Mammography Market Size by Product, Technology, Modality, End-use, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2029

Overview

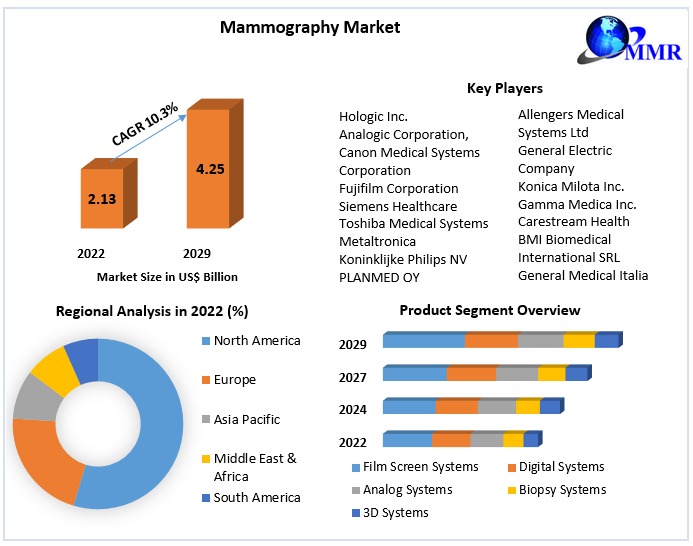

Mammography Market was valued at USD 2.13 Billion in 2022, and it is expected to reach USD 4.25 Billion by 2029, exhibiting a CAGR of 10.3% during the forecast period (2023-2029)

Mammography Market Overview:

The Global Mammography Market is segmented by product and technology. Based on product, the market is segmented into film screen systems, digital systems, analog systems, biopsy systems, and 3d systems. Based on technology, the market is segmented into breast tomosynthesis, CAD, and digital. On region, the market is segmented into North America, Asia Pacific, Europe, Middle East & Africa, and South America. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The growing breast cancer cases and increasing demand for early-stage diagnosis among patients are key factors expected to drive the need for the mammography market during the forecast period. Some of the crucial factors estimated to drive the market growth include the growing government initiatives to support clinical interpretation and increased access to breast cancer screening systems. The Health Resources and Services Administration has announced a healthcare program to increase the screening procedures in medically underserved areas, due to this breast cancer diagnosis initiative the market is estimated to witness a significant growth.

COVID-19 Impact on Mammography Market

Due to COVID-19 pandemic, the mammography market witnessed reductions in cancer management visits, cancer screening, and cancer procedures all around the world. Mammograms reduced to a drastic level up to 92.3% in some areas of U.S. In 2022, the number of women examined for breast cancer was approximately 38.8 million, suggesting that end number of women in the U.S. may have delayed or missed screenings due to the COVID-19. This reduction in the screening volume caused by the pandemic has presented radiologists with further challenges.

An investigation into the effects of delayed cancer detection caused by COVID-19 was conducted in the UK and published in the Lancet Oncology in March 2021. Over 100,000 patients with breast, colorectal, esophageal, or lung cancer were included in the study. The study discovered that the COVID-19 pandemic will significantly lower cancer survival rates at 1 and 5 years due to a shortage of screening services. The mammography market was restrained due to lockdowns which caused screening services to be slightly disrupted, which decreased the demand for mammography devices.

Mammography Market Dynamics

Rising Occurrence of Breast Cancer: One of the main reasons of the mammography market's growth is the rising prevalence of breast cancer in the world. For example, according to a Globocan report, breast cancer had a prevalence rate of 11.7 percent, making it the most dominant type of cancer. The same survey found that Asia had the biggest number of affected people 3,218,496 (41.3%), followed by Europe 2,138,117 (27.4%), and North America 1,189,111 in terms of the five-year estimated prevalence for both sexes (15.3 %).

Furthermore, the WHO estimates that 627,000 women across the globe died from breast cancer in 2022, and that the incidence of breast cancer is greater among women in developed nations than in developing ones. Similar to this, according to Cancer Organization India, 25.0% of all female cancer cases in 2022 included the mouth and breast. Additionally, the Susan G. Komen Breast Cancer Foundation, Inc. estimates that 41,760 women will lose their lives to breast cancer in 2019.

Additionally, breast cancer was one of the most common cancers in South Africa in 2022 and one of the main causes of death, according to the South African Journal of Radiology. Because mammography machines may be used for diagnostic reasons, the rising prevalence of breast cancer is one of the major factors influencing the demand for these devices. Moreover, a significant share of women may live to be 60 or older due to the growing global population. About 78 percent of all breast cancer-related deaths in women over 60 are women. The high incidence and mortality rate of breast cancer in this age group suggests that there is a sizable unmet need for breast cancer diagnostics. The necessity for mammography will probably increase as more incidents and fatalities occur. Thus, it is expected that during the forecast period, the growing elderly population would drive market expansion.

Development in Mammography Devices: It is estimated that the release of new items would increase consumer acceptance. Early mammography technologies only produced 2D pictures of the breast, which had implications for interpretation quality. Craniocaudal (CC) and Mediolateral-Oblique (MLO) pictures are produced by 2D mammography systems. Due to tissue overlap and calcifications, which conceal malignant lesions, the flat appearance of these pictures makes it challenging for doctors to interpret images and diagnose tumours. A 3D picture of the breast may be obtained thanks to a new 3D-based technique called Digital Breast Tomosynthesis (DBT). Radiologists may now scan the breast slice by slice and spot anomalies that 2D pictures would have hidden.

Mammography Market Segment Analysis

Based on product, the market is segmented into film screen systems, digital systems, analog systems, biopsy systems, and 3d systems. During the forecast period, the digital systems segment is expected to dominate the market. Digital systems segment had a revenue share of more than 60% in 2022. One of the key reasons expected to drive the growth of the market is the rising need for technologically advanced breast cancer screening systems. A rise in demand for the 3D system was caused by government-issued Acts, such as the Medical Imaging Modernization Act, 2022, intended to foster technical breakthroughs. Additionally, the segment is growing as a result of its broad commercial availability and increased demand among healthcare professionals. General Electric Company and Siemens Healthcare Private Limited are two of the prominent players in this market segment (GE Healthcare).

With a CAGR of 12.2%, the 3D systems segment is estimated to grow at a highest rate during the forecast period. This is due to a number of benefits; hospitals & diagnostic clinics are converting to 3D systems as 2D systems are frequently inadequate in identifying every indication of cancer, leading to a rise in the demand for extra screenings, which in turn raises the cost of diagnostics as a whole. Due to technical advantages including improved breast cancer detection rates, the capacity to handle higher operation volumes, and a more favourable reimbursement environment, 3D systems are now widely used.

Moreover, leasing contracts for 3D mammography systems are becoming increasingly common. End-users might pay a defined amount under rental contract arrangements for each 3D mammogram performed using free 3D mammography technology offered by manufacturers. This makes it possible for diagnostic centres and hospitals with limited resources to use this cutting-edge breast imaging equipment. Additionally, some nations have started offering free mammograms in recent years. The use of 3D mammography equipment enables the most precise detection of breast cancer in these public mammography screening programmes. Therefore, it is estimated that the above factors will contribute to the segment's quick rise in upcoming years.

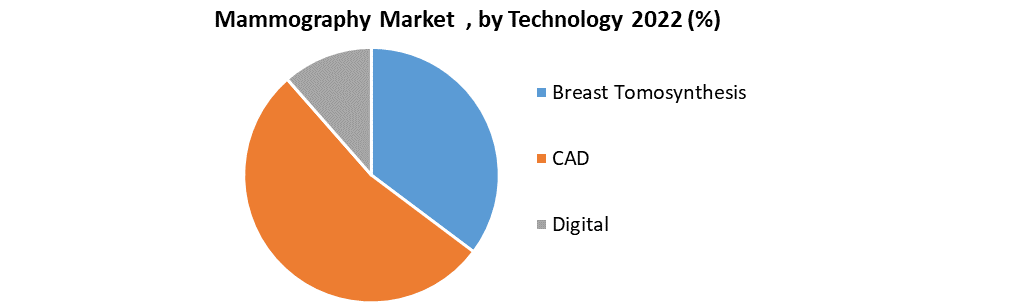

Based on technology, the market is segmented into breast tomosynthesis, CAD, and digital. Due to the numerous benefits of the technology, the digital mammography technology segment had the greatest revenue share in 2022 at over 66.0 percent. Instead of utilising X-ray films to analyse breast tissue for the presence of malignancies, digital mammography is a specialised and advanced kind of mammography. The screening method of choice for most nations has been traditional screen-film mammography (SFM) with a high spatial resolution. A rising number of nations are switching to these newer methods, nevertheless, as a result of digital mammography's greater representation of low-contrast objects, wider dynamic change, and improved diagnostic quality of pictures, particularly when assessing denser breasts.

They also have the additional advantage of having portable soft-copy reading and soft-copy visual displays. In many countries, including the U.K., mammography screening is now done digitally, which offers improved accuracy, higher quality, and more efficiency. Digital mammography is now the accepted screening technique, despite the fact that it is six times more expensive than conventional methods. Furthermore, radiation exposure is substantially lower than with analogue systems. Full-field digital mammography is the most widely utilised kind of the technology. It has the potential to significantly improve detection, reduce breast compression pressure, and minimise radiation doses in breast cancer diagnostics. Over the forecast period, each of these advantages will support the market's expansion.

Over the forecast period, the breast tomosynthesis technology segment is expected to experience a CAGR of 12.1%. A 3D picture of the breast is produced using the high-resolution limited-angle tomography technique known as digital breast tomosynthesis. This innovative method assists in the early detection of breast cancer. Analyzing dense breasts using digital breast tomosynthesis is highly helpful and can improve the capacity to find breast cancer. It reduces the need for a biopsy and the amount of false-positive readings. Any woman may wear it, but women with dense breasts benefit the most.

Furthermore, a number of significant studies have shown that systems that combine 2D and 3D mammography are more effective than 2D mammography alone in detecting breast cancer. According to the American Society of Clinical Oncology (ASCO) clinical trial report, a large US study of 4,54,850 patients found that combined 2D/3D screening detected 5.5 cancers per 1,000 women, compared to 4.3 cancers for 2D screening alone, a 28 percent higher detection rate with combined 2D/3D mammography systems. As a result, both high detection rates and growing awareness of the use of these devices are key factors in the segment's growth.

Regional Insights

North America dominated the market with a revenue share of around 41% in 2022 of the global Mammography market, and is estimated to grow at a significant CAGR during the forecast period. One of the key reasons boosting the market in North America is the increased occurrence of breast cancer. In 2022, there were around 279,830 new cases of invasive breast cancer in women. In addition, 48,610 women had in situ breast carcinoma, and it is expected that this figure will increase in the coming years. Many businesses have started to launch programmes to support breast cancer screenings. For instance, Hologic Inc. launched the Back to Screening campaign in August 2020. This announcement encouraged women to schedule their delayed mammograms as a result of the COVID-19 pandemic. The National Breast Cancer Foundation (NBCF) is a group in the US that provides free mammograms and information about breast cancer to women who are in need. Along with these reasons, rising healthcare spending and the presence of a highly developed healthcare infrastructure are other factors that are expected to drive the growth of the market.

Over the forecast period, Asia Pacific region is estimated to witness the CAGR of xx%. The main growth drivers of this region are the significant R&D expenditures on breast cancer treatments, rising incidence of breast cancer, and advancements in breast imaging technologies. According to the Centers for Disease Control and Prevention, regardless of race or ethnicity, breast cancer is the most common malignancy in most Asian nations (CDC). The age-standardized incidence rate of breast cancer in Asia Pacific region is 34.4 per 100,000 people, according to GLOBOCAN 2022. Thus, the rising incidence of breast cancer and the developing healthcare system in the area are expected to drive overall growth. It is estimated that the presence of developing nations like India, China, and Japan would accelerate market growth. Key players are also working hard to reach Asia Pacific's growing markets, which is expected to boost the development of the market.

Mammography Market Scope: Inquire before buying

| Global Mammography Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US 2.13 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 10.3 % | Market Size in 2029: | US 4.25 Bn. |

| Segments Covered: | by Product | Film Screen Systems Digital Systems Analog Systems Biopsy Systems 3D Systems |

|

| by Technology | Breast Tomosynthesis CAD Digital |

||

| by Modality | Portable Non-Portable |

||

| by End-use | Hospitals Specialty Clinics Diagnosis Centers Others |

||

Mammography Market by Region:

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players

1. Hologic Inc.

2. Analogic Corporation,

3. Canon Medical Systems Corporation

4. Fujifilm Corporation

5. Siemens Healthcare

6. Toshiba Medical Systems

7. Metaltronica

8. Koninklijke Philips NV

9. PLANMED OY

10. Allengers Medical Systems Ltd

11. General Electric Company

12. Konica Milota Inc.

13. Gamma Medica Inc.

14. Carestream Health

15. BMI Biomedical International SRL

16. General Medical Italia

17. Villa Systems Medical SpA

Frequently Asked Questions:

1] What segments are covered in the Global Mammography Market report?

Ans. The segments covered in the Mammography Market report are based on Product and Technology.

2] Which region is expected to hold the highest share in the Global Mammography Market?

Ans. The North America region is expected to hold the highest share in the Mammography Market.

3] What is the market size of the Global Mammography Market by 2029?

Ans. The market size of the Mammography Market by 2029 is expected to reach USD 4.25 Bn.

4] What is the forecast period for the Global Mammography Market?

Ans. The forecast period for the Mammography Market is 2023-2029.

5] What was the market size of the Global Mammography Market in 2022?

Ans. The market size of the Mammography Market in 2022 was valued at USD 2.13 Bn.