District Heating Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

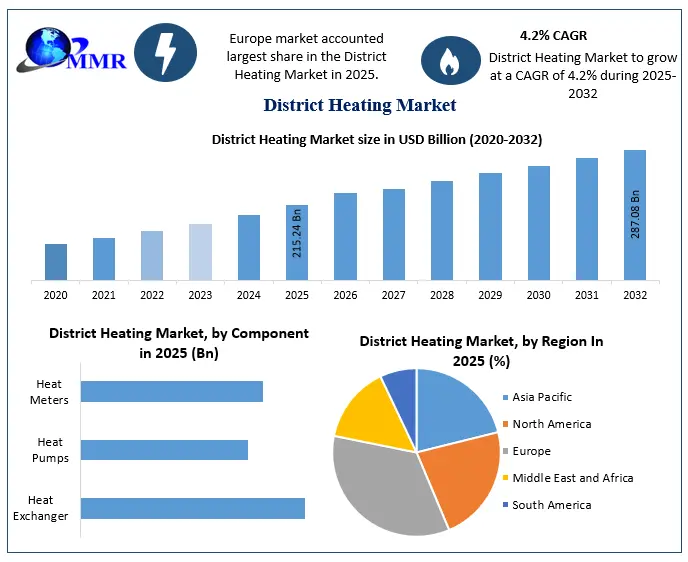

The District Heating Market size was valued at USD 215.24 Billion in 2025 and the total District Heating revenue is expected to grow at a CAGR of 4.2% from 2026 to 2032, reaching nearly USD 287.08 Billion by 2032.

The MMR report on the District Heating Market provides an in-depth, holistic assessment covering End-User Preference & Adoption Insights, detailed Cost–Benefit and Economic Feasibility Analysis, region-wise Pricing & Cost Structure, and comprehensive Infrastructure & Network Development Outlook. The study further includes forward-looking Investment & Policy Insights, breakthrough Technological Advancements, and a full Supply Chain & Procurement Analysis. In addition, it evaluates critical Sustainability & Environmental Impact metrics and offers an updated Regulatory Landscape by Region, ensuring stakeholders gain complete visibility into market dynamics, growth drivers, barriers, and future opportunities across global district heating ecosystems.

District Heating Market Overview

District heating involves generating heat in a centralized location and then distributing it to residences, businesses and industry in a local area. In a district heating system, a central heat generation plant produces heat energy through various means, such as burning natural gas, coal, biomass, or utilizing renewable sources like geothermal energy or waste heat from industrial processes. The heat is then transferred to a heat transfer fluid, usually water or steam. District heating systems are more reliable and less prone to breakdowns compared to individual heating systems.

The district heating market is expanding globally, driven by urbanization, rising energy demand, and the need for more efficient heating solutions. Both developed and developing countries are investing in district heating infrastructure to improve energy efficiency and reduce emissions. Growing environmental concerns and government policies aimed at reducing carbon emissions is promoting the adoption of district heating. These systems are seen as a way to decrease energy waste and make heating more environmentally friendly.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

District Heating Market Dynamics

Energy Efficiency and Sustainability to boost the District Heating Market growth

District heating systems are recognized for their energy efficiency, as they recover and reuse waste heat from various sources. A fundamental driver is the global shift toward renewable energy sources. District heating systems provide an ideal platform for integrating renewables such as biomass, geothermal, and solar thermal, facilitating the transition to cleaner energy. Governments are actively promoting district heating as part of their energy and environmental strategies, which significantly contributes for the growth of the District Heating Market growth. This includes subsidies, tax incentives, and emissions reduction targets to incentivize adoption. District heating diversifies energy sources, reducing dependence on imported fossil fuels.

This enhances energy security, especially in regions with supply vulnerabilities. District heating offers economic advantages for consumers, job creation, and economic growth in the regions where these systems are deployed. Advances in district heating technologies, such as more efficient heat pumps, thermal storage, and smart grid integration, enhance system performance and attractiveness. District heating systems are often more resilient to supply disruptions and extreme weather events, which is critical in regions prone to severe weather conditions.

The concept of micro-district heating and localized energy generation is gaining traction, providing flexibility and adaptability to communities. Growing public awareness and concern about environmental issues, such as air pollution and climate change, drive interest in clean and efficient heating solutions like district heating. District heating extends beyond residential use, serving industrial and commercial facilities to meet their heating and cooling needs efficiently. Aging and inefficient heating infrastructure in some regions necessitates upgrades and replacements, making district heating an attractive option, which is expected to fuel the District Heating Industry growth.

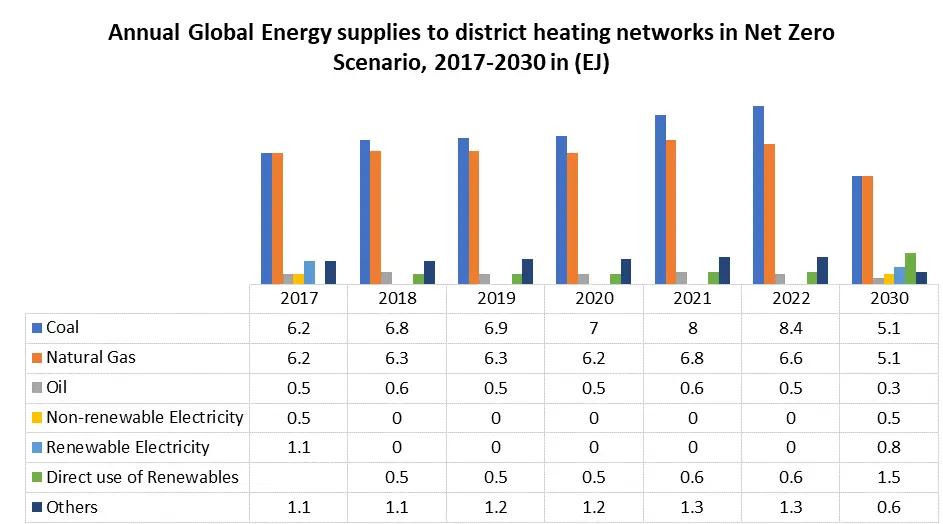

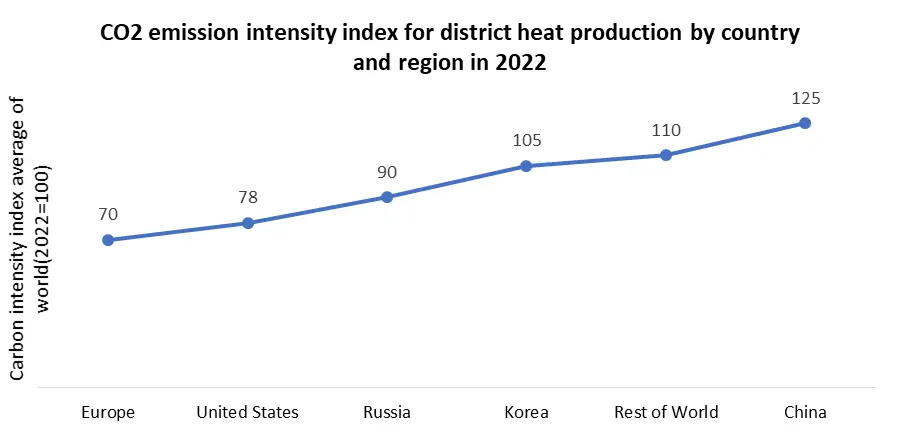

District heating systems harness waste heat from industrial processes, power generation, and data centers, converting it into valuable heating energy. As climate change intensifies, district heating's ability to provide reliable heating and cooling, even during extreme weather events, is a compelling driver for its adoption. In 2024, the district heating production was around 9% of the global final heating need in buildings and industry. However, the decarbonisation potential of district heating is largely untapped, as fossil fuels still dominate district network supplies globally (about 90% of total heat production), especially in the two largest markets of China and Russia.

District heating market trends at the stage

1. Low Temperature Supply Flow

The future networks will use low temperature 40-60 ºC supply in combination with radiant heating more efficiently.

2. Circular Economy

New-generation District Heating and cooling systems lean towards the decentralized generation of cold and heat, taking advantage of all available local energy sources. Some local authority polities focus on the research of the following points to create and promote circular economies: Research of low-grade heat dissipation from industrial or residential heat, Promote the usage of sewage water heat or waste heat from the water treatment plant, and Increase the use of waste energy.

3. Heat Generation Mix Balance

This profile simulation leads to a clearer picture of a complete heating plant performance. For achieving the best results in a District Heating design and a proper decision-making process, a detailed heating load profile simulation is essential. Only detailed Heating Load Profile calculations can guarantee that the resulting District Heating system is energy efficient.

High Initial Capital Costs to limit the District Heating Market growth

One of the primary challenges for district heating projects is the high upfront capital required for infrastructure development, including the construction of heat generation plants, distribution networks, and individual building connections. This initial cost deter potential investors and limit the expansion of district heating systems, particularly in smaller communities. Retrofitting older buildings and heating systems to connect them to district heating networks is technically challenging and expensive. It requires extensive renovations and disruptions to existing structures, making it less appealing to property owners and developers.

Regulatory barriers and permitting processes pose significant challenges to the implementation of district heating projects, which restraints the District Heating Market growth. Different regions have complex and time-consuming approval procedures that delay project development. In some areas, the district heating market is highly fragmented, with multiple small-scale systems operated by different entities. This fragmentation make it challenging to achieve economies of scale and optimize system operations. Lack of awareness and understanding of district heating among consumers hinder its adoption. Additionally, convincing property owners and residents to switch from their existing heating systems to district heating is barrier, especially if they are unfamiliar with the technology. Integrating various heat sources, including renewables and waste heat, into district heating networks technically complex. Compatibility issues, grid integration, and system optimization require careful planning and expertise.

District Heating Market Segmentation

Based on Heat Source, the market is segmented into Coal, Natural Gas, Renewable, Oil & Petroleum Products, and Others. Natural Gas segment dominated the market in 2024 and is expected to hold the largest District Heating Market share over the forecast period. Natural gas is utilized as a primary heat source in district heating systems. It can power boilers or combined heat and power (CHP) plants to generate heat efficiently. CHP systems are particularly efficient because they simultaneously produce electricity and capture waste heat for district heating, enhancing overall energy efficiency.

Natural gas is easily integrated into existing district heating systems or used in new installations, which is expected to boost the segment growth in the District Heating Market. It provides flexibility to district heating operators, allowing them to meet changing heat demand efficiently. In regions with access to affordable natural gas, it is cost-effective fuel source for district heating. It offers competitive pricing for consumers compared to other energy sources. Natural gas contributes to energy security by diversifying the energy mix in district heating. It reduces dependence on a single energy source and enhances resilience against supply disruptions.

Based on Plant Type, The Combined Heat & Power (CHP) segment dominated the District Heating Market in 2024 and continues to lead due to its superior efficiency, offering simultaneous electricity and heat generation from a single fuel source. Waste-Heat Recovery Plants follow, driven by industrial decarbonization and rising adoption of energy-from-waste systems that capture and reuse heat that would otherwise be lost. Heat-Only Boilers hold a steady share, supported by district networks requiring centralized heat without power generation, particularly in colder regions. Boilers remain the least dominant segment, used mainly in legacy systems and smaller networks but gradually losing traction as utilities shift toward cleaner, high-efficiency, and integrated heating solutions.

District Heating Market Regional Insight

Expanding District Heating Networks in Europe to boost the District Heating Market growth

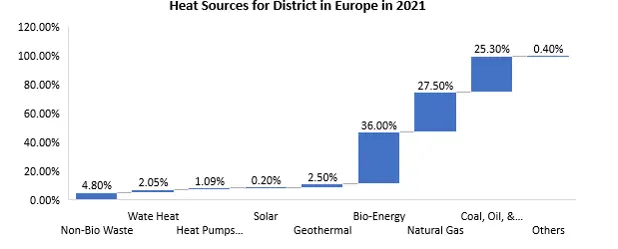

Europe held the largest District Heating Market share in 2025 and is expected to dominate the market over the forecast period. In Europe, district heating sales amount to nearly 500 TWh in 2021. The total installed capacity within the European district heating sector is about 300 GWth (2021) for the countries surveyed European countries, especially those in the northern regions, have well-established district heating networks. These networks continued to expand, connecting more residential, commercial, and industrial buildings. Expansion efforts aimed to reduce individual heating systems and increase energy efficiency. Europe has been at the forefront of integrating renewable energy sources into district heating systems.

Biomass, geothermal energy, and solar thermal technologies were increasingly being used to supply heat to district heating networks, reducing carbon emissions. European Union (EU) member states set ambitious energy efficiency targets, encouraging the adoption of district heating as a means to reduce energy waste. District heating was viewed as an effective way to recover and reuse waste heat from various sources. Some European countries undertook market liberalization efforts in the district heating sector, encouraging competition and potentially leading to improved service quality and cost-effectiveness for consumers. Both public and private sector investments were flowing into district heating projects across Europe. Public funding and subsidies supported the expansion of networks, while private investors saw the potential for sustainable returns.

In April 2024, the European Union provided EUR 401 million in support for the Czech green district heating scheme. In the United Kingdom, in March 2024, the Energy Security Bill introduced a heat networks regulation to enable heat zoning. The Climate Change Committee has estimated that around 18% of heat consumption in the United Kingdom could be supplied through heat networks by 2050. In January 2024, the first funds under the GBP 288 million Green Heat Network Fund were awarded to heat network projects in the United Kingdom.

In January 2024, the first funds under the GBP 288 million Green Heat Network Fund were awarded to heat network projects in the United Kingdom.

In Denmark in March 2024 the parliament adopted regulation to support geothermal, passing a law that will exempt geothermal heat projects from the price regulation already in place. Integration of Renewable Energy to boost the North America District Heating Market growth

Integration of Renewable Energy to boost the North America District Heating Market growth

The integration of renewable energy sources into district heating systems was gaining traction. Biomass, geothermal, and solar thermal technologies were increasingly used to provide heat to district heating networks, reducing carbon emissions and environmental impact. Various North American cities and states set ambitious energy efficiency and emissions reduction goals. District heating systems were seen as a key component in achieving these objectives by recovering waste heat and using more efficient heating technologies.

The city of Vancouver, Canada, is expanding its district heat network capacity by adding 6.6 MW of sewage heat recovery equipment to capture latent heat from wastewater with heat pumps.

District Heating Market Competitive Landscape

ESCOs that specialize in energy-efficient solutions, including district heating, provide services related to the design, construction, and operation of district heating systems. District Heating companies that supply equipment and technologies for district heating systems, such as heat pumps, boilers, pipes, and control systems, compete in the market by offering innovative and efficient solutions. The district heating market has seen the entry of innovative startups focusing on district heating solutions that incorporate advanced technologies, including data analytics and smart grid integration. Collaboration between different stakeholders, such as technology providers, utilities, and local governments, is common in the district heating industry to develop and expand district heating networks.

In some regions, government-owned enterprises or agencies are responsible for developing and operating district heating systems as part of national energy strategies. As the energy transition toward renewables gains momentum, new players, including renewable energy developers and investors, are entering the district heating market to provide low-carbon and sustainable heating solutions. Government regulations and policies play a significant role in shaping the competitive landscape. Regulations encourage or mandate the use of district heating and promote sustainability goals. Companies that invest in research and development and embrace innovative technologies gain a competitive edge by offering more efficient and environmentally friendly district heating solutions.

In 2020, Vattenfall Ab and Deutsche Telekom signed an energy supply deal based on solar power for 10 years. The electricity will be derived from a 60 MW solar park which will be developed in 2021 in Western Pomerania, Mecklenburg.

In another collaboration, UN Environment has partnered with Korea International Cooperation Agency (KOICA) to facilitate the transfer of clean energy technologies and expansion of markets for the same technologies throughout Central Asian countries.

District Heating Industry Ecosystem

District Heating Market Scope: Inquiry Before Buying

| Global District Heating Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 215.24 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.2% | Market Size in 2032: | USD 287.08 Bn. |

| Segments Covered: | by Heat Source | Coal Natural Gas Renewables Geothermal Biomass & Biofuel Industrial Waste-Heat Others Oil & Petroleum Products Others |

|

| by Component | Heat Exchanger Heat Pumps Heat Meters Others |

||

| by Plant Type | Boiler Combined Heat & Power Heat-Only Boiler Waste-Heat Recovery Plants |

||

| by Distribution Temperature | High Temperature (> 100 °C) Medium Temperature (80–100 °C) Low Temperature (< 80 °C, 4G/5G) |

||

| by Network Type | Closed-Loop Open-Loop |

||

| by Plant Capacity | Less Than Equals to 50 MWth 51–200 MWth 201–500 MWth Greater Than Equals to 500 MWth |

||

| by Ownership Model | Public Utility Private Utility Public-Private Partnership |

||

| by Application | Residential Commercial Industrial |

||

District Heating Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

District Heating Market, Key Players

1. Danfoss

2. Fortum

3. Veolia

4. Vattenfall AB

5. ENGIE

6. Alfa Laval

7. Uniper SE

8. Statkraft

9. Orsted A/S

10. EnBW

11. A2A S.p.A.

12. Wien Energie GmbH

13. ARANER

14. Kelag Energie & Wärme GmbH

15. Iren S.p.A.

16. Nevel Oy

17. Göteborg Energi AB

18. HOFOR

19. FVB Energy Inc.

20. DTE Energy

21. Enwave Energy Corporation

22. CenTrio

23. Cordia Energy

24. Shinryo Corporation

25. Keppel DHCS Pte Ltd

26. SK E&S Co., Ltd.

27. Korea District Heating Corporation (KDHC)

28. Dall Energy A/S

29. Others

Frequently Asked Questions:

1] What segments are covered in the District Heating Market report?

Ans. The segments covered in the District Heating Market report are based on Heat Source, Component, Distribution Temperature, Plant Type, Network Type, Plant Capacity, Ownership Model, Application and region

2] Which region is expected to hold the highest share of the District Heating Market?

Ans. The Europe region is expected to hold the highest share of the District Heating Market.

3] What is the market size of the District Heating Market by 2032?

Ans. The market size of the District Heating Market by 2032 is USD 287.08 Bn.

4] What is the growth rate of the District Heating Market?

Ans. The Global District Heating Market is growing at a CAGR of 4.2 % during the forecasting period 2026-2032.

5] What was the market size of the District Heating Market in 2025?

Ans. The market size of the District Heating Market in 2025 was USD 215.24 Bn.