Ventilator Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

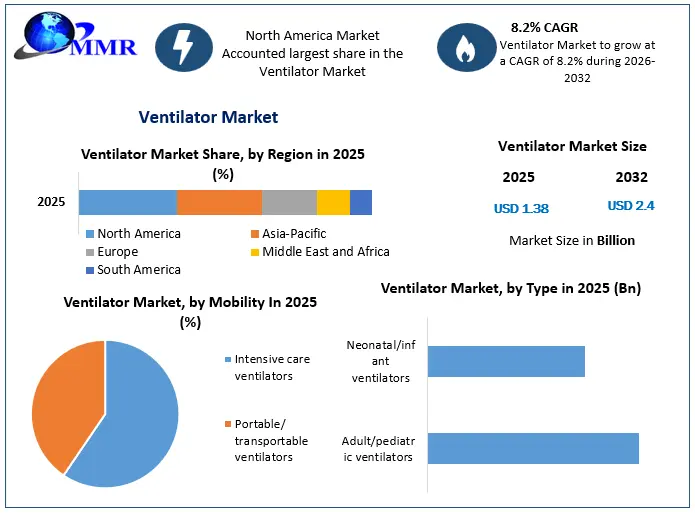

The Ventilator Market size was valued at USD 1.38 Billion in 2025 and the total Ventilator revenue is expected to grow at a CAGR of 8.2% from 2026 to 2032, reaching nearly USD 2.4 Billion.

Ventilator Market Overview

The global ventilator market comprises medical devices designed to provide mechanical respiratory support to patients experiencing acute or chronic breathing insufficiency. Ventilators are widely used across intensive care units (ICUs), emergency departments, operating rooms, neonatal and pediatric care units, ambulatory surgical centers, and home healthcare settings to manage conditions such as chronic obstructive pulmonary disease (COPD), acute respiratory distress syndrome (ARDS), pneumonia, asthma, neuromuscular disorders, and respiratory failure. The market continues to expand due to the rising prevalence of respiratory diseases, the growing geriatric population, increasing surgical procedures requiring anesthesia, and heightened preparedness for infectious disease outbreaks. Technological advancements—including portable and transport ventilators, AI-enabled ventilation management, non-invasive ventilation systems, cloud-connected monitoring platforms, and smart alarm integration—are enhancing patient outcomes, improving clinical efficiency, and supporting broader adoption across healthcare facilities.

The Ventilator Market is expected to witness sustained growth through 2032, driven by increasing investments in healthcare infrastructure, expanding critical care capacity, and rising demand for home-based respiratory care. Digital transformation in healthcare, coupled with the integration of artificial intelligence, IoT-enabled remote patient monitoring, predictive analytics, and automated ventilation modes, is improving device performance and facilitating personalized respiratory management. Growing emphasis on energy-efficient designs, portable ventilation solutions, and advanced infection control technologies is creating new opportunities for manufacturers. Additionally, favorable reimbursement policies in developed economies, expanding access to healthcare in emerging markets, and continued innovation in battery-operated and wearable respiratory support devices are strengthening market prospects. Although high equipment costs, stringent regulatory requirements, and maintenance complexities remain notable constraints, continuous product innovation, strategic collaborations, and increasing healthcare expenditure are expected to support the long-term growth of the global ventilator market.

To know about the Research Methodology :- Request Free Sample Report

Ventilator Market Dynamics:

Rising prevalence of respiratory disorders is accelerating ventilator adoption

The increasing incidence of respiratory diseases such as chronic obstructive pulmonary disease (COPD), asthma, pneumonia, acute respiratory distress syndrome (ARDS), and sleep-related breathing disorders is significantly driving demand in the global ventilator market. The growing geriatric population, which is more susceptible to chronic respiratory conditions, is further contributing to the need for advanced respiratory support systems across hospitals and home healthcare settings. Additionally, the rising number of intensive care unit (ICU) admissions, emergency cases, and complex surgical procedures requiring mechanical ventilation has strengthened market demand. Governments and healthcare providers continue to invest in expanding critical care infrastructure and emergency preparedness following the COVID-19 pandemic, encouraging healthcare facilities to upgrade to technologically advanced ventilators featuring AI-assisted ventilation modes, remote monitoring, and automated patient management systems.

Expansion of home healthcare and smart ventilation technologies is creating new growth opportunities

Growing preference for home-based healthcare services and portable respiratory support devices is opening significant opportunities for the Ventilator Market. Manufacturers are increasingly developing compact, lightweight, battery-powered ventilators equipped with wireless connectivity, cloud-based data management, and IoT-enabled remote monitoring capabilities. Artificial intelligence and predictive analytics are improving ventilation accuracy by enabling personalized respiratory support and reducing clinician workload. Emerging economies are also investing heavily in healthcare infrastructure, increasing access to advanced respiratory care equipment. Furthermore, the integration of telemedicine platforms with ventilators and rising demand for non-invasive ventilation solutions are enabling broader adoption across home care, long-term care facilities, and ambulatory settings, creating favorable conditions for sustained market expansion.

High acquisition and maintenance costs continue to limit market penetration

Despite growing demand, the high capital investment required for advanced ventilators remains a significant challenge, particularly for small healthcare facilities and hospitals in developing economies. Premium ventilators equipped with intelligent ventilation modes, integrated monitoring systems, and advanced safety features involve substantial procurement, installation, and maintenance expenses. Regular servicing, calibration, software upgrades, and replacement of consumables further increase the total cost of ownership. Additionally, stringent regulatory approval processes, compliance with international medical device standards, and reimbursement limitations in certain regions delay product commercialization and restrict market accessibility, especially among cost-sensitive healthcare providers.

Shortage of skilled professionals and complex regulatory compliance remain major industry challenges

Effective operation of modern ventilators requires trained respiratory therapists, intensivists, anesthesiologists, and critical care professionals capable of managing sophisticated ventilation modes and patient-specific treatment protocols. Many developing countries continue to face shortages of skilled healthcare personnel, limiting optimal utilization of advanced ventilator technologies. At the same time, manufacturers must comply with evolving global regulatory frameworks, rigorous clinical validation requirements, cybersecurity standards for connected medical devices, and post-market surveillance obligations. Supply chain disruptions affecting electronic components, sensors, and semiconductor availability also create manufacturing challenges, making it difficult for companies to maintain production continuity and meet increasing global demand.

Ventilator Market Trends:

AI-powered ventilation management is improving patient outcomes -Artificial intelligence is increasingly being integrated into ventilator systems to optimize ventilation parameters based on real-time patient data. AI-assisted algorithms support predictive monitoring, automated ventilation adjustments, and personalized respiratory therapy, reducing clinician workload while improving patient safety and treatment efficiency.

Portable and transport ventilators are witnessing strong demand -Healthcare providers are increasingly adopting compact, lightweight, and battery-operated ventilators for emergency medical services, ambulances, military healthcare, disaster response, and home healthcare applications. Improvements in portability and battery life are expanding the use of ventilators beyond traditional hospital settings.

Connected ventilators with IoT-enabled remote monitoring are gaining momentum - Manufacturers are incorporating IoT connectivity, wireless communication, and cloud-based data management into ventilator systems, enabling continuous remote monitoring of patients. These digital capabilities improve clinical decision-making, facilitate tele-ICU programs, and support predictive maintenance of medical equipment.

Non-invasive ventilation technologies continue to expand across healthcare settings - Demand for non-invasive ventilators is growing due to their ability to reduce complications associated with invasive mechanical ventilation, shorten hospital stays, and improve patient comfort. These systems are increasingly used for managing COPD, obstructive sleep apnea, and other chronic respiratory disorders in both hospitals and home care environments.

Ventilator Market Segment Analysis:

Based on Mobility, the ventilator market is divided into Intensive Care Ventilators and Portable/Transportable Ventilators.

Intensive care ventilators dominated the global ventilator market in 2025 due to their widespread deployment in hospitals, intensive care units (ICUs), and emergency departments for managing critically ill patients requiring continuous respiratory support. These ventilators offer advanced ventilation modes, precise monitoring capabilities, integrated patient data management, and compatibility with hospital information systems, making them indispensable in tertiary care settings. Rising ICU admissions, increasing prevalence of chronic respiratory diseases, growing surgical procedures, and investments in critical care infrastructure continue to support segment dominance. Recent innovations, including AI-assisted ventilation algorithms, touchscreen interfaces, closed-loop ventilation systems, and cloud-enabled monitoring, have further enhanced clinical efficiency and patient outcomes.

Portable/transportable ventilators are expected to register the fastest growth during the forecast period owing to increasing demand for emergency medical services, ambulatory care, military healthcare, disaster response, and home healthcare applications. Their lightweight design, battery-operated functionality, and wireless connectivity enable respiratory support beyond conventional hospital environments. Technological advancements such as longer battery life, compact designs, IoT-enabled remote monitoring, and improved portability are accelerating adoption. Growing preference for home-based respiratory care and expanding healthcare access in emerging economies are further supporting segment growth.

Based on Type, the ventilator market is divided into Adult/Pediatric Ventilators and Neonatal/Infant Ventilators.

Adult/Pediatric ventilators accounted for the largest share of the global ventilator market in 2025, primarily driven by the high prevalence of respiratory disorders, increasing critical care admissions, rising surgical procedures, and the growing elderly population requiring mechanical ventilation. These ventilators are extensively used in hospitals, specialty clinics, and emergency care units to manage conditions such as chronic obstructive pulmonary disease (COPD), acute respiratory distress syndrome (ARDS), pneumonia, and post-operative respiratory complications. Manufacturers continue to enhance these systems through AI-powered ventilation modes, advanced monitoring capabilities, adaptive ventilation technologies, and integrated clinical decision-support tools, strengthening their adoption across healthcare facilities.

Neonatal/Infant ventilators are projected to witness the fastest growth during the forecast period due to increasing preterm births, rising incidence of neonatal respiratory distress syndrome, and expanding neonatal intensive care unit (NICU) infrastructure worldwide. Continuous advancements in gentle ventilation technologies, high-frequency ventilation, synchronized respiratory support, and non-invasive neonatal ventilation are improving survival rates and reducing ventilation-associated complications in newborns. Increasing government investments in maternal and child healthcare, along with improved access to specialized neonatal care in emerging economies, are expected to further accelerate the growth of this segment.

Ventilator Market Recent Industry Developments:

| Date | Recent Development |

| June 2026 | GE HealthCare received U.S. FDA clearance for the CARESCAPE Canvas™ Patient Monitor, designed to integrate advanced monitoring capabilities with critical care workflows, supporting ventilator management in ICUs. |

| April 2026 | Hamilton Medical introduced enhanced AI-assisted ventilation features in its HAMILTON-C6 platform to improve personalized respiratory support and reduce clinician workload. |

| October 2025 | Dräger launched the Atlan® A100 anesthesia workstation in additional global markets with enhanced ventilation technologies and digital workflow integration for operating rooms. |

| September 2025 | Mindray expanded its critical care product portfolio by introducing next-generation transport ventilators featuring intelligent monitoring and wireless connectivity for emergency and ICU applications. |

| May 2025 | Medtronic expanded the availability of its respiratory intervention technologies and advanced ventilatory support solutions across multiple international markets to strengthen critical care capabilities. |

| February 2025 | ResMed announced further integration of cloud-connected respiratory care technologies and digital health platforms to improve remote patient monitoring and home ventilation management. |

| November 2024 | Philips expanded its hospital patient monitoring ecosystem with enhanced interoperability and connected respiratory care capabilities to support critical care environments. |

| August 2024 | Fisher & Paykel Healthcare increased production capacity for respiratory care devices and consumables to address growing global demand from hospitals and home healthcare providers. |

Ventilator Market Scope: Inquire before buying

| Ventilator Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 1.38 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 8.2% | Market Size in 2032: | USD 2.4 Bn. |

| Segments Covered: | By Mobility | Intensive care ventilators Portable/ transportable ventilators |

|

| Bby Type | Adult/pediatric ventilators Neonatal/infant ventilators |

||

| By Interface | Invasive ventilation segment Non-invasive ventilation |

||

| By Mode | Combined-mode ventilation Volume-mode ventilation Pressure-mode ventilation Other ventilation modes |

||

| By End User | Hospitals & clinics Home care settings Ambulatory care centers Emergency medical services |

||

Ventilator Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Ventilator Market, Key Players are

North America

- Medtronic plc (Minneapolis, Minnesota, United States)

- GE HealthCare Technologies Inc. (Chicago, Illinois, United States)

- Zoll Medical Corporation (Chelmsford, Massachusetts, United States)

- Ventec Life Systems, Inc. (Bothell, Washington, United States)

- Philips Respironics (Murrysville, Pennsylvania, United States)

- React Health Holdings, LLC (Port Washington, New York, United States)

- Vyaire Medical, Inc. (Mettawa, Illinois, United States)

- Airon Corporation (Melbourne, Florida, United States)

- Percussionaire Corporation (Sandpoint, Idaho, United States)

Europe

- Drägerwerk AG & Co. KGaA (Lübeck, Germany)

- Getinge AB (Gothenburg, Sweden)

- Hamilton Medical AG (Bonaduz, Switzerland)

- ResMed (Dublin, Ireland)

- Löwenstein Medical Technology GmbH + Co. KG (Bad Ems, Germany)

- Weinmann Emergency Medical Technology GmbH + Co. KG (Hamburg, Germany)

- Air Liquide Medical Systems S.A. (Antony, France)

- Schiller AG (Baar, Switzerland)

- HEYER Medical AG (Bad Ems, Germany)

Asia Pacific

- Nihon Kohden Corporation (Tokyo, Japan)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (Shenzhen, China)

- Shenzhen Comen Medical Instruments Co., Ltd. (Shenzhen, China)

- BMC Medical Co., Ltd. (Beijing, China)

- Aeonmed Co., Ltd. (Beijing, China)

- Beijing Aeonmed Co., Ltd. (Beijing, China)

- Shenzhen Prunus Medical Co., Ltd. (Shenzhen, China)

- Heal Force Bio-Meditech Holdings Limited (Shanghai, China)

Latin America

Others

Frequently Asked Questions:

1. Which is the dominating market for the Ventilators in terms of the region at the end of the forecast period?

Ans. North America is the potential market for the Ventilators in terms of the region at the end of the forecast period.

2. What are the opportunities for new market entrants?

Ans. The key opportunity in the market is Technological advancements in microprocessor-controlled ventilation.

3. What is expected to drive the growth of the Ventilator Market in the forecast period?

Ans. A major driver in the Ventilator market is the Increasing number of COPD and asthma patients globally.

4. What was the Global Ventilator Market size in 2025?

Ans: The Global Ventilator Market size was USD 1.38 Billion in 2025.

5. What segments are covered in the Ventilator Market report?

Ans. The segments covered are Mobility, Type, Interface, Mode, End User, and Region.