Cancer Diagnostics Market Size by Product Type, Test Type, Application, End-User and Region - Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2030

Overview

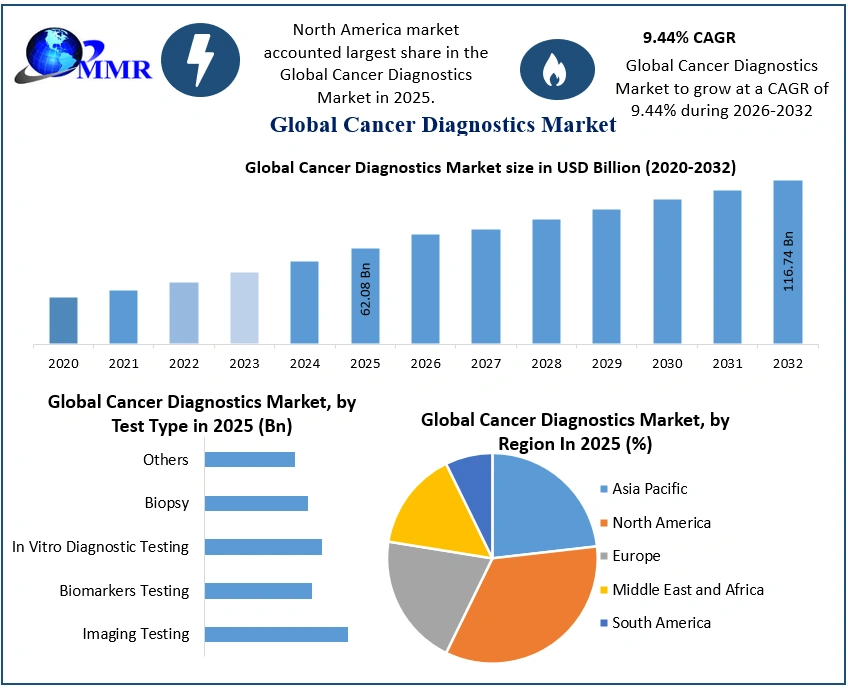

The Cancer Diagnostics Market size was valued at USD 62.08 Billion in 2025 and the total Cancer Diagnostics revenue is expected to grow at a CAGR of 9.44% from 2026 to 2032, reaching nearly USD 116.74 Billion by 2032.

Cancer Diagnostics Market Overview:

Cancer diagnosis are the methods used to find and diagnose cancer, which help to choose early treatment and manage patient care. Advances in technology and the growing need for accurate and early detection techniques are driving the dynamic and changing global cancer diagnostics market. Cancer diagnostic industry leaders such as Abbott Laboratories, Siemens Healthineers and Roche Diagnostics are always at the forefront of innovation to meet the strict regulatory requirements set by organizations such as the FDA and EMA. For example, the FDA-approved Guardant Health Guardant360 liquid biopsy examines circulating tumor DNA to provide personalized treatment programs based on genetic abnormalities.

Significant potential customers have emerged in the market, such as combining artificial intelligence with liquid biopsy for early diagnosis, improving the patient experience through data sharing and remote monitoring, and developing personalized therapy. Recent advances include a deep learning system created by MIT to use CT scans for early detection of lung cancer and the deployment of Illumina's advanced sequencing technologies for accurate genomic profiling.

Due to their common use in diagnostic procedures, consumables dominate the market, , but instruments are growing rapidly as a result of improvements in analytical technology. Although biomarker testing is becoming increasingly popular for individualized treatment decisions, imaging testing such as PET-CT and MRI are still essential for cancer detection and monitoring. Geographically, the North American cancer diagnostics market is leading due to the increasing incidence of cancer and the continuous development of diagnostic technology. Rising incidence of cancer and encouraging government initiatives are driving the rapid growth of the market in Asia Pacific.

The competitive landscape is driven by continuous innovation and strategic alliances between major competitors to expand product range and increase market share. Companies such as Exact Sciences and Guardant Health developing non-invasive liquid biopsy techniques are gaining more recognition. The overall cancer diagnostics market is expected to grow due to increasing cancer prevalence, technological advances, and global initiatives to improve patient outcomes and diagnostic accuracy.

To know about the Research Methodology :- Request Free Sample Report

Global Cancer Diagnostics Market Dynamics:

Integrating liquid biopsy and artificial intelligence for early cancer diagnosis

Improving the patient experience, data sharing and remote monitoring, personalized medicine, early detection and intervention, and closing disparities in cancer care are all key market opportunities. These opportunities are driven by advances in technology, aging populations and the growing burden of cancer on global health systems. Overall, the cancer diagnostics market has significant opportunities for growth and innovation that can improve patient outcomes and promote equity in diagnosis and treatment. New product launches and mergers and acquisitions of key players in the industry are propelling the cancer diagnostics market growth.

For example, the breast cancer segment has grown significantly due to increased research to develop improved screening tools, while the lung cancer segment is expected to grow rapidly in the coming years due to the availability of technologically advanced diagnostic products, new product launches, and mergers. and acquisitions. Together, these variables present opportunities in the cancer diagnostics market. Technological advances, especially the inclusion of artificial intelligence, lead to earlier-stage cancer diagnosis

1. On January 5, 2024, MIT researchers announced that they are developing a deep learning algorithm to examine low-dose CT scans to predict lung cancer up to six years in advance.

2. In 2023, Illumina launched new sequencing platforms and assays that improve the accuracy and efficiency of genomic profiling in cancer research and clinical applications. These developments support personalized medicine approaches by providing oncologists with comprehensive genomic information.

3. In 2021, Following the acquisition of Varian Medical Systems, Siemens Healthineers expanded its oncology portfolio with integrated diagnostic and treatment solutions. In 2023, Siemens Healthineers launched new imaging and radiation therapy technologies that improve the accuracy and efficiency of cancer treatment planning and monitoring. These innovations aim to optimize oncology therapies and improve patient outcomes.

4. In 2023, Guardant Health, a pioneer in liquid biopsy testing, launched new products, such as Guardant Reveal. Guardant Reveal is designed to detect colon cancer early and monitor recurrence using proprietary digital sequencing technology to analyze ctDNA from blood samples. This launch represents Guardant Health's commitment to advancing liquid biopsy technology to improve cancer diagnosis.

Navigating the regulatory landscape is challenging the Companies growth providing cancer diagnostics.

Managing the regulatory landscape is a significant challenge for cancer diagnostic companies, especially when developing and commercializing innovative diagnostic tests such as liquid biopsies. Before new diagnostic technologies are licensed for clinical use, regulatory bodies such as the FDA in the United States and the EMA in Europe set strict standards to ensure their safety, efficacy, and clinical value.

For instance, Companies developing liquid biopsy diagnostics must provide compelling clinical evidence through rigorous clinical trials to gain regulatory approval. The purpose of these studies is to evaluate the accuracy of the test in detecting specific cancer-related biomarkers, sensitivity to distinguish between cancer and non-cancerous conditions, and therapeutic value in guiding treatment decisions.

1.One such example is Guardant Health's Guardant360 Liquid Biopsy. Guardant360 analyzes circulating tumor DNA (ctDNA) in the blood to detect genetic changes in solid tumors and guide personalized treatment plans. Guardant Health conducted rigorous clinical validation studies using thousands of patient samples from various cancer types to obtain FDA certification as a companion diagnostic. The purpose of these studies was to show the accuracy of the test in identifying certain mutations that predict response to targeted drugs, allowing oncologists to choose the best treatment for their patients.

2. In Europe, companies such as Roche and Qiagen face strict scrutiny of their diagnostic products by the EMA. For example, Roche's Cobas EGFR Mutation Test v2 for non-small cell lung cancer showed that it can accurately detect specific mutations in the EGFR gene in clinical trials, confirming its effectiveness compared to traditional tissue biopsy methods.

Navigating the regulatory landscape is a complex and rich resource, but critical to ensuring that new cancer detection technology meets stringent requirements for safety, efficacy, and clinical benefit. Companies that effectively address these barriers will advance the development of precision medicine and improve outcomes for cancer patients worldwide.

Global Cancer Diagnostics Market Segment Analysis:

By Product Type, according to MMR analysis, the Consumables segment dominated the global cancer diagnostics market in 2025 and is expected to continue its dominance due to Volume and Frequency of Use, its cost structure, and technological advancements. Cancer diagnostic consumables include reagents, test kits, and disposable supplies used in various diagnostic tests. These accessories are in high demand and are frequently used in laboratories and diagnostic centers around the world. This high usage rate plays a role in determining their market share. Consumables form an important part of the total cost structure of diagnostic procedures. Although the initial cost of the instruments is higher, there is a constant need for consumables for testing purposes. This constant need for consumables ensures a constant flow of income for producers and suppliers.

The Instruments segment is expected to grow at fastest rate during the forecast period. Analytical instruments are devices or equipment that help automate the diagnostic process and combine samples and reagents. Pathology laboratories use tools and robots to measure and detect infectious bacteria, blood antigens and viral load. Increasing technical improvements will boost growth during the forecast period.

For example, in March 2022, Illumina announced TRUSIGHT, a comprehensive test set for oncology diagnosis, the IVD test, which is used to profile various cancers in Europe.

By Test Type, according to MMR Analysis, the Imaging Testing held the largest market share of the global cancer diagnostic market in 2025. These diagnostic methods are critical in detecting, diagnosing, staging, monitoring, and evaluating cancer recurrence in various cancer types. Advanced techniques such as PET-CT (positron emission tomography - computed tomography), MRI (magnetic resonance imaging), CT (computed tomography), ultrasound, and others are used in imaging procedures to obtain detailed images of the internal body that provide important information. to doctors about the type and progression of tumors.

Breast MRI is one of the most important types of imaging that best describes the revolutionary nature of oncology imaging. This technique uses a combination of radio waves and strong magnets to create high-resolution cross-sectional images of breast tissue. When a standard mammogram or ultrasound may not provide enough information, such as evaluating dense breast tissue or detecting small lesions that are not palpable, a breast MRI is particularly useful.

The accuracy, speed and convenience of patient diagnosis have improved due to the continued growth of imaging techniques. Advances such as functional MRI (fMRI), which evaluates tissue function in addition to structure, and PET imaging, which uses new radioactive tracers that target specific biochemical pathways in cancer, are increasing the diagnostic effectiveness of imaging tests.

Biomarker testing is widely used in various types of cancer, indicating its fastest growing popularity in the global cancer diagnostic market. For example, risk assessment and treatment methods have completely changed with the introduction of genetic biomarkers such as BRCA1 and BRCA2 mutations in breast and ovarian cancer. In addition to identifying the most vulnerable, these biomarkers also help to choose preventive measures such as enhanced surveillance or prophylactic surgery.

By Application, according to MMR report in 2025, Breast Cancer dominated the global cancer diagnostic market due to intensive research and the development of advanced screening methods such as MRIs, mammograms, and biomarker tests such as HER2/neu and hormone receptors. These initiatives aim to increase early detection rates and improved patient outcomes through early intervention.

Lung cancer is expected to increase its market share while improving its diagnostic capabilities during the forecast period. Since lung cancer is one of the most common and deadly malignancies in the world, efforts have been made to create high-tech advanced devices that help detect the disease at an early stage. Lung cancer sales have grown due to new product launches, smart mergers and acquisitions, and the availability of state-of-the-art diagnostic equipment.

1. According to the World Cancer Research Fund, the combined incidence of lung cancer cases and breast cancer cases accounted for approximately 25 percent of all new cancer cases in 2020, underscoring the scale of the global cancer landscape. The discovery and use of biomarkers and the latest diagnostic tools are essential to improve the survival and quality of life of cancer patients as these cases spread worldwide.

2. In October 2023, FirstLook Lung, published by DELFI Diagnostika, is an example of this progress. FirstLook Lung, which uses machine learning-based liquid biopsy technology, is a major advance in cancer diagnosis. By examining tumor DNA (ctDNA) circulating in the blood, this blood test aims to detect lung cancer at an early stage and can provide information about genetic changes and mutations associated with lung cancer. Compared to traditional tissue biopsies, such liquid biopsies offer a non-invasive and potentially more sensitive approach that allows for early detection and individualized treatment plans.

Global Cancer Diagnostics Market Regional Analysis:

North American Cancer Diagnostic Market had a significant market share in 2025, showing dominance in the medical diagnostics market. This leading position is largely due to several factors that have greatly accelerated the growth of the cancer diagnostics market in the region.

Cancer rates are increasing in the United States and Canada, increasing the need for improved detection tools. The increasing incidence of cancer had highlighted the need for effective early detection and diagnostic tools. The demographic trends have encouraged North American medical device companies to increase their efforts to create innovative diagnostic devices. These developments aim to improve patient outcomes and enable early intervention in addition to increasing accuracy and reliability.

In July 2022, the Canadian company Nanostics Inc. initiative that launched a clinical trial focused on bladder cancer detection. The research focus was on Nanostics' ClarityDX diagnostic platform, which aims to identify the best biomarkers for the early detection of bladder cancer using a liquid biopsy that requires little physical contact. This technique could completely change the way bladder cancer is recognized and treated, as it represents a major advance in diagnostic capabilities.

Another important factor influencing the growth of the North American market was the conscious focus on new releases. Bringing new diagnostic devices to the market encourages innovation and market competitiveness and expands the range of tools available. Such development was necessary to meet the changing demands of patients and healthcare professionals, especially in the field of oncology, where rapid and accurate diagnosis had a significant impact on treatment outcomes.

During the forecast period, the cancer diagnostics market in Asia Pacific is expected to grow rapidly, mainly due to the growth of cancer and healthcare reforms. Lung cancer is the most common type of cancer, with 4.8 million new cases expected in China alone. This high impact shows the urgency of the need for advanced diagnostic solutions, which in turn is accelerating the growth of the market.

The governments of Singapore and Taiwan also support market development through financing and favorable regulatory conditions. Together, these elements are pushing large global companies into the Asia-Pacific region, where they will increase the industry's growth prospects and enable the adoption of modern diagnostic technology.

Global Cancer Diagnostics Market Competitive Landscape:

The competitive landscape in the global cancer diagnostics market has been characterized by competitive innovation and strategic growth of key competitors. Leading companies such as Roche Diagnostics, Abbott Laboratories and Siemens Healthineers have maintained significant market shares by constantly developing diagnostic technology.

1. Roche Diagnostics has expanded its offering by introducing cutting-edge oncology diagnostics that improve personalized treatment options.

2. Abbott Laboratories has used its established platforms, such as Alinity and Vysis technologies, to improve its molecular diagnostic capabilities in cancer diagnosis.

Emerging companies such as Exact Sciences Corporation and Guardant Health have gained popularity with their state-of-the-art non-invasive liquid biopsy method. These technologies are being adopted in clinical settings worldwide due to their promising results in early cancer detection.

Partnerships and collaborations have also been important tactics used by companies to increase their market presence. Thermo Fisher Scientific has collaborated with other academic institutions to develop advanced genetic profiling tools for precision oncology. Such partnerships facilitate the creation of accurate diagnostic instruments that can be used to study genetic and molecular markers associated with cancer.

Overall, technological innovation, business alliances and focus on expanding product offerings have shaped the evolving needs of the global cancer diagnostics market.

1. In October 2023, QIAGEN and Myriad Genetics signed a product development agreement to create additional diagnostic tests for cancer treatment.

2.In June 2023, Exact Sciences announced a partnership with the Broad Institute of MIT and Harvard to improve patient care by improving access to genetic information. The partnerships aim to provide smarter solutions both before and during cancer treatment by combining cancer information. important people in the field using cutting edge technology.

3. In September 2022, Major US distribution partner and Precipio, Inc. signed a distribution agreement for HemeScreen. The company continues to take a multi-pronged approach to expanding distribution of HemeScreen, focusing on referral laboratories, national and regional hospital networks, and physician-owned laboratories.

Cancer Diagnostics Market Scope: Inquiry Before Buying

| Global Cancer Diagnostics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 62.08 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 9.44% | Market Size in 2032: | USD 116.74 Bn. |

| Segments Covered: | by Product Type | Instruments Consumables |

|

| by Test Type | Imaging Testing Biomarkers Testing In Vitro Diagnostic Testing Biopsy Others |

||

| by Application | Breast Cancer Colorectal Cancer Cervical Cancer Lung Cancer Prostate Cancer Skin Cancer Blood Cancer Kidney Cancer Liver Cancer Pancreatic Cancer Ovarian Cancer Others |

||

| by End-User | Hospitals and Clinics Diagnostic Laboratories Diagnostic Imaging Centers Research Institutes |

||

Cancer Diagnostics Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Major Players in the Cancer Diagnostics Market

1. Abbott Laboratories (USA)

2. Roche Diagnostics (Switzerland)

3. Siemens Healthineers (Germany)

4. Thermo Fisher Scientific (USA)

5. Agilent Technologies, Inc. (USA)

6. Becton, Dickinson, and Company (USA)

7. Sysmex Corporation (Japan)

8. GE Healthcare (USA)

9. Qiagen (Germany)

10. PerkinElmer (USA)

11. Illumina (USA)

12. Bio-Rad Laboratories (USA)

13. Myriad Genetics (USA)

14. Hologic (USA)

15. Cepheid (Danaher Corporation) (USA)

16. Exact Sciences (USA)

17. Gaurdant Health (USA)

18. Foundation Medicine (a part of Roche Group) (USA)

19. NeoGenomics (USA)

20. Philips Healthcare (Netherlands)

Frequently Asked Questions

1. What is the projected market size & growth rate of Cancer Diagnostics Market?

Ans-The Cancer Diagnostics Market size was valued at USD 62.08 Billion in 2025 and the total Cancer Diagnostics revenue is expected to grow at a CAGR of 9.44% from 2026 to 2032, reaching nearly USD 116.74 Billion by 2032.

2. What is the key driving factor for the growth of Cancer Diagnostics Market?

Ans- Rising public awareness and supportive government measures are driving the market growth.

3. What are the top players operating in Cancer Diagnostics Market?

Ans- Abbott Diagnostics, Agilent Technologies, Inc., Becton, Dickinson and Company are some of the top players operating in the Cancer Diagnostics Market.

4. Region accounted for the largest Cancer Diagnostics Market share?

Ans- Because of factors such as high awareness about early detection and cancer diagnosis, rising prevalence of types of cancer, the cancer diagnostics market in North America is expected to account for the largest revenue share during the forecast period.

5. What makes Asia Pacific a Lucrative Market for Cancer Diagnostics Market?

Ans- High cancer prevalence, improved healthcare infrastructure, rising disposable income, increased awareness of early cancer detection, and favourable government efforts are all contributing to Asia Pacific's market growth.