Molecular Diagnostics Market Size by Product & Service, Test Type, Technology, Application, End User, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

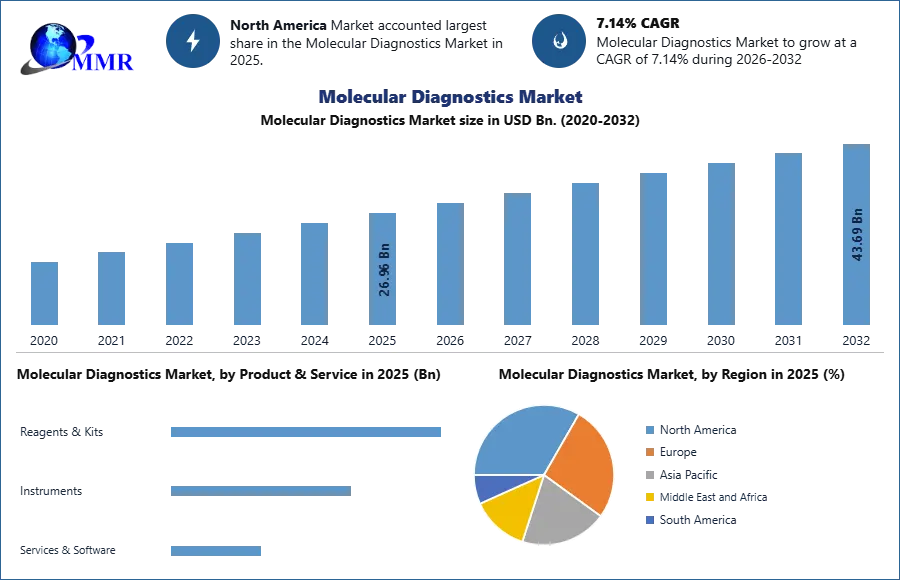

The Molecular Diagnostics Market size was valued at USD 26.96 Billion in 2025 and the total Molecular Diagnostics revenue is expected to grow at a CAGR of 7.14 % from 20264 to 2032, reaching nearly USD 43.69 Billion by 2032.

The Molecular Diagnostics Market revolves around the utilization of genetic and proteomic information to detect, diagnose, classify, prognosis, and monitor response to therapy. It integrates molecular biology techniques into medical diagnostics, focusing on genetic polymorphisms and biomarkers in the genome and proteome, assessing gene expression through protein analysis in cells. This field employs powerful methodologies such as PCR-based techniques for bacterial gene detection and quantification of infection-specific proteins using ELISA and proteomics, marking a significant advancement. The Molecular Diagnostics Market leaders such as Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, and Siemens Healthineers have spearheaded recent developments, showcasing innovations in highly sensitive and accurate diagnostic platforms.

Rising incidence of infectious diseases and cancers, augmented understanding and acceptance of personalized treatments, and continual advancements in biomarker discovery are major factors which drives the growth of The Molecular Diagnostics Market. Stringent regulatory hurdles for new molecular diagnostic techniques may impede The Molecular Diagnostics Market growth. The Molecular Diagnostics industry is expected a shift toward increased adoption of molecular diagnostics in emerging economies, offering promising prospects for market growth. Recent developments by key players involve the launch of novel platforms and technologies enhancing the scope, accuracy, and applicability of molecular diagnostics across various disease categories, underlining its pivotal role in modern healthcare.

To know about the Research Methodology :- Request Free Sample Report

Molecular Diagnostics Market Dynamics:

Major Epidemics of the Modern Era as Market Drivers

Rising Need for Point-of-Care Diagnostics:

The rising demand for Point-of-Care Diagnostics serves as a significant growth driver for the Molecular Diagnostics Market, driven by the increasing frequency of global bacterial and viral epidemics. This rise necessitates rapid and easily accessible diagnostic solutions. For instance, the COVID-19 pandemic catalyzed the need for swift and on-the-spot testing. Technologies such as rapid antigen tests and PCR-based diagnostics emerged as vital tools for immediate disease identification, treatment initiation, and containment efforts, showcasing the Molecular Diagnostics Market response to urgent healthcare needs.

Impact of Tuberculosis and Cancer Prevalence:

The prevalence of diseases such as Tuberculosis (TB) and cancer, affecting 10.5 million individuals globally in 2023, primarily in countries such as India and China, has boosted the Molecular Diagnostics Market growth. The accuracy and speed of these diagnostic tools are crucial in identifying TB strains, aiding in medication sensitivity analysis, and enabling prompt treatment decisions. The growing global cancer incidence, expected to reach 28 million cases by 2040, underscores the necessity for precise microorganism identification and characterization. Molecular diagnostics, with advancements such as liquid biopsy techniques, play a pivotal role in early cancer detection and personalized treatment strategies, further solidifying its position as an indispensable healthcare tool and driving force behind Molecular Diagnostics Market growth.

Better testing detects the organism's strain and medication sensitivity more rapidly, minimizing the time it takes to locate the proper antibiotic. Technological advances, such as polymerase chain reaction (PCR), have also enabled the identification of antibiotic resistance genes and the provision of public health information, such as strain characterization via genotyping. As a result of the aforementioned reasons, the Molecular Diagnostics Market is expected to increase significantly during the forecast period.

Understanding Emerging and Re-emerging Infectious Diseases

Global epidemics of severe infectious illnesses caused by harmful microorganisms have substantially spurred researchers to create speedy and accurate pathogen detection technologies. Culture-based approaches have traditionally been regarded as gold standards for pathogen detection; however, the lengthy turnaround time associated with these procedures owing to overnight culturing and pathogen isolation limits their use to some extent. The discovery Product & Services of molecular diagnostic tools have sparked a revolution in the diagnosis and surveillance of infectious illnesses in recent years.

Initial investments and ongoing expenses pose financial barriers to accessing molecular diagnostics

Stringent regulatory requirements hampers the growth of Molecular Diagnostics Market, exemplified by the FDA's rigorous validation procedures during the COVID-19 pandemic, caused delays in approving crucial diagnostic tests such as Ellume's at-home PCR test. These prolonged processes hindered rapid deployment, undermining the market's potential growth despite the tests' effectiveness.

Financial barriers, comprising significant initial investments and ongoing expenses, hinder accessibility to molecular diagnostics. For instance, next-generation sequencing (NGS) platforms by Illumina require high initial costs, limiting access for smaller laboratories. Inadequate reimbursement policies further stymie Molecular Diagnostics Market growth. Reimbursement challenges faced by liquid biopsy tests, such as Guardant Health's assays, due to insufficient coverage by insurers, hamper patient access to advanced cancer diagnostics.

| Financial Barrier | Description |

| High Initial Investment | Illumina's Next-Generation Sequencing (NGS) platform costs between $500,000 to $1,000,000, hindering smaller laboratories' affordability. |

| Ongoing Operational Costs | Annual expenses for maintaining NGS equipment, estimated at $200,000 - $500,000, adding to financial burden. |

| Skilled Personnel Costs | Average annual salary for a molecular diagnostics expert, ranging from $80,000 to $150,000, contributing to high operational costs. |

| Reagent Expenses | Annual reagent costs for NGS procedures, estimated at $50,000 - $100,000, adding to the overall financial burden. |

| Training and Education Costs | Expenses for specialized training programs in molecular diagnostics, averaging $5,000 - $10,000 per participant, increasing initial investment. |

| Capital Budget Constraints | Limited capital budgets allocated for molecular diagnostics, with an average annual budget of $1,000,000 for equipment and resources. |

| Affordability for Smaller Labs | Percentage of smaller laboratories unable to afford NGS platforms due to high initial costs, estimated at 40%. |

| Impact on Research Funding | Reduction in research grants for molecular diagnostics projects, with a decrease of 20% in funding allocation over the past five years. |

| Cost-Prohibitive Technology | Percentage of healthcare institutions limiting adoption due to high costs, with 30% unable to afford advanced molecular diagnostics. |

| Impact on Market Growth | Financial barriers leading to a projected 15% decrease in market growth for molecular diagnostics over the next three years. |

The complexity of molecular diagnostic technologies presents a steep learning curve, impeding their widespread implementation. Interpreting genomic data, as seen in Foundation Medicine's comprehensive genomic profiling for precision medicine, demands specialized expertise, restricting routine clinical adoption. Ethical concerns surrounding genetic data misuse, for instance, privacy debates from the unauthorized use of DNA databases such as GEDmatch in criminal investigations, erode patient trust and potentially challenge Molecular Diagnostics Market growth.

Understanding the clinical significance of genetic variations identified through whole-genome sequencing, as demonstrated by Genomics England in rare genetic disorder analysis, requires substantial expertise, limiting broader adoption. Fragmentation within the Molecular Diagnostics Market, arising from diverse molecular diagnostic platforms and techniques, hinders standardization and compatibility, impeding seamless integration and interoperability.

Molecular Diagnostics Market Segment Analysis:

Based on Product & Service, In 2024, the reagents & kits category had the most revenue share of the molecular diagnostics market. It is expected to continue its dominance over the forecast years as a result of its widespread use in research and therapeutic settings. Standard reagents aid in producing efficient and precise outcomes. Standardized outcomes, increased efficiency, and cost-effectiveness are expected to drive market growth.

The increased usage of devices to detect coronavirus, which was previously developed for other infectious disorders, is expected to drive market growth. For example, Roche Diagnostics extended its Covid RT-PCR assays offering to the new Cobas 5800 system in countries that obtained the CE mark clearance in February 2022.

Based on Test Type, the lab tests category held the greatest proportion of the molecular diagnostics market share. The growing requirement for automation, as well as the increased occurrence of numerous infectious illnesses, are driving the growth of this category. Control is one of the advantages of laboratory testing. Conducting distribution testing in a laboratory setting allows for managing the test intensity level, as well as ensuring regulatory compliance, repeatability, and impartiality. Cost reductions, real-time monitoring, and a shorter time to market. All these factors are expected to drive the growth of lab tests during the forecast period.

Based on Technology, the polymerase chain reaction (PCR) category generated the largest revenue in molecular diagnostics. This is due to its Test Type in the diagnosis of COVID-19 and other infectious disorders. The growing use of high-throughput PCR technology to diagnose viral and genetic illnesses boost market growth. DNA sequencing methods and new NGS technologies such as sequencing platforms and RNA sequencing are examples of sequencing technologies for the molecular diagnostics sector. Medication discovery, innovative drug development, and customized treatment are all inextricably related to DNA sequencing technology. Companies are developing novel NGS-based assays for early illness detection.

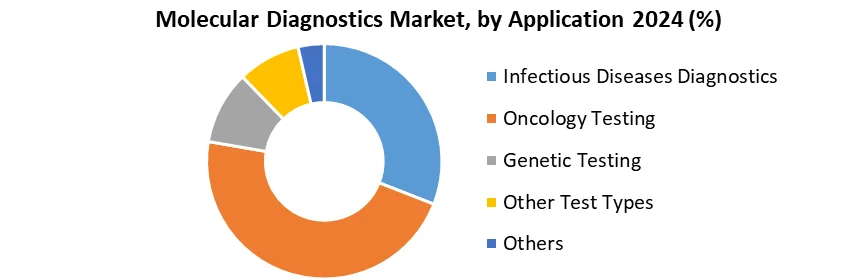

Based on Application, the Infectious Disease Diagnostics category had the most revenue share of the molecular diagnostics market. The growing use of molecular, particularly PCR assays, for the diagnosis of COVID-19 is the primary cause of this segment's dominance. Traditional testing's shortcomings, such as long turnaround times, poor in vitro kinetic development, difficulties cultivating organisms in manually produced culture medium, and lack of sensitivity, have been mitigated by technology advances such as PCR and ISH.

Molecular Diagnostics Market Regional Insights:

North America's Dominance in the Molecular Diagnostics Market

North America holds a commanding position in the Molecular Diagnostics market and is expected to maintain its lead in the forecast period. The region's supremacy is attributed to several factors, including significant outbreaks of bacterial and viral diseases, a burgeoning need for point-of-care diagnostics, rapid technological advancements, and the presence of key Molecular Diagnostics market players. During the COVID-19 pandemic, the United States, under the guidance of the Centers for Disease Control and Prevention (CDC), employed advanced diagnostic methods, such as one-step PCR techniques, for COVID-19 diagnosis.

The adoption of molecular diagnostics in the United States has transformed disease diagnostics, ensuring timely identification and accurate treatment for critically ill patients. Factors such as increased healthcare spending per capita, advancements in healthcare infrastructure, and a rising incidence of infectious diseases and cancer have boosted a shift towards molecular diagnostics from traditional methods. In Canada, the prevalence of chronic illnesses, especially among the elderly population, is expected to drive the demand for molecular diagnostic testing. Statistics from the Canadian government indicate a significant percentage of the population grappling with prevalent chronic disorders, signaling a growing need for advanced diagnostic solutions.

Meanwhile, Europe, while being a significant consumer, actively imports molecular diagnostic tools to supplement its healthcare capabilities. As for the Asia-Pacific (APAC) region, it stands at the forefront of emerging markets, showcasing rapid growth in molecular diagnostics driven by increasing healthcare expenditure, growing awareness, and a rising demand for advanced healthcare solutions. This regional landscape indicates a symbiotic relationship between North America's production prowess, Europe's consumption patterns, and APAC's emerging market dynamics, fostering a global exchange of expertise and technologies that drive the evolution of molecular diagnostics on a worldwide scale.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 06 March 2026 | Thermo Fisher Scientific | Introduced a specialized molecular test to assist transplant patients in receiving anti-rejection medication sooner. | This development improves patient outcomes in organ transplantation through faster molecular monitoring of drug efficacy. |

| 26 February 2026 | Insight Molecular Diagnostics | Achieved final ISO 13485 certification for the GraftAssureDx test kit, enabling regulatory filings in the U.K. and E.U. | The certification paves the way for international commercialization of decentralized transplant monitoring solutions. |

| 22 January 2026 | Abbott | Announced the pending acquisition of Exact Sciences, expected to close in the second quarter of 2026. | This multi-billion dollar move solidifies Abbott's leadership in the high-growth cancer molecular diagnostics market. |

| 05 August 2025 | Seegene Inc. | Unveiled CURECA and STAgora at the ADLM 2025 conference to advance syndromic molecular testing. | These platforms enhance high-throughput diagnostics by integrating automated data analysis and standardized clinical reporting. |

| 29 May 2025 | Danaher Corporation | Partnered with AstraZeneca to develop AI-powered diagnostics for precision medicine. | The collaboration streamlines companion diagnostic development, directly linking molecular testing with targeted cancer therapies. |

Molecular Diagnostics Market Competitive Landscapes:

The Molecular Diagnostics Market is highly competitive characterized by dynamic strategies adopted by Molecular Diagnostics key players, focusing on collaborations, acquisitions, product launches, and expansions to drive market growth, especially within the instruments segment. Mylab Discovery Solutions and Hemex Health forged a strategic partnership aimed at developing next-generation diagnostic solutions for Point-of-Care (POC) testing. Hemex's Gazelle POC testing platform combined with Mylab's assay design expertise is poised to bolster the POC molecular diagnostics market, indicating a trend towards innovative partnerships driving segment growth. Similarly, Cepheid's establishment of direct operations in Canada signifies a strategic move to expand its market presence, aiming to augment molecular diagnostic testing adoption in the region, particularly within North America.

Pioneering product launches have been instrumental in shaping the competitive landscape. Roche introduced the Cobas 5800 System, enhancing testing accessibility and patient care, particularly in regions accepting the CE mark. Hologic, Inc.'s rollout of the Novodiag Molecular Diagnostic System in Europe signifies a significant advancement in on-demand molecular testing, integrating real-time PCR and DNA microarray capabilities for efficient pathogen identification.

Government initiatives have also played a pivotal role, as demonstrated by the US Department of Defense's substantial investment in Qiagen for scaling up COVID-19 Test Kit and Reagent manufacturing, underlining the strategic partnerships between public bodies and industry players to meet crucial testing demands.

Strategic acquisitions have also shaped Molecular Diagnostics market dynamics, for instance, Hologic, Inc.'s acquisition of Biotheranostics Inc., a move aimed at broadening their molecular diagnostics portfolio. Partnerships such as Bio-Rad Laboratories Inc.'s collaboration with Seegene Inc., focusing on developing and commercializing infectious disease molecular diagnostic products in the United States, underscore the industry's concerted efforts towards innovation and diversification to address evolving healthcare needs. These multifaceted strategies underscore the competitive landscape's vibrancy, emphasizing a mix of collaborations, product innovations, acquisitions, and partnership to advance molecular diagnostics market globally.

Molecular Diagnostics Market Scope: Inquire before buying

| Molecular Diagnostics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 26.96 USD Bn. |

| Forecast Period 2026-2032 CAGR: | 7.14% | Market Size in 2032: | 43.69 USD Bn. |

| Segments Covered: | by Product & Service | Reagents & Kits Instruments Services & Software |

|

| by Test Type | Lab Tests PoC Tests |

||

| by Technology | Polymerase Chain Reaction (PCR) Isothermal Nucleic Acid Amplification Technology (INAAT) DNA Sequencing & Next- generation Sequencing (NGS) In Situ Hybridization (ISH) DNA Microarrays Other Technologies |

||

| by Application | Infectious Diseases Diagnostics Oncology Testing Genetic Testing Other Test Types |

||

| by End User | Diagnostic Laboratories Hospitals & Clinics Other |

||

Molecular Diagnostics Market by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Molecular Diagnostics Market Report in Strategic Perspective:

- Abbott Laboratories

- Danaher Corporation,

- Quest Diagnostics

- Hologic, Inc.

- Thermo Fisher Scientific

- Sysmex Corporation

- BGI Group

- Biocon

- Mylab Discovery Solutions

- Trivitron Healthcare

- XCyton Diagnostics

- HLL Lifecare Limited

- F. Hoffmann-La Roche Ltd.

- QIAGEN N.V.

- bioMérieux

- Siemens Healthineers,

- Illumina, Inc.

- BD (Becton, Dickinson and Company)

- Agilent Technologies

- Seegene Inc.

- Exact Sciences

- QuidelOrtho

- Bio-Rad Laboratories

- Myriad Genetics