Genome Editing Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

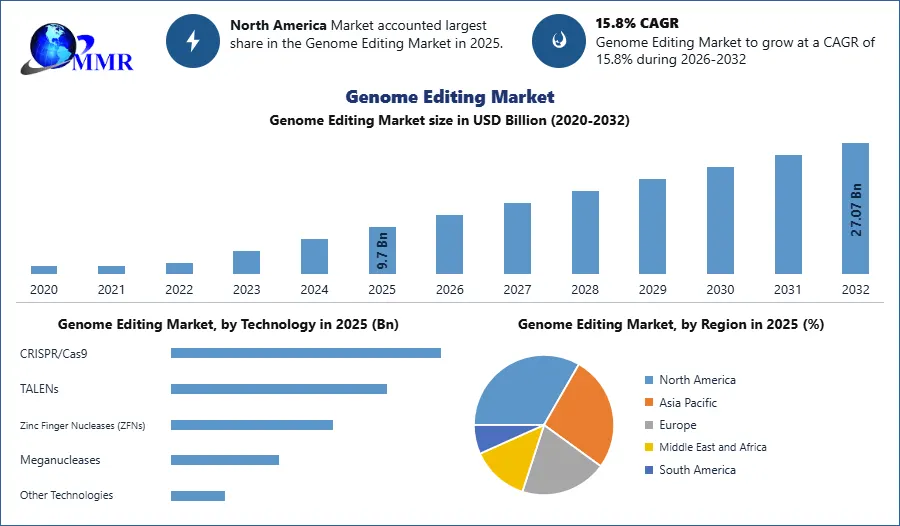

The Genome Editing Market size was valued at USD 9.7 Bn in 2025 and market revenue is growing at a CAGR of 15.8% from 2026 to 2032, reaching nearly USD 27.07 Bn by 2032.

Genome Editing Market

The extensive incorporation of CRISPR technology has helped in a transformative era in biotechnological applications within the Genome Editing Market. The precision and flexibility of genome editing technology have not only influenced research, medicine, and agriculture but have also strategically positioned the Genome Editing market for continuous growth. The development of genetically modified crops, aimed at tackling agricultural challenges, highlights the economic and environmental impact that drives the Genome Editing market forward. Amid the ongoing pandemic, the need for rapid and accurate diagnostics has emphasized the importance of CRISPR, reinforcing its role in the Genome Editing market. The dynamic interplay involving the demand for synthetic genes, CRISPR technology, government backing, and innovative applications uniquely situates the Genome Editing Market for pioneering contributions across diverse domains.

To know about the Research Methodology :- Request Free Sample Report

Genome Editing Market Dynamics:

Increased application areas of genomics boost the Market Growth

Genomics spans diverse application areas and is important in documenting human genetic disorders, drug discovery, agriculture, veterinary sciences, and forensic studies. The demand for genomics in forensics has witnessed a substantial increase, particularly with the advent of Next Generation Sequencing (NGS), amplified by specialized products from Illumina designed for forensic science applications. Unlike traditional DNA analysis used for fingerprint profiling, NGS has revolutionized forensic investigations, enabling enhanced analysis of specimens at crime scenes and extracting richer information from trace or damaged DNA samples. Expected future trends in genomic engineering extend to novel applications in marine engineering, such as the development of nutraceuticals from algae. Forensic sciences and personalized medicine are emerging as key application areas, underscoring the versatility of genomics.

The Genome Editing Market plays a dynamic role in various aspects of genomics, influencing drug discovery processes, and contributing to the diagnosis and treatment of human genetic disorders. Genome editing technologies are integral to NGS, DNA analysis, profiling, and genetic engineering in both plant and animal domains. As genomics continues to find new applications, the Genome Editing Market is poised for increased global demand in the forecast period.

Ethical and regulatory concerns limit the market growth

Ethical and regulatory concerns pose formidable challenges for the Genome Editing Market, impeding the responsible application of this transformative technology. Issues arise from potential irreversible consequences linked to editing the human germline, sparking debates on informed consent, individual autonomy, and equitable access to emerging genome editing technologies. Regulatory oversight is deemed crucial to navigate these challenges, ensuring the ethical development and application of genome editing techniques. Concerns heighten if regulatory frameworks are perceived as insufficient or lack transparency. Striking a balance between scientific progress and ethical principles is vital, particularly in a rapidly advancing genome editing market.

Cultural, religious, and dual-use considerations further complicate the ethical landscape, emphasizing the need for inclusive discussions reflecting diverse viewpoints. The prospect of dual-use, with genome editing technology serving both beneficial and harmful purposes, adds a layer of complexity. Sustained dialogue and collaboration among scientists, policymakers, and the public are essential to restrain the Genome Editing Market, establish guidelines, and navigate the multifaceted ethical challenges. This collaborative effort is imperative to ensure responsible, ethical application of genome editing technologies, considering their societal impact.

Increasing Therapeutic Applications creates lucrative growth opportunities for the market growth

Advancements in genome editing for therapeutic purposes open promising opportunities in medicine. This technology, using tools like CRISPR-Cas9, TALEN, and zinc finger nucleases, allows scientists to precisely modify genes linked to genetic disorders, paving the way for potential cures to previously untreatable diseases. In addressing conditions such as sickle cell anemia, muscular dystrophy, and cystic fibrosis, therapeutic genome editing aims to correct genetic mutations, providing relief or, in some cases, a permanent cure. Also, the application extends to cancer treatment, where precision medicine targets specific genetic mutations in tumor growth.

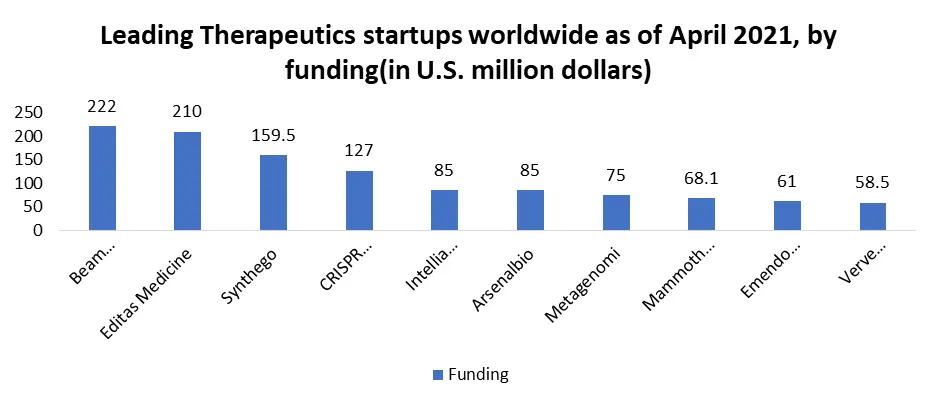

Current clinical trials examining the safety and effectiveness of therapeutic genome editing represent a significant shift from lab research to practical applications which creates lucrative growth opportunities for the Genome Editing Market growth. While challenges like off-target effects and long-term safety are being addressed, successful applications could revolutionize treatments, offering personalized and potentially curative solutions for genetic diseases and specific cancers. This evolving field holds promise for groundbreaking advancements in medical science, alleviating human suffering through targeted genetic interventions. Notably, according to the April 2021 MMR Study report, Beam Therapeutics and Editas Medicine led CRISPR startups globally in funding, indicating substantial investment in this transformative field.

Off-target belongings of CRISPR technology:

Off-target effects are a major concern regarding CRISPR-Cas9. Subsequently, Cas9 encourages double-stranded breaks, and any off-target nuclease activity causes mutations in these genes, leading to possible oncogenesis. CRISPR-Cas9 tolerates one to three mismatches in its target, which lead to off-target nuclease activity. Also, the high frequency of off-target activity (≥50%)—mutations at sites other than the intended on-target site—is a major concern. For example, CRISPR hits the tumor suppressor gene or activates the cancer-causing gene. Various companies that are planning clinical trials have faced issues because of this undesired effect. Clinical trials have been put on hold, and regulatory authorities are asserting extra research to enhance the safety of this method.

High growth forecasts for the market in emerging countries:

Emerging markets, such as the BRICS nations, are expected to offer significant opportunities for the growth of the Genome Editing Market. This is attributed to the growing R&D funding for various research organizations in these countries.

Brazil leads in industrial biotechnology, notably in cellulosic sugars and agribusiness. Biotech firms there focus on medications, diagnostics, vaccines, cell therapies, and genetic testing. In response, major players in genome editing strategically pursue partnerships and collaborations, enhancing distribution networks and manufacturing capabilities in Brazil and other emerging markets, tapping into the nation's biotech potential.

Genome Editing Market Trends:

The increasing technological advancement is driven by the rapidly evolving CRISPR technology with its wide range of applications for gene editing. This technology is mainly used to gain accessibility to genetically modified crops by delivering gene-editing reagents to the plants. This technology is also accessible for genetically modified animals with applications for agricultural purposes and biomedical fields. Gene Editing or genome editing is mainly used to change an organism’s DNA by various groups of technologies. This method allows genetic material to be replaced, added, or removed at spotted locations in the genome. Therefore, various editing approaches have been developed for their application in the industry.

Gene editing is also used for the prevention and treatment of human diseases such as cystic fibrosis, sickle cell disease, HIV infection, cancer, and others. Rising funding for genetic studies in developed regions including North America drives the gene-editing market growth over the forecast period. In the U.S., more than 20 federal agencies funded research and development government firms to produce useful materials, devices, and methods. the U.S. government funds various research firms that help in the development and manufacturing of drug discovery for various rare genetic diseases. For instance, the National Human Genome Research Institute supports research programs and projects to advance in the field of genomics.

Genome Editing Market Segment Analysis:

Based On Technology, The CRISPR/Cas9 segment dominates the Technology segment of the Genome Editing Market in 2025. This technological segment is simple, easy to use, and inexpensive compared to other techniques. Increasing demand for CRISPR/Cas9 for the investigation of the genome to identify genetic disorders and its drug discovery increases the opportunity for the genome editing market segment. CRISPR technology is used for the treatment of cancer through gene-editing technology. Key market players such as Caribou Biosciences, Takara Bio, and Thermo Fisher Scientific are focusing on their research and development activities for adapting innovations in the CRISPR/Cas9 technology.

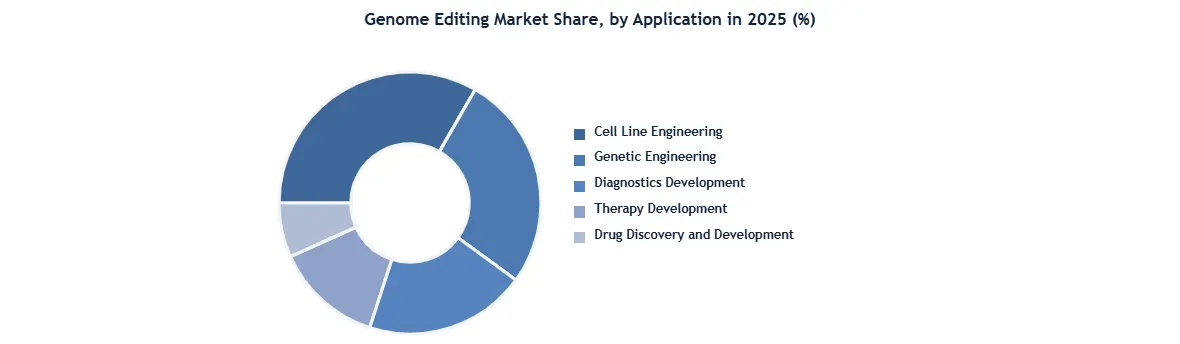

Based On Application, The Cell-line engineering segment dominates the Application Segment of the Genome Editing Market in 2025. As this is widely used for stem cell-based cell therapy treatment. Advancements in genome editing have quickly enabled the introduction of genetic changes into induced pluripotent stem cells (iPSCs) and the correction of disease-causing mutations. Recent improvements in editing techniques, including Zinc Finger Nucleases (ZFNs), CRISPR/Cas, and TALENs, have not only reduced the cost of cell engineering but also streamlined the process. These developments represent significant progress in genetic manipulation and its application to induced pluripotent stem cells.

Genome Editing Market Regional Insights:

North America dominated the Genome Editing Market in the year 2025. This is because of the rise in the number of rare diseases in the U.S. and Canada. According to the MMR Study report, there are approximately 7,000 rare diseases affecting between 25 and 30 million Americans. Therefore, the demand for the development of drugs to cure rare diseases increases with the adoption of new gene-editing tools and technologies. Also, the presence of leading industry players in North America fosters Genome editing market growth. Asia Pacific region is expected to be the second dominant region in this market. The rising number of research organizations in emerging countries augments the regional industry scenario. Major companies are inclining toward the development of gene editing techniques that fuel the regional industry growth. Increasing research and development activities in Japan, China, and India boost the regional market trends.

Genome Editing Market Scope: Inquire before buying

| Genome Editing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 9.7 USD Billion |

| Forecast Period 2026-2032 CAGR: | 15.8% | Market Size in 2032: | 27.07 USD Billion |

| Segments Covered: | by Technology | CRISPR/Cas9 TALENs Zinc Finger Nucleases (ZFNs) Meganucleases Other Technologies |

|

| by Delivery Method | Ex vivo In vivo |

||

| by Delivery Modality | Viral Vectors Non-Viral Vectors |

||

| by Gene Editing Approach | Gene Knock-out Gene Knock-in |

||

| by Type of Therapy | Cell Therapies Gene Therapies Other Therapies |

||

| by Mode | In-house Contract |

||

| by Payment Method Employed | Upfront Payments Milestone Payments |

||

| by Application | Cell Line Engineering Genetic Engineering Animal Genetic Engineering Plant Genetic Engineering Diagnostics Development Therapy Development Drug Discovery and Development Others |

||

| by End User | Pharmaceutical and Biotechnology Companies Academic and Research Institutes Contract Research Organizations (CROs) |

||

Genome Editing Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Genome Editing Market key players

1. Editas Medicine, Inc.

2. Intellia Therapeutics, Inc.

3. Beam Therapeutics Inc.

4. Caribou Biosciences, Inc.

5. Precision BioSciences, Inc.

6. Sangamo Therapeutics, Inc.

7. Prime Medicine, Inc.

8. Graphite Bio, Inc.

9. Vor Biopharma Inc.

10. ArsenalBio

11. Synthego Corporation

12. Integrated DNA Technologies (IDT)

13. Agilent Technologies, Inc.

14. Bio-Rad Laboratories, Inc.

15. Illumina, Inc.

16. BGI Genomics Co., Ltd.

17. GenScript Biotech Corporation

18. Takara Bio Inc.

19. ToolGen, Inc.

20. Biocytogen Pharmaceuticals

21. NTrans Technologies

22. CRISPR Therapeutics AG

23. Cellectis S.A

24. Lonza Group AG

25. Merck KGaA (Sigma-Aldrich)

26. QIAGEN N.V.

27. Eurofins Scientific

28. OXGENE

29. Avectas

30. Congenica Ltd

31. Thermo Fisher Scientific Inc.

32. Danaher Corporation

33. Revvity, Inc.

34. New England Biolabs, Inc.

35. OriGene Technologies, Inc.

36. Charles River Laboratories International, Inc.

37. Horizon Discovery (Revvity)

38. Transposagen Biopharmaceuticals, Inc.

39. Arcturus Therapeutics Holdings Inc.

40. Century Therapeutics, Inc.

1] Which region is expected to hold the highest share of the Global Genome Editing Market?

Ans. The North America region is expected to hold the highest share of the Genome Editing Market.

2] What is the market size of the Global Genome Editing Market by 2032?

Ans. The market size of the Genome Editing Market by 2029 is expected to reach US$ 27.07 Bn.

3] What was the market size of the Global Genome Editing Market in 2025?

Ans. The market size of the Genome Editing Market in 2025 was valued at US$ 9.7 Bn.

4] Key players in the Genome Editing Market.

Ans. Editas Medicine, Inc., Intellia Therapeutics, Inc. Beam Therapeutics Inc. Caribou Biosciences, Inc., Precision Biosciences, Inc.