Wind Energy Market- Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

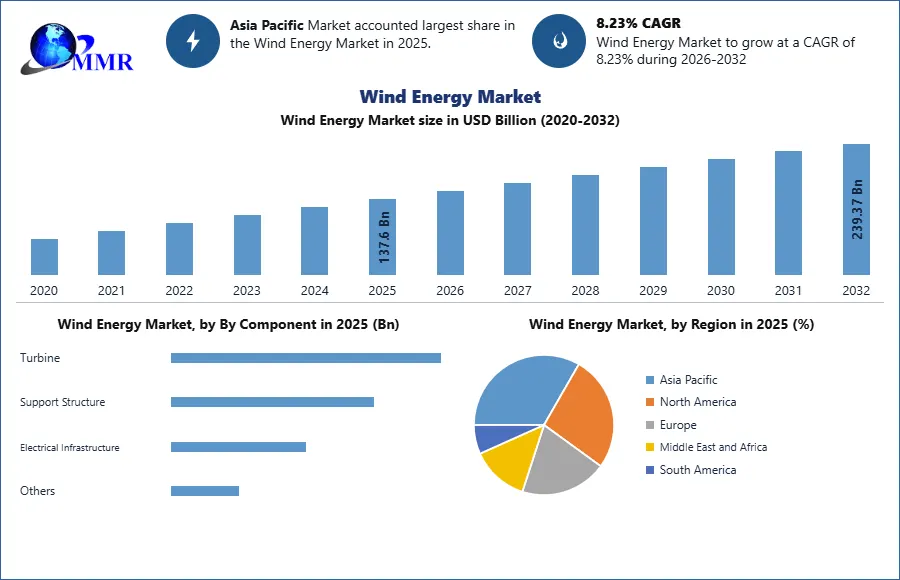

The Wind Energy Market size was valued at USD 137.6 Billion in 2025 and the total Wind Energy revenue is expected to grow at a CAGR of 8.32% from 2026 to 2032, reaching nearly USD 239.37 Billion by 2032

Wind Energy Market Overview

Wind energy is a renewable energy source derived from harnessing the kinetic energy of the wind to generate electricity. This is typically achieved using wind turbines, which consist of large blades mounted on a rotor connected to a generator. Wind energy is considered environmentally friendly because it produces no greenhouse gas emissions or air pollutants during operation. It is also abundant and inexhaustible, making it a sustainable alternative to fossil fuels for electricity generation. Wind energy is deployed in various settings, including onshore wind farms located on land and offshore wind farms situated in bodies of water such as oceans and lakes. Onshore wind farms are more common and often less expensive to build, while offshore wind farms take advantage of stronger and more consistent wind speeds, albeit at a higher cost of installation and maintenance.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The global wind energy market is growing steadily over the past decade, driven by increasing concerns about climate change, government initiatives promoting renewable energy, and technological advancements in wind turbine technology. Wind energy installations are spread across the globe, with countries such as China, the United States, Germany, India, and the United Kingdom leading in terms of installed capacity. The wind energy market comprises both onshore and offshore segments. Onshore wind farms, located on land, have traditionally dominated the market due to lower installation costs.

Wind Energy Market Dynamics

Government initiatives worldwide to boost Wind Energy Market growth

Governments worldwide are implementing significant new policies aimed at substantially boosting renewable energy adoption and hastening the reduction of emissions. In the United States, the Inflation Reduction Act of 2022 stands as a landmark legislation, earmarking an estimated $391 billion over a decade for energy and climate change initiatives. Notable measures include the extension of the Production Tax Credit and backing for domestic manufacturing of wind energy components via an Advanced Manufacturing Production Tax Credit. The Infrastructure Investment and Jobs Act allocates $550 billion for investments in clean energy transmission and electric vehicle infrastructure, facilitating the electrification of numerous school and transit buses and establishing a new grid deployment authority to bolster grid upgrades. The U.S.'s steadfast commitment provides essential policy stability to the Wind Energy market and fosters the growth of wind energy well into the future.

In response to the unprecedented challenges confronting the European energy supply chain, the European Commission has adopted an all-encompassing policy agenda named REPowerEU. The revised targets outlined in the REPowerEU initiative aim to achieve a total installed capacity for wind energy of 510 GW, a significant increase from the current 190 GW. Beyond advancing the ambitious climate change objectives set by EU member states, this projected surge in wind capacity aligns with Europe's new priorities for energy autonomy, resilience, and local economic growth, which significantly boosts the Wind Energy Market growth. The EU is exploring avenues to streamline the permitting process to expedite the implementation of wind projects.

China has pledged to attain carbon neutrality by 2060, while India aims to ramp up its renewable energy capacity to 500 GW by 2030 and achieve carbon neutrality by 2070. Wind energy remains a pivotal component in realizing these ambitious targets.

Wind Energy Market Trends Growth and Investment Opportunities Wind Energy Market Harnessing the Clean Energy Revolution: The global installed wind power capacity reached a staggering 743 gigawatts in 2020, a significant increase from 24 GW in 200. This growth is expected to continue, with Wind Europe predicting a total installed capacity of 500 GW in Europe alone by 2030. Offshore wind farms, which harness the strong winds at sea, are gaining prominence. Europe leads the way in offshore wind capacity, with a projected increase from 25 GW in 2020 to 130 GW by 2030. The United States and Asia are also ramping up their offshore wind projects.

Investing in Wind Energy: Wind energy has experienced impressive expansion. As reported by the Global Wind Energy Council (GWEC), cumulative wind power installations exceeded 651 GW by the conclusion of 2020, marking a significant surge compared to prior periods. Moreover, projections suggest that wind power capacity soar to around 1,400 GW by 2030, underscoring the vast potential within this industry.

Riding the Green Wave: The ever-increasing need for energy, coupled with the depletion of fossil fuels, has forced nations to explore renewable energy sources. Wind energy, being abundant and sustainable, has experienced an upsurge due to its tremendous potential.

Grid integration challenges to restrain Wind Energy Market Growth

Many existing electricity grids are not designed to accommodate large-scale renewable energy sources like wind power. Integrating variable renewable energy into the grid requires upgrades and enhancements to transmission and distribution infrastructure, as well as advanced grid management and control systems. Regulatory barriers and grid access issues impede the connection of new wind farms to the grid, delaying project development and deployment. Economic factors also pose restraints on the wind energy market. While the cost of wind energy has decreased significantly in recent years due to technological advancements and economies of scale, it still faces competition from conventional fossil fuel sources, which benefit from longstanding subsidies and infrastructure investments. Additionally, the upfront capital costs of wind energy projects is substantial, requiring access to financing and investment incentives to attract developers and investors.

Social acceptance and community opposition is expected to hinder the development of wind energy projects, which significantly restraints the Wind Energy Market growth. Concerns about noise pollution, visual impacts, and effects on wildlife and ecosystems lead to resistance from local communities and stakeholders. Engaging with communities early in the project development process, conducting thorough environmental assessments, and implementing effective stakeholder engagement and communication strategies are essential to addressing these concerns and gaining social license for wind energy projects.

Wind Energy Market Segment Analysis

Based on Type, the market is segmented into Offshore and Onshore. The onshore segment dominated the market in 2025 and is expected to hold the largest Wind Energy Market share over the forecast period. In 2024, out of the total installed wind capacity of 900 GW, 93% comprised onshore systems, leaving the remaining 7% allocated to offshore wind farms. Onshore wind technology has achieved widespread adoption, operating in 115 countries globally, whereas offshore wind is still in its early stages of expansion, with capacity established in only 20 countries. However, offshore wind's reach is expected to increase in the coming years as more countries embark on the development or planning phases of their first offshore wind projects. In 2024, offshore technology contributed 18% of the total wind capacity growth of 74 GW. Onshore wind turbines utilize similar technology to their offshore counterparts, consisting of tall towers with turbine blades attached to a rotor. As the wind passes through the blades, it generates rotational motion that drives a generator, producing electricity.

Wind Energy Market Regional Insight

Government Support and Policies to boots Asia Pacific Wind Energy Market growth

Asia Pacific dominate the market in 2025 and is expected to hold the largest Wind Energy Market share over the forecast period. Many countries in the Asia-Pacific region have implemented supportive policies and incentives to encourage the development of renewable energy, including wind power. This support often comes in the form of subsidies, feed-in tariffs, tax incentives, and renewable energy targets. In 2025, China maintained its position as the frontrunner in wind capacity expansions, introducing 37 GW of new capacity, which includes 7 GW from offshore installations. The unveiling of the 14th Five-Year Plan for Renewable Energy in 2022 set forth bold objectives for the deployment of renewable energy, indicating a promising trajectory for future expansions, which is expected to boost the Wind Energy Market growth. China published its 14th Five-Year Plan for Renewable Energy in June 2022, which includes an ambitious target of 33% of electricity generation to come from renewables by 2025 (up from about 29% in 2021), including an 18% target for wind and solar technologies.

Wind energy stands as a pivotal industry in Europe, strategically anchoring the continent's energy security framework. With 300,000 high-quality jobs and a €42 billion contribution to the EU GDP, it serves as a cornerstone of economic vitality. On average, each new turbine spurs €11 million in economic activity, underscoring its profound impact on local and regional economies. With 248 factories dispersed throughout Europe, including in economically marginalized areas, wind energy emerges as a significant European export industry.

Wind farms bring substantial economic benefits to their host communities, generating approximately €7 billion in taxes and fostering job creation and investment, particularly in rural locales. Collective ownership models further democratize revenue distribution, empowering local residents and engendering a sense of ownership in their energy provision.

By leveraging its European supply chain and nurturing local prosperity, wind energy plays a pivotal role in fostering an inclusive and equitable energy transition. Surveys reveal overwhelming public support, with 70-80% of Europeans endorsing wind energy, a sentiment even more pronounced among those residing near wind farms. The Wind Energy industry remains steadfast in its commitment to retraining individuals transitioning from fossil fuel industries, ensuring a just and sustainable workforce transition. Wind energy meets 17% of Europe's electricity demand and constitutes a larger share in several countries: Denmark (55%), Ireland (34%), UK (28%), Portugal (26%), Germany (26%), and Spain (25%).

Wind Energy Market Scope: Inquire before buying

| Wind Energy Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 137.6 USD Billion |

| Forecast Period 2026-2032 CAGR: | 8.23% | Market Size in 2032: | 239.37 USD Billion |

| Segments Covered: | By Component | Turbine Tower Rotor Blades Others Support Structure Substructure Steel Foundation Others Electrical Infrastructure Wires & Cables Substation Others Others |

|

| By Turbine Type | Horizontal Axis Wind Turbine (HAWT) Vertical Axis Wind Turbine (VAWT) |

||

| By Location | Offshore Onshore |

||

| By Connectivity | On Grid Off Grid |

||

| By Rating | ≤2 MW 2–5 MW 5–8 MW 8–10 MW >10 MW |

||

| By Application | Utility Scale Distributed / Small Wind |

||

| By End User | Industrial Commercial Residential |

||

Wind Energy Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Wind Energy Market, Key Players

North America:

1. Vestas Wind Systems A/S: Aarhus, Denmark

2. General Electric Renewable Energy: Schenectady, New York, USA

3. Siemens Gamesa Renewable Energy: Zamudio, Spain

4. NextEra Energy Resources: Juno Beach, Florida, USA

5. EDF Renewables: Paris, France

6. AES Corporation: Arlington, Virginia, USA

Europe:

7. Ørsted A/S: Fredericia, Denmark

8. Enel Green Power : Rome, Italy

9. RWE Renewables : Essen, Germany

10. Nordex Group: Hamburg, Germany

11. Iberdrola Renewables: Bilbao, Spain

12. EDP Renováveis: Lisbon, Portugal

Asia-Pacific:

13. Goldwind : Beijing, China

14. Ming Yang Smart Energy : Zhongshan, China

15. China Energy Investment Corporation : Beijing, China

16. Suzlon Energy Limited: Pune, India

17. Hyundai Heavy Industries Co., Ltd.: Ulsan, South Korea

18. Envision Energy: Shanghai, China

Frequently Asked Questions:

1. What is wind energy?

Ans: Wind energy is a renewable energy source derived from harnessing the kinetic energy of the wind to generate electricity using wind turbines.

2. How has the global wind energy market been growing?

Ans: The global wind energy market has been growing steadily over the past decade, driven by increasing concerns about climate change, government initiatives promoting renewable energy, and technological advancements in wind turbine technology.

3. What are the key drivers for wind energy market growth?

Ans: Key drivers include government support and policies promoting renewable energy adoption, advancements in wind turbine technology, and increasing concerns about climate change.

4. What are the challenges facing the wind energy market?

Ans: Challenges include grid integration issues, regulatory barriers, economic factors, social acceptance, and community opposition to wind energy projects.

5. What are the regional insights into the wind energy market?

Ans: Different regions, such as Europe and Asia-Pacific, have unique dynamics and government initiatives driving wind energy market growth, offering diverse investment prospects in the sector.