Microfinance Market Size by Type, Loan Type, End User, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

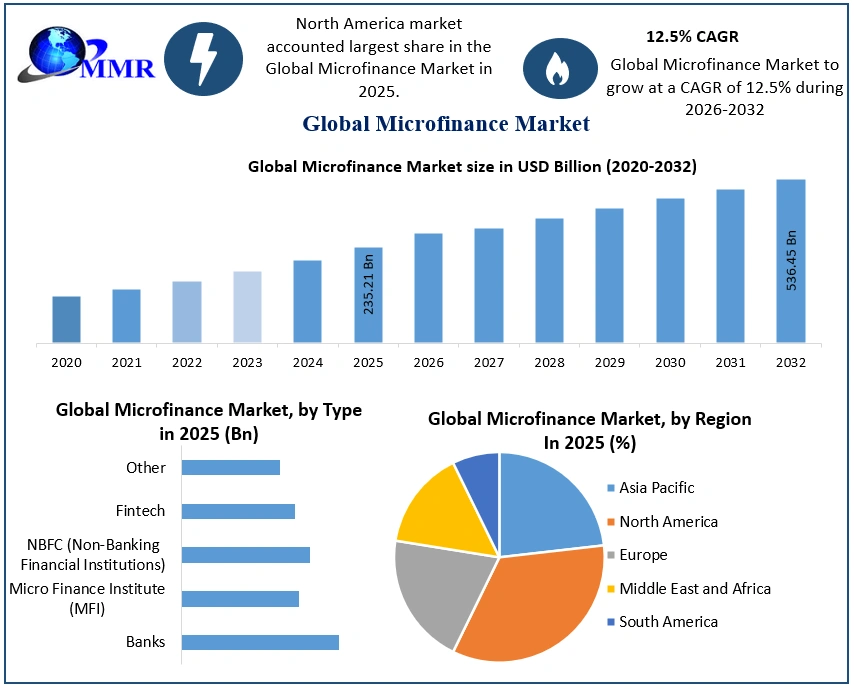

The Microfinance Market size was valued at USD 235.21 Billion in 2025 and the total Microfinance revenue is expected to grow at a CAGR of 12.5% from 2025 to 2032, reaching nearly USD 536.45 Billion by 2032.

Microfinance Market Overview

The report covers a detailed analysis of the global microfinance market, including market size, growth prospects, and major players. Also, in-depth examination of the key trends shaping the microfinance sector, such as technological integration, product diversification, social impact investing, and client-centric approaches. The need for financial inclusion is growing, especially in developing nations where a sizable fraction of the populace lacks access to banking. Around 1.4 billion adults worldwide do not have access to traditional banking services, according to the World Bank, which means that microfinance institutions (MFIs) have a huge market opportunity. The demand is being driven by initiatives that support financial inclusion as more individuals become aware of the advantages of formal financial products.

Advancements in technology, such as the widespread use of mobile banking and financial technology (fintech), are making unbanked people more accessible, particularly in rural areas. By streamlining loan processing, repayments, and other financial activities, mobile technology lowers expenses and increases reach. Additionally, MFIs' growth is being aided by a favorable regulatory climate that is defined by expedited licensing processes and lowered capital requirements. To meet changing customer needs, MFIs are growing the range of products they offer beyond traditional microloans to include savings accounts, money transfers, insurance, and leasing services. Also, because of the microfinance industry's potential for both financial rewards and social effects, investors are becoming more interested in it, which gives MFIs more funding for service improvement and growth.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

There are several ways for investors to interact with the microfinance industry. Common ways include participating in microfinance funds that distribute risk across a variety of portfolios, making direct investments in respectable MFIs through stock or debt instruments, or using impact investing platforms that connect investors with social entrepreneurs. Achieving a balance between financial return and effect, doing extensive due diligence on the financial health and governance of MFIs, and adopting a long-term view are all important factors to take into account because sustainable microfinance institution development takes time.

Microfinance Market Dynamics

Financial Inclusion Initiatives

Access to savings accounts and loans allows low-income people to invest in education, health, and small companies, thereby breaking the poverty cycle. Financial inclusion promotes entrepreneurship and helps small and medium-sized businesses (SMEs) develop, which in turn fosters economic growth. Broader financial inclusion also improves overall financial stability by lowering reliance on erratic and dangerous unregulated financial channels. The increasing awareness of financial inclusion initiatives and the lowering of obstacles to formal financial services are driving a strong demand for microfinance services. Demand for insurance, savings products, and small loans has increased significantly as more low-income people and SMEs actively look for them. Governments work with microfinance institutions (MFIs) to lower lending risks to underprivileged people by establishing credit bureaus, funding, and favorable legislation that promotes policy. Advancing the spread of microfinance, technology advancements in mobile banking and fintech allow MFIs to reach rural and remote locations at a reasonable cost.

The rise of mobile banking and financial technology

The rise of mobile banking and financial technology (fintech) presents a transformative opportunity for the microfinance market, particularly in expanding outreach and reducing costs. Mobile technology enables microfinance institutions (MFIs) to reach the unbanked by providing financial services via mobile phones, hence removing the need for physical branches. This improves accessibility, especially for isolated locations or communities without established financial infrastructure. In addition, when compared to conventional branch-based models, mobile solutions significantly cut MFIs' operating expenses, which in turn resulted in reduced borrower interest rates and higher profitability. Also, mobile platforms provide faster loan processing, repayments, and transactions, improving both operational efficiency and client experience. MFIs are expected to improve risk assessment, offer individualized products, and promote financial inclusion by gaining important insights into client behavior and creditworthiness through mobile data analytics.

Risk Management

Microfinance institutions (MFIs) face numerous risks, including credit, operational, liquidity, and external hazards. Credit risk is increased when serving clients with short credit histories and no traditional collateral, which exacerbates the effects of defaults on the MFI's portfolio and financial stability. Operational risk exposes MFIs to financial losses and reputational damage due to operational issues in remote areas, such as infrastructure limits and potential fraud threats. MFIs that rely on outside finance are vulnerable to funding changes, which are expected to impact loan disbursements and operational costs. It is known as liquidity risk. Additional dangers to operations and market stability include external issues including political unpredictability, economic downturns, and natural disasters. Microfinance institutions (MFIs) face challenges in attracting necessary funds for growth because of increased risks, which has resulted in a loss in investor confidence. Due to their higher risk profiles, MFIs frequently have to charge their clients higher interest rates, which makes it harder for the needy borrowers they are trying to help to receive credit. Inadequate risk management can lead to operational inefficiencies, which impede the ability to scale effectively and affect profitability in general. When the microfinance industry faces high rates of delinquency and systemic concerns, it leads to wider market instability and an economic downturn, which poses difficulties for microfinance institutions (MFIs) and the communities they serve.

Microfinance Market Segment Analysis

By Type: The microfinance market consists of various providers, including established banks extending their reach through structured loan products and partnerships with MFIs, specialized Micro Finance Institutes (MFIs) prioritizing social impact via group lending, adaptable Non-Banking Financial Institutions (NBFCs) offering flexible services, technology-driven Fintechs enhancing accessibility with digital solutions, and various other entities like cooperatives and credit unions serving specific community needs.

By Loan Type: Microfinance loans are categorized based on their purpose. Microfinance caters to varied financial needs through income-generating loans bolstering entrepreneurship, consumption loans addressing immediate household expenses, emergency loans providing crucial support during crises, agricultural loans empowering farmers, and a range of other specialized products like housing or vocational training loans. Emergency loans provide quick financial relief for unforeseen crises, ensuring borrowers have access to urgent funds. Agricultural loans support farmers by financing seeds, equipment, and livestock, enhancing productivity and rural development. Other loan types may include specialized financial products tailored to unique borrower needs.

By End User: Microfinance primarily serves diverse borrower groups. Individual borrowers, often from low-income backgrounds, seek small loans for personal or business needs, including individual borrowers seeking small loans for personal needs, Micro, Small, and Medium Enterprises (MSMEs) requiring capital for growth, women entrepreneurs driving economic development, and farmers and rural communities fostering agricultural productivity and economic diversification.

Microfinance Market Regional Analysis

The North America in the microfinance market, demand is increasing, particularly when compared to industrialized economies. Microfinance, despite its modest scope, is essential to the uplift of certain communities in the area. It is remarkable for its focus on entrepreneurship and inclusivity, to bridge wealth disparities and raise upward mobility through assistance for small enterprises and the advancement of financial inclusion. The microfinance environment in North America has changed recently. As key stakeholders, Community Development Financial Institutions (CDFIs) provide loans and financial services to marginalized populations. Peer-to-peer micro lending has also been made easier by the emergence of Internet lending services like Kiva, which link borrowers and lenders both locally and globally.

The United States dominates North American microfinance, with a larger sector than Canada. Numerous reasons contribute to its strength, such as the country's bigger population and the variety of localities facing varied degrees of financial need. Through programs like the CDFI Fund, which has invested over $5 billion into Community Development Financial Institutions (CDFIs) since 1994, the US has shown a significant commitment to microfinance. CDFIs support a variety of projects, from small businesses to affordable housing and community development. Also, the Association for Enterprise Opportunity (AEO) reports that microloans in the US, which have an average value of $13,100, have greatly boosted entrepreneurship, with 88% of clients using the money to launch or grow their enterprises. Additionally, government support through Small Business Administration (SBA) programs further supports microfinance efforts, underscoring the United States' leading role in fostering financial inclusion and economic empowerment within the region.

Microfinance Market Competitive Landscape

The microfinance industry has seen a notable upsurge in creative methods in recent years. A significant focus on mobile-based financial services was evident in 2023 with the release of new apps and digital platforms designed specifically with microfinance clients in mind. In 2022, MFIs and tech companies began to collaborate more frequently on fintech projects to increase operational effectiveness and reach unbanked customers. In 2021, new customized microloan products were launched to cater to certain demands including financing for schooling or climate-resilient agriculture. It indicates that the microfinance industry is always striving to be more flexible and customized. Increased rivalry among microfinance firms encourages efficiency, creativity, and cost savings for financial goods. Because of the increased competition and creative approaches used to target underprivileged people, this competitive landscape encourages more financial inclusion and outreach. Also, the growth of a varied range of market participants leads to a variety of microfinance products designed to fulfill particular requirements and financial goals. Market saturation, on the other hand, carries a possible risk of driving unsustainable practices and riskier lending because of fierce competition. Because regulators need to keep a close eye on the market to reduce risks and guarantee the integrity and sustainability of microfinance operations.

Microfinance Market Scope: Inquire Before Buying

| Global Microfinance Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 235.21 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 12.5% | Market Size in 2032: | USD 536.45 Bn. |

| Segments Covered: | by Type | Banks Micro Finance Institute (MFI) NBFC (Non-Banking Financial Institutions) Fintech Other |

|

| by Loan Type | Income-Generating Loans Consumption Loans Emergency Loans Agricultural Loans Others |

||

| by End User | Individual Borrowers Micro, Small, and Medium Enterprises (MSMEs) Women Entrepreneurs Farmers and Rural Communities |

||

Microfinance Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players in the Microfinance Market

By offering low-cost financial services to marginalized communities, microfinance companies such as Accion International and Grameen Bank are instrumental in advancing financial inclusion. These institutions leverage innovative technology, such as mobile banking and AI-driven credit scoring, to deliver scalable solutions. By partnering with fintech startups and focusing on digital-first approaches, microfinance companies ensure efficient service delivery.

1. Bandhan Bank

2. Kiva

3. BRAC

4. Bank Rakyat Indonesia

5. BSS Microfinance Private limited

6. FINCA International

7. Grameen Bank

8. Svatantra microfinance

9. Al Amana Microfinance

10. Grameen Foundation

11. Accion International

12. Opportunity International

13. Bharat Financial Inclusion Limited

14. Cashpor Micro Credit

15. Compartamos Banco

16. IndusInd Bank Limited

17. Manappuram Finance Ltd

18. Spandana

19. Women's World Banking

20. Sparkle Microfinance Bank

21. CARD MRI

22. Amret Co Ltd

23. Accion International

24. Kingdom Bank Ltd

25. Aregak UCO

26. Acleda Bank Plc

27. MIBANCO Banco de la Microempresa SA

28. Banco Caja Social

29. ProCredit Holding AG & Co.

30. BRAC Bank Ltd

FAQs:

1. What are the main products and services offered by MFIs?

Ans. MFIs offer a range of financial products and services, including microloans for business expansion or income-generating activities, savings accounts, microinsurance, and money transfer services.

2. What are the challenges facing the Microfinance market?

Ans. Challenges in the microfinance sector include sustainability concerns, over-indebtedness among clients, regulatory constraints, and limited access to funding, risk management issues, and the need for continuous innovation to meet evolving client needs.

3. What is the projected market size & and growth rate of the Microfinance Market?

Ans. The Microfinance Market size was valued at USD 235.21 Billion in 2025 and the total Microfinance revenue is expected to grow at a CAGR of 12.5% from 2025 to 2032, reaching nearly USD 536.45 Billion by 2032.

4. What segments are covered in the Microfinance Market report?

Ans. The segments covered in the Microfinance market report are type and Loan Type and End User.