Polymer Fillers Market by Product, End-Use Industry, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

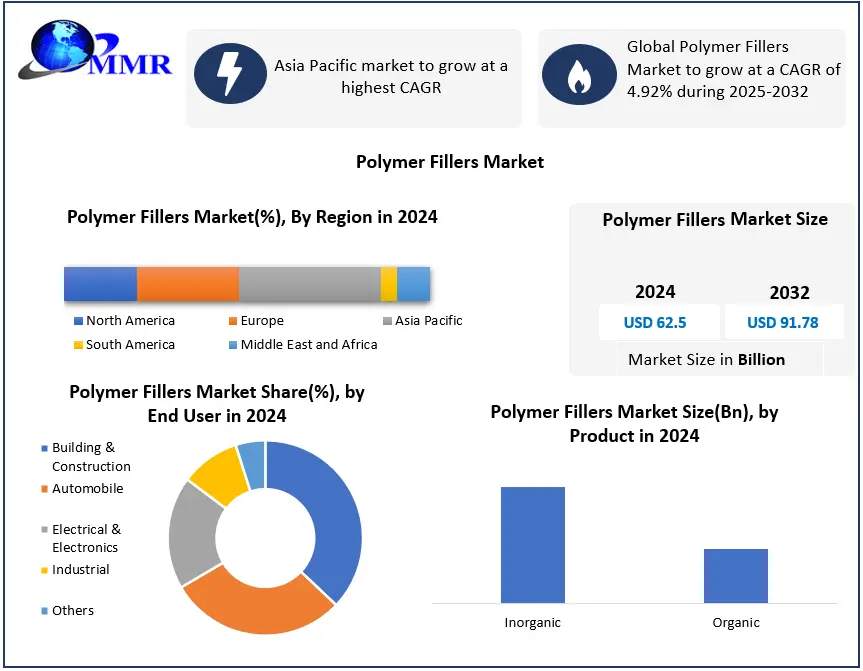

Global Polymer Fillers Market size was valued at USD 62.5 Bn. in 2024 and the total Polymer Fillers Market revenue is expected to grow by 4.92% from 2025 to 2032, reaching nearly USD 91.78 Bn.

Polymer Fillers Market Overview:

It also saves them money. Inorganic (mineral) fillers, such as calcium carbonate or silica-based fillers, or organic fillers, such as polyethylene powder, are examples of polymeric fillers.

The report explores the Polymer Fillers market segments (Product, End-User, and Region). Data has been provided by market participants, and regions (North America, Asia Pacific, Europe, Middle East & Africa, and South America). This market report provides a thorough analysis of the rapid advances that are currently taking place across all industry sectors. Facts and figures, illustrations, and presentations are used to provide key data analysis for the historical period from 2018 to 2023. The report investigates the Polymer Fillers market drivers, limitations, prospects, and barriers. This MMR report includes investor recommendations based on a thorough examination of the Polymer Fillers market contemporary competitive scenario.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Polymer Fillers Market Dynamics:

Driver: Globally growth of end-use industries

The polymer fillers market is driven by the growing end-use industries across the globe. The major factor driving this market is an increase in demand from the automotive industry where lightweight cars with high-performance materials are developed using these products. Other factors such as increasing demand for plastic products and rapid industrialization in developing countries such as China, India, and Brazil would drive the global polymer fillers market.

In the automotive and construction industries, it is widely used

Due to improved qualities such as flexural modulus and heat resistance, the product is employed in a variety of interior and exterior automotive applications. The market for polymer fillers is being fueled by rising plastic consumption in automobiles due to their lightweight qualities.

Organic fillers are in more demand than inorganic fillers

Increased demand for organic fillers over inorganic fillers is expected to boost market growth at a substantial rate during the review period, owing to factors such as easy availability, low cost, and lack of environmental restraints, among others. In addition, the rise in demand for low-cost, high-strength materials, as well as advancements in polymer filler, are some of the drivers expected to boost the market growth in the future years.

Growing of the Aerospace Sector

Polymer fillers like as carbon nanotubes, graphite, graphene oxide, and nanoclay are in high demand in the aerospace industry, as they are desirable structural constituents for aircraft due to their lightweight and equivalent mechanical qualities. India is likely to drive demand for 2,300 aircraft worth US$320 billion over the next 20 years, according to Boeing. As the aviation industry grows, so the demand for polymer fillers, which would act as a growth driver for the polymer filler market.

Opportunity: A common material used in a wide range of applications

Polymer filler is a common material for a variety of applications due to its high-quality qualities and ability to replace expensive plastic resins. Polymer fillers open up new market opportunities, such as novel products that improve molding qualities. Polymers filler's growth is expected to be boosted by increased demand for high strength and lightweight materials in automotive and industrial applications, as well as environmentally friendly applications.

Restraint: High volatility, and production cost

The market is forecasted to be hampered by the high volatility of polymer fillers and the high manufacturing costs of petroleum products. Traditional fillers were initially employed to cut costs and improve composite goods. Traditional fillers such as carbonate, glass fibers, carbon black, and calcium talc, on the other hand, became a vital part of many applications throughout time, notably for reinforcing the mechanical qualities of polymers, resulting in a price increase for carbon fillers. Also, the processing techniques used to make these polymer fillers, such as solvent processing, LBL assembly, and electro-spinning, are not commercially viable. Melt processing is the only economically viable processing method, however, it produces poor dispersion and inferior characteristics. Polymer fillers have a high processing cost because they require significant filler loading for property enhancement, which causes melt movement and processing issues because of the high viscosity of the filled materials. As a result, the high cost of fillers such as carbon and the high cost of filler processing may limit the growth of the polymer filler market during the forecast period.

Polymer Fillers Market Trends:

The rapid growth of the manufacturing sector in countries such as China and India is driving up demand for composite plastics, which in turn is driving up demand for polymer fillers. The demand for polymer fillers in packaging applications is increasing because packaging materials created with polymer fillers are easy to seal and help keep food fresh for extended periods of time. During the projection period, the Asia-Pacific electric vehicle market is predicted to grow at a CAGR of over 20%, reaching USD 350 billion by 2030. During the projected period, this is likely to create attractive chances for the polymer filler market to develop. Imerys and 20 Microns Limited are two big enterprises operating in the Asia-Pacific region. The mentioned factors, together with government backing, are expected to boost polymer filler demand during the forecast period.

Segment Analysis:

Based on Product, the Polymer Fillers Market is segmented into Inorganic, Organic. Traditional inorganic polymer fillers have been used because of their ease of availability and superior characteristics. Calcium carbonate and calcium sulfate are expected to lead the market in 2024, accounting for more than 60% of the inorganic fillers market. Salts are preferred in the construction business since they are less expensive and have appropriate strength. Organic fillers environmentally friendly character has been a key driving element in recent years, and this trend is projected to continue in the future. Organic polymer fillers with low specific gravities, such as shell and wood flour, are likely to save money when used to lengthen resins. Their flame and chemical resistance may vary depending on the degree of polymer loading. Because of its extraordinary strength, carbon fibre is predicted to expand at the fastest rate. Their flame and chemical resistance may vary depending on the degree of polymer loading. Because of its extraordinary strength, carbon fibre is forecasted to expand at the fastest rate.

Based on End-User, Building and construction are expected to dominate the market, accounting for more than 20% of the total. The use of calcium carbonate fillers in building applications accounts for the industry's high penetration. Over the forecast period, the automotive industry is expected to increase the most. Factors. The sector's rapid growth can be due to the growing need for high-strength, low-weight materials. Product demand is also forecasted to be boosted by stricter vehicle emission rules. Because of the rising use of polymer fillers in building and construction activities, the building and construction application held the highest share in the polymer filler market in 2024 and is growing at a CAGR of 4.2 %. Polymer fillers are in high demand in the building and construction sectors for use in floors, windows, pipelines, seals, glass, signage, cladding, and other applications. Due to their great qualities such as low weight, exceptional strength, incredibly durable, cost-effectiveness, and low heat conductivity, polymer fillers are widely utilized in the building and construction industries.

Polymer Fillers Market Regional Insights:

The Asia-Pacific region held the largest market share accounting for 47.3% in 2023.

The regional demand is likely to be driven by rising demand in the automotive, packaging, and construction industries. The Polymer Filler Market is expected to be driven by rapid industrialization in India and China. The Indian government has put in place investment promotion schemes to help enterprises involved in polymer and composite manufacturing. The United States is the world's largest manufacturer of polymer fillers, with key industry players having manufacturing facilities there. The majority of the major players are backward integrated, giving them an advantage over alternative suppliers. Because of the low cost of raw materials and labor, as well as the minimal demand ofortechnological know-how, the threat of new entrants is significant in China, India, and other Asia-Pacific countries. Over the forecast period, the North American market is expected to increase at a high rate. Regional growth is expected to be aided by increased investment in the polymer processing sector. The growing demand for carbon composites in the automotive industry would give market players new opportunities.

The objective of the report is to present a comprehensive analysis of the global Polymer Fillers Market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Polymer Fillers Market dynamic, and structure by analyzing the market segments and projecting the Polymer Fillers Market size. Clear representation of competitive analysis of key players by Design, price, financial position, product portfolio, growth strategies, and regional presence in the Polymer Fillers Market make the report investor’s guide.

Polymer Fillers Market Competitive Landscape:

Imerys, 20 Microns Limited, GCR Group, Minerals Technologies Inc., Quarzwerke GmbH, Hoffman Minerals, Unimin Corporation, Omya AG, Mondo Minerals, LKAB Group, and others are among the major competitors in the worldwide polymer fillers market. Leading companies are boosting their positions by extending their manufacturing capabilities. Polymer fillers are in high demand in a variety of industries, including automotive, construction, packaging, and industrial items. Key players are expanding their product portfolios and developing new products to fulfill rising demand.

Polymer Fillers Market Scope: Inquiry Before Buying

| Polymer Fillers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 62.5 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 4.92% | Market Size in 2032: | USD 91.78 Bn. |

| Segments Covered: | by Product | Inorganic Organic |

|

| by End-User | Building & Construction Electrical & Electronics Automobile Industrial Others |

||

Polymer Fillers Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Polymer Fillers Market, Key Players:

1. Imerys S.A.

2. Lkab Group

3. Minerals Technologies Inc.

4. OMYA AG

5. 20micron Ltd.

6. Hoffmann Minerals

7. GCR Group

8. Unimin Corporation

9. Quarzwerke Group

10. Karntner Montanindustrie Gesellschaft M.B.H.

Frequently Asked Questions:

1. Which region has the largest share in Global Polymer Fillers Market?

Ans: Asia Pacific region held the highest share in 2024.

2. What is the growth rate of Global Polymer Fillers Market?

Ans: The Global Polymer Fillers Market is growing at a CAGR of 4.92% during forecasting period 2025-2032.

3. What is scope of the Global Polymer Fillers market report?

Ans: Global Polymer Fillers Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Polymer Fillers market?

Ans: The important key players in the Global Polymer Fillers Market are – Imerys S.A., Lkab Group, Minerals Technologies Inc., OMYA AG, 20micron Ltd., Hoffmann Minerals, GCR Group, Unimin Corporation,

5. What is the study period of this market?

Ans: The Global Polymer Fillers Market is studied from 2024 to 2032.