Organic Pet Food Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

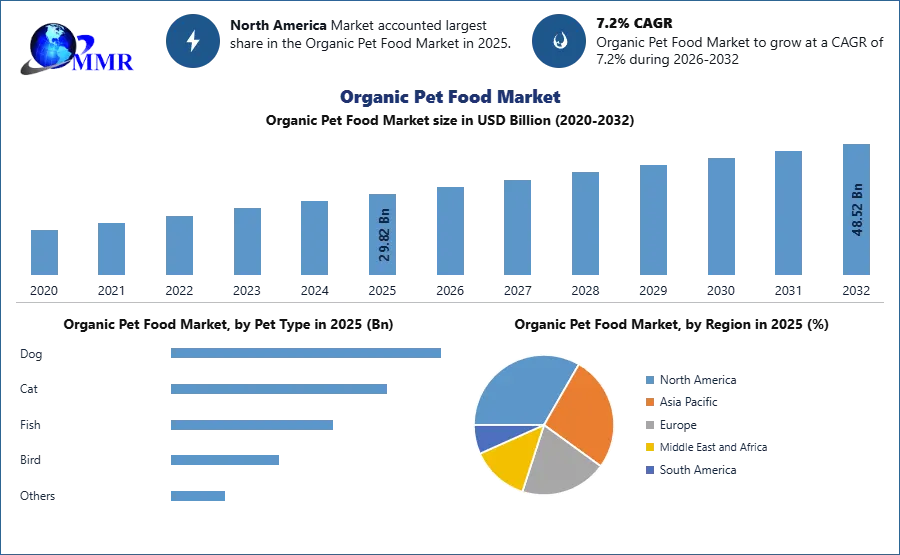

The Organic Pet Food Market size was valued at USD 29.82 Billion in 2025 and the total Organic Pet Food Market revenue is expected to grow at a CAGR of 7.2% from 2026 to 2032, reaching nearly USD 48.52 Billion.

Pet nutrition of the highest quality is becoming increasingly important, with many pet owners shifting to natural and organic products and health supplements as they become more conscious of their pets' healthcare requirements. They want their pet food to be fresh and healthy and prefer it to be served more naturally.

As per the MMR Study, dog food sales grew 52.7% and cat food sales saw a growth of 42.8% in 2025. Organic pet food consists of natural vitamins, proteins, amino acids, fatty acids, and minerals without any preservatives, artificial flavors, or genetically modified content. They are customized according to the pet's breed and age. The most consumed organic pet foods in the US are partially organic and contain varying amounts of nutrient content, adhering to USDA norms. Organic food for pets can lead to improved skin and coat appearance, higher energy levels, and a healthier weight.

Organic pet food has emerged as a lucrative segment of the global pet food market. Major pet food companies such as Nestle, General Mills, and Colgate-Palmolive Company have entered the organic industry to dominate the organic pet food market. To gain more market presence, the manufacturers have streamlined their supply chain network with veterinary hospitals, consulting doctors, and pet homes. The COVID-19 pandemic has accelerated the growth of e-commerce in the organic pet food sector, and a rising number of pet owners now enjoy the convenience and affordability of shopping online for their pet food. To capitalize on this trend, Organic Pet Food Store brands are investing in e-commerce strategies to compete online.

Organic Pet Food Market Scope and Research Methodology:

The Organic Pet Food Industry encompasses a diverse and rapidly evolving industry dedicated to the production and distribution of food products designed for domesticated animals, primarily cats and dogs. This market encompasses various product types, including dry food, wet food, snacks & treats, and specialized products catering to the dietary needs of pets. Understanding the scope and dynamics of this market requires a comprehensive research methodology. Primary research involves conducting surveys, interviews, and collecting data from pet owners, industry experts, and key stakeholders. This data provides real-time information on consumer preferences and market trends. Extensive secondary research is conducted by reviewing industry reports, market analyses, academic literature, and data from reputable sources.

Secondary research validates and complements primary data. Statistical and analytical tools are utilized to process and interpret data. This includes trend analysis, market sizing, and forecasting to assess market potential and growth rates. Detailed analysis of key players, their market strategies, product portfolios, and market share is performed to understand the competitive landscape. Inputs from industry experts and analysts provide valuable qualitative insights into market dynamics and trends. Historical data is examined to trace market evolution and identify patterns that may shape its future. Findings are compiled into comprehensive market reports, which include market size, trends, forecasts, and recommendations for stakeholders in the pet food industry. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Market Dynamics:

Increasing consumer awareness of pet health drives market growth:

Consumer spending on healthcare for their pets has increased in recent decades particularly as the “humanization” of pets grows. This rising pet ownership is providing the necessary boost to the pet-care ecosystem, which involves retail chains, pet nutrition, and services, as well as pet care services.

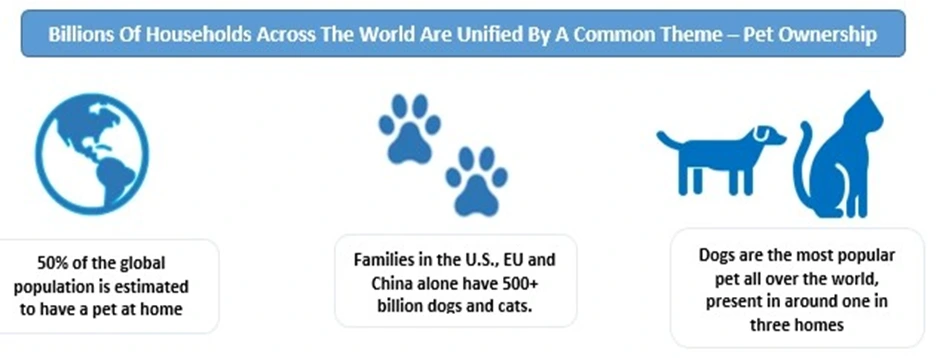

According to the APPA National Pet Owners Survey 2022-2023, 72% of households currently have pets. An increasing population treats their pets like their human family members and selects food based on diet regimens, like veganism. Amazon.com alone yielded millions of searches for pet food products that meet specialty diet keywords such as raw, vegan, and protein, and those with functional ingredients like pumpkin between July 2020 and July 2022. Searches for pet food characteristics including organic, low-calorie, diabetic support pet food saw as much as triple-digit growth compared to the previous years. In the European Union, pet owners spend over €22 billion on pet food each year, with a 2.8% annual growth rate.

The USDA has issued several contradictory statements about organic pet food, creating an uncertain regulatory environment in which key players proceed at their own risk. In Australia, AUS $30.7 billion was spent on pets in 2021, with the bulk of spending going toward pet foods (Organic and Raw), veterinary services, and healthcare products. The above-mentioned factors are expected to boost the Organic Pet Food store during the forecast period. Online platforms have become part of everyday life, and about 4.48 billion social media users worldwide in July 2022. Pet owners use social media extensively in their daily lives, with many owners researching products before purchasing something for their pets. Online customers use multiple search engines like Google, Amazon, YouTube, etc., and also seek recommendations from friends and influencers on social media. With this in mind, social media is becoming an important tool for online pet food businesses for a wide range of reasons, such as the ability to immediately communicate with customers about the most recent information from their company. The pandemic saw e-commerce websites gain market share in the organic pet food industry because people were restricted to time outside their homes. Internet sales of organic pet food have grown steadily in recent years and the pandemic significantly accelerated this trend.

Online platforms have become part of everyday life, and about 4.48 billion social media users worldwide in July 2022. Pet owners use social media extensively in their daily lives, with many owners researching products before purchasing something for their pets. Online customers use multiple search engines like Google, Amazon, YouTube, etc., and also seek recommendations from friends and influencers on social media. With this in mind, social media is becoming an important tool for online pet food businesses for a wide range of reasons, such as the ability to immediately communicate with customers about the most recent information from their company. The pandemic saw e-commerce websites gain market share in the organic pet food industry because people were restricted to time outside their homes. Internet sales of organic pet food have grown steadily in recent years and the pandemic significantly accelerated this trend.

Social media has contributed to the increase in organic pet food sales for various reasons, such as advertising the latest promotions that a business wants to offer. Integrating a blog page is also important to increasing traffic and improving overall engagement with an online organic pet food market. Social networking is a great advantage for Natural Pet Food stores as well as online pet food businesses. The average individual spent around 2.5 hours per day on social media last year; this presents a great chance for Natural Pet Food Store to try to grab the attention of pet owners looking for products for their pets. Increasing demand for the Organic Dog Food segment drives market growth:

Increasing demand for the Organic Dog Food segment drives market growth:

Increasing dog populations in the U.S., Germany, the UK, France, South-East Asia, Argentina, and other key countries are expected to fuel the overall Organic Dog Food and snacks industry by 2029. According to the American Pet Product Association (APPA), more than 69% of U.S. households have a pet and are investing more money in pet care. Organic dog food is becoming increasingly popular as pet parents strive to provide the healthiest nutrition for their pups. Organic dog food is made from ingredients without the use of pesticides, synthetic fertilizers, or other chemicals during its manufacturing. The food also contains zero genetically modified organisms (GMOs) or antibiotics.

Organic dog food is more expensive than regular products, but it has several advantages for dogs. Increasing dog ownership along with rising concerns about dog health has led to an awareness of specialized and commercially available dog food & snacks, contributing to a considerable increase in the Organic Pet Food market size by 2029. Higher-income customers are more likely to spend money on nutritious and organic pet food to improve their pet's health. The widespread availability of products in a variety of price ranges is increasing the global potential volume of organic dog food. Shifting Pet Owner Attitudes Fuel Transformation in the Pet Food Market:

Shifting Pet Owner Attitudes Fuel Transformation in the Pet Food Market:

The global Natural pet food market is experiencing significant transformation, presenting a range of opportunities for businesses to thrive in this evolving industry. This transformation is primarily driven by shifting consumer attitudes and preferences, with pet owners increasingly viewing their furry companions as cherished family members. There is a growing demand for nutritionally dense pet food products. Pet owners want food that meets their pets' specific dietary needs, emphasizing ingredients rich in fiber, protein, vitamins, and minerals. Brands like Royal Canin have capitalized on this opportunity by offering specialized diets for different breeds and health conditions.

They provide breed-specific formulas and therapeutic diets tailored to pets with specific health concerns. Consumers are increasingly seeking all-natural and sustainable pet food options, pushing companies to reduce artificial additives and emphasize environmentally responsible practices. For instance, The Honest Kitchen, a pet food company, focuses on using human-grade, whole-food ingredients. Their commitment to sustainability includes recyclable packaging and environmentally friendly sourcing.

There's a growing trend towards personalized pet nutrition and innovation in pet food products. Consumers want options that cater to their pet's unique needs and lifestyles. PetPlate offers personalized meal plans for dogs, with recipes tailored to individual dietary requirements. They deliver freshly cooked meals directly to customers' doors, combining personalization and convenience. Pet owners are increasingly prioritizing their pets' behavior and mental well-being, creating opportunities for products that enhance pets' mental performance. Kong, known for its durable dog toys, introduced the Kong Genius line, designed to mentally stimulate dogs and provide mental enrichment through treat-dispensing puzzles. As sustainability concerns expand, there's a need for pet food companies to address water usage and reduce their environmental footprint. Wild Earth, a pet food company, uses yeast-based proteins as an alternative to traditional animal proteins, reducing water consumption and greenhouse gas emissions in pet food production.

Organic Pet Food Market Segment Analysis:

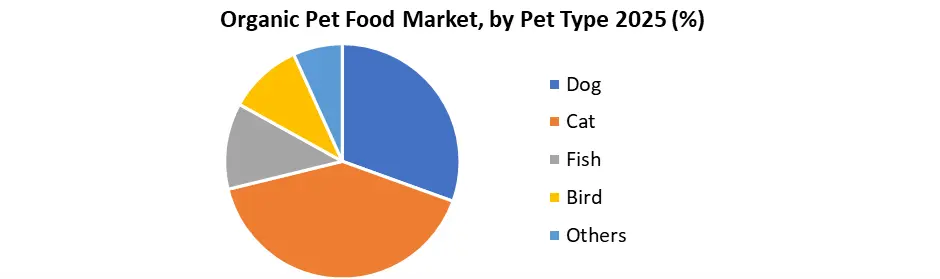

Based on Pet Type, the dog segment dominated the market in 2025 and is expected to grow in the forecast period because of the rising adoption of dogs to reduce stress and improve cardiovascular health. The growing dog population and dog owners’ concern about the health and well-being of their pets are expected to increase market demand. Because of increased consumer awareness of pet health concerns, dog weight control and improvement have gained increasing attention.

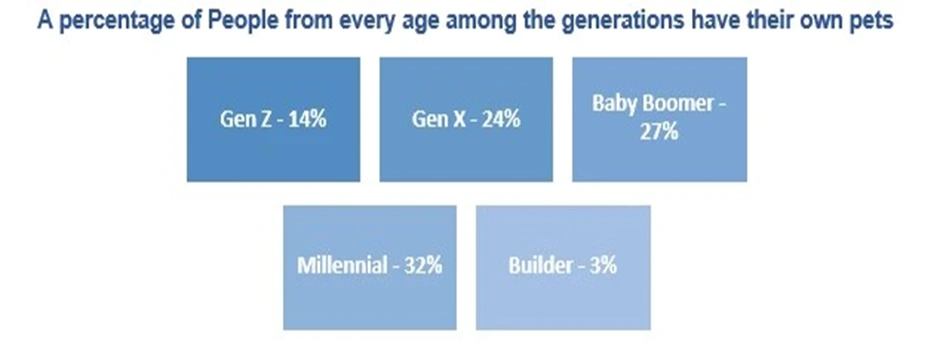

More millennial pet owners grew up in a more health-conscious scenario, showcasing the upward trend towards organic dog pet food and it is expected to grow on a similar trajectory. Lord Jameson's Holiday Treats, an artisan dog bakery, announced plans to produce a limited-edition line of holiday-themed, organic dog food products in 2020, with recipes including Gingerbread, Holiday Cobbler, and Hanukkah Gelt. This collection's formulas are handmade without corn, wheat, artificial chemicals, dairy, preservatives, or GMOs, and the products are rolled in organic coconut flakes for extra nutrition and flavor.

Based on Product Type, the Organic dry pet food segment led the market in 2025 and is expected to dominate the market over the forecast period. The advantages associated with dry organic pet food such as an enriching environment and convenience in cleaning teeth have fueled the growth of this segment. Longer shelf life, along with increased demand for dry pet food by pet owners due to non-spill and easy storage advantages, contribute to the global growth of the dry pet food market.

Based on the Distribution Channel, the online retail segment is expected to grow at the fastest CAGR because of rising smartphone penetration and an increase in the number of online sales channels such as Amazon, Flipkart, and others. Customers all around the world may access several different products via e-commerce sites. Customers may buy the products of their choice while sitting in their homes or offices. Online retail is the fastest-growing distribution channel for the organic pet food industry because of factors such as ease of access, availability of a wide range of products, and the convenience offered by these channels in terms of product delivery, cashback, discount coupons, and attractive deals.

Organic Pet Food Market Regional Insights:

In North America, the Organic Pet Food market accounted for the highest revenue share in 2025. Increased pet ownership and consumer knowledge of pet health can be attributed to the growing demand for organic Pet Food Stores and Natural Pet Food Stores. Furthermore, the introduction of private-label retail brands, as well as an increase in urbanization and disposable income, are among the primary factors driving the growth of the Natural pet food market in North America. The United States has the largest number of confirmed COVID-19 cases in North America, out of all key countries. The pandemic has had a significant influence on the pet food business in North America and its subsidiaries, particularly the organic pet food sector. Natural Pet Food Store is widely available through a variety of distribution channels, and the introduction of e-commerce platforms has benefited the industry's growth. Furthermore, the increased demand for pet food with customized diets and meal plans as well as door-to-door delivery is boosting online organic pet food stores in the North American region.

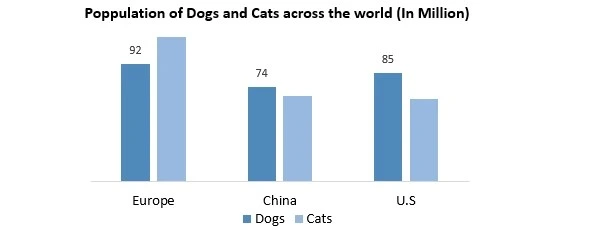

The Europe region is expected to grow at a CAGR of 6.5 % during the forecast period. According to the revenue generation study by country, the United Kingdom, Germany, France, and Italy have made the greatest contributions to Europe's organic pet food market. Pet food items are becoming increasingly popular in Europe, where manufacturers are developing new and innovative products. The pet owners are taking great care of the ingredients to give a better living for their pets. With a shift in consumer preference, companies are trying to offer Natural Pet Food stores, organic, and non-processed products. Organic pet food store goods are sold in Europe in the amount of 6.5 billion tons per year. Germany has around 10 million dogs which is the second-highest dog population in Europe as of 2023. The rising popularity of organic food in Italy and Germany is expected to fuel the Natural Pet Food market growth.

Competitive Landscape

Key Players of the Organic Pet Food Market profiled in the report are Bailey's Bowl, Benevo, Biopet Pet Care Pty Ltd, Blues Buffalo, Castor & Pollux Natural Petworks, Diamond Naturals, Evanger's, Diamond Pet Foods, etc., Evanger's Dog & Cat Food Company, Inc., Harrison’s Bird Foods, Hill’s Pet Nutrition, Inc., Honest Kitchen, Kirkland Signature, Lily’s Kitchen, Mars, Incorporated, Newman's Own, Inc., Organix, PetGuard Holdings, LLC, Primal, Purina PetCare (Nestle), Stella & Chewy's, Wellness Core. This provides huge opportunities to serve many End-users and customers and expand the Organic Pet Food Market.

Kormotech, a prominent pet food manufacturer from Ukraine, has established Kormotech Ventures, a London-based company, to expand its presence in international markets and support potential pet food startups. Kormotech has made a significant investment by acquiring a majority share in Rocketo, a British company specializing in organic air-dried dog food. This strategic move signifies Kormotech's commitment to both global expansion and innovation within the pet food industry.

After acquiring Pooch & Mutt in 2023, Czech pet food manufacturer Vafo Group is furthering its growth in the domestic market. Vafo Group's marketing manager, Tereza Alvarez Sone, revealed investments in new technology at their Chotoviny wet feed factory. This includes process streamlining, automated packaging, and the addition of a new canning line.

Canadian pet food company Healthy Bud is set to introduce superfood-infused mini-training treats for dogs, crafted from natural ingredients. These treats mark the brand's first addition to its product range in two years. They will be available for sale in both Canada and the United States.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 25 March 2026 | Nulo Pet Food | The company launched its Silky Mousse Kitten line, a protein-forward formulation designed to replace common starch binders with high-quality nutrients. | This expansion targets the fast-growing cat ownership demographic, which is currently outpacing dog ownership growth in major markets. |

| 12 March 2026 | Wellness Pet Company | The brand debuted new wet cat formats and dog meal pouches at the Global Pet Expo 2026, marking its centennial milestone. | The launch strengthens the company's position in the premium wet food segment, catering to the demand for high-moisture, protein-rich diets. |

| 15 January 2026 | The Honest Kitchen | The company significantly expanded its retail distribution of certified organic pet food across major North American specialty and e-commerce channels. | This move increases the accessibility of human-grade organic nutrition, directly competing with traditional shelf-stable kibble brands. |

| 01 December 2025 | The Nutriment Company | The group completed the acquisition of Zoo Factory, a major Polish distributor of premium and natural pet treats. | The acquisition marks a strategic entry into the Eastern European market, consolidating the group's regional presence in the natural pet care sector. |

| 22 October 2025 | Merrick Pet Care | The Castor & Pollux brand introduced new organic formulations specifically targeting digestive health and food sensitivities in adult dogs and cats. | This release addresses the growing functional pet food trend by combining certified organic status with specific therapeutic health benefits. |

| 15 May 2025 | Nestlé Purina | Nestlé invested in the Indian startup Drools, valuing the pet food manufacturer at $1 billion to support its global expansion. | The investment provides Purina with a stronger foothold in the Asia-Pacific market, which is currently the fastest-growing region for pet nutrition. |

Organic Pet Food Market Scope: Inquiry Before Buying

| Organic Pet Food Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 29.82 USD Billion |

| Forecast Period 2026-2032 CAGR: | 7.2% | Market Size in 2032: | 48.52 USD Billion |

| Segments Covered: | by Pet Type | Dog Cat Fish Bird Others |

|

| by Product Type | Dry Food Wet Food Others |

||

| by Distribution Channel | Supermarkets and Hypermarkets Specialty Stores Online Retail Others |

||

| by Flavor | Unflavored Flavored Others |

||

| by Pet Life-Stage | Puppy/Kitten Adult Senior |

||

Organic Pet Food Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Organic Pet Food Market Report in Strategic Perspective:

- Nestlé Purina PetCare

- Mars Petcare Inc.

- The J.M. Smucker Company

- Hill's Pet Nutrition (Colgate-Palmolive)

- General Mills (Blue Buffalo)

- The Honest Kitchen

- Castor & Pollux (Merrick Pet Care)

- Newman's Own

- Wellness Pet Company

- Natural Balance Pet Foods

- Canidae Pet Foods

- Yarrah Organic Petfood B.V.

- Primal Pet Foods

- Tender & True Pet Nutrition

- Open Farm

- Evanger's Dog & Cat Food Company

- Diamond Pet Foods

- Stella & Chewy's LLC

- Smallbatch Pets LLC

- Lily's Kitchen

- Party Animal Inc.

- Grandma Lucy's

- OrgaNOMics Pet Food Company

- Nulo Pet Food

- The Nutriment Company