Microfluidics Market by Product Type, Material, Application, End-User, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

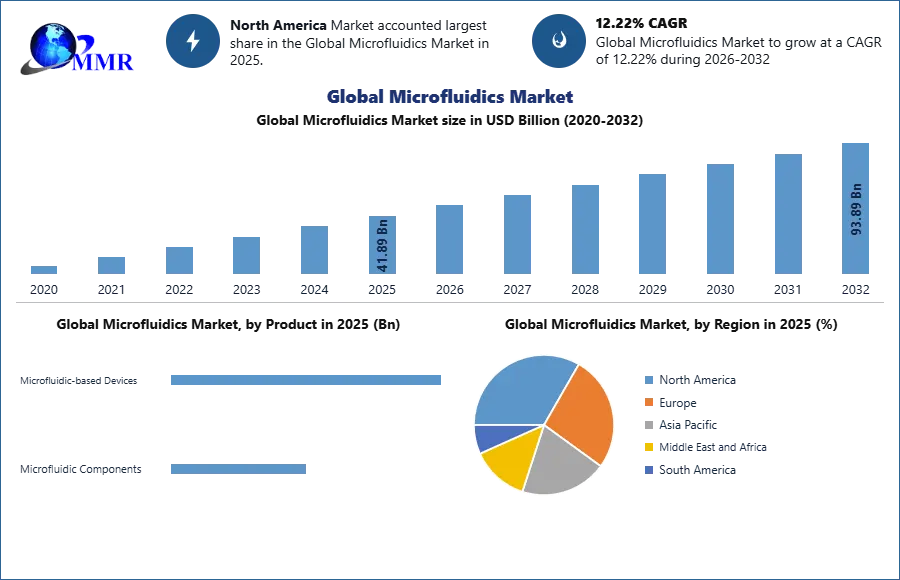

The Microfluidics Market size was valued at USD 41.89 Billion in 2025 and the total Microfluidics revenue is expected to grow at a CAGR of 12.2% from 2025 to 2032, reaching nearly USD 93.89 Billion.

Microfluidics is a technology that offers an excellent toolkit for handling and manipulating fluid samples, suspended cells, and particles. The use of Microfluidics in industries such as pharmaceuticals and healthcare are grown in recent years. These Microfluidics devices offer significant advantages over traditional diagnostic methods in terms of accuracy, sensitivity, and specificity. It can be used for point-of-care (POC) testing, which is a major factor driving the Microfluidics market.

Every year, several innovative microfluidic methods for cell observation and manipulation, organ mimicking, biomarker detection, and many more fields of study are reported. The increased accessibility allows a growing number of researchers to design, produce, and use microfluidic devices that shows the potential for widespread applications all across life sciences.

Sustained development of new microfluidics technologies such as 3-D printed microfluidics, paper-based microfluidics, and droplet-based microfluidics is likely to generate significant market growth potential for the microfluidics market throughout the forecast period. The integration of artificial intelligence (Al) and machine learning (ML) in microfluidic devices are gaining traction since these technologies may be utilized for real-time analysis and decision-making in a wide range of applications. However, the high cost of Microfluidics devices is a restraint for the market.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Microfluidics Market Dynamics:

Microfluidic methods accelerate the vaccine R&D and its production

Global demand for vaccines is increasing rapidly, with >25% annual growth. The advent of new viruses such as Ebola and the COVID-19 pandemic has resulted in more demand and increased pressure to reduce development time and cost. Microfluidic technology has the key to reducing lead times, enhancing efficiency and quality, and lowering development costs.

Microfluidic tools can be used at all stages of the development and production cycle from disease analysis to optimization of production protocols, from high throughput antibody screening to vaccine encapsulation, and from adjuvant development to directed evolution of the yeast and bacteria used in vaccine biomanufacturing. DNA vaccines deliver to the patient a specific viral gene in order to generate an immune response. Bacteria may be individually encapsulated in droplets, screened for performance, and sorted using FACS to identify ideal strains using microfluidic methods.

Researchers at the University of Illinois Chicago have just invented a new continuous-flow microfluidic device that will assist in the research and study of pharmaceutical compounds and their crystalline forms and structures, which are important factors in determining medication stability. This innovative technology will assist researchers as well as pharmaceutical corporations in evaluating data more quickly and significantly accelerating the drug development process.

Technologically advanced systems such as implantable drug delivery systems can provide significant market growth

The use of microfluidic devices for drug administration has some advantages, such as the reduction of both pain and the risk of side effects. Microfluidics brings further improvements in cost, user-friendliness, safety, and portability. Technologically advanced systems such as implanted drug delivery systems may create considerable growth opportunities for market participants, as microfluidics technology allows the manufacture of portable and wearable products that can assure accurate and consistent drug administration. Insulin pumps are the most common microfluidics-based medication delivery systems, and various related technologies for micropumps are now under development. These devices are likely to be available on a larger scale over the next two to three years.

The major advantages of microfluidics, such as regulated medication release and biocompatibility are likely to provide significant opportunities for technological adoption. some researchers have succeeded in building microfluidic devices which can mimic entire biological systems, such as human organs and arteries. These microfluidics devices replicate the in vivo organs’ microenvironments and provide a low-cost preclinical test platform for research.

The technique that allows this is called compartmentalization and multicompartment microfluidic-based devices can therefore be used to enhance the drug development process. Aside from portable, wearable, and implantable technologies, researchers are working on intelligent pills and subcutaneous patches for controlled release. The release can be better regulated by using micro technologies to create diffusion barriers. Pharmaceutical and medical device companies are investing extensively in creating novel drug delivery systems using microfluidics in order to profit from this market's rapid growth.

Growing demand for faster and more accurate point-of-care testing.

Point-of-care diagnostics is an important part of healthcare, particularly in disease diagnosis. Microfluidics also known as Lab-on-Chip [LOC] devices for biosensors and diagnostics has proven to be a robust and optimum medical technology as compared to normal laboratory-based testing, particularly in demanding and resource-constrained environments. Microfluidics' user-friendliness and ease of result interpretation have the potential to be an appealing alternative in contexts where experienced healthcare staff are few.

Advantages such as portability, ease of access, ease of operation, and reduced process time compared to traditional methods of diagnosis are driving widespread adoption of microfluidic POC testing, and this trend is expected to continue over the forecast period. Market players have extended their diagnostic platforms to include point-of-care testing using microfluidic devices. The rising prevalence of lifestyle-related and viral infections increased preference for home healthcare POC testing, and use in hospitals during medical emergencies for rapid diagnosis and decision-making are expected to drive market revenue growth.

Low adoption of Microfluidics in poor nations due to its high R&D costs

The high cost of R&D and manufacturing of microfluidic devices is the main obstacle to mass production. Current stringent regulatory rules such as the Food and Drug Administration (FDA) licensing procedure for medical devices have a significant impact on drug delivery, In-vitro Diagnostics (IVD), and pharmaceutical sectors. Furthermore, uncertainty in the clearance process has a significant impact on product profitability. Access to advanced healthcare is limited in certain emerging and low-income countries. Other factors that are expected to hamper the Microfluidics market growth include a lack of understanding about disease prevention, limited access to healthcare information, and a shortage of sufficient healthcare services.

Microfluidics Market Segment Analysis:

Based on Product Type, Microfluidic-based devices hold the largest market share in the microfluidics market in 2025, due to their wide range of applications across various industries, including healthcare, pharmaceuticals, biotechnology, and diagnostics. These devices enable precise manipulation of small volumes of fluids, leading to enhanced sensitivity, accuracy, and faster results, which are critical for applications such as point-of-care diagnostics, drug development, and lab-on-a-chip technologies. In healthcare, the growing demand for rapid and minimally invasive diagnostic tests, coupled with advancements in personalized medicine, drives the adoption of microfluidic devices. Additionally, the device's ability to integrate multiple laboratory processes into a single chip reduces costs, space, and time, making them highly attractive to researchers and healthcare providers. Their versatile nature, combined with technological advancements and the growing need for efficient and scalable solutions, solidifies their dominant position in the microfluidics market.

By Application, the lab-on-a-chip segment dominated the market and accounted for the largest revenue share of 39.5% in 2025. Lab-on-a-chip segment provides high speed for detection along with maintaining the required sensitivity during the DNA or RNA amplification and detection procedures which makes it suitable for molecular biology applications.

By Material, The Polydimethylsiloxane (PDMS) segment dominated the microfluidics market and accounted for the largest revenue share of 36.7% in 2025. Polydimethylsiloxane has grown in popularity among other polymers, particularly in microfluidic devices with rapid prototyping. This is due to the great acceptability of these polymers among academic specialists, owing to the material's simplicity of production and cost. In addition, unique PDMS surface modifications are being launched into the market to address issues connected with PDMS hydrophobicity. Hydrophobicity makes operating microchannels in aqueous solutions difficult due to the fact that such analytes become adsorbed on the PDMS surface, interfering with the analysis.

By End-User, the in-vitro diagnostics and life science research segment together hold over 59% of the market in 2024 and this trend is expected to continue during the forecast period. The market growth can be attributed to the increasing adoption of testing due to the pandemic. The development of automated In-vitro Diagnostics systems for laboratories and hospitals to provide efficient, accurate, and error-free diagnoses is expected to fuel the market growth during the forecast period.

The growing number of an experiment carried out in life science research using microfluidics is increasing. Aside from that, the demand for in-vitro diagnostics is also increasing owing to the rising diseases all over the world.

Microfluidics Market Regional Insights

In 2025, North America, dominated the Microfluidics market . Research institutions are actively involved in the development of innovative microfluidic devices, which are expected to maintain regional dominance in the worldwide market. The United States emerged as a significant contributor to the region's dominance. In addition to well-established firms, the country is home to a number of new microfluidics companies.

Microfluidics is a corporation established in the United States that provides unique microfluidics technology, particularly microfluidizers. This technology is used in the production of high-shear fluid processors that produce efficient cell disruption, nanoemulsions, and particle size reduction. The high frequency and increasing prevalence of various diseases, as well as government funding for research and clinical testing by various organizations in the United States, growing R&D activities, and considerable development in the pharmaceutical and biotechnology industries are expected to increase market demand during the forecast period.The Europe Microfluidics Market is experiencing steady growth due to strong biotechnology research, advanced healthcare infrastructure, and increasing demand for rapid diagnostic technologies. Countries such as Germany, the UK, and France lead the region, while Europe accounts for roughly 20–30% of the global microfluidics market share

The Asia Pacific market had a moderate revenue share in 2025. Rising demand from the biomedical and pharmaceutical industries, as well as PoCT, growing frequency of chronic diseases, and rising R&D investments, particularly in Singapore are some of the primary drivers driving the Microfluidics market growth. Various technologies for 30 printing microfluidic devices with fluid management and operating components are being developed and tested in the region.

Singapore University of Technology and Design developed the approach to allow for the rapid development of microfluidics for LOC applications in chemical testing and cell research. China, Japan, and India account for the majority of revenue in the Asia-Pacific microfluidics market, and this trend is expected to continue over the forecast period.

The microfluidics market in China is expected to develop at a CAGR of 18.7% over the forecast period. The Chinese government has been vocal in its support for increased infrastructure and intellectual property rights owners. As a result, the microfluidics industry is expected to grow significantly. The growing need for healthcare services is also likely to propel the microfluidics market in the region to new heights in the coming years.

The Microfluidics Market report forecasts revenue growth at global, and country levels and provides an analysis of the latest industry trends in each of the sub-segments during the forecast period. MMR has segmented the global Microfluidics Market report based on Component, Deployment Mode, Organization Size, End-User, and region.

The report contains strategic profiling of top key players in the market, a wide-ranging analysis of their core competencies, and their strategies like new product launches, growths, agreements, joint ventures, partnerships, and acquisitions that apply to the businesses. Our team of analysts can also provide you with data in excel files and pivot tables or can assist you in creating presentations from the data sets available in the report.

Microfluidics Market Recent Development

- December 2024 – Dapu Biotechnology (DPBIO) and Leveragen

Dapu Biotechnology (DPBIO) partnered with Leveragen to accelerate antibody discovery using DPBIO’s Cytospark droplet microfluidics platform. The technology enables rapid screening of millions of single cells, reducing antibody discovery timelines from several months to approximately 1–2 days, thereby supporting faster development of advanced antibody-based therapeutics for complex disease targets. - November 2024 – Parallel Fluidics

Parallel Fluidics raised USD 7 million in seed funding to expand its microfluidic manufacturing platform for life science applications. The investment will support the development of scalable microfluidic devices used in diagnostics, drug discovery, and precision medicine, helping reduce development time and manufacturing costs for advanced biomedical technologies. - July 2024 – Bio-Rad Laboratories

Bio-Rad Laboratories introduced Celselect Slides 2.0, an upgraded microfluidics-based platform designed to improve the capture and analysis of circulating tumor cells (CTCs). The new system enhances throughput and recovery rates, supporting more efficient cancer research and enabling improved detection of rare tumor cells in clinical studies.

Microfluidics Industry Ecosystem

Microfluidics Market Scope: Inquire before buying

| Global Microfluidics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 41.89 USD Billion |

| Forecast Period 2026-2032 CAGR: | 12.22% | Market Size in 2032: | 93.89 USD Billion |

| Segments Covered: | by Product | Microfluidic-based Devices Microfluidic Components Chips Micro-pumps Sensors Others |

|

| by Technology | Lab-on-a-chip Organ-on-a-chip Continuous Flow Microfluidics Optofluidics & Microfluidics Acoustofluidics & Microfluidics Electrophoresis & Microfluidics |

||

| by Material | Silicon Glass Polymer PDMS Others |

||

| by Application | Medical Pharmaceuticals Medical Devices In-vitro Diagnostics Others Non-medical |

||

Microfluidics Market, by region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Microfluidics Market, Key Players are

- Fluigent

- Micronit Microtechnologies

- Elveflow

- uFluidix Inc.

- BioFluidix GmbH

- Microfluidic ChipShop GmbH

- ThinXXS Microtechnology AG

- ALine Inc.

- Parallel Fluidics Inc.

- Blacktrace Holdings Ltd.

- Sphere Fluidics Limited

- TTP plc (TTP Group)

- Dolomite Bio

- Cellix Ltd.

- Darwin Microfluidics

- MicruX Technologies

- ChipShop (Microfluidic ChipShop)

- Parker Hannifin Corporation

- IDEX Health & Science

- SMC Corporation

- Camozzi Automation S.p.A.

- Aignep S.p.A.

- Zeon Corporation

- Nordson Corporation

- Hamilton Company

- Standard BioTools Inc. (Fluidigm)

- 10x Genomics

- Fluxergy LLC

- Berghof Automation GmbH