Silicon Carbide Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

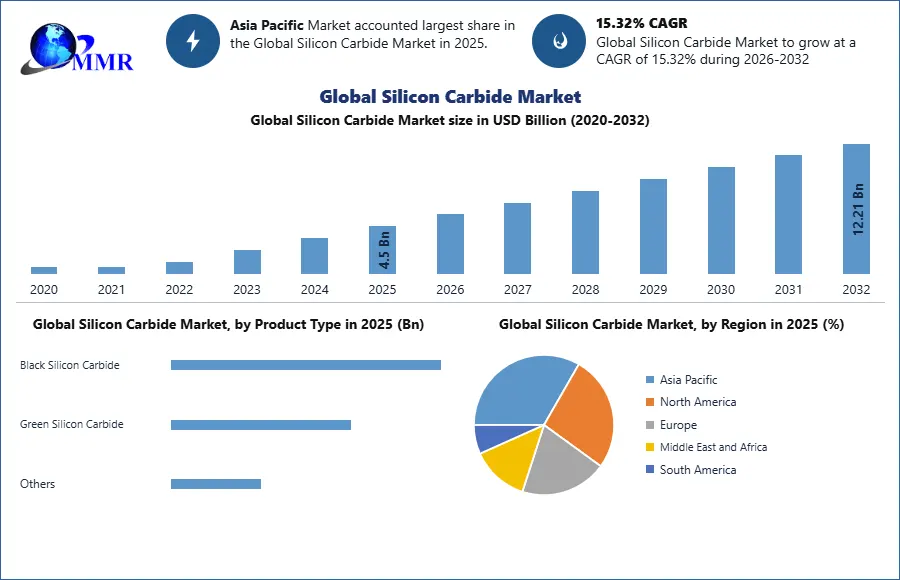

The Silicon Carbide Market size was valued at USD 4.5 Billion in 2025 and the total Silicon Carbide revenue is expected to grow at a CAGR of 15.32% from 2026 to 2032, reaching nearly USD 12.2115.32 Billion by 2032.

Silicon Carbide Market Overview:

Silicon carbide (SiC) is a kind of compound that has silicon and carbon atoms. It is recognized for its excellent features, like good heat conductivity, strength as well as resistance to corrosion and wear. Silicon carbide shows better performance than usual materials which makes it useful in many industries. The silicon carbide market has shown great growth over the past few years, due to a rising desire for top-quality materials in many different sectors. In this market, some companies make and distribute silicon carbide in forms like grains, powders, or wafers. People want silicon carbide because it has special features which include excellent thermal conductivity along with strength and ability to resist tough settings – all these qualities make it very useful for many applications.

To know about the Research Methodology :- Request Free Sample Report

The silicon carbide market is led by the Asia Pacific region, which has many manufacturers and increasing demand from industries like automotive, electronics, and energy. Europe and North America also play significant roles in this market due to their advancements in power electronics as well as electric vehicles. The silicon carbide market remains one of the sectors that are expected to show continuous growth over the next few years. Increasing demand for energy-saving solutions, progress in power electronics, and more use of electric vehicles are expected to push market expansion. Also, continuous research and development efforts concentrating on improving the manufacturing method and material quality might offer fresh prospects for the market's growth.

Global Silicon Carbide Market Dynamics:

Global Silicon Carbide Market Drivers

Demand for Energy Efficiency and Rising Adoption of Electric Vehicles (EVs) are the drivers of the Silicon Carbide Services Market

SiC, which has high thermal conductivity and wide bandgap, is very good for things needing energy efficiency. The rising need for devices that save energy in different areas like cars, power electronics or renewable power sources drives the use of SiC-based solutions. As the world shifts towards electric mobility, it is expected to be more demand for SiC-based power electronics in vehicles. In the field of electrical vehicles (EVs), SiC is becoming more popular due to its ability for higher efficiency and power density. It also allows longer driving ranges as well as faster charging times compared to components made with traditional silicon-based technology.

Advancements in Manufacturing Technologies, Government Regulations and Incentives drives the market

SiC manufacturing technologies continue to improve, such as epitaxial growth, better substrate quality, and advancement in device packaging. These advancements help reduce costs while also improving the overall quality of products. As a result, SiC becomes more commercially feasible which leads to increased market size. Government actions like rules for saving energy or encouraging the use of renewable power and making transport more electric with regulations, grants, and extra benefits are important factors that support the growth of the SiC market. Policies from governments that back clean energy technologies make it appealing for different areas to use SiC-based solutions.

Global Silicon Carbide Market Restraints

High manufacturing Costs can hamper the growth of the Silicon Carbide Market

The Silicon Carbide (SiC) market things need complex ways, requiring high temperatures and special tools. This makes the SiC materials more costly to produce than normal semiconductors made from silicon. The production capability for SiC materials and devices is still limited compared to silicon-based ones. SiC, known for its excellent features such as strong heat conductivity and stability in high temperatures, is becoming more popular in different sectors such as automobile or power electronics. However, the complex production methods needed to utilize these benefits require big investments and ongoing expenses. The special equipment needed for Silicon Carbide production contributes to the capital expenditure, making overall manufacturing costs even higher.

Limited Production Capacity of Silicon Carbide is another restraint

The struggle to fulfill the growing worldwide need for SiC materials and devices is also impacted by the limited production capability. As more industries understand the advantages of SiC compared with usual silicon-based semiconductors, the gap between demand and supply becomes clearer. This leads to a situation where the demand is increased, like when there are new technologies or changes towards energy-saving answers, and can cause less available supplies causing prices to go up more than normal. To deal with these challenges, need to focus on improving the production abilities. Work on making the manufacturing processes better and invest in research and development to find more effective and cheaper ways of SiC production. It is helpful to have joint actions among those involved in the industry, along with policymakers. This could lessen supply restrictions and create a stronger environment worldwide for materials made from SiC as well as devices made using them.

Global Silicon Carbide Market Opportunities

Rising Adoption in Renewable Energy and Emerging Opportunities in 5G Infrastructure are creating opportunities in the Market:

Silicon Carbide (SiC) is very effective and dependable in renewable energy systems, especially for things like solar inverters and wind turbines. It's because of its high efficiency and reliability that it becomes a preferred choice in these systems. As the use of renewable energy grows around the world, there is likely an increase in demand for power electronics based on SiC. The recognition silicon carbide industry's capacity to improve energy conversion and system effectiveness is shown in this trend.

The arrival of 5G networks is bringing a need for components that cope with high frequencies and power levels. Devices based on SiC show unique benefits in this area, like less power loss and more operating frequencies. As the deployment of 5G infrastructure is increasing everywhere, SiC technology is expected to play an important role in helping to advance it. The properties of SiC itself help in creating better, stronger parts that are very important for handling the growing requirements of 5G networks.

SiC's success in renewable energy and 5G infrastructure shows that it has the right qualities for a variety of technology areas. Its ability to make energy conversion more efficient and help with high-frequency operations makes SiC an important part of pushing forward invention and stability in these growing fields. As industries keep focusing on performance, trustworthiness, and eco-friendliness, there is an increasing need for solutions based on SiC which strengthens its position as a crucial technology for future energy and communication needs.

Global Silicon Carbide Market Segment Analysis

The global Silicon Carbide Market is segmented By Product Type, Streaming Devices, Monetization Model, and Service verticals.

By Product Type: The silicon carbide (SiC) market is divided by product type into two main sections, Green SiC and Black SiC. Green SiC, which is made using petroleum coke and silica sand, has a very good hardness and abrasion resistance. This makes it useful for many things such as making abrasive tools, grinding wheels, or even being used as a refractory material. It's also important to note that Black SiC - made from petroleum coke and silica sand through the process of smelting - has qualities such as excellent thermal conductivity combined with low thermal expansion; these factors make it very beneficial in applications related to abrasives as well as those involving refractories and the metallurgical industry.

From these parts, Green SiC takes up much of the market because it has many uses and is already being used in different industries. But Black SiC also has a chance to grow in the future because more people are starting to use it for abrasive and metallurgical purposes, as well as its use by the steel industry in making refractory linings and crucibles. Because of improvements made in manufacturing methods and increasing numbers of end-use sectors, it is predicted that the desire for Black SiC substantially rise over the forthcoming years.

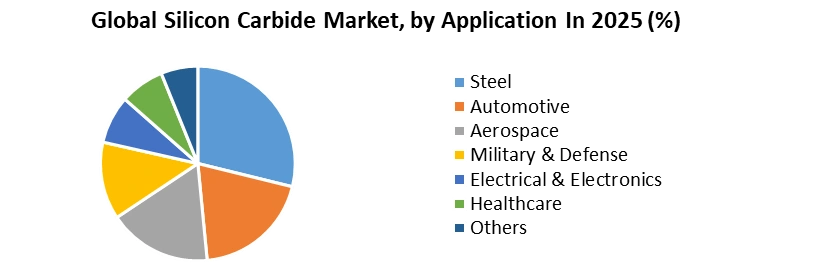

By Application: Market segmentation in the silicon carbide (SiC) market is done by application, which includes important sectors such as Power Electronics, Steel, Automotive, Aerospace, and Defense. The segment of power electronics is one of the most broadly utilized applications. Power devices made from SiC are becoming very popular because they offer better effectiveness, improved thermal control, and higher power density compared to old-fashioned semiconductor materials that use only silicon. The use of power electronics based on SiC is widespread in electric vehicles (EVs), renewable energy systems, industrial power supplies, and grid applications.

The possibility for growth in this area is massive, as the world is moving towards sustainable transportation and using more renewable energy. It is expected to be a massive growth of the future market for power electronics based on SiC because of continuous progress in power electronics technology and the growing need for solutions that use less energy. The rise comes from different reasons like governments pushing electric cars and renewable energy, plus a desire for more power strength along with better performance across various industries.

Global Silicon Carbide Market Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 14 January 2025 | onsemi | Completed the acquisition of the Silicon Carbide Junction Field-Effect Transistor (SiC JFET) technology business from Qorvo for $118.8 million. | Strengthens the EliteSiC power portfolio and addresses high energy efficiency needs in AI data center power supply units. |

| 22 January 2025 | Wolfspeed, Inc. | Launched the new Gen 4 MOSFET technology platform designed for breakthrough performance in high-power applications. | Enhances power density and system efficiency for electric vehicle (EV) drivetrains and renewable energy systems. |

| 13 February 2025 | Infineon Technologies AG | Commenced the first customer deliveries of SiC products manufactured using advanced 200 mm (8-inch) wafer technology from its Villach site. | Improves cost efficiency and supply scale for high-voltage applications including fast-charging stations and heavy industrial motors. |

| 25 September 2025 | ROHM and Infineon | Signed a Memorandum of Understanding to collaborate on compatible packages for SiC power semiconductors. | Increases procurement flexibility for global customers by establishing a stable second-source ecosystem for SiC devices. |

| 17 December 2025 | Toyota Motor Corp. | Launched the next-generation RAV4 hybrid in Japan featuring SiC power semiconductors in its hybrid system for the first time. | Achieved an 18% weight reduction in the hybrid system while extending the electric driving range to 150 km. |

| 28 April 2026 | STMicroelectronics | Advanced the concentration of investment into the new Silicon Carbide Campus in Catania, Italy, dedicated to 200 mm wafer technology. | Solidifies the company’s leadership in wide-bandgap semiconductors and supports the goal of 2027 carbon neutrality through energy-efficient tech. |

Silicon Carbide Market Regional Insights:

Asia Pacific region dominated the Silicon Carbide Market in 2025, with the largest market share. The Asia-Pacific region is a significant player in the global SiC semiconductors industry, including these countries as main manufacturing centers for SiC wafers, devices and components. The swift growth of industries such as electric vehicles (EV), consumer electronics (CE), and telecommunications has also led to an increasing need for SiC-based semiconductor solutions within this region.

China is the largest Silicon Carbide exporter whereas Japan and South Korea are becoming major powers in the worldwide semiconductor industry. The economic advancement of the region, in context with silicon carbide manufacturing capabilities, has progressed dynamically over the last decade. This has encouraged the establishment of downstream sectors which further elevates SiC penetration in this region.

In Europe, countries such as Germany, Norway, and the United Kingdom, have an important presence in this industry. Norway is the largest exporter of the Silicon Carbide Market in the Europe region. The continent has seen growing investments in developing and producing SiC technology, pushed by efforts to boost energy efficiency and sustainability across different sectors. Alongside these movements, the automotive domain of Europe has shown strong acceptance of power electronics based on SiC for electric vehicles and hybrid vehicles.’

The United States is the largest Silicon Carbide importer with above 19% followed by Germany with above 13%. Whereas Japan, South Korea, India, and Poland respectively have a share above 12%, 6.5%, 5%, and 4% in the Silicon Carbide Market.

| Top Importers of the Silicon Carbide Market (in USD Million) | |||

|---|---|---|---|

| United States | 255 | ||

| Germany | 180 | ||

| Japan | 163 | ||

| South Korea | 80 | ||

| India | 69 | ||

| Poland | 56 | ||

Silicon Carbide Market Competitive Landscape:

The competition situation for the silicon carbide (SiC) market shows a mix of old and fresh participants. This variety is caused by the growing possibilities in this market. Among these, Wolfspeed stands out as a well-known company that has its main office located within the United States itself while newcomers, Rohm Semiconductors, etc are leading silicon carbide manufacturers who offer many types of SiC-based products such as power semiconductors and materials.

Additionally, the industry is seeing fresh participants as the silicon carbide market expands. One such example is seen with UnitedSiC, an American company that has gained recognition for its SiC power semiconductors. Concentrating on producing SiC FETs and diodes that show excellent performance makes them attractive to important sectors such as renewable energy, power supplies, and electric vehicles. UnitedSiC is making its market presence stronger and increasing the range of products it offers through forming new partnerships and collaborations. The silicon carbide industry has also seen notable activities related to mergers and acquisitions.

1. In January 2024, Infineon Technologies AG. announced expanding the wafer supply agreement, which is valued at USD 20 billion, with Wolfspeed, Inc. The plan is for Infineon to provide SiC 150 mm wafers to Wolfspeed for making SiC devices.

2. In December 2023, STMicroelectronics N.V., announced the agreement they signed with Li Auto. This is a China-based company that manufactures smart premium electric vehicles. As per this agreement, STMicroelectronics will provide SiC MOSFET devices to support and strengthen Li Auto's plans concerning high-voltage battery electric vehicles (BEVs) for different market divisions.

3. In July 2023, Wolfspeed, Inc. announced the agreement with Renesas Electronics Corporation for wafer supply, worth USD 2 billion, with, a supplier of advanced semiconductor solutions.

4. In March 2022, Microchip Technology, announced the launch of 3.3 kV Silicon Carbide (SiC) power devices, which provide high efficiency and reliability and have the lowest resistance, helping customers to move to high-voltage SiC with speed and ease.

The objective of the report is to present a comprehensive analysis of the global Silicon Carbide Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which gives a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Global Silicon Carbide Market dynamic, and structure by analyzing the market segments and projecting the Global Silicon Carbide Market size. Clear representation of competitive analysis of key players By Price Range, price, financial position, product portfolio, growth strategies, and regional presence in the Global Silicon Carbide Market make the report an investor’s guide.

Silicon Carbide Market Scope: Inquire before buying

| Global Silicon Carbide Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 4.5 USD Billion |

| Forecast Period 2026-2032 CAGR: | 15.32% | Market Size in 2032: | 12.21 USD Billion |

| Segments Covered: | by Product Type | Black Silicon Carbide Green Silicon Carbide Others |

|

| by Wafer Size | 2-inch 4-inch 6-inch 8-inch |

||

| by Application | Steel Automotive Aerospace Military & Defense Electrical & Electronics Healthcare Others |

||

Silicon Carbide Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Silicon Carbide Market Key Players for North America

1. Wolfspeed - [United States]

2. ON Semiconductor Corporation - [United States]

3. United Silicon Carbide Inc. - [United States]

4. GeneSiC Semiconductor Inc. - [United States]

5. Alpha and Omega Semiconductor - [United States]

6. Littelfuse Inc. - [United States]

7. Microsemi Corporation (Microchip Technology) - [United States]

8. Powerex Inc. - [United States]

9. General Electric Company - [United States]

10. AGSCO Corporation - [United States]

Silicon Carbide Market Key Players for Europe

1. Infineon Technologies AG - [Germany]

2. STMicroelectronics N.V. - [Switzerland]

3. Ascatron AB - [Sweden]

4. Danfoss Group - [Denmark]

5. ESD-SIC BV - [Netherlands]

Silicon Carbide Market Key Players for Asia Pacific

1. ROHM Co. Ltd. - [Japan]

2. Toshiba Corporation - [Japan]

3. Mitsubishi Electric Corporation - [Japan]

4. WeEn Semiconductors - [China]

5. Sumitomo Electric Industries Ltd. - [Japan]

Frequently Asked Questions:

1] What segments are covered in the Silicon Carbide Market report?

Ans. The segments covered in the Silicon Carbide Market report are based on Product Type, Wafer Size, and Application.

2] Which region is expected to hold the highest share in the global Silicon Carbide Market?

Ans. Asia Pacific was hold the highest share of the global Silicon Carbide Market in 2025.

3] What is the market size of the global Silicon Carbide Market by 2032?

Ans. The market size of the global Silicon Carbide Market by 2032 is USD 12.21 Bn.

4] Who are the top key players in the global Silicon Carbide Market?

Ans. Wolfspeed, ROHM Co. Ltd., Toshiba Corporation, Mitsubishi Electric Corporation, Infineon Technologies AG, STMicroelectronics N.V., etc are the top key players in the global Silicon Carbide Market.

5] What was the market size of the global Silicon Carbide Market in 2025?

Ans. The market size of the global Silicon Carbide Market in 2025 was USD 4.5 Bn.