Refractories Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

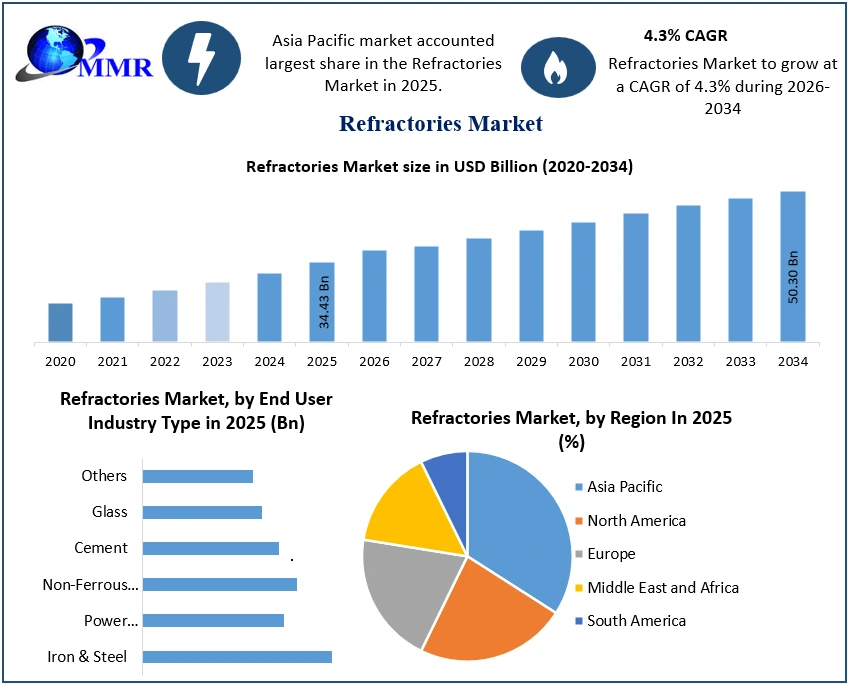

The Refractories Market size was valued at USD 34.43 Billion in 2025 and the total Refractories revenue is expected to grow at a CAGR of 4.3% from 2026 to 2034, reaching nearly USD 50.30 Billion.

Refractories Market Overview

Refractory materials, essential in the refractories market, refer to inorganic, non-metallic substances capable of withstanding extreme temperatures of 1580°C or above. These materials include natural ores and specially manufactured products, created through specific processes to meet the demands of high-temperature applications. Known for their high-temperature mechanical strength and market stability, refractory materials ensure good volume stability under intense heat, making them indispensable across various industries. The refractories market size of refractory materials reflects their critical role in supporting industries with high-temperature equipment, such as steel, cement, and glass production, driven by ongoing demand and market analysis of applications that prioritize longevity and efficiency in extreme environments.

Recent Developments in Refractories Market

To know about the Research Methodology :- Request Free Sample Report

Refractories Market Dynamics

The rising demand and supply dynamics boost the growth within the refractories market.

As industries such as steel, cement, and glass manufacturing continue to expand, the need for high-performance refractory materials grows.

For instance, in 2022, global steel production reached approximately 1.95 billion metric tons, directly impacting the consumption of refractories used in steelmaking processes, which are essential for withstanding high temperatures and corrosive environments. The cement industry is also a major contributor to the demand for refractories, particularly in regions like Asia-Pacific, where infrastructure development is booming. Additionally, supply chain factors, including the volatility of raw material prices, have a notable impact on production costs.

In 2021, bauxite prices surged by 30%, affecting the cost structure for manufacturers and potentially leading to increased prices for refractory products in the market.

A pertinent example of market growth can be seen in Mexico, where the revenue from the refractory products manufacturing industry was approximately USD 185 million in 2018, with projections indicating it will reach around USD 250.16 million by 2025. This statistic underscores the robust growth potential in the region. Innovation in the refractory industry further enhances material performance and expands applications. Recent advancements include the development of ultra-low cement castables, which improve thermal efficiency and durability while reducing environmental impact. Sustainability initiatives are gaining momentum, with industries increasingly seeking eco-friendly alternatives to traditional refractory materials. The shift towards renewable energy sources and the push for carbon-neutral production processes are prompting the adoption of advanced refractories in sectors like energy and petrochemicals.

For instance, the growing trend of utilizing gasification technology in power plants highlights the need for refractories that can withstand extreme thermal and mechanical stresses. This combination of demand from diverse industrial applications, coupled with innovative solutions and sustainability initiatives, underscores the multifaceted growth factors shaping the refractory industry.

Latest Trends in the Research and Development of Refractories

Recent research trends in the refractories industry, particularly those presented at UNITECR 2019, have highlighted a significant focus on unshaped refractories. Many researchers concentrated on bonding structures and grain properties, aiming to develop high-functionality unshaped refractories by leveraging the characteristics of compounds such as MgO and SiO2. One notable trend is the acceleration in the development of low-carbon refractories, driven by the need of ultra-low-carbon steel production. Researchers are striving to improve thermal shock resistance by optimizing the structure of matrices and chemical compounds that exhibit properties of both ceramics and metals. This involves innovative approaches such as incorporating catalytic compounds and nanoparticles to enhance the microstructural properties of refractories. The effective utilization of numerical analysis and simulations has become essential for understanding material behavior in hot working processes, structural mechanics, and the stresses caused by thermal fluctuations, with many research contributions emerging from Europe.

In addition to advancements in unshaped refractories, specific innovations in materials and microstructure have gained attention. For instance, researchers are exploring the effects of different grain shapes on the performance of unshaped refractories, with studies revealing that splintered coarse grains exhibit higher durability compared to cubic grains. The use of additives with catalytic functions, such as Fe2O3 and nanoalumina, has proven effective in enhancing mechanical properties and thermal shock resistance. As industries increasingly prioritize clean steel production, there is a growing demand for low-carbon refractories. Efforts are being made to replace graphite with Ti-MAX phases to mitigate oxidation issues, while the addition of nanocarbon has been shown to improve the microstructure and overall performance of refractories. Furthermore, innovative carbon-free, unburned alumina-magnesia bricks have been developed, demonstrating comparable mechanical properties to fired products and showcasing superior performance in ladle applications. Overall, these trends indicate a robust commitment to innovation and sustainability within the refractories market, as industry players adapt to evolving demands and environmental considerations.

Refractories Market Segment Analysis

Based on the Form, the market is segmented into Unshaped Refractories and Shaped Refractories. The unshaped Refractories segment is expected to grow rapidly at a high CAGR during the forecast period 2026-2034. Unshaped refractories are increasingly replacing traditional refractories in applications that demand high-temperature resistance. Monolithic linings, also known as unshaped refractories, reduce batch delays and enable extensive repairs with minimal downtime. The unshaped refractory has a high purity, compactness, and gradation that is reasonable. It can be produced into a monolithic refractory, which is a continuous lining and structure.

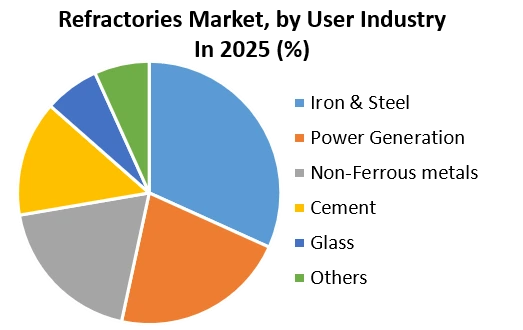

Based on the End-Use Industry, the market is segmented into Iron & Steel, Power Generation, Non-Ferrous metals, Cement, Glass, and Others. The iron & Steel segment is expected to hold the largest refractories market share of 65% by 2034. Internal linings of iron and steel furnaces, furnaces for heating steel before further processing, vessels for holding and transporting metal and slag, flues or stacks through which hot gases are conducted, and other applications are among the most common uses of refractories in the iron and steel industry.

According to the World Steel Association, global steel demand reached 1.76 million metric tonnes in 2025 and is expected to reach 1.81 million tonnes by 2034, representing a 1.7% increase. This reflects the global market's demand outlook, which is important in boosting steel output. These are the key drivers that are expected to boost the growth of this segment during the forecast period.

Refractories Market Regional Analysis

The Asia Pacific Refractories Market is expected to dominate the global refractories market during the forecast period 2026-2034 with the largest market share. China has the largest economy in the Asia-Pacific region in terms of GDP. Even with the economic disruption created by the country's trade war with the United States, the country's GDP grew by roughly 6.1% in 2025. In comparison to the previous year, China's economic growth rate in 2025 was expected to be mild. Due to the local availability of raw materials such as magnesite, China dominates the refractories industry in terms of consumption and production.

In China, the building industry grew rapidly in 2025. The country is the world's largest construction market, accounting for 20% of all worldwide construction investments. In the next five years, till 2030, the country will invest USD 1.43 trillion in significant development projects. The Shanghai Plan, according to the National Development and Reform Commission (NDRC), calls for a total investment of USD 38.7 billion over the next three years. Even though cement production has decreased over the last half-decade, the above-mentioned causes are expected to improve demand for metals, cement, and other market-related items, resulting in a positive outlook for refractories.

| Refractories Market Consumption Rate by Industry in India | |||

|---|---|---|---|

| Industry | Percentage (%) of Refractory Consumption | ||

| Steel | 69.2% | ||

| Cement | 7% | ||

| Ceramics | 6% | ||

| Glass | 4.8% | ||

| Chemicals | 4% | ||

| Non-Ferrous Metals | 3% | ||

| Others | 6% | ||

The European Refractories Market is also expected to hold the major share of the global market. The region has a long history of refractories production and application along with several manufacturers who are actively investing in research and development to improve the performance and lifespan of refractory products and end-user industries that heavily rely on refractories. In the region, efforts like ReStaR (Review and Improvement of Testing Standards for Refractory Products) have been established to guarantee the region's current refractory testing standards are reliable and precise.

Refractories Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 18 April 2026 | Imerys | The company signed an agreement to acquire Great Lakes Minerals, a prominent U.S.-based processor and distributor of industrial minerals. | This transaction expands the company's North American raw-material footprint for high-temperature refractory applications, integrating crucial supplies of calcined bauxite, mullite, and fused alumina. |

| 12 March 2026 | HarbisonWalker International (HWI) | The manufacturer officially opened its new Fulton lightweight monolithics facility in Missouri, featuring vertically integrated operations with direct access to local clay reserves. | The automated plant scales up the domestic commercial supply chain and includes a purpose-built furnace to drive advanced green aggregate production with robotic packaging systems. |

| 17 November 2025 | RHI Magnesita | A European technology consortium led by the company unveiled RAPTOR, an AI-powered mobile multi-sensor sorting system. | This automated innovation converts mixed, end-of-life materials into high-grade secondary raw resources to drastically improve refractory recycling and sustainability targets. |

| 23 July 2025 | HarbisonWalker International (HWI) | The firm entered into a strategic manufacturing partnership with Electrified Thermal Solutions to develop specialized refractories. | The partnership focuses on producing electrically conductive firebricks customized for high-temperature grid-scale thermal batteries. |

| 27 June 2025 | RHI Magnesita | The corporate group announced a strategic joint venture with US-based mineral processor BPI, Inc. | The initiative establishes a robust circular economy model in North America by maximizing the reclamation and reuse of spent lining raw materials. |

| 18 June 2025 | INTOCAST | The producer commissioned a new high-performance tempering kiln at its industrial plant located in Oberhausen, Germany. | The capital expansion actively modernizes European production lines to optimize the manufacturing output of heavy-duty magnesia-carbon (MgO-C) shaped bricks. |

Refractories Market Competitive Landscape

This section of the report includes investment plans of Refractory's key competitors and strategies to increase their presence in the industry. The Refractories Market report includes a detailed analysis of the collaborations, mergers, acquisitions, and joint ventures taking place in the industry.

The RHI Magnesita completed the acquisition of Seven Refractories on July 17, 2023. This has created new opportunities in the development of low-CO2-emitting manufacturing technologies. Seven Refractories is a specialist supplier of alumina refractory mixes, serving customers in the iron and steel, aluminum, cement, and non-ferrous metals industries, with a proven track record of consistent growth in these sectors. Chosun Refractories Co., Ltd. highly focuses on researching and developing large-scale furnaces, differentiated from small-scale furnaces in terms of operation and structure in response to customer demand. They have successfully developed a two-way grate for large-scale furnaces with their own technology.

Refractories Industry Ecosystem:

Refractories Market Scope: Inquiry Before Buying

| Refractories Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 34.43 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 4.3% | Market Size in 2034: | USD 50.30 Bn. |

| Segments Covered: | by Alkalinity | Acidic & neutral Basic |

|

| by Form | Monolithic & Unshaped Bricks & Shaped |

||

| By End User Industry | Iron & Steel Power Generation Non-Ferrous metals Cement Glass Others |

||

Refractories Market, Key Players

North America:

1. RHI Magnesita

2. HarbisonWalker International (HWI) Inc.

3. Morgan Advanced Materials PLC

4. Coorstek Incorporated

5. Lhoist Group

Europe:

1. Saint-Gobain S.A

2. Vesuvius PLC

3. Imerys SA

4. Krosaki Harima Corporation

5. Refratechnik Holding GmbH

Asia Pacific:

6. Shinagawa Refractories Co., Ltd.

7. Puyang Refractories Group Co., Ltd.

8. Chosun Refractories Co., Ltd.

9. IFGL Refractories Ltd.

10. Luyang Energy-Saving Materials Co., Ltd.

Middle East & Africa:

11. Corning Incorporated

12. Resco Products, Inc.

13. Zircar Ceramics, Inc.

South America:

14. RHI Magnesita

15. Vesuvius PLC

16. Others

Frequently Asked Questions:

1] What segments are covered in the Global Refractories Market report?

Ans. The segments covered in the Global Refractories Market report are based on Alkalinity, Form, and End-Use Industry.

2] Which region is expected to hold the highest share in the Global Refractories Market?

Ans. Asia Pacific is expected to hold the highest share of the Global Refractories Market.

3] Who are the Refractory Market key competitors in the Industry?

Ans. RHI Magnesita, Saint-Gobain S.A, Shinagawa Refractories Co. Ltd, and Krosaki Harima Corporation are the key players in the Global Refractories Market.

4] Which segment is expected to hold the largest Refractories market share by 2034?

Ans. The iron and Steel end-use industry segment hold the largest market share in the Global Refractories market by 2034.

5] What is the market size of the Global Refractories market by 2034?

Ans. The market size of the Global Refractories market is USD 50.30 Bn by 2034.

6]. What was the Global Refractories Market size in 2025?

Ans: The Global Refractories Market size was USD 34.43 Billion in 2025.