Ocean Carbon Removal Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

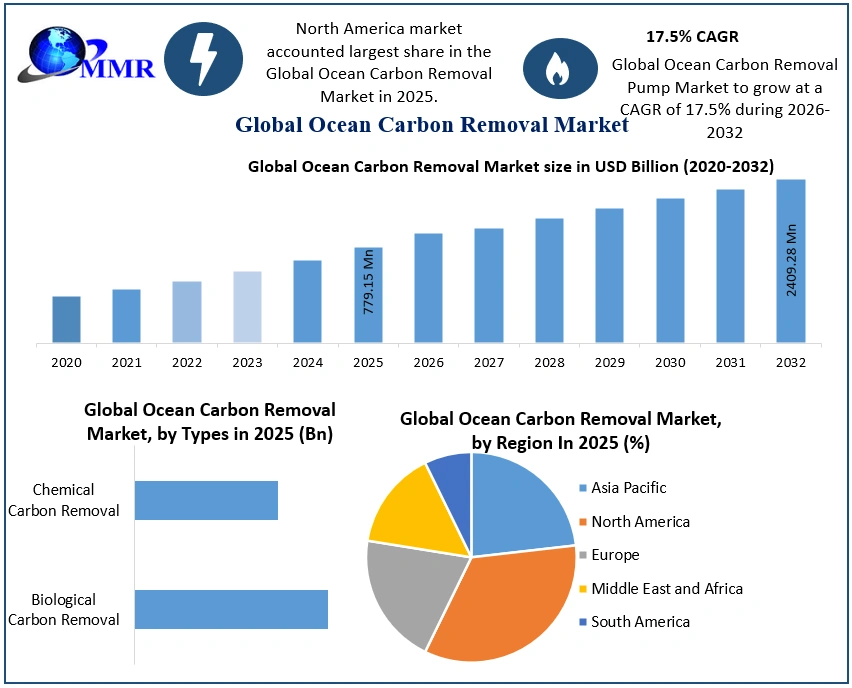

The Ocean Carbon Removal Market size was valued at USD 779.15 Million in 2025 and the total Ocean Carbon Removal revenue is expected to grow at a CAGR of 17.5% from 2026 to 2032, reaching nearly USD 2409.28 Million by 2032.

Ocean Carbon Removal refers to the process of mitigating carbon dioxide (CO2) levels from the Earth's atmosphere by leveraging the natural ability of the oceans to absorb carbon. This involves various techniques and approaches aimed at enhancing the ocean's capacity to sequester CO2, reducing its concentration in the atmosphere, and addressing climate change. The Ocean Carbon Removal Market has seen significant growth and attention due to heightened global concerns about climate change and its impact. The Ocean Carbon Removal market has witnessed increased investments and technological advancements in various methods, driving the development of innovative strategies for efficient carbon removal from oceans.

Key players such as Brilliant Planet, Captura, Ebb Carbon, Equatic, Ocean-Based Climate Solutions, and Planetary have been instrumental in pioneering solutions in this domain. Several driving forces underpin Ocean Carbon Removal market growth. Favorable government policies and initiatives globally supporting carbon removal have acted as catalysts for market growth. The urgency to combat climate change has spurred research and development, resulting in innovative and sustainable carbon removal technologies. The increasing awareness and acceptance of carbon credit programs has also encouraged investments in ocean carbon removal initiatives, propelling Ocean Carbon Removal market growth.

Emerging trends indicate a growing focus on collaborative efforts among governments, businesses, and environmental organizations to foster advancements in ocean carbon removal. Moreover, a shift towards innovative solutions such as direct air capture (DAC) technology and the exploration of blue carbon credits from ocean-based sequestration projects has marked new opportunities within the Ocean Carbon Removal market. Additionally, trends show an increasing emphasis on exploring various techniques like biochar sequestration, reef restoration, aquaculture, and iron fertilization to enhance carbon removal. Microsoft's entry into ocean carbon removal has signaled a significant development in the market. By incorporating ocean carbon removal into its portfolio, Microsoft has joined the league of organizations aiming to bolster these initiatives, contributing to advancements and scaling up carbon removal efforts. This move is anticipated to inspire similar investments and collaborations, further propelling Ocean Carbon Removal market growth and innovation.

To know about the Research Methodology :- Request Free Sample Report

Market Dynamics:

Climate Change Mitigation and Environmental Regulations are the major drivers of the ocean carbon removal market:

The most compelling impetus driving the ocean carbon removal market is the urgent global need to combat climate change. The increasing levels of carbon dioxide (CO2) in Earth's environmental atmosphere are the most prominent catalyst for global warming and the subsequent environmental consequences. Ocean-based carbon removal solutions are gaining prominence because they offer a promising approach to curbing atmospheric CO2 levels and mitigating the adverse effects of climate change. This driver is rooted in the universal acknowledgment of the severe and escalating threats posed by climate change, including phenomena such as rising sea levels, extreme weather events, and disruptions to ecosystems. The ocean carbon removal market is significantly influenced by increasingly stringent environmental regulations and emissions reduction targets enacted by governments and international organizations. These regulations serve as a potent catalyst for the development and adoption of carbon removal technologies.

Businesses and industries are facing mounting pressure to reduce their carbon emissions, compelling them to consider carbon removal solutions as an appealing option for achieving compliance with environmental mandates. As regulatory requirements continue to evolve and strengthen, the demand for effective carbon removal methods is poised to surge. Another pivotal driver of the ocean carbon removal market is the growing interest and financial support emanating from diverse stakeholders. These stakeholders include private investors, philanthropic organizations, and governmental entities. Their investments inject substantial capital into research, development, and the deployment of ocean carbon removal technologies. The recognition of carbon removal as a critical climate solution has kindled heightened interest in the investment community, thus fostering innovation and scalability in the market. Financial backing is indispensable for propelling these technologies forward and making them accessible on a broader scale.

Environmental Concerns and High Costs are the dominating restraints of the ocean carbon removal market:

A paramount constraint confronting the ocean carbon removal market pertains to the prospect of unintended environmental repercussions linked to specific removal methodologies. These apprehensions center on the potential alteration of marine ecosystems and the induction of ocean acidification. The intricate challenge lies in achieving an equilibrium between the necessity of carbon removal and the safeguarding of ecological integrity. The imperative task involves ensuring that carbon removal methods do not inflict harm on marine life or disrupt delicate ecosystems, which demands nuanced and meticulous approaches.

Many ocean carbon removal techniques entail considerable financial investments in implementation and ongoing operation. The substantial cost factor constitutes a deterrent, as these methodologies may lack economic viability in the absence of financial incentives or subsidies for the Ocean Carbon Removal market. The exorbitant expenses linked to technology development, surveillance, and maintenance pose formidable obstacles to widespread adoption. Strategies geared towards cost reduction and securing adequate funding become imperative to surmount this hurdle effectively.

Aquaculture Innovation, Ocean Rainforest Sustainable Practices for CO2 Reduction:

Silver Lining initiative explores this technique to combat ocean acidification and capture CO2 from the atmosphere. Controlled iron release stimulates phytoplankton growth, absorbing CO2 during photosynthesis. Climos is a pioneering company experimenting with this method to potentially enhance carbon capture in the ocean. Innovations in direct air capture (DAC) technology adapted for oceanic use can extract CO2 from seawater.

Companies like Global Thermostat aim to create cost-effective DAC solutions for ocean carbon removal. Establishing robust markets for blue carbon credits encourages investment in oceanic carbon removal initiatives. Groups like the Blue Carbon Initiative focus on creating tradeable carbon credits from ocean-based sequestration projects. For instance, In April , for example, Autodesk, H&M Group, JPMorgan Chase, and Workday dedicated $100M collectively into the Frontier advance market commitment initiative, which enables member companies to pre-purchase high-quality, permanent carbon removal offsets. This adds to the $925M already committed to Frontier from Stripe, Alphabet, McKinsey, Meta, and Shopify last year.

Utilizing biomass-derived biochar, when submerged in the oceans, can sequester carbon for extended periods. Organizations like the International Biochar Initiative are exploring this technique for ocean-based carbon removal. Restoring coral reefs not only conserves biodiversity but also supports carbon sequestration. Entities like The Ocean Agency prioritize reef restoration, recognizing its potential for carbon removal. Integrating carbon-sequestering aquaculture practices like shellfish farming mitigates carbon while meeting food demands. Initiatives such as Ocean Rainforest focus on sustainable aquaculture to reduce atmospheric CO2. Governments incentivizing oceanic carbon removal initiatives through policies and funding foster market growth. For instance, The NOAA Ocean Acidification Program, working in collaboration with the National Oceanographic Partnership Program (NOPP), has disclosed an investment totaling $24.3M. This financial initiative is specifically directed toward fostering collaboration among academic researchers, federal scientists, and industry experts.

The primary objective of this funding is to propel research endeavors in marine carbon dioxide removal. The allocated funds will aid in broadening the comprehension of different facets related to marine carbon dioxide removal strategies. These include understanding associated risks, identifying co-benefits such as mitigating ocean acidification and conducting scientific studies pivotal in establishing regulatory frameworks. Ultimately, the aim is to facilitate the testing and scaling of marine carbon dioxide removal methods, leveraging the combined expertise of multiple sectors to drive forward advancements in this critical area of environmental research. Collaborative policies, like the EU's Ocean Decade initiative, propel research and development in the Ocean Carbon Removal sector, supporting diverse strategies for effective carbon removal from the ocean, thereby driving market growth and innovation.

Ocean Carbon Removal Market Segment Analysis:

Based on Type, The Ocean Carbon Removal Market is segmented into two primary categories, Biological Carbon Removal and Chemical Carbon Removal. Biological carbon removal holds dominance in the Ocean Carbon Removal market due to its natural and environmentally friendly approach to sequestering carbon. It includes various methods such as ocean afforestation, blue carbon initiatives, ocean alkalinity enhancement, and oceanic biochar production. These techniques leverage natural processes and ecosystems like seaweed farming, coastal habitat conservation, and mineral dissolution to absorb and store carbon dioxide. Biological carbon removal methods have gained traction for their sustainable approach and potential to simultaneously benefit marine ecosystems while mitigating climate change effects.

Chemical carbon removal, while showing promise, is still in the nascent stages of development and adoption. This segment involves methods like ocean-based carbon capture technologies, ocean iron fertilization, and ocean reforestation through coral restoration. These methods involve more direct interventions, such as introducing substances like iron to stimulate phytoplankton growth or utilizing carbon capture technologies in oceanic environments. However, chemical methods raise concerns regarding potential ecological impacts and require further research to address these challenges.

Despite its potential, Chemical Carbon Removal faces regulatory and environmental scrutiny, leading to slower adoption rates compared to Biological Carbon Removal. In the forecast period, Biological Carbon Removal is anticipated to continue dominating the Ocean Carbon Removal market due to its proven effectiveness, natural processes, and growing support from environmentalists and policymakers. The adoption of these methods is expected to rise as they offer sustainable, nature-based solutions, aligning with global climate goals and garnering greater acceptance from stakeholders. Chemical Carbon Removal, although poised for advancement, might face regulatory hurdles and scrutiny requiring comprehensive assessments and approvals for wider adoption, thus lagging behind Biological Carbon Removal in market dominance during the forecast period.

Ocean Carbon Removal Market Regional Insights:

North America dominated the Ocean Carbon Removal Market in 2025 and is expected to dominate during the forecast period, due to its extensive investments in research and technological advancements related to carbon sequestration initiatives. The region houses several key players actively engaged in innovative ocean carbon removal projects and research, bolstering its Ocean Carbon Removal Market dominance. For instance, in the United States, research institutions and private companies are actively involved in various ocean carbon removal methods like ocean afforestation, coastal restoration, and carbon capture and storage (CCS) initiatives. The U.S.

Department of Energy (DOE) has allocated $36 million across 11 projects spanning 8 states to expedite the advancement of marine carbon dioxide removal (mCDR) capture and storage technologies. This funding, sourced from the DOE’s Sensing Exports of Anthropogenic Carbon through Ocean Observation (SEA-CO2) program, aims to bolster pioneering initiatives focused on measuring, reporting, and validating mCDR. The projects will strive to pinpoint cost-effective and energy-efficient solutions for carbon removal. The prioritization of innovative methods like mCDR holds immense importance in combating greenhouse gas emissions, aligning with the Biden-Harris Administration’s commitment to addressing the climate crisis and achieving a net-zero emissions economy by 2050. Government support through policies aimed at reducing carbon emissions and fostering sustainable practices has further propelled North America's leadership in the Ocean Carbon Removal Market.

Europe follows closely, exhibiting significant growth potential driven by ambitious climate goals and strong initiatives towards achieving carbon neutrality. European nations like Norway, the UK, and Germany have been investing in projects focusing on ocean-based solutions, such as ocean alkalinity enhancement and blue carbon programs, to reduce carbon dioxide levels. The European Union's strategies aiming for net-zero carbon emissions by 2050 have propelled the region's advancements in ocean carbon removal technologies.

Asia-Pacific, while currently at a nascent stage, shows promising Ocean Carbon Removal Market growth opportunities. Countries like Japan and Australia have started exploring ocean-based carbon removal projects, including ocean reforestation and marine conservation efforts, albeit at a slower pace compared to North America and Europe. With increasing concerns about climate change and rising support for sustainability initiatives, Asia-Pacific is projected to witness accelerated growth in the coming years. This is evident through initiatives like Japan's efforts in ocean afforestation and the Australian government's focus on marine ecosystem restoration projects, indicating a potential surge in the region's Ocean Carbon Removal Market presence and technological advancements in ocean carbon removal in the forecast period.

Competitive Landscape

The landscape of carbon dioxide removal (CDR) technologies has expanded considerably, presenting a diversified portfolio of innovative approaches aimed at curbing greenhouse gas emissions. Direct Air Capture (DAC), traditionally led by companies like Carbon Engineering and Climeworks, DAC has witnessed new entrants such as Noya and Verdox. These startups are innovating DAC technologies by integrating them into existing infrastructure, like cooling towers in buildings, to reduce energy usage.Biomass-based CDR, Companies like Charm Industrial and Kodama Systems are exploring the utilization of organic plant materials for direct carbon removal. Charm Industrial transforms leftover crop biomass into carbon-rich “bio-oil” injected into the ground for carbon sequestration. Kodama Systems focuses on forest management practices and carbon removal through forest thinning.

Mineralization, Companies like Vesta are investigating ocean alkalinity enhancement, employing reactive rocks like olivine mixed with sand to speed up chemical reactions that trap carbon dioxide while replenishing eroded coastlines. Ocean CDR, Ventures like Seafields and Seaweed Generation focus on farming seaweed, like kelp or sargassum, in open oceans to sequester carbon. Methods include sinking the seaweed into the deep ocean, potentially mitigating invasive sargassum growth, and removing carbon. Crop Enhancement, Companies like Living Carbon and Recapture explore enhanced photosynthesis in trees for increased carbon absorption. This involves genetically modified trees or hybrid species bred for better carbon sequestration. These innovative ventures align with the NOAA Ocean Acidification Program’s $24.3M funding and the U.S. DOE's $36M allocation, emphasizing the urgency to develop efficient carbon removal solutions to combat climate change and achieve a net-zero emissions economy.

Ocean Carbon Removal Market Scope: Inquire before buying

| Ocean Carbon Removal Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 779.15 Mn. |

| Forecast Period 2026 to 2032 CAGR: | 17.5% | Market Size in 2032: | USD 2409.28 Mn. |

| Segments Covered: | by Process | Enhanced Ocean Productivity Algae Cultivation Direct Air Capture Ocean Alkalinity Enhancement Subsurface Injection Seaweed Farming Ocean Afforestation Mineralization |

|

| by Types | Biological Carbon Removal Chemical Carbon Removal |

||

| by Application | Climate Change Mitigation Carbon Offset Markets Biofuel Production Marine Ecosystem Restoration Ocean Acidification Mitigation |

||

| by End-User | Government & Regulatory Bodies Private Sector Research Institute Environmental Organization |

||

Ocean Carbon Removal by Regions

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players of the Ocean Carbon Removal Market

1. Brilliant Planet (UK)

2. Captura (United States)

3. Ebb Carbon(United States)

4. Equatic (United States)

5. Ocean-Based Climate Solutions (United States)

6. Planetary Technologies (Canada)

7. Running Tide (United States)

8. Seafields (United States)

9. SeaO2 (Italy)

10. Vesta (United States)

11. Climeworks (Iceland)

12. Global Thermostat (United States)

13. Carbfix (Iceland)

FAQs:

1. What are the growth drivers for the Ocean Carbon Removal Market?

Ans. Climate Change Mitigation and Environmental Regulations are the major drivers of the ocean carbon removal market and is expected to be the major driver for the Ocean Carbon Removal Market.

2. What is the major restraint for the Ocean Carbon Removal Market growth?

Ans. Environmental Concerns and High Costs are the dominating restraints of the ocean carbon removal market are expected to be major restraints In the Ocean Carbon Removal Market.

3. Which country is expected to lead the global Ocean Carbon Removal Market during the forecast period?

Ans. North America is expected to lead the Ocean Carbon Removal Market during the forecast period.

4. What was the Global Ocean Carbon Removal Market size in 2025?

Ans: The Global Ocean Carbon Removal Market size was USD 779.15 Million in 2025.

5. What segments are covered in the Ocean Carbon Removal Market report?

Ans. The segments covered in the Ocean Carbon Removal Market report are by Process, Types, Application, End-User and Region.