa Smart Fleet Management Market Challenges

3.2.5. South America

3.2.5.1. South America Smart Fleet Management Market Drivers

3.2.5.2. South America Smart Fleet Management Market Restraints

3.2.5.3. South America Smart Fleet Management Market Opportunities

3.2.5.4. South America Smart Fleet Management Market Challenges

3.3. PORTER's Five Forces Analysis

3.4. PESTLE Analysis

3.5. Technology Roadmap

3.6. Regulatory Landscape by Region

3.6.1. North America

3.6.2. Europe

3.6.3. Asia Pacific

3.6.4. Middle East and Africa

3.6.5. South America

3.7. Key Opinion Leader Analysis For Smart Fleet Management Industry

3.8. Analysis of Government Schemes and Initiatives For Smart Fleet Management Industry

3.9. Smart Fleet Management Market Trade Analysis

3.10. The Global Pandemic Impact on Smart Fleet Management Market

4. Smart Fleet Management Market: Global Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

4.1. Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

4.1.1. Hardware

4.1.2. Software

4.1.3. Services

4.2. Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

4.2.1. Fleet Tracking And Monitoring

4.2.2. Predictive Maintenance

4.2.3. Fuel Management

4.2.4. Driver Behavior Monitoring

4.2.5. Route Optimization

4.2.6. Fleet Analytics

4.2.7. Remote Diagnostics

4.2.8. Asset Tracking

4.3. Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

4.3.1. Cloud

4.3.2. On Premise

4.4. Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

4.4.1. Passenger Vehicles

4.4.2. Light Commercial Vehicles

4.4.3. Heavy Commercial Vehicles

4.5. Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

4.5.1. Embedded Systems

4.5.2. Tethered Systems

4.5.3. Integrated Systems

4.6. Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

4.6.1. Large Enterprises

4.6.2. Small And Medium Enterprises

4.7. Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

4.7.1. Logistics And Transportation

4.7.2. Automotive

4.7.3. Oil And Gas

4.7.4. Mining

4.7.5. Construction

4.7.6. Utilities

4.7.7. Public Transportation

4.7.8. Government Fleet

4.8. Smart Fleet Management Market Size and Forecast, by Region (2025-2032)

4.8.1. North America

4.8.2. Europe

4.8.3. Asia Pacific

4.8.4. Middle East and Africa

4.8.5. South America

5. North America Smart Fleet Management Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

5.1. North America Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

5.1.1. Hardware

5.1.2. Software

5.1.3. Services

5.2. North America Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

5.2.1. Fleet Tracking And Monitoring

5.2.2. Predictive Maintenance

5.2.3. Fuel Management

5.2.4. Driver Behavior Monitoring

5.2.5. Route Optimization

5.2.6. Fleet Analytics

5.2.7. Remote Diagnostics

5.2.8. Asset Tracking

5.3. North America Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

5.3.1. Cloud

5.3.2. On Premise

5.4. North America Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

5.4.1. Passenger Vehicles

5.4.2. Light Commercial Vehicles

5.4.3. Heavy Commercial Vehicles

5.5. North America Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

5.5.1. Embedded Systems

5.5.2. Tethered Systems

5.5.3. Integrated Systems

5.6. North America Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

5.6.1. Large Enterprises

5.6.2. Small And Medium Enterprises

5.7. North America Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

5.7.1. Logistics And Transportation

5.7.2. Automotive

5.7.3. Oil And Gas

5.7.4. Mining

5.7.5. Construction

5.7.6. Utilities

5.7.7. Public Transportation

5.7.8. Government Fleet

5.8. North America Smart Fleet Management Market Size and Forecast, by Country (2025-2032)

5.8.1. United States

5.8.1.1. United States Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

5.8.1.1.1. Hardware

5.8.1.1.2. Software

5.8.1.1.3. Services

5.8.1.2. United States Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

5.8.1.2.1. Fleet Tracking And Monitoring

5.8.1.2.2. Predictive Maintenance

5.8.1.2.3. Fuel Management

5.8.1.2.4. Driver Behavior Monitoring

5.8.1.2.5. Route Optimization

5.8.1.2.6. Fleet Analytics

5.8.1.2.7. Remote Diagnostics

5.8.1.2.8. Asset Tracking

5.8.1.3. United States Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

5.8.1.3.1. Cloud

5.8.1.3.2. On Premise

5.8.1.4. United States Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

5.8.1.4.1. Passenger Vehicles

5.8.1.4.2. Light Commercial Vehicles

5.8.1.4.3. Heavy Commercial Vehicles

5.8.1.5. United States Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

5.8.1.5.1. Embedded Systems

5.8.1.5.2. Tethered Systems

5.8.1.5.3. Integrated Systems

5.8.1.6. United States Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

5.8.1.6.1. Large Enterprises

5.8.1.6.2. Small And Medium Enterprises

5.8.1.7. United States Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

5.8.1.7.1. Logistics And Transportation

5.8.1.7.2. Automotive

5.8.1.7.3. Oil And Gas

5.8.1.7.4. Mining

5.8.1.7.5. Construction

5.8.1.7.6. Utilities

5.8.1.7.7. Public Transportation

5.8.1.7.8. Government Fleet

5.8.2. Canada

5.8.2.1. Canada Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

5.8.2.1.1. Hardware

5.8.2.1.2. Software

5.8.2.1.3. Services

5.8.2.2. Canada Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

5.8.2.2.1. Fleet Tracking And Monitoring

5.8.2.2.2. Predictive Maintenance

5.8.2.2.3. Fuel Management

5.8.2.2.4. Driver Behavior Monitoring

5.8.2.2.5. Route Optimization

5.8.2.2.6. Fleet Analytics

5.8.2.2.7. Remote Diagnostics

5.8.2.2.8. Asset Tracking

5.8.2.3. Canada Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

5.8.2.3.1. Cloud

5.8.2.3.2. On Premise

5.8.2.4. Canada Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

5.8.2.4.1. Passenger Vehicles

5.8.2.4.2. Light Commercial Vehicles

5.8.2.4.3. Heavy Commercial Vehicles

5.8.2.5. Canada Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

5.8.2.5.1. Embedded Systems

5.8.2.5.2. Tethered Systems

5.8.2.5.3. Integrated Systems

5.8.2.6. Canada Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

5.8.2.6.1. Large Enterprises

5.8.2.6.2. Small And Medium Enterprises

5.8.2.7. Canada Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

5.8.2.7.1. Logistics And Transportation

5.8.2.7.2. Automotive

5.8.2.7.3. Oil And Gas

5.8.2.7.4. Mining

5.8.2.7.5. Construction

5.8.2.7.6. Utilities

5.8.2.7.7. Public Transportation

5.8.2.7.8. Government Fleet

5.8.3. Mexico

5.8.3.1. Mexico Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

5.8.3.1.1. Hardware

5.8.3.1.2. Software

5.8.3.1.3. Services

5.8.3.2. Mexico Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

5.8.3.2.1. Fleet Tracking And Monitoring

5.8.3.2.2. Predictive Maintenance

5.8.3.2.3. Fuel Management

5.8.3.2.4. Driver Behavior Monitoring

5.8.3.2.5. Route Optimization

5.8.3.2.6. Fleet Analytics

5.8.3.2.7. Remote Diagnostics

5.8.3.2.8. Asset Tracking

5.8.3.3. Mexico Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

5.8.3.3.1. Cloud

5.8.3.3.2. On Premise

5.8.3.4. Mexico Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

5.8.3.4.1. Passenger Vehicles

5.8.3.4.2. Light Commercial Vehicles

5.8.3.4.3. Heavy Commercial Vehicles

5.8.3.5. Mexico Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

5.8.3.5.1. Embedded Systems

5.8.3.5.2. Tethered Systems

5.8.3.5.3. Integrated Systems

5.8.3.6. Mexico Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

5.8.3.6.1. Large Enterprises

5.8.3.6.2. Small And Medium Enterprises

5.8.3.7. Mexico Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

5.8.3.7.1. Logistics And Transportation

5.8.3.7.2. Automotive

5.8.3.7.3. Oil And Gas

5.8.3.7.4. Mining

5.8.3.7.5. Construction

5.8.3.7.6. Utilities

5.8.3.7.7. Public Transportation

5.8.3.7.8. Government Fleet

6. Europe Smart Fleet Management Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

6.1. Europe Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.2. Europe Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.3. Europe Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.4. Europe Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.5. Europe Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.6. Europe Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.7. Europe Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8. Europe Smart Fleet Management Market Size and Forecast, by Country (2025-2032)

6.8.1. United Kingdom

6.8.1.1. United Kingdom Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.1.2. United Kingdom Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.1.3. United Kingdom Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.1.4. United Kingdom Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.1.5. United Kingdom Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.1.6. United Kingdom Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.1.7. United Kingdom Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8.2. France

6.8.2.1. France Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.2.2. France Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.2.3. France Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.2.4. France Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.2.5. France Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.2.6. France Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.2.7. France Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8.3. Germany

6.8.3.1. Germany Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.3.2. Germany Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.3.3. Germany Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.3.4. Germany Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.3.5. Germany Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.3.6. Germany Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.3.7. Germany Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8.4. Italy

6.8.4.1. Italy Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.4.2. Italy Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.4.3. Italy Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.4.4. Italy Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.4.5. Italy Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.4.6. Italy Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.4.7. Italy Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8.5. Spain

6.8.5.1. Spain Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.5.2. Spain Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.5.3. Spain Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.5.4. Spain Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.5.5. Spain Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.5.6. Spain Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.5.7. Spain Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8.6. Sweden

6.8.6.1. Sweden Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.6.2. Sweden Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.6.3. Sweden Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.6.4. Sweden Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.6.5. Sweden Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.6.6. Sweden Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.6.7. Sweden Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8.7. Austria

6.8.7.1. Austria Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.7.2. Austria Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.7.3. Austria Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.7.4. Austria Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.7.5. Austria Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.7.6. Austria Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.7.7. Austria Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

6.8.8. Rest of Europe

6.8.8.1. Rest of Europe Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

6.8.8.2. Rest of Europe Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

6.8.8.3. Rest of Europe Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

6.8.8.4. Rest of Europe Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

6.8.8.5. Rest of Europe Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

6.8.8.6. Rest of Europe Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

6.8.8.7. Rest of Europe Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7. Asia Pacific Smart Fleet Management Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

7.1. Asia Pacific Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.2. Asia Pacific Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.3. Asia Pacific Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.4. Asia Pacific Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.5. Asia Pacific Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.6. Asia Pacific Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.7. Asia Pacific Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8. Asia Pacific Smart Fleet Management Market Size and Forecast, by Country (2025-2032)

7.8.1. China

7.8.1.1. China Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.1.2. China Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.1.3. China Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.1.4. China Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.1.5. China Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.1.6. China Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.1.7. China Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.2. S Korea

7.8.2.1. S Korea Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.2.2. S Korea Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.2.3. S Korea Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.2.4. S Korea Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.2.5. S Korea Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.2.6. S Korea Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.2.7. S Korea Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.3. Japan

7.8.3.1. Japan Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.3.2. Japan Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.3.3. Japan Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.3.4. Japan Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.3.5. Japan Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.3.6. Japan Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.3.7. Japan Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.4. India

7.8.4.1. India Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.4.2. India Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.4.3. India Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.4.4. India Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.4.5. India Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.4.6. India Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.4.7. India Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.5. Australia

7.8.5.1. Australia Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.5.2. Australia Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.5.3. Australia Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.5.4. Australia Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.5.5. Australia Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.5.6. Australia Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.5.7. Australia Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.6. Indonesia

7.8.6.1. Indonesia Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.6.2. Indonesia Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.6.3. Indonesia Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.6.4. Indonesia Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.6.5. Indonesia Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.6.6. Indonesia Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.6.7. Indonesia Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.7. Malaysia

7.8.7.1. Malaysia Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.7.2. Malaysia Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.7.3. Malaysia Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.7.4. Malaysia Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.7.5. Malaysia Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.7.6. Malaysia Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.7.7. Malaysia Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.8. Vietnam

7.8.8.1. Vietnam Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.8.2. Vietnam Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.8.3. Vietnam Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.8.4. Vietnam Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.8.5. Vietnam Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.8.6. Vietnam Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.8.7. Vietnam Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.9. Taiwan

7.8.9.1. Taiwan Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.9.2. Taiwan Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.9.3. Taiwan Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.9.4. Taiwan Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.9.5. Taiwan Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.9.6. Taiwan Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.9.7. Taiwan Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

7.8.10. Rest of Asia Pacific

7.8.10.1. Rest of Asia Pacific Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

7.8.10.2. Rest of Asia Pacific Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

7.8.10.3. Rest of Asia Pacific Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

7.8.10.4. Rest of Asia Pacific Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

7.8.10.5. Rest of Asia Pacific Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

7.8.10.6. Rest of Asia Pacific Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

7.8.10.7. Rest of Asia Pacific Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

8. Middle East and Africa Smart Fleet Management Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

8.1. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

8.2. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

8.3. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

8.4. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

8.5. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

8.6. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

8.7. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

8.8. Middle East and Africa Smart Fleet Management Market Size and Forecast, by Country (2025-2032)

8.8.1. South Africa

8.8.1.1. South Africa Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

8.8.1.2. South Africa Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

8.8.1.3. South Africa Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

8.8.1.4. South Africa Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

8.8.1.5. South Africa Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

8.8.1.6. South Africa Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

8.8.1.7. South Africa Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

8.8.2. GCC

8.8.2.1. GCC Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

8.8.2.2. GCC Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

8.8.2.3. GCC Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

8.8.2.4. GCC Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

8.8.2.5. GCC Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

8.8.2.6. GCC Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

8.8.2.7. GCC Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

8.8.3. Nigeria

8.8.3.1. Nigeria Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

8.8.3.2. Nigeria Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

8.8.3.3. Nigeria Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

8.8.3.4. Nigeria Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

8.8.3.5. Nigeria Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

8.8.3.6. Nigeria Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

8.8.3.7. Nigeria Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

8.8.4. Rest of ME&A

8.8.4.1. Rest of ME&A Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

8.8.4.2. Rest of ME&A Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

8.8.4.3. Rest of ME&A Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

8.8.4.4. Rest of ME&A Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

8.8.4.5. Rest of ME&A Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

8.8.4.6. Rest of ME&A Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

8.8.4.7. Rest of ME&A Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

9. South America Smart Fleet Management Market Size and Forecast by Segmentation (in USD Billion) 2025-2032

9.1. South America Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

9.2. South America Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

9.3. South America Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

9.4. South America Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

9.5. South America Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

9.6. South America Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

9.7. South America Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

9.8. South America Smart Fleet Management Market Size and Forecast, by Country (2025-2032)

9.8.1. Brazil

9.8.1.1. Brazil Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

9.8.1.2. Brazil Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

9.8.1.3. Brazil Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

9.8.1.4. Brazil Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

9.8.1.5. Brazil Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

9.8.1.6. Brazil Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

9.8.1.7. Brazil Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

9.8.2. Argentina

9.8.2.1. Argentina Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

9.8.2.2. Argentina Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

9.8.2.3. Argentina Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

9.8.2.4. Argentina Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

9.8.2.5. Argentina Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

9.8.2.6. Argentina Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

9.8.2.7. Argentina Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

9.8.3. Rest Of South America

9.8.3.1. Rest Of South America Smart Fleet Management Market Size and Forecast, by Component (2025-2032)

9.8.3.2. Rest Of South America Smart Fleet Management Market Size and Forecast, by Solution (2025-2032)

9.8.3.3. Rest Of South America Smart Fleet Management Market Size and Forecast, by Deployment Mode (2025-2032)

9.8.3.4. Rest Of South America Smart Fleet Management Market Size and Forecast, by Fleet Type (2025-2032)

9.8.3.5. Rest Of South America Smart Fleet Management Market Size and Forecast, by Vehicle Connectivity (2025-2032)

9.8.3.6. Rest Of South America Smart Fleet Management Market Size and Forecast, by Organization Size (2025-2032)

9.8.3.7. Rest Of South America Smart Fleet Management Market Size and Forecast, by Application (2025-2032)

10. Company Profile: Key Players

10.1. Verizon Connect

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Scale of Operation (small, medium, and large)

10.1.7. Details on Partnership

10.1.8. Regulatory Accreditations and Certifications Received by Them

10.1.9. Awards Received by the Firm

10.1.10. Recent Developments

10.2. Geotab Inc.

10.3. Trimble Inc.

10.4. Samsara Inc.

10.5. Teletrac Navman

10.6. Omnitracs LLC

10.7. Fleet Complete

10.8. TomTom Telematics

10.9. Mix Telematics

10.10. AT&T Inc.

10.11. Cisco Systems Inc.

10.12. IBM Corporation

10.13. Oracle Corporation

10.14. Siemens AG

10.15. Bosch Mobility Solutions

10.16. Continental AG

10.17. Huawei Technologies Co. Ltd.

10.18. CalAmp Corporation

10.19. Zonar Systems Inc.

10.20. Inseego Corp.

10.21. Octo Telematics

10.22. Masternaut

10.23. Azuga Inc.

10.24. Fleetmatics Group PLC

10.25. Spireon Inc.

11. Key Findings

12. Industry Recommendations

13. Smart Fleet Management Market: Research Methodology

14. Terms and Glossary

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report