System Integration Market Size by Service Type, Enterprise Size, End-user, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2030

Overview

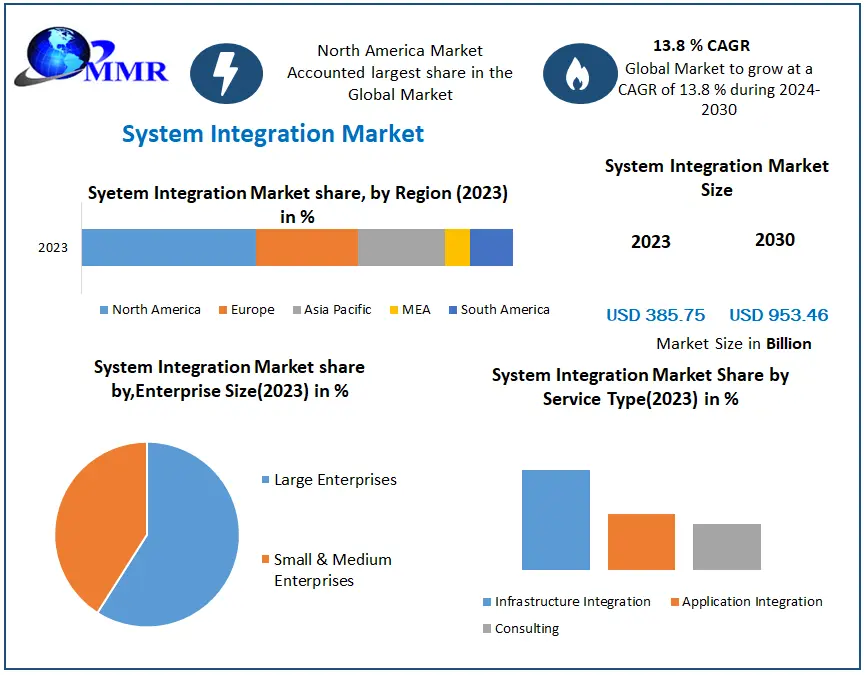

System Integration Market was valued at USD 385.75 Bn in 2023 and is expected to reach USD 953.46 Bn by 2030, at a CAGR of 13.8 % during the forecast period.

System Integration Market Overview

System integration is the process of combining different sub-systems or components into one larger system that functions as a whole. This involves ensuring that all the components work together seamlessly to achieve the intended functionality or purpose of the system. Bringing together hardware, software, and networking components to create a cohesive system. This involve integrating different software applications, databases, servers, and other IT infrastructure components. System integration is essential in various domains such as information technology, manufacturing, telecommunications, and healthcare, where complex systems with multiple components need to work together to achieve specific objectives. It requires careful planning, coordination, and testing to ensure that the integrated system meets the requirements and performs as expected. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The system integration market is growing, due to digital transformation initiatives, the adoption of cloud computing, the proliferation of IoT devices, and the need for seamless connectivity among various systems. The market size is substantial and is expected to continue growing as businesses seek to optimize their operations and enhance efficiency through integrated solutions. The market is competitive, with numerous players offering system integration services and solutions. Key players include large multinational corporations such as IBM, Accenture, Deloitte, Capgemini, and Accenture, as well as smaller regional players and specialized integrators focusing on specific industries or technologies. The system integration market shows regional variations in terms of market maturity, adoption rates, and regulatory environments. Developed economies such as North America and Europe have been early adopters of integrated solutions while emerging economies in Asia-Pacific and Latin America are experiencing rapid growth driven by increasing digitalization and infrastructure development.

System Integration Market Dynamics

Digital Transformation across various industries to boost System Integration Market growth

Growth in digital technologies across industries, organizations are increasingly adopting digital transformation initiatives. System integration plays a important role in this process by enabling the seamless integration of disparate systems, applications, and data sources. Businesses are investing in system integration services to modernize their IT infrastructure, enhance operational efficiency, and deliver superior customer experiences, which significantly boosts the System Integration Market growth. The widespread adoption of cloud computing services is reshaping how businesses deploy and manage their IT resources. System integrators are in high demand to assist organizations in migrating to cloud platforms, integrating cloud-based applications with on-premises systems, and ensuring interoperability across hybrid IT environments. The scalability, flexibility, and cost-effectiveness of cloud solutions drive the need for robust system integration capabilities.

The growth of data generated by businesses presents both opportunities and challenges for System Integration Market. System integration facilitates the aggregation, processing, and analysis of vast datasets from diverse sources, empowering organizations to derive actionable insights and make informed decisions. As the demand for advanced analytics, business intelligence, and predictive modeling increases, so does the demand for sophisticated system integration solutions. The proliferation of IoT devices across industries is generating vast streams of real-time data that require integration with existing IT systems and applications. System integrators play a crucial role in connecting IoT devices, sensors, and gateways with backend systems, enabling organizations to harness the full potential of IoT for improved asset monitoring, predictive maintenance, and operational efficiency, which boosts the System Integration Market growth.

Complexity and Interoperability Challenges to limit System Integration Market growth

Integrating disparate systems, applications, and data sources often entails navigating complex technical environments with varying architectures, protocols, and standards. Achieving seamless interoperability between legacy systems and modern platforms is daunting, leading to project delays, cost overruns, and performance issues, which limits the System Integration Market growth. The inherent complexity of integration developments poses a significant restraint for both service providers and their clients, which is expected to restrain System Integration Market growth. Many organizations grapple with legacy IT infrastructure characterized by outdated technologies, monolithic architectures, and accumulated technical debt. Retrofitting legacy systems for integration with modern cloud-based platforms or emerging technologies resource-intensive and time-consuming. Legacy constraints hinder agility, scalability, and innovation, limiting the effectiveness of system integration initiatives.

System integration projects often entail substantial upfront investments in technology, resources, and expertise. Budgetary constraints and cost pressures limit organizations' ability to allocate sufficient funds for integration initiatives, leading to compromises in project scope, quality, or timelines. Random project costs and ROI uncertainties deter investment in system integration services, particularly for small and medium-sized enterprises (SMEs). Successful system integration depends not only on technical capabilities but also on organizational readiness, change management, and cultural alignment. Resistance to change, internal politics, and cultural barriers impede collaboration, communication, and stakeholder buy-in, undermining the success of integration projects. Overcoming organizational inertia and fostering a culture of innovation and agility are essential for realizing the full benefits of system integration initiatives.

System Integration Market Segment Analysis

Based on Service Type, the market is segmented into Infrastructure Integration, Application Integration, and Consulting. Infrastructure Integration segment dominated the market in 2023 and is expected to hold the largest System Integration Market share over the forecast period. Software integration focuses on the seamless integration of diverse software applications, platforms, and systems to enable data sharing, process automation, and workflow optimization. It involves integrating enterprise software solutions such as ERP (Enterprise Resource Planning), CRM (Customer Relationship Management), SCM (Supply Chain Management), and BI (Business Intelligence) systems to streamline business processes and enhance decision-making capabilities. Infrastructure Integration is essential for organizations seeking to modernize their IT infrastructure, optimize resource utilization, and enhance operational efficiency, which significantly boosts the System Integration Market growth. By integrating hardware, software, networking, data center, cloud, and security components effectively, organizations create robust, scalable, and resilient IT environments that support their evolving business needs and drive digital transformation initiatives.

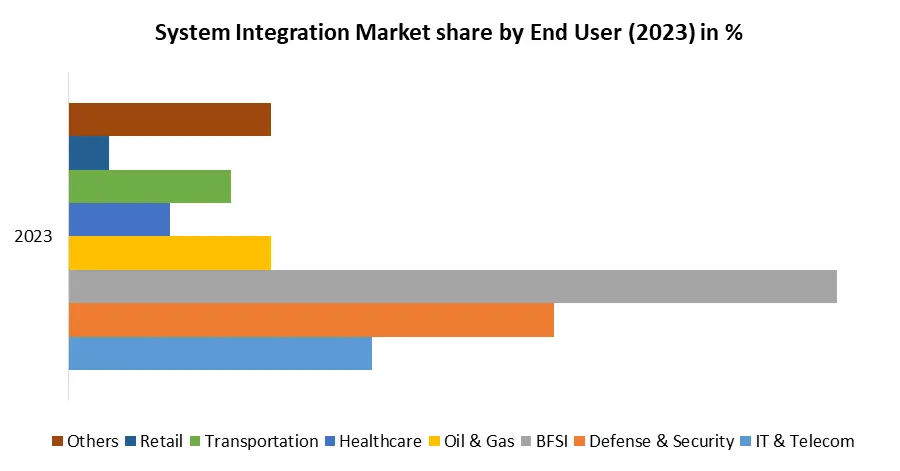

Based on End User, the market is segmented into IT & Telecom, Defense & Security, BFSI, Oil & Gas, Healthcare, Transportation, Retail, and Others. BFSI segment dominated the market in 2023 and is expected to hold the largest System Integration Market share over the forecast period. Core banking systems serve as the backbone of banking operations, managing essential functions such as customer accounts, transactions, loans, and deposits. System integrators in the BFSI segment specialize in integrating core banking platforms with other banking applications, channels, and third-party systems to ensure seamless data flow, real-time processing, and enhanced customer experiences. Regulatory compliance is a top priority for BFSI institutions, given the stringent regulations governing the industry, such as Basel III, Dodd-Frank Act, GDPR, and PCI-DSS. System integrators help BFSI organizations integrate risk management, regulatory compliance, and reporting systems with core banking systems, customer databases, and transaction monitoring platforms to ensure adherence to regulatory requirements, mitigate compliance risks, and enhance transparency and accountability.

System Integration Market Regional Insight

North America held a market share of over 35% in 2022, owing to the rising use of IoT in industrial automation and the growing adoption of cloud-based services among large organizations. The BFSI sector in the region has embraced modern-day technology, which presents significant growth prospects for the system integration market in North America. To this end, banks are taking considerable care to ensure they meet every client’s requirement. For instance, according to Bank of America, 70% of its customers use digital services for their financial needs. It help the bank to develop its client base and stay competitive in the market. The migration of organizations to these services increase the demand for system integration services in the region during the forecast period.

The growth of the system integration market in Europe is due to increased partnership/collaboration activities, which have enabled the companies operating in the European region to have access to advanced system integration solutions. For instance, in December 2023, Infosys and LKQ Europe, a European distributor of automobile aftermarket components, established a five-year cooperation. LKQ's recent strategic acquisitions, the Bengaluru-based strategic partnership seeks to improve product availability, expedite end-to-end delivery, and optimize business operations. When it comes to standardizing and integrating systems and procedures for effectiveness and advantages, Infosys set the standard.

The development of the system integration market in France is credited to governmental initiatives aimed at fostering its growth. In September 2023 when the French government proposed mandates for B2B e-invoicing. This initiative involves the collaboration of two key entities: the Direction Générale des Finances Publiques (DGFIP), responsible for public finances, and the Agence pour l'informatique financière de l'Etat (AIFE), the state financial information agency. It's important to note that the proposed revised schedule by DGFIP and AIFE remains tentative until confirmed with the announcement of the 2024 Finance Act by the government, expected no later than October 2023.

System Integration Market Scope :Inquire before buying

| System Integration Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | USD 385.75 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 13.8% | Market Size in 2030: | USD 953.46 Bn. |

| Segments Covered: | by Service Type | Infrastructure Integration Application Integration Consulting |

|

| by Enterprise Size | Large Enterprises Small & Medium Enterprises |

||

| by End-user | IT & Telecom Defense & Security BFSI Oil & Gas Healthcare Transportation Retail Others |

||

System Integration Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Leading System Integration key players include:

North America:

1. IBM Corporation: Armonk, New York, USA

2. Accenture plc: New York, USA)

3. Deloitte Touche Tohmatsu Limited: New York, USA)

4. Cognizant Technology Solutions Corporation: Teaneck, New Jersey, USA

5. Hewlett Packard Enterprise Company: San Jose, California, USA

Europe:

6. Capgemini SE: Paris, France

7. Atos SE: Bezons, France

8. T-Systems International GmbH: Frankfurt, Germany

Asia-Pacific:

9. Tata Consultancy Services Limited (TCS): Mumbai, Maharashtra, India

10. Infosys Limited: Bengaluru, Karnataka, India

11. NEC Corporation: Minato, Tokyo, Japan

12. HCL Technology Limited: Noida, Uttar Pradesh, India

13. Tech Mahindra Limited: Pune, Maharashtra, India

14. Wipro Limited: Bengaluru, Karnataka, India

15. Fujitsu Limited: Tokyo, Japan

Frequently asked Questions:

1] What segments are covered in the Global System Integration Market report?

Ans. The segments covered in the System Integration Market report are based on, Service Type, Enterprise Size, End User, and Regions.

2] Which region is expected to hold the highest share of the Global System Integration Market?

Ans. The North America region is expected to hold the highest share of the System Integration Market.

3] What is the market size of the Global System Integration Market by 2030?

Ans. The market size of the System Integration Market by 2030 is expected to reach USD 953.46 Bn.

4] What was the market size of the Global System Integration Market in 2023?

Ans. The market size of the System Integration Market in 2023 was valued at USD 385.75 Bn.

5] Key players in the System Integration Market.

Ans. Capgemini, Fujitsu, Deloitte Touche Tohmatsu Limited, Infosys, etc.