Laboratory Information System Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

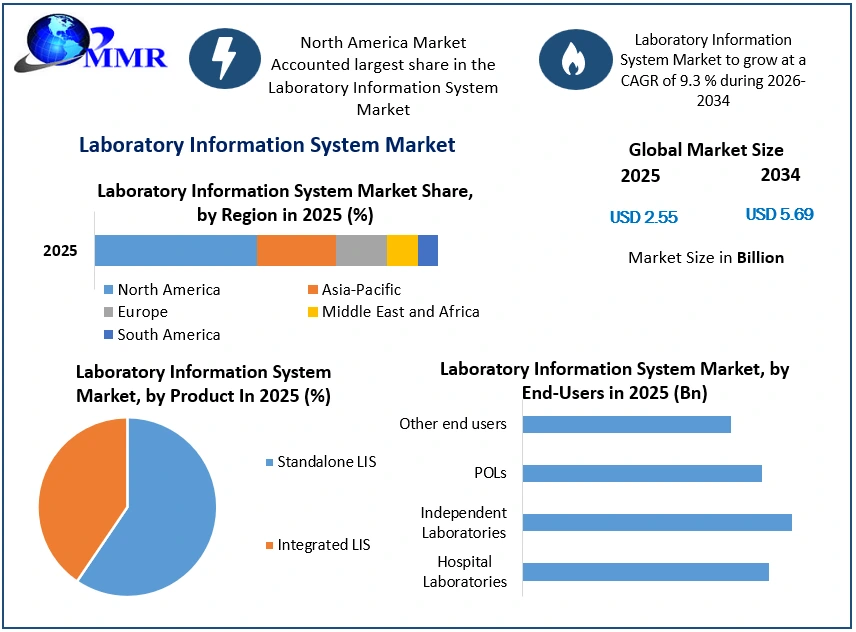

Laboratory Information System Market size was valued at USD 2.55 Bn. in 2025 and the total Laboratory Information System (LIS) revenue is expected to grow at 9.3% from 2026 to 2034, reaching nearly USD 5.69 Bn.

Laboratory Information System Market Overview:

Laboratory Information System (LIS) efficiently manages the flow of samples and patient data to improve lab efficiency. It increases access to high-quality diagnostic testing while also providing accurate and timely information for patient treatment. Raster LIS aids in the standardization of workflows, testing, and procedures while also offering precise process controls. Laboratory equipment (both unidirectional and bidirectional) may be coupled with Raster LIS using Raster IoMT to automate data collection and calibration. The completely integrated configuration tools aid in adjusting the product to end-user requirements while maintaining maintenance and future upgrades.

The growing demand for lab automation and innovation in R&D labs, particularly in pharmaceutical and biotechnological laboratories, is driving the laboratory information system (LIS). The high accuracy and efficiency outcomes of laboratory informatics solutions are boosting the laboratory informatics market globally.

According to a 2025 survey conducted by MMR, a professional healthcare IT service provider, 61% of LIMS users benefited from the elimination of manual operations, 57% improved their sample management approach, and 46% saw a significant increase in productivity within their laboratory setting.

With laboratory informatics, technological improvements have enabled healthcare professionals and scientists to prepare samples and carry out diagnoses with more precision and accuracy, hence driving the market growth. LabVantage Analytics, for example, was introduced in March 2021 by LabVantage Solutions, Inc., one of the leading providers of laboratory informatics systems and services, including purpose-built LIMS solutions that allow laboratories to go online sooner and at a lower overall cost.

It is a self-service, full-featured advanced analytics tool that enables users to effortlessly explore, analyze, and visualize LIMS, corporate, and external data to generate meaningful business insights. Such advances are expected to drive market growth.

Laboratory Information System Market Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Laboratory Information System Market Dynamics:

Rising demand for laboratory automation

Laboratory automation is gaining traction as an effective alternative for addressing the laboratory professional shortage and eliminating manual involvement in lab procedures. Automation of basic laboratory operations, using dedicated workstations and software to control instruments, increases lab efficiency and allows individual researchers to focus on vital tasks. Automation creates higher data and allows for improved documentation. The establishment of supervisory standards, together with severe regulatory requirements for error-free outputs, encourages the creation of efficiencies that provide reproducible results.

Lab automation reduces the risk of human error associated with repetitive tasks such as pipetting and moving plates and it furthers improves accuracy. According to research, error rates for completely automated processes range from 1-5%; for semi-automated operations, 1-10%; and for manual procedures, 10-30%. The appropriate use of integrated workstations, automated analyzers, and total laboratory automation (TLA) allows skilled laboratory professionals to be reassigned to jobs that provide significantly more value to operations.

The exponential increase of data produced by lab systems has created a demand for effective data storage, processing, and sharing solutions. Laboratory information systems provide an excellent solution to this requirement since they greatly enhance, advance, and increase the productivity and efficiency of laboratory activities.

Expensive servicing and maintenance costs

The expensive service and maintenance expenses with LIS are a significant constraint to market growth. The cost of maintaining IT systems exceeds the cost of the product itself. Service and maintenance (which includes modifying the software to meet changing user requirements) are recurrent expenses that account for around 20-30% of the total cost of ownership. In addition, the training and implementation costs account for around 15% of the total cost.

Because of these limitations, it is difficult for many small and medium-sized laboratories to invest in these systems, restricting their adoption and eventually the market growth. However, as cloud-based LIS options develop, the impact of this restriction is expected to reduce during the forecast period.

Rising adoption of cloud-based LIS

The adoption of cloud-based services has resulted in considerable advancements in the LIS industry. Virtualization advancements and greater access to high-speed internet allow for rapid innovation, generally at a reduced cost. Companies that use cloud-based solutions simply have to pay for software subscriptions rather than a complete license. This technique considerably decreases the expenses associated with in-house implementation, cost per user, and IT personnel expenditures.

However, unlike thick-client or on-premise LIS solutions, cloud-based LIS solutions do not require any upfront capital investments for hardware, reducing the strain on healthcare providers, reducing the need for IT workers, and providing quick and secure data transmission.

Pharmaceutical corporations are more likely to use centralized corporate-based facilities to build a virtual network of contract research, development, and manufacturing organizations (CRDMOs) and academic institutions. The use of cloud-based solutions would assist these businesses in coping with the massive amounts of data created by these operations, as well as in lowering the total cost of ownership of LIS. Cloud-based models have emerged as viable solutions for managing LIS systems, presenting considerable growth potential to LIS suppliers due to benefits such as improved data accessibility, cost-effectiveness, and real-time analysis.

Interfacing concerns with diverse laboratory systems

The changing nature of laboratory processes, technology, and screening activities has made it increasingly vital to simplify laboratory operations. Because of the changing nature of laboratory work, automated systems with higher flexibility and interface capabilities are required. A better interface allows for greater flexibility and the capacity to quickly establish different application-oriented activities, resulting in enhanced productivity and data consistency in businesses. Some laboratories may have instruments that are a decade old and require a different but effective type of interface. One of the biggest issues vendors have is offering software solutions that are compatible with a wide range of laboratory systems.

Laboratory Information System Market Segment Analysis:

Laboratory Information System Market By Product, the Integrated LIS segment held the biggest market share of about 68% and dominated the market in 2025. This segment is expected to maintain its dominance at the end of the forecast period. This segment's growth may be attributable to numerous critical benefits such as automated laboratory administration, lower risk of mistakes, instrument and equipment integration, and greater overall efficiency. Additionally, integrated LIS eliminates the need for manual order input, reducing the risk of human mistakes and saving time. For order input and tracking, the system utilizes barcode technology with an interface to LIS.

In general, integration refers to the process of merging elements so that they operate together or create a whole. There are numerous popular usages in information technology:

1. Integration during product development is the process of combining components or subsystems and addressing difficulties in their interconnections.

2. The application components were all created concurrently with a common objective and/or architecture.

3. The operating system, programming language, and database are all shared by the application modules.

The term "interface" refers to software and technology that conceptually joins two computers or various application modules and allows them to communicate with one another. The device or component that physically and logically connects other devices or systems and allows them to interact. The physical link between application modules or hardware components allows data to be exchanged so that they can efficiently interact or function together.

The major distinction is that with integration, the different modules are architecturally homogenous, sharing a similar operating system, database, and programming language, whereas interfaces are often heterogeneous and differ in software design. If done correctly, either can enable compatibility inside the LIS.

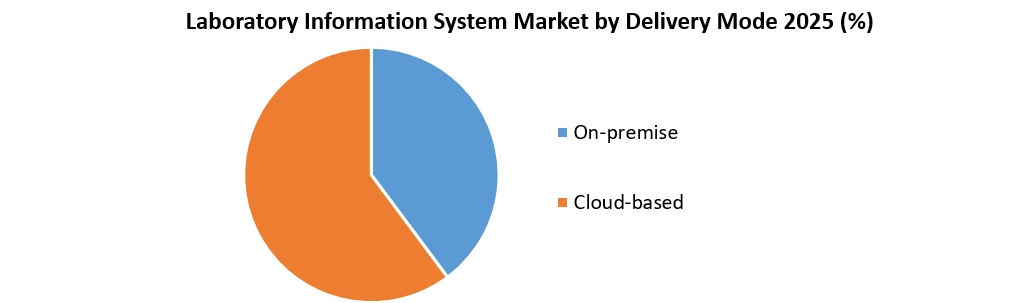

Laboratory Information System Market By Delivery Mode, the On-Premise segment dominated the market with the highest market share in 2025 and is expected to grow at a CAGR of 9% during the forecast period. On-premise software needs laboratories to have a software license. Because this licensed copy remains within the laboratory, it can provide far more data security than Cloud-based distribution. This is critical since the patient data being held is very sensitive and legally protected.

To perform successfully, an on-premise solution requires in-house server infrastructure, software licenses, integration capabilities, and IT personnel. However, in the Cloud, the services would be provided by a third-party host.

However, the Cloud-based delivery mode segment is also expected to grow at a CAGR of 8.5% during the forecast period owing to its significantly lower costs. Cloud storage is a more powerful technology than it appears. Cloud storage has almost no storage capacity constraints, which greatly benefits the laboratory information management system and other healthcare applications.

1. The data centers offer a greater bandwidth for accessing the servers. That is more than enough to provide for traffic-free access.

2. Because cloud servers contain several redundant systems, there is always a backup, and data loss is not an issue.

3. The laboratory management system's centralized data center allows authorized users to access data from anywhere in the world.

4. When compared to standalone LIMS, the upkeep of these servers is incredibly cost-effective.

5. Because LIMS is hosted in the cloud, it may link many stakeholders. Users may also manage sample tracking, processing, and delivery. In business, scalability is simple.

The connectivity of LIMS cloud-based software servers also connects patients to the Laboratory Information Management System's internal workings. Patients can simply maintain track of their data because the LIMS software made the information freely accessible. This also allows people to easily maintain their health records up to date.

Laboratory Information System Market Regional Insights:

North American regional market held the largest market share of about 40% and dominated the market followed by Europe with 36% and the Asia Pacific with 20% in 2025. This region is expected to maintain its dominance in terms of the market share at the end of the forecast period because of the region's well-established healthcare IT sector and government initiatives to make laboratory services more affordable. It also dominates the laboratory informatics sector and is expected to do so during the forecast period.

In addition, the improved infrastructure and increased demand for digitalized technologies in North America are driving the adoption of various analytical solutions across various industries. North America's market dominance may be linked to the US and Canadian economies, which have permitted considerable investments in new technologies, an increase in biobanks, convenient availability of LIMS products and services, and severe regulatory requirements across sectors.

The United States has dominated the laboratory informatics market in North America because of the growing adoption of digital healthcare in the country and growing investments in creating innovative laboratory informatics technology in the country. For example, Abbott, based in the United States, has committed USD 2,420 million in R&D for the fiscal year 2025. Many significant manufacturers that produce laboratory informatics software, such as Orchard Software Corporation, Cerner, Epic Systems, Roper Technologies, and Comp Pro Med Inc., are situated in the United States, which would contribute to the growth of the industry.

Besides that, the rapid adoption of new services throughout the country is expected to drive market growth. For example, LigoLab Information System disclosed in March 2020 that the business is offering fully integrated and automated LIS support for customer laboratories in California, Washington, and New York that use FDA-approved instruments to execute high-volume COVID-19 testing. In addition, Xybion Corporation, a global low-code SaaS provider that allows digital transformation in a highly regulated industry like Life Sciences, launched the Pristina XD Digital Pathology in August 2021.

Asia Pacific market is expected to be the fastest-growing regional market during the forecast period as a result of the increasing number of LIMS-providing CROs in this region. In 2016, India ranked #1 among 55 evaluated nations in outsourcing for web-enabled services, according to the Global Services Location Index (GSLI).

In addition, some biopharma companies are relocating their manufacturing units to the Asia Pacific for lower-cost production. This is increasing demand for LIMS in Asian countries. Nonetheless, the COVID-19 outbreak pushed stakeholders in developed markets, such as the United States and Europe, to minimize their reliance on Asian nations and return to in-house operations. The primary future markets for LIMS include China, Singapore, India, Brazil, Japan, and Middle Eastern nations. These marketplaces lack government rules and sufficient standards, opening up enormous opportunities for suppliers that are unable to match the requirements established in industrialized nations such as the United States.

China market is expected to dominate the market at the end of the forecast period. The consistently evolving need for laboratory automation and the development of an integrated system for labs is driving the expansion of the laboratory informatics market in China. Additionally, biobanks and biorepositories are driving the demand for laboratory informatics systems. Because of its vast demographics, aging population, frequent epidemics, and so on, China has one of the world's largest healthcare industries.

China National GeneBank (CNGB), the world's largest and most advanced biobank, was established in 2019 at a cost of more than USD 1 billion, with approval and funding from the Chinese government. Biobanking and biorepositories have seen steady growth in the nation, with a chain of biobanks and repositories established in China.

Healthcare and life sciences institutions are key contributors to the market, but other industries such as chemicals, petrochemicals, food and beverages, environmental testing, and so on are also anticipated to adopt the technology and solutions during the forecast period.

Laboratory Information System Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 July 2025 | Clinisys | Clinisys completed the strategic acquisition of Orchard Software Corporation. | The merger creates an expansive LIS portfolio serving over 6,000 laboratories across 39 countries. |

| 10 August 2025 | Oracle Health | Oracle Health launched a new AI-powered EHR platform with enhanced lab data interoperability features. | This integration improves clinical data flow and simplifies lab result exchange within complex hospital workflows. |

| 12 January 2026 | Cerner Corporation | Cerner Corporation introduced an upgraded cloud-native LIS module specifically designed for molecular diagnostics. | The update enables faster turnaround times for high-complexity genomic testing through automated data processing. |

| 22 February 2026 | Epic Systems | Epic Systems expanded its Beaker LIS integration capabilities to support HL7 FHIR R5 standards for real-time diagnostics exchange. | This advancement enhances interoperability between disparate health systems, reducing manual transcription errors. |

Laboratory Information System Market Scope: Inquire before buying

| Laboratory Information System Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 2.55 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 9.3% | Market Size in 2034: | US $ 5.69 Bn. |

| Segments Covered: | by Product | Standalone LIS Integrated LIS |

|

| by Component | Services Software |

||

| by Delivery Mode | On-premise Cloud-based |

||

| by End-Users | Hospital Laboratories Independent Laboratories POLs Other end users |

||

Laboratory Information System Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Laboratory Information System Market, Key Players are

1. Cerner Corporation(US)

2. Dendi, Inc.(US)

3. Computer Programs and Systems Inc.(US)

4. Meditech(US)

5.SCC Soft Computer(US)

6. Epic Systems Corporation(US)

7. Computer Service and Support(US)

8. ASPYRA LLC.(US)

9. Apex Healthware(US)

10. Seacoast Laboratory Data Systems(US)

11. Pathagility(US)

12. LabVantage Solutions(US)

13. HEX Laboratory Systems(US)

14. LigoLab Information Systems(US)

15. Comp Pro Med(US)

16. American Soft Solutions Corp.(US)

17. Allscripts Healthcare Solutions, Inc.(US)

18. WebPathLab(US)

19. XIFIN(US)

20. CompuGroup Medical(Germany)

21. Alphasoft GmbH(Germany)

22. Clinsis( Australia)

23. TECHNIDATA (UK)

Frequently Asked Questions:

1. Which is the potential market for the Laboratory Information System (LIS) in terms of the region?

Ans. North America is the potential market for the Laboratory Information System (LIS) in terms of the region.

2. What are the opportunities for new market entrants?

Ans. The key opportunity in the market is the rising adoption of cloud-based LIS.

3. What is expected to drive the growth of the Laboratory Information System Market in the forecast period?

Ans. A major driver in the Laboratory Information System Market is the Rising demand for laboratory automation.

4. What is the projected market size & growth rate of the Laboratory Information System Market?

Ans. Laboratory Information System Market size was valued at USD 2.55 Bn. in 2025 and the total Laboratory Information System (LIS) revenue is expected to grow at 9.3% from 2026 to 2034, reaching nearly USD 5.69 Bn.

5. What segments are covered in the Laboratory Information System Market report?

Ans. The segments covered are Product, Component, Delivery Mode, End Users, and Region.