Peat Market by Type, Material Type, End User, Distribution Channel and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

The Peat Market size was valued at USD 1669.5 Million in 2025 and the total Peat revenue is expected to grow at a CAGR of 4.22% from 2025 to 2032, reaching nearly USD 2229.68 Million by 2032.

Global Peat Market: Overview

The global peat market is evolving amid rising sustainability concerns, regulatory shifts, and technological advancements. Peat, widely used in horticulture, agriculture, and industrial applications, remains a key resource despite increasing environmental scrutiny. Market leaders such as Legro, and Neova are focusing on sustainable extraction methods, product innovation, and ecosystem restoration to align with global environmental policies.

Regulatory actions are significantly shaping the market. The UK is set to ban horticultural peat by 2026, prompting a shift toward alternative growing media. Additionally, soilless cultivation techniques such as hydroponics and aeroponics are gaining traction, offering increased efficiency, higher yields, and cost savings, impacting traditional peat demand.

The market’s trade dynamics reveal strong global activity. In 2023, India exported $12.6M worth of peat, with key destinations including Morocco ($4.17M), Australia ($3.82M), and Egypt ($3.16M). India also imported $2.7M in peat, primarily from Latvia ($1.3M), Lithuania ($631k), and Estonia ($581k). The fastest-growing export markets were Saudi Arabia, Ecuador, and Lebanon, while imports surged from Estonia, Lithuania, and the UK.

Sustainability initiatives are driving shifts toward eco-friendly alternatives such as cocopeat, valued at USD 1669.5 M in 2025 and projected to reach USD 2229.68 M by 2032. With growing environmental concerns, companies are investing in responsible extraction and peatland restoration, while industry players explore sustainable substitutes to maintain market relevance. As regulatory frameworks tighten, the global peat market is set to undergo significant restructuring, opening opportunities for innovation and alternative solutions.

To know about the Research Methodology :- Request Free Sample Report

Global Peat Market Dynamics:

Sustainable Practices are expected to Drive Peat Market.

Consumers are increasingly environmentally conscious and seek sustainable products. stricter regulations are pushing the industry towards sustainability. The increasing awareness of the environmental impact of peat extraction has catalyzed a transformation within the peat market is driving growth through the exploration of substitutes and the promotion of sustainable management practices. It has led to the exploration of substitutes and the development of peat alternatives. The peat market, which has traditionally been dominated by several industries such as agriculture, horticulture and energy, has faced a significant paradigm shift as the environmental concerns associated with peat extraction increase. Companies that actively participate in bog restoration projects are expected to demonstrate their commitment to environmental responsibility and potentially create new peat-producing areas over time. The future of the peat market seems to be in sustainable practices. the industry is expected to ensure its long-term viability and cater to the growing demand for environmentally responsible products by embracing sustainability.

Growing horticultural demand is driving the Peat Market.

Peat moss offers exceptional benefits for horticulture. Peat is widely used in horticulture for seed starting, potting mixes, and soil conditioning in nurseries and gardens. Growing interest in gardening and landscaping is increase the demand for peat moss products. In horticulture, peat is used to increase the moisture-holding capacity of sandy soils and to increase the water infiltration rate of clay soils. It is also added to potting mixes to meet the acidity requirements of certain potted plants. Peat used in water filtration and is sometimes utilized for the treatment of urban runoff, wastewater, and septic tank effluent. As sustainable practices become more established, the use of responsibly sourced peat moss is expected to grow in horticulture.

The rise of organic farming is a major trend impacting both the peat and cocopeat markets.

Consumers are increasingly seeking organic food, driving a need for organic farming practices. The surging demand for organically produced goods has reached unprecedented levels. cocopeat has emerged as an ideal product to meet organic food demand. organic farming practices and eco-friendly characteristics have positioned cocopeat as a dominant choice in organic agriculture. It provides essential phytohormones that effectively regulate various aspects of plant growth, development, reproductive cycles, and longevity. It contributes to enhancing the native microflora within the soil, supplementing the soil's cation exchange capacity, and promotion increased microbiological activities.

Cocopeat effectively improves drainage and aeration in potting mixes, promoting healthy root development for plants. It excels at retaining moisture, reducing the need for frequent watering, which is a benefit for both farmers and the environment. Farmers seeking organic certification, which confidently use cocopeat without compromising on plant growth or sustainability goals.

An increase in Interest in Alternative Gardening Substrates is one of the global peat market growth limiting factors.

Rising interest in alternative gardening substrates is a major limiting factor. Consumers are increasingly aware of the environmental impact of peat bog harvesting, driving a shift towards more sustainable alternatives. New alternatives like coconut coir and composted green waste offer comparable or even superior water retention and aeration properties to peat moss, which are readily available in the developing regions. Coconut coir is a popular alternative made from the husks of coconuts, offering excellent drainage and water retention. Development of peat moss blends incorporating sustainable materials or peat moss treated for faster decomposition in the soil are expected to offer more attractive options for the key players operating in the global peat market.

Global Peat Market Segment Overview:

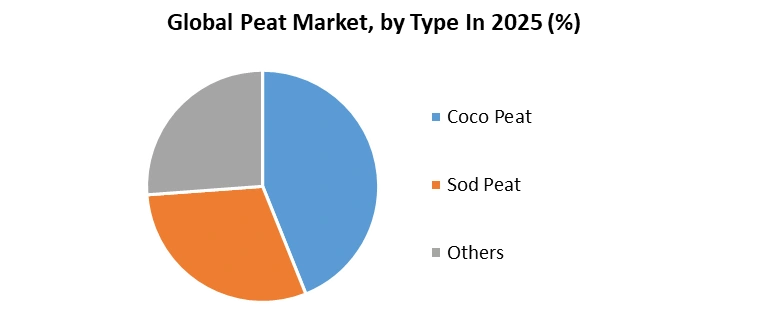

By Type, the Peat Market is segmented into Coco Peat, Sod Peat, and Others. Coco Peat is derived from coconut husks and is widely used in horticulture as a growing medium. It's valued for its water retention properties and ability to aerate soil. Sod peat is also known as turf peat, it's harvested from natural peat bogs and used for various purposes including fuel, gardening, and agriculture. It has historically been used as a source of fuel in some regions. It is a type of organic matter that is harvested from bogs and wetlands for applications such as gardening, agriculture, and horticulture. The Coco Peat segment held the dominant position in the market with a share of 44.50% in 2025. The improvement of farming technologies in numerous places across the world is primarily responsible for the segment's growth. In addition, it is expected that factors including rising demand from many emerging countries, increased usage in the horticulture and agriculture sectors, and growing awareness of reuse and long lifecycle are expected to lead to an increase in demand for coco peat.

By Material Type, the Peat Market is segmented into Sapric, Hemic, and Fabric. Sapric Peat is a type of peat has undergone the most extensive decomposition. It has a dark brown or black color, a finer texture, and a higher humic acid content compared to other types. Sapric peat is less commonly used in horticulture because of its lower water holding capacity. Hemic peat has undergone a moderate level of decomposition. It has a reddish-brown color and a fibrous texture with some visible plant remains. Hemic peat offers a good balance between water holding capacity and drainage. It is popular choice for professional horticulture applications and also used in some fertilizer blends. Fabric peat has undergone the least decomposition. It has a light brown or yellow color, a coarse and fibrous texture with clearly visible plant remains. Fabric peat has the highest water holding capacity. Hemic segment held the leading position in the global peat market with a share of 40.41% in 2024 and is projected to continue its dominance during the forecast period.

By End-Use, the Peat Market is segmented into Agriculture, Fuel & Energy, Domestic, Medicine, and Others. Peat has a large number of uses, which is segmented by agriculture, fuel & energy, domestic, medicine and others. The agriculture and horticulture segment held the dominant position in the peat market in 2025. The agriculture segment represents a significant portion of the global peat market. Peat is widely used as a soil conditioner and growing medium in agriculture, and horticulture.

Demand for peat in agriculture is driven by its ability to improve soil structure, retain moisture, and provide essential nutrients to plants. The segment experiences steady growth because of high adoption rate of peat-based products in commercial farming, greenhouse cultivation, and landscaping. The fuel and energy segment accounts for a smaller but still significant portion of the global peat market. Peat is used as a renewable energy source for heat and electricity generation. The medicinal products include the steroids and antibiotics, and therapeutic applications such as peat baths and preparations. The domestic segment includes the peat finds mainly for gardening in residential and heating purpose. Other segment includes the application areas like water filtration, landscaping, and specialty products.

Global Peat Market Regional Insights:

North America held the dominant position in the global peat market with a value of USD 645.13 Mn in 2025 and it is projected to continue its dominance during the forecast year with a value of USD 886.80 Mn and 4.65% rate of CAGR. North America possesses significant reserves of peat, particularly in regions like Canada and parts of the United States. North America's well-developed agricultural sector, including commercial farming and landscaping industries, creates a steady demand for peat products for soil amendment and crop cultivation.

Global Peat Market Export Data:

Canada holds the top spot for both peat production (estimated 1.3 million metric tons annually) and export. Most Canadian peat goes towards horticultural purposes, supporting plant growth. The Canadian peat industry invests in research related to peat use. Germany follows Canada in peat production and export. Most of the peat produces comes from the lower part of the country in lower Saxony. The country held second rank after Canada in production and exportation. Latvia country comes in third after Germany and Canada. It produces approximately 473 million tons of peat annually. The Netherlands has a long history of peat production, dating back to the 13th century. Large-scale peat production began in the 19th century. Most peatlands were converted for agricultural use. Commercial peat production in Ireland started in the 19th and 20th centuries.

In Europe, Peat is an important factor in the horticultural growing media used in Europe. Some countries also use peat as an energy source. The MMR estimates that the mining and use of peat result in annual emissions of 25.3 million tonnes of CO2 equivalent. Peat usage and production thus spark political discussions in the context of escalating environmental concerns. Climate policies are expected to create carbon leakage due to the peat trade.

Shri Lanka Peat Market Export Dynamics Overview:

The cocopeat industry in Sri Lanka traces its roots to traditional coir extraction for basic products. The industry has experienced substantial growth, with cocopeat now constituting a significant portion of the total coconut production. Out of the 3 billion coconut husks produced annually, approximately 70-75% is utilized for fiber and peat production. The cocopeat industry has seen a surge, producing around 324,000 MT of cocopeat annually in Shri Lanka. Today Cocopeat exports play a pivotal role in the Sri Lankan economy. A significant portion of the cocopeat produced are primarily allocated for the export industry. Intrinsic qualities such as water holding & expansion capacities are some of the factors that expected to create specific demand for Sri Lankan cocopeat products. Currently cocopeat products cater mainly to the horticulture & floriculture industries-both indoor & out door. Sri Lanka has established itself as a key player in the global cocopeat market as the 4 th largest coconut producer in the world and 3rd largest cocopeat exporter.

China is one of biggest new potential markets for peat in the world.

China has a vast and growing agricultural sector, leading to a rising demand for soil amendments and growing media. The demand for peat for different uses in China is estimated on the basis of factors like crop area and peat need per ha. The total demand of growing media for growing seedlings in China is about 49.51 million cubic meters per year. The total estimated peat demand in China is about 250 million cubic meters for all possible applications. Greenhouse growing is a main target market for growing media in the seedling industry. The growth trend of greenhouse area presents the dynamic process of demand increase of professional growing media in China. Degradation, fertilization failures and pollution of agricultural soils are serious problems in China. Food safety is highly challenged. The restoration of degraded and polluted soil is urgent and demands for of soil improvement is massive.

Global Peat Market Industry Recommendation:

Diversification of Product Portfolio: Continue expanding the range of cocopeat products to cater to many industries and their specific requirements. Customized blends, variations in size and production of plant specific ready-to-grow peat products are expected to capture niche markets and offer a competitive edge.

Quality Assurance and Innovation: Maintain a strong focus on quality control and innovation to sustain the intrinsic qualities that make cocopeat unique. Developing enhanced formulations or value-added products, which are expected to attract new market segments.

Market Penetration and Partnerships: Explore new markets and strengthen existing partnerships. Engage in strategic collaborations with agricultural research institutions, governments, and private enterprises to promote peat advantages and expand its applications.

Sustainability Practices: The sustainable practices throughout the production process to boost the eco-friendly reputation of peat.

Market Intelligence and Adaptation: Stay informed about global market trends, demand shifts, and evolving consumer preferences

Global Peat Market Key Findings:

1. North America held the dominant position in the global peat market with a value of USD 666.97 Mn in 2025 and it is projected to continue its dominance during the forecast year with a value of USD 916.82 Mn and 4.65% rate of CAGR.

2. Based on Type, The Coco peat segment held the dominant position in the market with a Value of USD 715.08 Mn in 2025 and expected to grow with a CAGR of 4.82% during the forecast period (2026-2032).

3. The agriculture and horticulture segment held the dominant position in the peat market with a value of USD 639.06 Mn in 2023. The agriculture segment represents a significant portion of the global peat market.

4. Indonesia stands at the forefront among global cocopeat suppliers, exporting approximately USD 500.27 million.

5. Vietnam, Brazil, the Philippines, and Thailand traditionally focused on coconut kernel products, they've now ventured into cocopeat and fiber production.

6. The China, the Netherlands, Russia, and Kenya function as re-exporters within the cocopeat industry.

Peat Market Scope: Inquire before Buying

| Peat Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 1669.5 Mn. |

| Forecast Period 2026 to 2032 CAGR: | 4.22% | Market Size in 2032: | USD 2229.68 Mn. |

| Segments Covered: | by Type | Coco Peat Sod Peat Others |

|

| by Material Type | Sapric Hemic Fabric |

||

| by End User | Agriculture Fuel & Energy Domestic Medicine Others |

||

| by Distribution Channel | Direct Sales Retail & Wholesale Distribution Online Platforms |

||

Peat Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key players in Global Peat Market

North America

1. AB Rėkyva

2. American Peat Technology, LLC

3. Annapolis Valley Peat Moss Co.

4. Beltwide Inc.

5. Lambert Peat Moss

6. Sun Gro Horticulture

7. Theriault & Hachey Peat Moss Ltd.

8. Peat Based LLC

9. Profile Products LLC (USA)

Europe

1. AS Tootsi Turvas

2. BALT WOOD ENTERPRISE SIA

3. Berger Peat Moss

4. Clover Peat

5. Dockers LLC

6. Dutch Plantin Coir India Pvt. Ltd.

7. HAWITA Gruppe GmbH

8. Klasmann-Deilmann GmbH

9. Neova Oy

10. Peatfield

11. Tippland Horticulture

12. Mikskaar AS

13. UAB Solvika

Asia-Pacific

1. Heng Huat Resources Group Berhad

2. Knaap (Thailand) Co., Ltd.

3. Sai Cocopeat Export Private Limited

4. Vasundhra Agro

5. Sriramcocopeat

6. Sai Cocopeat Export Private Limited.

7. AnushikA Agri Products.

South America

1. Rajahrani Impex Private Limited

2. Ferment LLC

3. Middle East and Africa

4. Hortimed Sia

5. SAB Syker Agrarberatungs- und Handels GmbH

FAQ:

1] What segments are covered in Peat Market report?

Ans. The segments covered in Peat Market report are based on Type, Material Type, End User, Distribution Channel, and Region.

2] Which region is expected to hold the highest share in the Global Peat Market?

Ans. Asia Pacific region is expected to hold the highest market share in Peat Market.

3] What is the market size of the Global Peat Market by 2032?

Ans. The market size of Peat Market by 2032 is expected to reach USD 2229.68 Million

4] What is the forecast period for the Global Peat Market?

Ans. The forecast period for Peat Market is 2026-2032.

5] What was the market size of the Global Peat Market in 2025?

Ans. The market size of North America Market in 2025 was valued at USD 1669.5 Million.