Urea Market by Grade, End User and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

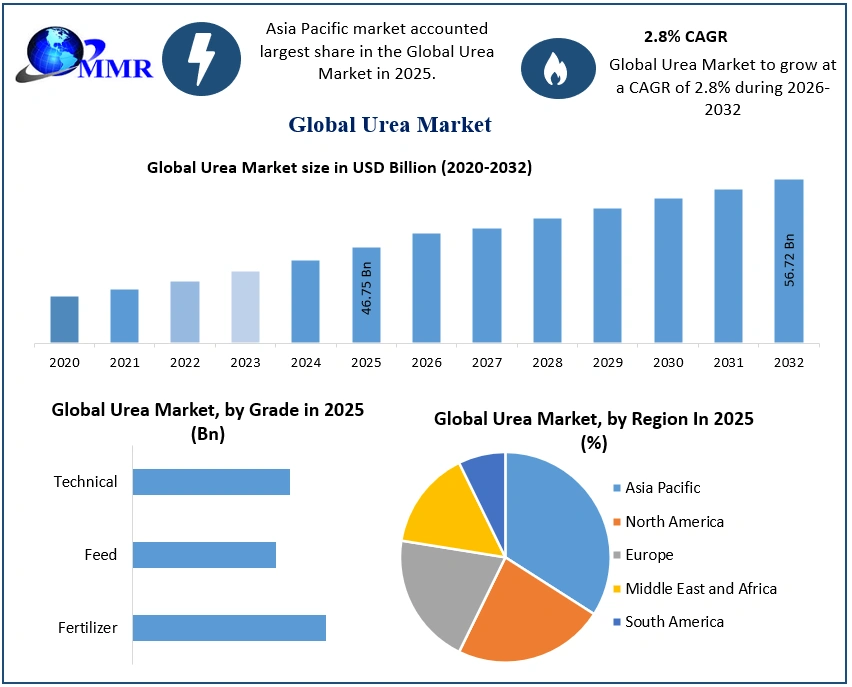

The Urea Market size was valued at USD 46.75 Billion in 2025 and the total Urea revenue is expected to grow at a CAGR of 2.8% from 2026 to 2032, reaching nearly USD 56.72 Billion by 2032.

Global Urea Market Overview :

Urea is a nitrogen-rich chemical compound primarily used as a fertilizer due to its high nitrogen content (46%), making it essential for improving soil fertility and enhancing crop productivity. In addition to agriculture, urea is widely used in the production of resins, adhesives, plastics, pharmaceuticals, animal feed supplements, and diesel exhaust fluid (DEF) for reducing vehicle emissions.

The global urea market is driven by rising food demand, increasing fertilizer consumption, and expanding industrial applications. Growing populations, declining arable land, and the need for higher agricultural productivity are boosting demand, particularly in Asia-Pacific, led by China and India. Technological advancements in production, capacity expansions, and the development of sustainable fertilizer solutions are further supporting market growth. Despite challenges such as fluctuating natural gas prices and environmental regulations, the market is expected to witness steady growth throughout the forecast period, supported by strong demand from both the agricultural and industrial sectors.

To know about the Research Methodology :- Request Free Sample Report

Global Urea Market Dynamics

Market Drivers

Rising Global Demand for Nitrogen Fertilizers and Food Security

The primary driver of the global urea market is the increasing demand for nitrogen-based fertilizers to support global food production. Rapid population growth, shrinking arable land, and the need to improve crop yields have significantly increased the adoption of urea, owing to its high nitrogen content (46%) and cost-effectiveness. Developing economies such as India, China, Brazil, and Southeast Asian countries continue to witness robust fertilizer consumption, supported by government subsidy programs and initiatives aimed at enhancing agricultural productivity. Precision farming practices and balanced nutrient management are further strengthening urea demand as farmers seek to maximize crop output while improving resource efficiency.

Expanding Industrial Applications and Emission Control Technologies

Besides agriculture, urea is experiencing growing demand from various industrial sectors. It serves as a key raw material in the production of urea-formaldehyde resins, adhesives, laminates, plastics, pharmaceuticals, and animal feed supplements. Additionally, the increasing adoption of diesel exhaust fluid (DEF), also known as automotive-grade urea, in selective catalytic reduction (SCR) systems is driving market growth as governments worldwide enforce stricter vehicle emission standards. Rising commercial vehicle production and expanding transportation infrastructure, particularly across Asia-Pacific and the Middle East, continue to support demand for automotive-grade urea. Technological advancements in low-carbon ammonia and energy-efficient urea manufacturing are further enhancing production efficiency and supporting long-term market expansion.

Market Restraints

Volatile Feedstock Prices and Environmental Regulations

The urea market faces significant challenges due to fluctuations in natural gas prices, the primary feedstock for ammonia and urea production. Changes in energy costs directly affect manufacturing expenses and profit margins, particularly in regions dependent on imported natural gas. Furthermore, increasingly stringent environmental regulations aimed at reducing greenhouse gas emissions and nitrogen pollution are compelling manufacturers to invest in cleaner production technologies and emission control systems. Excessive or improper application of urea fertilizers can contribute to ammonia volatilization, nitrate leaching, and water eutrophication, prompting governments to encourage sustainable fertilizer practices and alternative nutrient management solutions. These factors may limit market growth, particularly in environmentally regulated regions such as Europe and North America.

Market Opportunities

Sustainable Fertilizers and Capacity Expansion in Emerging Economies

Growing investments in enhanced-efficiency fertilizers, coated and stabilized urea products, and green ammonia production present substantial opportunities for market participants. The development of slow-release and controlled-release urea fertilizers helps improve nitrogen-use efficiency while minimizing environmental impact, aligning with global sustainability goals. Simultaneously, increasing investments in domestic fertilizer production across emerging economies, particularly India, the Middle East, and Africa, are strengthening supply chains and reducing import dependence. Rising adoption of precision agriculture, digital farming technologies, and government initiatives promoting food security are expected to create significant growth opportunities for the global urea market throughout the forecast period.

Market Trends

• Growing Adoption of Enhanced-Efficiency Fertilizers

Farmers are increasingly adopting coated, stabilized, and slow-release urea fertilizers to improve nitrogen-use efficiency, reduce nutrient losses, and comply with environmental regulations. These products support sustainable agriculture while enhancing crop productivity.

• Expansion of Green Ammonia and Low-Carbon Urea Production

Manufacturers are investing in green ammonia, carbon capture technologies, and energy-efficient production processes to reduce the carbon footprint of urea manufacturing. Sustainability initiatives and government decarbonization policies are accelerating this trend.

• Rising Demand for Automotive-Grade Urea (DEF)

The implementation of stricter vehicle emission standards across major economies is driving demand for diesel exhaust fluid (DEF), creating new growth opportunities for automotive-grade urea manufacturers.

• Increasing Adoption of Precision Agriculture

The use of precision farming technologies, including GPS-guided fertilizer application, soil nutrient monitoring, and digital farm management systems, is improving fertilizer efficiency and supporting the optimal use of urea.

Urea Market Segment Analysis

By Grade

Agricultural Grade Dominates the Market

Agricultural-grade urea accounts for the largest share of the global urea market due to its widespread use of nitrogen fertilizer for cereals, grains, fruits, vegetables, and other crops. It Contains approximately 46% nitrogen, it is one of the most cost-effective fertilizers available, making it the preferred choice for farmers worldwide. Rising global food demand, government fertilizer subsidy programs, and increasing adoption of modern farming practices in countries such as India, China, and Brazil continue to drive the dominance of this segment.

Industrial Grade Expected to Witness the Fastest Growth

Industrial-grade urea is projected to register the fastest growth during the forecast period owing to its expanding applications in urea-formaldehyde resins, adhesives, plastics, pharmaceuticals, animal feed supplements, and diesel exhaust fluid (DEF). Growing industrialization, stricter vehicle emission regulations, and increasing demand from the automotive and chemical industries are supporting the rapid growth of this segment.

By Application

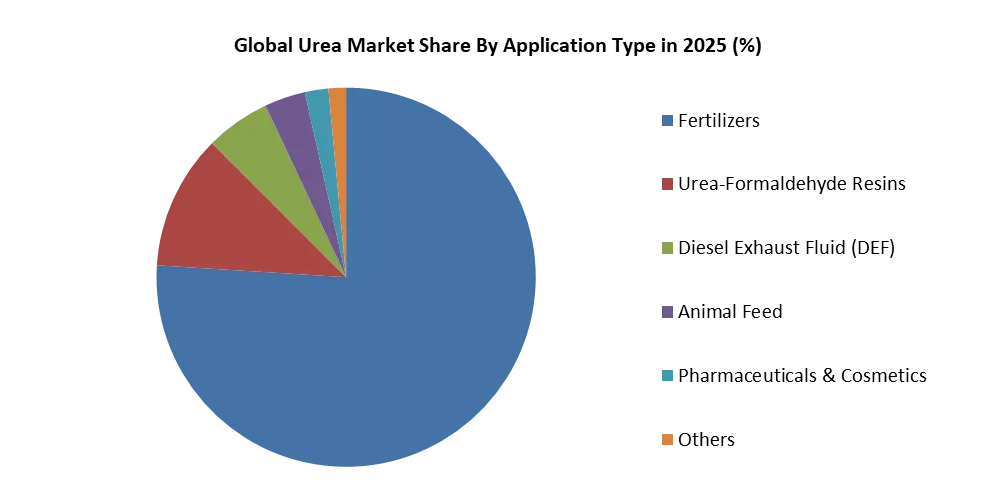

Fertilizers Hold the Largest Market Share

The fertilizer segment dominates the global urea market, accounting for the majority of overall consumption. Urea remains the most widely used nitrogen fertilizer due to its high nutrient content, affordability, and effectiveness in improving crop yields. Increasing agricultural production, rising fertilizer consumption, and government initiatives supporting food security continue to strengthen demand for urea fertilizers across both developed and developing economies.

Chemical Manufacturing Emerges as the Fastest-Growing Segment

The chemical manufacturing segment is expected to witness the highest growth rate during the forecast period. Urea is widely used as a raw material in the production of urea-formaldehyde and melamine resins, adhesives, laminates, coatings, and various industrial chemicals. Additionally, growing demand for diesel exhaust fluid (DEF) in selective catalytic reduction (SCR) systems and expanding applications in pharmaceuticals, cosmetics, and animal nutrition are further driving growth in this segment. Rising industrialization, increasing environmental regulations, and investments in downstream chemical manufacturing are expected to support sustained expansion over the forecast period.

Urea Market Regional Insights:

Asia-Pacific

Asia-Pacific dominates the global urea market, accounting for the largest revenue share due to its vast agricultural base, high population, and strong demand for nitrogen fertilizers. China remains the world's largest producer and consumer of urea, while India is one of the largest importers, supported by government fertilizer subsidy programs and rising food security initiatives. Expanding domestic production capacities, increasing adoption of precision farming, and growing industrial applications continue to strengthen the region's market position. Additionally, rising demand from Southeast Asian countries is expected to support sustained regional growth throughout the forecast period.

North America

North America represents a significant share of the global urea market, driven by advanced commercial agriculture, abundant natural gas resources, and increasing adoption of precision farming technologies. The region also benefits from rising demand for diesel exhaust fluid (DEF) used in selective catalytic reduction (SCR) systems to comply with stringent vehicle emission standards. Investments in domestic fertilizer production and stable feedstock availability continue to enhance regional market growth, although seasonal import requirements remain an important factor influencing supply.

Europe

Europe holds a considerable share of the urea market, supported by modern agricultural practices and a well-established chemical manufacturing industry. The region is witnessing growing demand for sustainable fertilizers and enhanced-efficiency urea products as governments implement stricter environmental regulations to reduce greenhouse gas emissions and nitrogen pollution. However, higher energy costs and dependence on imported natural gas continue to affect domestic urea production, encouraging investments in low-carbon manufacturing technologies and green ammonia projects.

Latin America

Latin America is emerging as a high-growth market owing to the expansion of commercial agriculture, particularly in Brazil and Argentina. Increasing cultivation of soybean, corn, and sugarcane, coupled with rising fertilizer consumption to improve crop productivity, is driving urea demand across the region. Although domestic production remains limited, ongoing investments in agricultural modernization and infrastructure development are expected to sustain market growth, despite continued reliance on imports.

Middle East & Africa

The Middle East & Africa region plays a strategic role in the global urea market due to its abundant natural gas reserves and large-scale fertilizer production facilities. Countries such as Saudi Arabia, Qatar, and the UAE are major exporters of urea, supplying international markets with cost-competitive products. Meanwhile, Africa is experiencing increasing fertilizer demand driven by agricultural modernization, government initiatives to improve food security, and expanding cultivation areas. Continued investments in production capacity and export infrastructure are expected to strengthen the region's position in the global market over the forecast period.

Competitive Landscape For Global Urea Market

The global urea market is moderately fragmented, with competition driven by production capacity, access to low-cost natural gas feedstock, global distribution networks, and investments in sustainable fertilizer technologies. Leading manufacturers are focusing on expanding production capacity, optimizing supply chains, and developing enhanced-efficiency fertilizers and low-carbon ammonia solutions to strengthen their market positions. Strategic partnerships, capacity expansion projects, and investments in green ammonia and carbon capture technologies are becoming key competitive strategies as the industry transitions toward sustainable fertilizer production.

| Company | Key Strengths | Strategic Focus |

| Yara International ASA | Strong global production and distribution network with a diversified fertilizer portfolio. | Expanding green ammonia production, sustainable fertilizers, and global capacity. |

| Nutrien Ltd. | Integrated fertilizer production with an extensive agricultural retail network. | Digital agriculture, production optimization, and supply chain expansion. |

| CF Industries Holdings, Inc. | Leading producer of nitrogen fertilizers with large-scale manufacturing capabilities. | Investments in low-carbon ammonia, carbon capture, and operational efficiency. |

| OCI Global | Diversified nitrogen fertilizer and industrial chemicals portfolio. | Green hydrogen, clean ammonia, and international market expansion. |

| Indian Farmers Fertiliser Cooperative Limited | Strong domestic manufacturing and extensive farmer distribution network. | Capacity expansion and improved fertilizer accessibility. |

| Qatar Fertiliser Company | Cost-efficient production supported by abundant natural gas resources. | Export growth, production efficiency, and capacity optimization. |

| EuroChem Group AG | Vertically integrated operations with a diversified fertilizer portfolio. | Global expansion and specialty fertilizer development. |

| National Fertilizers Limited | Strong public-sector presence and nationwide distribution capabilities. | Plant modernization and sustainable fertilizer production. |

| Saudi Arabian Fertilizer Company | Competitive production costs and significant export capabilities. | Low-carbon fertilizer production and international partnerships. |

| PT Pupuk Kalimantan Timur | Leading producer serving Southeast Asian agricultural markets. | Production efficiency, regional expansion, and sustainability initiatives. |

Recent Developments in the Global Urea Market

- June 2026: The Government of India announced a roadmap to introduce Green Urea by procuring approximately 724,000 metric tonnes of green ammonia annually under the National Green Hydrogen Mission. The initiative aims to reduce dependence on imported urea, promote low-carbon fertilizer production, and accelerate the decarbonization of India's fertilizer industry.

- June 2026: India confirmed that two new urea manufacturing plants are set to commence operations, adding approximately 2.54 million tonnes of annual production capacity. The expansion is expected to strengthen domestic fertilizer supply, reduce import dependence, and support the country's growing agricultural sector.

- June 2026: Petróleo Brasileiro S.A. (Petrobras) announced the resumption of construction of the UFN-III fertilizer plant in Três Lagoas, Brazil. Once operational, the facility will produce approximately 3,600 tonnes of urea per day, helping reduce Brazil's reliance on imported nitrogen fertilizers.

- January 2026: Yara International ASA entered advanced negotiations with Air Products and Chemicals, Inc. to collaborate on low-emission ammonia projects in the United States and Saudi Arabia. The partnership focuses on expanding low-carbon ammonia production, supporting the transition toward sustainable urea manufacturing.

- 2025–2026: Leading fertilizer manufacturers across Asia, the Middle East, and Europe accelerated investments in green ammonia, carbon capture and storage (CCS), and energy-efficient urea production technologies to meet increasingly stringent environmental regulations and growing demand for sustainable fertilizers.

Global Urea Market Scope: Inquire before buying

| Global Urea Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 46.75 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 2.8% | Market Size in 2032: | USD 56.72 Bn. |

| Segments Covered: | By Grade | Agricultural Grade (Dominant) Industrial Grade (Fastest Growing) |

|

| By Application | Fertilizers (Dominant) Urea-Formaldehyde Resins Diesel Exhaust Fluid (DEF) Animal Feed Pharmaceuticals & Cosmetics Others |

||

Global Urea Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Leading Companies in the Urea Industry

North America

1. Nutrien

2. CF Industries Nitrogen

3. uf chemical co.

4. Phospholutions

Europe

5. BASF

6. OCI Global

7. Achema

8. Agrofert

Asia Pacific

9. Acron Group

10. Chambal Fertilisers and Chemicals

11. Coromandel International

12. Gujarat Narmada Valley

13. Zuari Agro Chemicals

14. National Fertilizers

15. Talcher Chemicals and Fertilizers

16. Fauji Fertilizer Company

17. Madras Fertilizers

18. Indorama Corporation

19. China BlueChemical

20. Ramagundam Fertilizers & Chemicals

21. Petronas Chemicals Group

ME

22. Gulf Formaldehyde Company

23. SABIC

24. AlexFert

25. Ibn Al-Bayttar

Frequently Asked Questions:

1] What segments are covered in the Global Urea Market report?

Ans. The segments covered in the Urea Market report are based on Grade Type and End User.

2] Which region is expected to hold the highest share in the Global Urea Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Urea Market.

3] What is the market size of the Global Urea Market by 2032?

Ans. The market size of the Urea Market by 2032 is expected to reach USD 56.72 Bn.

4] What is the forecast period for the Global Urea Market?

Ans. The forecast period for the Urea Market is 2026-2032.

5] Who are the top key players in the Global Urea Market?

Ans. Acron, Agrium Inc., BASF SE, BIP (Oldbury) Limited, and CF Industries Holdings, Inc. are the top key players in the Global Urea Market.