South America Offshore Support Vessel Market – Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2029

Overview

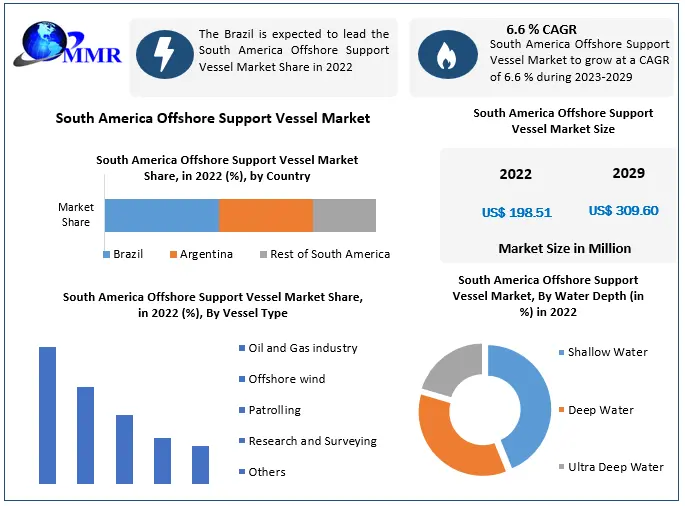

The South America Offshore Support Vessel Market size was valued at USD 198.51 Million in 2022 and the total South America Offshore Support Vessel Market revenue is expected to grow at a CAGR of 6.7 % from 2023 to 2029, reaching nearly USD 309.60 Million.

The South America offshore support vessel market plays a pivotal role in facilitating the exploration and production of oil and gas at sea. Among the key players in the South America offshore support vessel industry, Brazil stands out as a significant contributor, obtaining 95% of its oil production from offshore sources despite economic and political challenges. The success of the South America offshore support vessel (OSV) industry hinges on critical success factors (CSFs) that dictate its functioning and performance. These CSFs encompass both macro and micro aspects and have been identified through a mixed-methodology approach involving input from scholars and practitioners in the oil and gas supply chain. The expansion of the offshore oil and gas sectors has fuelled a growing demand for OSV these vessels have evolved into technologically advanced entities with diverse functions, ranging from seismic surveying and platform supply to anchor handling, construction, and more.

The market for offshore support vessels has a positive global economic impact, bolstered by increased business volume and port activities on the high seas. Brazil's maritime support vessel market is notably dynamic, with the country ranking among the top ten global oil and natural gas producers. The Brazilian Ministry of Mines and Energy's "Ten Year Energy Expansion Plan 2029" estimates Brazil's position to rise to the fifth largest producer in the medium term. Deep-water production dominates Brazil's oil and gas sector, constituting a substantial portion of the industry's activities. By the end of 2019, 93% of Brazilian oil and gas production occurred at sea, reinforcing the nation's focus on offshore production. This commitment prompted a resurgence in Brazil's naval industry, driven by factors such as the Fleet Renewal Program for Maritime Support initiated in 1999. This program facilitated the construction of support vessels for platforms and secured eight-year service contracts, contributing to the reinvigoration of the Brazilian naval sector.

South America Offshore Support Vessel Market Scope and Research Methodology:

The South America Offshore Support Vessel (OSV) Market analysis encompasses a comprehensive evaluation of the region's industry, focusing on the utilization of OSVs for offshore oil and gas operations. The study delves into key aspects including market trends, growth drivers, challenges, and market segments. The research methodology employs a mixed approach, combining quantitative and qualitative techniques. Primary data is collected through interviews and surveys with industry experts, stakeholders, and practitioners involved in the OSV sector. Secondary data sources include reputable industry reports, market databases, and scholarly publications. The scope spans various dimensions, including vessel types, water depth categories, market dynamics, and regional insights from countries like Brazil and Argentina. The research aims to provide stakeholders with a comprehensive understanding of the South America Offshore Support Vessel Market, shedding light on its current status, future growth prospects, and potential challenges. The study serves as a valuable resource for strategic decision-making within the evolving offshore support vessel landscape in South America. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

South America Offshore Support Vessel Market Dynamics:

Brazil and Guyana Lead Offshore Expansion in South America with $30 Billion Investment:

Investments in offshore oil and gas Greenfield projects across Latin America are anticipated to surge to their highest levels in a decade, with Brazil and Guyana spearheading this growth with a projected combined spending of $30 billion. The region is asserting itself as a leader in both deep-water and shallow-water activity, synergizing with the North Sea and the Middle East to drive global offshore expansion. Rystad Energy's analysis forecasts a remarkable uptick in global offshore oil and gas project investments, expecting expenditures to reach $214 billion within the next two years. Notably, annual Greenfield capital expenditure (capex) is set to exceed $100 billion in 2023 and 2024, marking a consecutive two-year achievement not seen since 2012 and 2013.

Brazil is slated to amplify its spending from $20.5 billion in 2022 to $23 billion this year, while Guyana's investments will rise from $5 billion to $7 billion year-on-year. The developments include Brazil's deployment of 16 floating, production, storage, and offloading (FPSO) units across six fields by the end of the decade. These initiatives underscore the enduring significance of offshore oil and gas production, particularly as the global energy landscape evolves towards lower carbon-intensive methods. While the prospects are promising, the sector is not without challenges. Bottlenecks in subsea umbilicals, risers, and flowlines (SURF), sub-suppliers for essential equipment like Christmas trees, yard capacity limitations, and labor shortages pose potential obstacles. Escalating material costs and price hikes among suppliers may test project feasibility. Nonetheless, as the offshore industry gains momentum in Latin America and beyond, it remains a pivotal driver in advancing sustainable energy transitions and reducing carbon footprints on a global scale. Challenges Mount for South America's OSV Sector in Wake of Oil Price Decline:

Challenges Mount for South America's OSV Sector in Wake of Oil Price Decline:

The South America offshore support vessel market is grappling with significant challenges due to the persistent decline in global oil prices. This has created a tumultuous environment for the OSV subsector, which plays a crucial role in supporting offshore drilling operations. Historically generating over $25 billion in annual revenues, the sector is now facing a turbulent period as exploration and production companies curtail rig counts. Notably impacted are platform supply vessels and anchor-handling tug supply vessels, key segments of the OSV market. The sector is witnessing layoffs, vessel stacking, and delays in new ship construction, compounded by rising debt burdens. The drop in oil prices from over $100 a barrel in early 2018 to under $30 a barrel in early 2019 has led to reduced demand for service vessels and crews, resulting in diminished revenues and squeezed day rates.

The shrinking rig counts serve as a bellwether for the struggling OSV market, a trend unlikely to reverse due to the ongoing low oil prices. Fewer active rigs translate to reduced demand for OSVs, particularly anchor-handling tug supply vessels, and platform supply vessels. Rapid fleet growth, partly driven by constant production at Chinese shipyards and easy credit access for operators, has intensified this mismatch between vessel and rig counts. Global and regional exploration and production companies' budget cuts have further exacerbated the situation, prompting a push for cost reductions in services and vessel day rates. This trend is accompanied by a growing preference for more cost-effective onshore projects over offshore ventures. The South America offshore support vessel market is confronted with a complex landscape characterized by reduced margins and contract prices, reflecting the broader challenges posed by lower oil prices.

| Sr. No. | Type | Basin | Out of Operation | In Operation |

| 1 | Drillship | Santos | 0 | 11 |

| Campos | 0 | 3 | ||

| Sergipe | 0 | 1 | ||

| 2 | Fixed-prod | Potiguar | 25 | 4 |

| Sergipe | 24 | 1 | ||

| Campos | 9 | 6 | ||

| Ceara | 9 | 0 | ||

| Espirito Santo | 1 | 2 | ||

| Santos | 0 | 3 | ||

| 3 | Fixed Prod/ Drill | Compos | 1 | 1 |

| 4 | FPSO | Santos | 2 | 22 |

| Campos | 2 | 20 | ||

| Espirito Santo | 0 | 5 | ||

| Sergipe | 0 | 1 | ||

| 5 | FSO | Campos | 0 | 1 |

| 6 | Semi-Sub/Prod | Campos | 4 | 11 |

| 7 | Semi-Sub/Prod/Drill | Campos | 1 | 1 |

| 8 | Semi-Sub Drill | Campos | 1 | 7 |

| Santos | 3 | 0 |

South America Offshore Support Vessel Market Segment Analysis:

Based on Vessel Type, The South America offshore support vessel market is dominated by PSVs and Oil Spill Recovery Vessels (OSRV), constituting nearly half of the fleet. An Anchor Handling Vessel (AHTS) is designed for managing anchors and towing rigs, serving a crucial role in positioning and maneuvering offshore platforms. A tug supply vessel (TSV) combines the functions of towing and supplying, providing essential support in offshore operations. Platform Supply Vessel (PSV) delivers various products and equipment to offshore installations, meeting the multifaceted demands of concessionaires and operators. The South America Offshore Support Vessel market is poised for a promising outlook in 2023, driven by the strategic plans of key players including the state-run oil company Petrobras and various private operators.

The market dynamics are influenced by vessel types that align with the requirements of concessionaires, along with current Brazilian demand and international market trends, with a conservative growth expectation. Private operators with active offshore exploration and production projects in the region encompass Shell, TotalEnergies, Equinor, 3R Petroleum, Trident Energy, Perenco, PetroRio, Karoon, BW Energy, BP Energy, and Petronas. Among these, the most significant demand is observed for Platform Supply Vessels (PSVs), primarily multipurpose vessels featuring multiple product segregations. Designing such specialized PSVs necessitates modifications costing approximately $4.5 million to $5 million per vessel to adhere to technical specifications. The daily rates for these PSVs can reach as high as $40,000 for four-year contracts, enabling the recovery of the initial investment. Petrobras may initiate a new construction program to cater to its growing demand for PSVs, considering an additional requirement of 44 units, some of which are not readily available on the market. This potential shortage extends to other independent oil companies as well, driving the need for foreign-sourced vessels due to limited local content availability. The maritime support fleet in Brazilian waters comprises 410 vessels, with 374 being Brazilian-flagged and 36 foreign-flagged. According to Brazilian legislation, vessels constructed domestically hold preference in contracting processes due to compliance with client-required technical specifications. The South America Offshore Support Vessel Market thrives on the interplay between these vessel types, driven by the specific needs of Petrobras, private operators, and the broader offshore industry landscape.

Based on Water Depth, The South American offshore Support Vessel (OSV) market can be analyzed based on water depth, including shallow water, deep water, and ultra-deepwater segments. The dominating segment within the South America Offshore Support Vessel Market in terms of water depth is deep water. Deepwater regions encompass offshore areas with water depths ranging from around 200 meters to 1,500 meters. Operating in deep waters presents more complex challenges due to higher pressures, harsher environmental conditions, and longer distances from shore. Deep water OSV operations are essential for supporting subsea activities, remotely operated vehicles (ROVs), and more intricate drilling and production setups.

These operations require specialized vessels with advanced equipment to navigate and function effectively in deep water. Shallow water regions typically refer to offshore areas with water depths up to around 200 meters. These areas are characterized by relatively less challenging operational conditions and are often close to the coast. Shallow water OSV operations include activities such as platform supply, anchor handling, and support for drilling and maintenance. Shallow water fields are generally easier to access and develop compared to deeper waters, making them attractive for various exploration and production activities. Ultra deepwater refers to offshore areas with water depths exceeding 1,500 meters. These regions pose even greater technical and logistical challenges compared to deep water. Operating in ultra-deepwater requires highly advanced vessels, equipment, and technology to manage extreme water pressures, deep-sea currents, and complex subsea installations. OSVs in this segment play a crucial role in supporting deep-sea drilling, subsea construction, and specialized research activities.

Deep Water Experience, By Water Depth:

| Water Depth | Length (meter) | Bpd (In 1K) | Country |

| Shallow Water | 475 | 110 | Equatorial Guinea |

| Deep Water | 720 | 100 | Angola |

| 728 | 100 | Angola | |

| 960 | 80 | Equatorial Guinea | |

| 1221 | 100 | Brazil | |

| 1250 | 100 | Angola | |

| 1365 | 120 | Malaysia | |

| 1485 | 100 | Brazil | |

| Ultra-deep Water | 1525 | 120 | Guyana |

| 1600 | 220 | Guyana | |

| 1780 | 100 | Brazil | |

| 1850 | 60 | USA | |

| 1900 | 220 | Guyana | |

| 1900 | 220 | Brazil | |

| 2000 | 180 | Brazil | |

| 2100 | 120 | Brazil | |

| 2120 | 150 | Brazil | |

| 2140 | 150 | Brazil |

South America Offshore Support Vessel Market Regional Insights:

Brazil's OSV market has experienced turbulence due to a corruption scandal involving Petrobras, the state oil producer. The scandal, coupled with low oil prices, led to the cancellation or renegotiation of charter contracts, impacting the stability of the OSV sector. Brazilian-flagged vessels have challenged non-Brazilian-flagged vessels' charters, creating financial and legal complexities for the latter. Despite these challenges, the market for maritime support vessels in Brazil remains dynamic. As one of the world's top oil and natural gas producers, Brazil holds a prominent position, aiming for further growth according to the "Ten Year Energy Expansion Plan 2029" by the Brazilian Ministry of Mines and Energy.

Offshore production, mainly in deep water, drives the industry, with 93% of Brazilian oil and gas production occurring at sea by December 2019. The focus on offshore production has triggered a resurgence in the Brazilian naval industry, especially through the construction of support vessels for offshore platforms. Argentina is another key player in the South America offshore sector. Its OSV market could have varying dynamics compared to Brazil, driven by factors such as government policies, offshore exploration initiatives, and international partnerships. The nation's evolving energy landscape and offshore potential can influence its role in the regional OSV market.

Competitive Landscape

Key Players of the South America Offshore Support Vessel Market profiled in the report include Bumi Armada Berhad, DOF ASA, Hornbeck Offshore Services, Intermarine LLC, Maersk Supply Service A/S, Seacor Marine Holdings Inc., Seam Offshore, Solstad Farstad ASA, Tidewater Inc. This provides huge opportunities to serve many End-users and customers and expand the South America Offshore Support Vessel Market.

Bumi Armada Berhad is a significant player in offshore support services, providing services ranging from floating production, storage, and offloading (FPSO) vessels to offshore support vessels. The company's diversified fleet and experience in managing complex offshore projects position it as a key contributor to South America's OSV market.

DOF ASA is renowned for its specialized fleet of offshore vessels catering to a wide range of offshore operations. The company's extensive fleet includes advanced vessels designed for various roles, from subsea services to platform supply and construction support.

South America Offshore Support Vessel Market Scope: Inquire before buying

| South America Offshore Support Vessel Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2018 to 2022 | Market Size in 2022: | US $ 198.51 Million |

| Forecast Period 2023 to 2029 CAGR: | 6.7% | Market Size in 2029: | US $ 309.60 Million |

| Segments Covered: | by Vessel Type | Anchor Handling Vessel Tug Supply Vessel Platform Supply Vessel Multipurpose Support Vessel Crew Vessel Chase Vessel Seismic Vessel Standby Rescue Vessel |

|

| by Water Depth | Shallow Water Deep Water Ultra Deep Water |

||

| by End User | Oil and Gas industry Offshore wind Patrolling Research and Surveying Others |

||

South America Offshore Support Vessel Market Key Players:

1. Bumi Armada Berhad,

2. DOF ASA

3. Hornbeck Offshore Services

4. Intermarine LLC,

5. Maersk Supply Service A/S

6. Seacor Marine Holdings Inc.

7. Seam Offshore

8. Solstad Farstad ASA

9. Tidewater Inc.

FAQs:

1. What are the growth drivers for the South America Offshore Support Vessel Market?

Ans. Brazil and Guyana Lead Offshore Expansion in South America with a $30 Billion Investment and is expected to be the major driver for the South America Offshore Support Vessel Market.

2. What is the major challenge for the South America Offshore Support Vessel Market growth?

Ans. Challenges Mount for South America's OSV Sector in the Wakethe of Oil Price Decline and is the major challenge for the South America Offshore Support Vessel Market growth.

3. Which country is expected to lead the South America Offshore Support Vessel Market during the forecast period?

Ans. Brazil is expected to lead the South America Offshore Support Vessel Market during the forecast period.

4. What is the projected market size & and growth rate of the South America Offshore Support Vessel Market?

Ans. The South America Offshore Support Vessel Market size was valued at USD 198.51 Million in 2022 and the total South America Offshore Support Vessel Market revenue is expected to grow at a CAGR of 6.7 % from 2023 to 2029, reaching nearly USD 309.60 Million.

5. What segments are covered in the South America Offshore Support Vessel Market report?

Ans. The segments covered in the South America Offshore Support Vessel Market report are Vessel Type, Water Depth, End-Users, and Region.