Global Vegan Food Market Size by Product and Distribution Channel – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2032

Overview

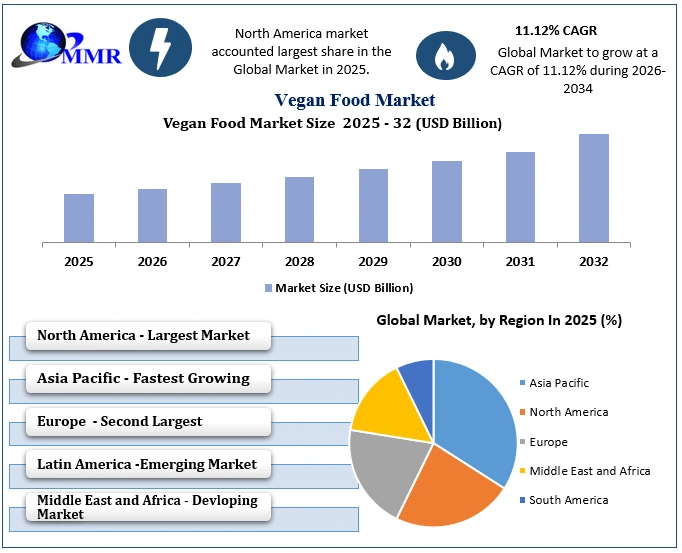

The Global Vegan Food Market was valued at USD 32.28 Billion in 2025 and is expected to reach USD 73.20 Billion by 2032, growing at a CAGR of 11.12% during the forecast period. Market growth is mainly driven by rising health consciousness, increasing adoption of flexitarian diets, growing awareness regarding environmental sustainability, and rising demand for plant-based protein alternatives worldwide among the consumers

An Overview of a Vegan Food Market

The vegan food industry has evolved from a niche dietary segment into a mainstream consumer movement. Consumers are seeking plant-based alternatives by choice to prioritize their health alongside ethics and environmental values. The emergence of lifestyle-related disorders, including obesity, cardiovascular diseases, and diabetes, has accelerated demand for vegan meat, dairy alternatives, plant-based beverages, vegan snacks, and functional food products. Furthermore, growing awareness regarding animal welfare and greenhouse gas emissions associated with livestock production has encouraged consumers to shift toward sustainable food choices.

Technological advancements in food processing, fermentation, and alternative protein development have significantly improved the taste, texture, and nutritional profile of vegan products. The increasing popularity of flexitarian consumers (individuals reducing meat consumption without fully eliminating animal products) has expanded the consumer base beyond traditional vegan communities. Additionally, expanding retail distribution, increasing online grocery penetration, and growing availability of vegan products in restaurants and quick-service chains are supporting long-term market growth.

Key Highlights – Vegan Food Market

• The global vegan food market is projected to reach USD 73.202 Billion by 2032.

• The market is expected to grow at a CAGR of 11.122% during 2025–2032.

• Vegan Meat & Seafood Products dominated the product segment in 2025 due to increasing demand for meat alternatives. The flexitarian consumers are adding contribution to the increasing demand of the vegan meat and seafood.

• Protein Liquids and Powders are expected to witness the fastest growth due to rising trend among the plant based protein consumers adopting a healthy lifestyle through heavy gym workout to meet the post workout nutrition demands

• Offline retail channels accounted for the largest revenue share, supported by supermarkets and hypermarkets. High visibility into the offline stores improves credibility and attracts the consumers.

• Online platforms are growing rapidly due to wider product availability, reviews, ingredient transparency, subscription models, and direct-to-consumer vegan brands.

• North America and Europe remain mature markets and expecting further continuous demand while Asia Pacific is emerging as one of the fastest-growing and dominant regional markets.

• Increasing flexitarianism and demand for clean-label food products are shaping industry growth. Consumers are occasionally preferring to eat meat and animal based foods as well as the purity in the clean – labeled credible vegan food is driving the market growth substantially.

To know about the Research Methodology :- Request Free Sample Report

Vegan Food Market Dynamics

Vegan Food Market Growth Drivers

• The major factor driving the vegan food market growth is the increasing preference for healthier and cleaner diets. Vegan foods which are often rich in fiber, antioxidants, vitamins, minerals, and plant compounds, making them attractive to consumers who focuses on weight management, digestion, heart health, and long-term wellness.

• Environmental sustainability is another major growth factor. Livestock farming is the source of greenhouse gas emission, water consumption, land degradation, and high resource usage. As the rise of climate awareness has made consumers to shift towards sustainable plant-based foods, eco-friendly food products, and low-carbon diet alternatives.

• Ethical concerns are also influencing purchasing behavior. Growing awareness of factory farming and animal cruelty has increased demand for animal cruelty-free food, vegan alternatives, and plant-based diets. Millennials and Gen Z consumers are especially active in adopting vegan and flexitarian lifestyles.

• Product innovation is further strengthening the market. The advancements in food – tech like fermentation technology, improved protein processing, and better flavor development have made plant-based meat, vegan seafood, vegan cheese, plant-based eggs, and dairy-free beverages more appealing to mainstream consumers.

Vegan Food Market Growth Restraints

• High Product Costs Compared to Conventional Food Products

Vegan food products often carry premium pricing due to specialized ingredients, advanced processing technologies, and higher production costs. Plant-based meat, dairy alternatives, and functional vegan products are generally more expensive than conventional animal-based products which limits the adoption among price sensitive customers.

• Taste and Texture Challenges

Although product quality has improved significantly, some consumers perceptions are still susceptible as they perceive vegan alternatives as inferior to traditional meat and dairy products in terms of taste, texture, and overall eating experience. This perception can hinder repeat purchase.

• Nutritional Deficiency Concerns

Consumers often express concerns regarding nutrient deficiencies associated with poorly planned vegan diets, particularly deficiencies in Vitamin B12, iron, calcium, zinc, and protein. These concerns may discourage some consumers from fully transitioning to plant-based diets.

• Limited Consumer Awareness in Developing Regions

While veganism is gaining momentum globally, awareness and acceptance remain relatively low in several developing countries. Cultural food preferences and traditional dietary habits continue to favor animal-based products in many regions, slowing market penetration.

• Supply Chain and Raw Material Price Volatility

The vegan food industry relies heavily on ingredients such as soy, peas, oats, almonds, and coconut. Fluctuations in agricultural production, climate conditions, and raw material prices can affect manufacturing costs and profit margins.

Vegan Food Market Segment Analysis

By Product Type

The vegan food market is be segmented into vegan meat, vegan milk, vegan dairy alternatives, vegan seafood, vegan cheese, vegan snacks, vegan ready meals, protein liquids and powders, and other plant-based products.

Vegan meat and seafood alternatives hold a significant market share because consumers want products that replicate the taste, texture, and cooking experience of traditional meat. These products are especially popular among flexitarians who want to reduce meat intake while maintaining casual eating habits.

Vegan milk and dairy alternatives are also growing strongly due to intolerance towards lactose , dairy allergies, and rising demand for plant-based beverages. Products such as oat milk, soy milk, almond milk, coconut milk, and rice milk are gaining popularity among health-conscious and lactose-intolerant consumers.

Vegan protein powders and liquids are expected to witness strong demand among athletes, gym-goers, wellness consumers, and people seeking convenient protein sources. Pea protein, soy protein, rice protein, and mixed plant protein blends are widely used as sports nutrition and meal-replacement products.

By Distribution Channel

The market is segmented into offline retail and online retail.

Offline distribution channels, including supermarkets, hypermarkets, specialty stores, convenience stores, and health food stores, are currently dominating the market. Consumers prefer offline shopping for food because they can check freshness, packaging, ingredients, and product quality before purchase. Dedicated vegan aisles and in-store promotions are also encouraging trial purchases.

Online distribution channels are growing quickly as e-commerce platforms provide access to a wider range of vegan food products, including niche brands and premium plant-based alternatives. Online retail also benefits from product reviews, detailed ingredient lists, influencer marketing, subscription boxes, and home delivery convenience.

By Source

Soy-Based Products Dominated the Market - Soy remains one of the most widely used raw materials in vegan food manufacturing due to its high protein content, affordability, and versatility. Soy-based ingredients are widely utilized in plant-based meat, dairy alternatives, beverages, and protein supplements, making them a dominant source category.

Pea and Oat-Based Ingredients Gaining Momentum - Pea and oat-based products are witnessing increasing adoption due to their allergen-friendly nature, improved nutritional profiles, and clean-label appeal. Growing consumer preference for soy-free and lactose-free alternatives is expected to support segment growth during the forecast period.

By End User

Household Consumers Accounted for the Largest Revenue Share - The household consumer segment dominated the market owing to increasing health consciousness, growing awareness regarding sustainable diets, and rising adoption of vegan and flexitarian lifestyles.

Foodservice Industry Emerging as a Key Growth Segment - The foodservice segment is expected to witness substantial growth due to increasing demand for vegan menu options across restaurants, cafés, quick-service restaurants, and institutional dining facilities. Leading food chains and restaurant operators continue expanding their plant-based offerings to cater to evolving consumer preferences.

Vegan Food Market Regional Insights

North America is one of the leading regions in the vegan food market, supported by high consumer awareness, strong retail penetration, and rising adoption of plant-based diets in the U.S. and Canada. Consumers in the region are increasingly choosing plant-based meat, vegan dairy, and meat-free meals due to health, sustainability, and ethical concerns.

The U.S. vegan food market is growing due to rising veganism, flexitarian eating, restaurant adoption, fast-food vegan launches, and the expansion of plant-based products in supermarkets. Younger consumers, especially Millennials and Gen Z, are major contributors to demand.

Europe is a major market for vegan food products, driven by climate awareness, animal welfare concerns, and strong consumer interest in sustainable eating. Countries such as Germany, the UK, the Netherlands, and France are witnessing increased demand for plant-based foods, vegan cheese, meat substitutes, and dairy-free alternatives.

European supermarkets and foodservice brands are actively expanding vegan product ranges. Major food chains and restaurants are launching plant-based menu items, while manufacturers are focusing on improving taste, affordability, and nutritional quality.

Asia Pacific is expected to be one of the fastest-growing regions in the vegan food market. Growth is supported by rising urbanization, health awareness, lactose intolerance, growing middle-class income, and increasing concern about food safety and sustainability.

Countries such as China, India, Japan, South Korea, and Australia are seeing growing acceptance of plant-based food, especially among younger urban consumers. India and China are important markets due to large populations, dietary shifts, and increasing demand for healthier food alternatives.

South America, the Middle East, and Africa are emerging markets for vegan food. Growth is still at an early stage, but increasing health awareness, startup activity, and interest in innovative meat substitutes are creating new opportunities. Brazil and other Latin American countries are seeing rising demand for plant-based proteins, while the Middle East is gradually adopting vegan and health-focused food trends.

Recent Developments in Vegan Food Market

Recent developments in the vegan food market show strong innovation and expansion by major companies and startups.

• Eat Just launched its vegan chicken product, Just Meat, made from wheat and soy protein, across thousands of Walmart stores in the U.S.

• Vegan Food Group and Eat Just formed a partnership to manufacture and supply Just Egg across Europe, supported by investment in automation and production facilities.

• The Bel Group and Climax Foods partnered to develop plant-based cheese products.

• Starbucks and Imagine Meats introduced vegan food products in India, including vegan wraps, vegan sausage croissant rolls, and vegan buns.

• Planet Based Foods partnered with online vegan marketplace Vejii Holdings to expand digital sales.

• Target launched its Good & Gather Plant-Based brand to strengthen its vegan and plant-based product portfolio.

• Nestle launched Wunda, a pea-based vegan milk alternative.

These developments show that the market is moving toward better product quality, wider retail availability, stronger foodservice adoption, and improved accessibility for mainstream consumers

Vegan Food Market Scope: Inquire before buying

| Vegan Food Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 32.28 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 11.12% | Market Size in 2032: | USD 73.20 Bn. |

| Segments Covered: | by Product Type | Vegan Meat & Seafood Products Vegan Dairy Alternatives Protein Liquids & Powders Vegan Snacks & Confectioner Ready-to-Eat & Ready-to-Cook Vegan Meal Others |

|

| by Source Type | Soy Almond Oat Wheat Pea Coconut Pulses Others |

||

| by Distribution Channel |

Supermarkets & Hypermarkets Specialty Stores Convenience Stores Online Retail Foodservice Channels |

||

| by End-User | Household Consumers Foodservice Industry Institutional Buyers |

||

Key Players – in the Vegan Food Industry

Vegan Meat & Meat Alternatives

1. Beyond Meat

2. Impossible Foods

3. Conagra Brands (Gardein)

4. Kellanova (MorningStar Farms)

5. Amy's Kitchen

6. Lightlife Foods

7. Quorn Foods

Vegan Seafood Alternatives

8. Good Catch Foods

9. Impossible Foods

10. Beyond Meat

11. Sophie's Kitchen

12. OmniFoods

13. New Wave Foods

Vegan Milk & Plant-Based Beverages

14. Danone (Alpro, Silk)

15. Oatly Group AB

16. Califia Farms

17. Blue Diamond Growers

18. The Hain Celestial Group

19. Nestlé (Wunda)

Vegan Cheese & Dairy Alternatives

20. Daiya Foods

21. Follow Your Heart

22. Violife

23. Bel Group (Nurishh)

24. Miyoko's Creamery

25. Kite Hill

Vegan Yogurt & Desserts

26. Danone

27. Daiya Foods

28. Oatly Group AB

29. So Delicious Dairy Free

30. The Coconut Collaborative

Vegan Ready Meals & Frozen Foods

31. Amy's Kitchen

32. Conagra Brands

33. The Hain Celestial Group

34. Nestlé

35. Beyond Meat

36. Impossible Foods

Vegan Snacks & Confectionery

37. The Hain Celestial Group

38. General Mills

39. Mondelez International

40. PepsiCo

41. Nestlé

Vegan Protein Ingredients & Supplements

42. Axiom Foods

43. ADM

44. Cargill

45. Roquette

46. Ingredion

47. Kerry Group

48. Glanbia

Vegan Egg Alternatives

49. Eat Just

50. Vegan Food Group

51. Follow Your Heart

52. Nabati Foods

53. Simply Eggless

Retail & Private Label Plant-Based Products

54. Target Corporation

55. Tesco

56. Sainsbury's

57. Aldi

58. Walmart

59. Kroger

60. Carrefour

Key players are focusing on product innovation, alternative protein development, strategic partnerships, acquisitions, and geographic expansion to strengthen their presence in the rapidly growing vegan food market.

Frequently Asked Questions

Q1. What is the projected market size of the Global Vegan Food Market by 2032?

The Global Vegan Food Market is expected to reach USD 73.202 Billion by 2032, growing at a CAGR of 11.122% during the forecast period.

Q2. What factors are driving the growth of the Vegan Food Market?

Growing health awareness, rising adoption of plant-based diets, environmental concerns, and increasing demand for sustainable food products are driving market growth.

Q3. Which product segment dominated the Vegan Food Market in 2025?

The Vegan Meat & Seafood Products segment dominated the market due to increasing consumer preference for meat alternatives.

Q4. Which region held the largest share of the Vegan Food Market?

North America held the largest market share owing to purchasing power of the consumers , expanded distribution channel and growing health awareness

Q5. Who are the major players in the Vegan Food Market?

Key players include Beyond Meat, Impossible Foods, Danone, Oatly Group AB, and Nestlé.

Q6. Which distribution channel accounts for the largest market share?

The offline distribution channel, including supermarkets, hypermarkets, and specialty stores, accounted for the largest market share.

Q7. What are the key trends shaping the Vegan Food Market?

Key trends include the growing popularity of flexitarian diets, innovation in alternative proteins, clean-label products, and expansion of plant-based food offerings.

Q8. What opportunities exist in the Vegan Food Market?

Increasing demand for functional plant-based nutrition, growth of e-commerce platforms, and expansion into emerging markets present significant opportunities for market players.