Global Frozen Meat Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

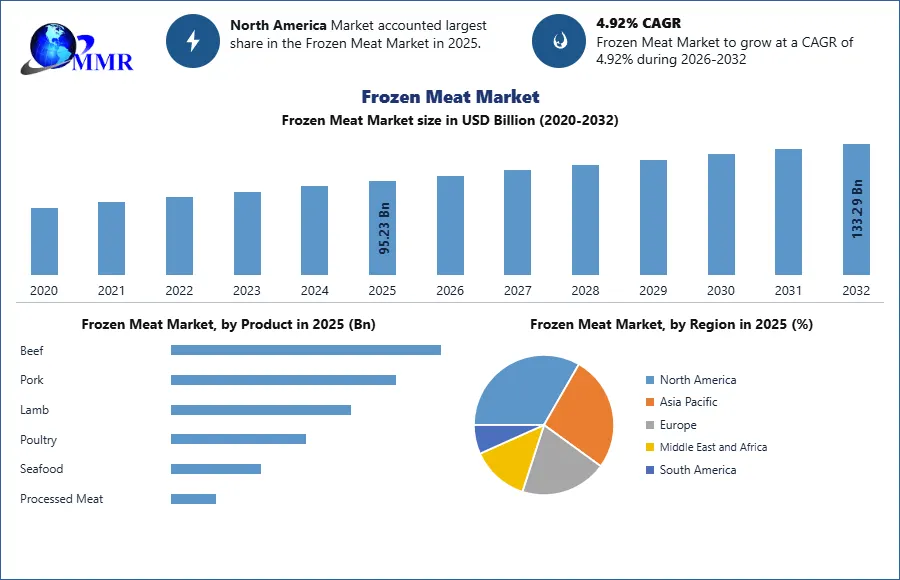

The Frozen Meat Market size was valued at USD 95.23 Billion in 2025 and the total Frozen Meat revenue is expected to grow at a CAGR of 4.92% from 2026 to 2032, reaching nearly USD 133.29 Billion by 2032.

Frozen meat refers to meat that has undergone the process of freezing, preserving it by reducing its internal temperature below its freezing point, typically -18 degrees Celsius, to extend its shelf life and maintain its quality for consumption. The frozen meat market is experiencing growth globally, with an increasing demand for convenient and preserved food products. Factors contributing to this growth include changing consumer lifestyles, urbanization, and the need for convenient yet nutritious meal solutions. The market's expansion is also fueled by evolving dietary preferences, a growing focus on food safety and quality, and rising disposable incomes. Key players in this market continue to innovate, focusing on product diversification, improved packaging technologies for prolonged shelf life, and expanding distribution networks to cater to a broader consumer base. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Recent developments involve strategic collaborations, acquisitions, and the launch of new product lines, including organic and specialty cuts, to tap into evolving consumer preferences for healthier and specialized options. Key players in this market, such as Tyson Foods, Inc., Cargill Incorporated, JBS S.A., BRF S.A., and Kerry Group, have been pivotal in shaping its trajectory. These companies have continually invested in research and development to introduce new frozen meat products, expand their product portfolios, and improve processing techniques, catering to evolving consumer preferences for convenience and quality. For instance, Tyson Foods, a leading global producer of meat and poultry, announced strategic investments in technological advancements to enhance its cold chain infrastructure, ensuring better preservation and distribution of frozen meat products. Advancements in freezing techniques and eco-friendly packaging solutions are being adopted to address consumer demands for freshness, taste, and sustainability.

Market Dynamics:

Rising demand for hassle-free frozen chicken indicates a shift toward time-saving meal solutions:

Evolving consumer preferences for convenience and time-saving options drive the frozen meat market. For instance, the rising demand for ready-to-cook frozen chicken products, like marinated chicken strips or pre-seasoned chicken breasts, reflects consumers' inclination towards hassle-free meal solutions, catering to busy lifestyles. Increasing globalization and ease of trade contribute to market growth. For instance, the growth of international trade agreements facilitates the accessibility of various frozen meat products globally, fostering market growth and diversity in product offerings. Innovations in freezing technologies, such as quick freezing methods, ensure the preservation of meat quality. For instance, advancements in Individual Quick Freezing (IQF) technology maintain the texture and freshness of meats, bolstering consumer trust and market growth.

Prime Factors Driving the Frozen Meat Market Globally:

1. Change in Lifestyle

2. Demand for Ready-to-Eat Food

3. Global Pandemic Crisis

4. Issue of Seasonality

5.Issue of Food Wastage

6. Growing Working Population

7. Rising penetration of Online Food Delivery Services

8. Shopping Trends of Millennial

Growing health awareness among consumers leads to a demand for healthier frozen meat options. Examples include the introduction of low-fat or preservative-free frozen meat products to cater to health-conscious consumers seeking nutritious options within the frozen meat category. The growth of retail channels and the rise of e-commerce platforms offer wider accessibility to frozen meat products. For instance, the increasing availability of diverse frozen meat selections online and in supermarkets amplifies consumer reach, spurring market growth. Continuous product innovation drives market growth. Examples include the introduction of plant-based or meat-alternative frozen products, meeting the demands of vegetarian or flexitarian consumers seeking plant-based protein sources. Frozen meat is often considered to be an excellent source of protein, with 100 grams providing up to 15.8g of protein, 0.7g of fat, and 1.4g of carbohydrate. It also contains a variety of vitamins, such as vitamin B2 and vitamin B6, as well as essential minerals like zinc and phosphorus. Frozen meat's high levels of omega-3 fatty acids make it an ideal choice for people looking for a healthier option when incorporating meats into their diet.

Shifting demographics and urbanization drive market growth by influencing consumption patterns. For instance, the growing urban population's preference for convenient, pre-packaged frozen meat items like burgers or sausages fuels market growth. Consolidation through strategic mergers and acquisitions contributes to market growth. Notable examples include companies acquiring businesses specializing in niche frozen meat categories to diversify their product portfolios and expand their market presence. Increasing concerns about environmental sustainability drive market growth through the introduction of eco-friendly packaging for frozen meat products. For instance, companies utilizing recyclable or biodegradable packaging materials align with consumer preferences for sustainable choices. Evolving dietary habits and culinary trends influence the market. For example, the increasing popularity of international cuisines prompts the demand for various frozen meat options, like pre-marinated ethnic cuts, catering to diverse culinary preferences.

Rising Popularity of Plant-Based Alternatives Impacts Frozen Meat Sales:

Substitute products for frozen meat encompass a wide range of alternatives that consumers increasingly consider as replacements for traditional frozen meat options.

These substitute products pose a restraint on the frozen meat market, and plant-based alternatives are gaining popularity. Plant-based meats, such as veggie burgers, tofu-based products, or plant-derived protein sources like seitan, mimicking the taste and texture of traditional meats, have garnered traction among consumers seeking healthier, environmentally sustainable options. Innovations in plant-based burgers, sausages, and meatballs cater to shifting dietary preferences, appealing to a growing demographic adopting flexitarian or vegetarian diets. These alternatives, often perceived as healthier due to their lower saturated fat content and sustainability benefits, directly compete with frozen meat products. Their rising availability, coupled with consumers' increasing inclination towards plant-centric diets, presents a substantial challenge to the frozen meat market's growth and market share.

Growing health consciousness has led to concerns about the consumption of processed meats due to their potential links to health issues like cardiovascular diseases and cancer. Increasing production costs, including energy-intensive freezing processes and storage expenses, often lead to higher prices for frozen meats, impacting consumer affordability and purchasing decisions. Despite freezing methods, frozen meats may suffer from quality degradation over time, potentially affecting taste, texture, and overall quality upon thawing, raising concerns among consumers regarding freshness. The surge in popularity of plant-based meat alternatives presents a substantial threat, with products like plant-based burgers and sausages increasingly appealing to consumers seeking healthier and sustainable protein sources.

Frozen meat production processes have environmental implications, including energy consumption and packaging waste, which might not align with the preferences of environmentally conscious consumers. Compliance with stringent regulatory standards for frozen meat production and storage poses challenges, especially concerning maintaining quality, safety, and hygiene standards throughout the supply chain. Limited space for frozen meat products in retail stores or supermarkets can restrict the visibility and availability of products, impacting consumer choices and purchases. Maintaining the cold chain and ensuring uninterrupted frozen product delivery can be challenging, especially in regions with inadequate infrastructure or transportation facilities.

Growing diversification in the healthier frozen meat varieties and Innovative Freezing Techniques:

Introducing new product lines, such as organic or specialty cuts, taps into evolving consumer preferences for healthier and specialized options, stimulating market growth. For instance, the launch of organic frozen meat products, like grass-fed beef or antibiotic-free poultry, caters to health-conscious consumers seeking premium quality meats. Embracing cutting-edge freezing techniques like blast freezing or cryogenic freezing ensures improved product quality and shelf life, meeting consumer expectations for freshness and taste. For example, implementing quick freezing methods preserves the natural texture and flavor of frozen meats, elevating consumer satisfaction and market demand. Penetrating untapped markets in emerging economies presents vast growth potential. For instance, targeting regions with rising disposable incomes, like Asia-Pacific or Latin America, opens avenues for increased consumption and market growth.

Leveraging online platforms for direct-to-consumer sales amplifies market reach. Enhancing e-commerce platforms with diverse frozen meat selections provides convenient access for consumers, fostering market growth through increased accessibility and convenience. Collaborating with retailers or food service providers enables broader distribution and exposure. For example, partnerships with supermarkets or restaurant chains increase product visibility, driving market penetration and sales. Addressing the growing demand for healthier options by introducing innovative, low-sodium, or preservative-free frozen meat selections resonates with health-conscious consumers, enhancing market prospects. Incorporating eco-friendly packaging solutions, such as recyclable or biodegradable materials, aligns with environmentally conscious consumer preferences, fostering market growth by appealing to sustainability-driven buyers.

Introducing ready-to-eat or pre-seasoned frozen meat products caters to consumers seeking convenient meal solutions. For instance, offering pre-marinated frozen chicken or seasoned beef cuts resonates with time-strapped consumers, driving market demand. Emphasizing transparency in sourcing and processing, such as highlighting quality certifications or ethical practices, builds consumer trust and credibility, leading to increased market share and brand loyalty. Tailoring frozen meat options to changing consumer lifestyles, like offering single-serve or portion-controlled packaging for smaller households or on-the-go options for busy professionals, addresses evolving preferences, propelling market growth.

Frozen Meat Market Segment Analysis:

Based on Type, The frozen meat market is segmented into Frozen Processed Meat and Frozen Whole Cuts. Frozen Processed Meat holds a dominant position due to its higher adoption rates compared to Frozen Whole Cuts. Processed meats undergo specific treatments, such as smoking, curing, or adding preservatives, enhancing their shelf life and convenience, and appealing to consumers seeking ready-to-cook options. This segment, comprising sausages, bacon, and pre-seasoned cuts, caters extensively to the demand for quick meal solutions, aligning with the fast-paced lifestyles of modern consumers. Frozen whole cuts, which hold a small market share presently, are expected to gain momentum in the coming years. These products, including unprocessed or minimally processed cuts like steaks and chops, target consumers looking for more natural and unaltered meat choices. The adoption of frozen whole cuts is anticipated to rise due to a growing preference for fresher and less processed food options among health-conscious consumers.

Frozen Meat Market Regional Insights:

North America stands as a significant dominator in the global frozen meat market. The region's dominance is propelled by the United States and Canada, leveraging advanced infrastructure, technological innovations, and shifting consumer preferences. The presence of established players, efficient distribution networks, and a high demand for convenient food options contribute to North America's market leadership. For instance, in the United States, frozen meat consumption has been steadily rising due to evolving consumer lifestyles, wherein individuals seek time-saving meal solutions without compromising on quality. Major cities like New York and Los Angeles witness high demand for frozen meat products, including ready-to-cook chicken strips, seasoned beef, and various processed meat items. Additionally, the growth of online retail and delivery services further boosts market accessibility and consumer reach.

Europe emerges as another prominent region dominating the frozen meat market. Countries like Germany, the United Kingdom, France, and Italy drive the region's frozen meat market with their established food processing industries, evolving food habits, and a growing inclination toward convenience foods. For instance, in Germany, a nation with a rich tradition in meat consumption, the Frozen Meat Market experiences substantial growth. Consumers increasingly opt for frozen meat due to its convenience, long shelf life, and wide range of options. Popular frozen meat products in Europe include pre-marinated cuts, sausages, and specialty frozen meat items, catering to diverse culinary preferences across the continent.

Asia Pacific has emerged as a rapidly growing region in the frozen meat market. The market's growth is driven by countries such as China, Japan, India, and South Korea, owing to increasing urbanization, rising disposable incomes, and a burgeoning middle-class population with changing dietary preferences. For instance, in China, a significant contributor to the regional market, urbanization, and lifestyle changes have led to an upsurge in the demand for frozen meat products. Rapidly expanding e-commerce platforms and the adoption of Western eating habits among the younger demographic have further fueled the market. Popular frozen meat choices include various chicken cuts, pork, and seafood, meeting the demands of a diverse consumer base. As these regions continue to evolve, the Frozen Meat Market is expected to witness further growth and diversification, with innovative product offerings tailored to meet regional demands and preferences.

Competitive Landscape

The recent developments have significantly impacted the frozen food market by fostering expansion and diversification. Prasuma's foray into the frozen food segment in India, alongside Seara Foods targeting the Middle Eastern and Latin American poultry markets, indicates a growing focus on regional demands. Préval AG's acquisition of J&G Foods and Armand Agra's takeover of Seattle Fish Company underline the industry's consolidation drive, enhancing product diversity and global market presence. Agthia Group's investment in Ismailia Investments denotes an increasing interest in expanding product portfolios across borders. These moves collectively signal a dynamic shift towards catering to diverse consumer preferences and expanding market footholds across continents.

Frozen Meat Market Recent Developments:

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 18 February 2026 | Hormel Foods Corporation | Hormel Foods launched the Flash 180 Platform, a specialized quick-prep breaded chicken solution designed for rapid foodservice and retail applications. | The initiative targets the high-growth convenience segment, aiming to drive 1%-4% organic net sales growth in 2026 by reducing prep time for frozen protein products. |

| 18 February 2026 | Hormel Foods Corporation | The company confirmed the divestiture of the hen part of its turkey business while retaining the premium Jennie-O brand and tom turkey operations. | This portfolio optimization streamlines supply chain efficiency and allows the company to refocus resources on its most profitable value-added frozen meat lines. |

| 01 January 2025 | ABPA / Apex-Brasil | The Brazilian Association of Meat Exporters reported that Brazil's beef exports reached a historic record of 2.89 million tonnes entering the 2025 cycle. | This record volume, led by JBS and Marfrig, solidifies South America's dominance in the global frozen beef trade, filling supply gaps in the US and Asian markets. |

| 13 March 2025 | Moy Park (Pilgrim's Pride) | Moy Park introduced an expanded line of flavor-diverse breaded chicken products specifically for Asda retail stores across the UK. | The launch addresses the rising demand for affordable protein in the UK market, which is projected to reach a valuation of $10.54 billion by 2026. |

Frozen Meat Market Scope: Inquire Before Buying

| Frozen Meat Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 95.23 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.92% | Market Size in 2032: | 133.29 USD Billion |

| Segments Covered: | by Product | Beef Pork Lamb Poultry Chicken Duck Others Seafood Fish Salmon Seabass Tuna Cod Octopus Others Crustaceans Prawns Crabs Lobsters Others Mollusks Scallops Mussels Squid Others Others Processed Meat Sausages Meatballs Nuggets Others |

|

| by Nature | Organic Conventional |

||

| by Packaging Type | Bulk Packaging Retail Packaging Vacuum Packaging |

||

| by Processing Method | Individually Quick Frozen (IQF) Block Frozen Blast Frozen |

||

| by Pricing | Premium Mid-range Economy |

||

| by Distribution Channel | Business to Business Business to Consumer Hypermarkets/Supermarkets Convenience Stores Specialty Stores Online Retail |

||

Frozen Meat Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Frozen Meat Market, Key Players:

1. Allanasons Pvt Ltd

2. Ajinomoto Foods

3. Astral Foods

4. Austevoll Seafood ASA

5. Cargill Inc

6. Conagra Brands, Inc

7. General Mills Inc

8. Green Farms LLC

9. Hormel Foods Corporation

10. JBS SA

11. Kellogg Co

12. Kerry Group Plc

13. Kraft Heinz Company

14. LantmännenUnibake

15. M&J Seafood Holdings Limited

16. m. Morrison Supermarkets Limited

17. Marfrig Global Foods SA

18. McCain Foods Ltd.

19. Nestlé SA

20. Nomad Foods Limited

21. Pilgrim`s Pride Corporation

22. Samworth Brothers

23. Tyson Foods, Inc

24. Unilever

25. Verde Farms LLC

26. VH Group

27. Waitrose & Partners

28. Xiamen Yinxiang Group Co., Ltd.