Middle East Medical Imaging Market – Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2030

Overview

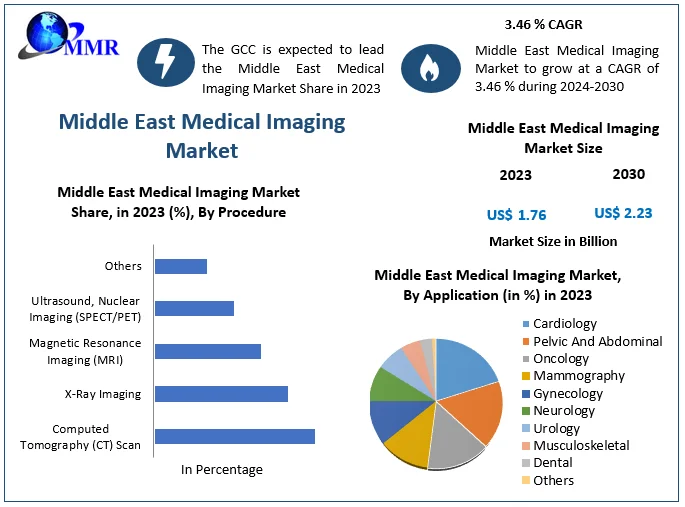

The Middle East Medical Imaging Market size was valued at USD 1.76 Billion in 2023 and the total Middle East Medical Imaging Market revenue is expected to grow at a CAGR of 3.46% from 2024 to 2030, reaching nearly USD 2.23 Billion.

Middle East Medical Imaging refers to the use of various imaging modalities and technologies for diagnosing and monitoring diseases and conditions in the countries of the Middle East region. These imaging techniques include X-rays, computed tomography (CT), magnetic resonance imaging (MRI), ultrasound, nuclear medicine, and molecular imaging. Medical imaging plays a crucial role in modern healthcare by providing detailed images of the internal structures of the body, aiding healthcare professionals in accurate diagnosis, treatment planning, and monitoring of patients.

The Middle East Medical Imaging Market is experiencing significant growth driven by factors such as increasing healthcare expenditure, growing prevalence of chronic diseases, rising demand for advanced diagnostic techniques, and government initiatives to improve healthcare infrastructure. The market includes a wide range of imaging modes and technologies, including X-ray, CT, MRI, ultrasound, nuclear medicine, and molecular imaging. Countries like the United Arab Emirates (UAE), Saudi Arabia, Qatar, and Kuwait are witnessing substantial investments in healthcare infrastructure, leading to the growth of medical imaging facilities and the adoption of advanced imaging technologies.

The growing demand for advanced diagnostic imaging services is driven by the rising burden of chronic diseases such as cardiovascular diseases, cancer, and diabetes. Government initiatives aimed at promoting preventive healthcare and early disease detection are fueling the adoption of medical imaging technologies. The increasing preference for minimally invasive diagnostic procedures, coupled with advancements in imaging modalities such as MRI and CT, is driving growth. Moreover, the growing medical tourism industry in the Middle East is boosting the demand for high-quality imaging services, further propelling Middle East Medical Imaging Market growth.

Technological advancements in imaging modes, increasing investment in healthcare infrastructure, and rising awareness of the benefits of early diagnosis. The market is witnessing a trend towards the adoption of AI-driven imaging solutions, which enhance diagnostic accuracy and efficiency. The emergence of telemedicine and teleradiology is creating opportunities for remote interpretation of imaging studies, especially in underserved areas. With the growing demand for personalized medicine, there is a rising focus on precision imaging techniques for tailored treatment approaches.

Key market players in the Middle East Medical Imaging Market have been actively involved in strategic initiatives to expand their presence and introduce innovative imaging solutions. For example, Siemens Healthineers launched the SOMATOM X.cite CT scanner, featuring AI-powered technologies for personalized imaging. Philips Healthcare introduced the Ingenia Ambition X MRI system, offering high-resolution imaging with reduced scan times. GE Healthcare collaborated with healthcare providers in the region to implement advanced imaging solutions and improve patient care.  To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Market Dynamics:

AI-Powered Medical Imaging Solutions Driving Market Growth:

The integration of AI-powered medical imaging solutions, like Lunit's INSIGHT MMG, drives Middle East Medical Imaging Market growth by enhancing diagnostic accuracy and efficiency. For instance, Lunit's partnership with Dr. Sulaiman Al Habib Medical Group aims to analyze hundreds of thousands of mammography images annually, improving breast cancer detection rates. AI's transformative impact on diagnostics, discussed at events like Medlab Middle East, accelerates healthcare outcomes. AI-driven medical imaging technologies in the UAE, supported by government initiatives, enhance disease detection, and streamline screening processes. Partnerships like United Imaging's collaborations in the Middle East drive market growth by introducing advanced imaging solutions. For example, United Imaging's partnerships in the Gulf countries and Morocco expand access to state-of-the-art PET/MR and MRI systems, improving diagnostic capabilities.

Government initiatives, such as Saudi Arabia's introduction of AI-powered eye screening tests, stimulate market growth by promoting innovation and investment in medical imaging technologies. These initiatives facilitate the adoption of AI-driven solutions, leading to more accurate diagnoses and improved patient outcomes. Increasing demand for advanced imaging services, driven by rising healthcare needs and population growth, fuels Middle East Medical Imaging Market growth. For instance, the Middle East and Africa represent significant markets for United Imaging's products, with over 10,400 hospitals and research institutions utilizing their imaging solutions. The region's status as a medical tourism hub attracts investments in cutting-edge medical imaging technologies, contributing to Middle East Medical Imaging Market growth. Investments in advanced equipment, like PET/MR imaging systems, aim to enhance healthcare services and attract patients seeking high-quality diagnostic and therapeutic procedures.

Collaborative research projects, such as Stratasys and Siemens Healthineers' landmark project, drive innovation in medical imaging. These initiatives focus on developing state-of-the-art solutions, like advanced imaging phantoms for CT imaging, which contribute to technological advancements and market growth. The emergence of precision medicine drives demand for personalized diagnostic approaches, leading to increased utilization of advanced imaging technologies. AI-driven solutions enable tailored treatment strategies by providing precise and comprehensive diagnostic insights, supporting the growth of the medical imaging market. Investments in healthcare infrastructure, including the installation of advanced imaging equipment, contribute to Middle East Medical Imaging Market growth. Agreements like United Imaging's partnership with My Doctor Medical Center in Qatar facilitate the deployment of high-end MRI, CT, and X-ray systems, improving diagnostic capabilities and patient care. Private Healthcare Sector Driving Investments in Advanced Imaging Technologies:

Private Healthcare Sector Driving Investments in Advanced Imaging Technologies:

The growth of the private healthcare sector leads to increased investments in advanced medical imaging technologies. Private hospitals and clinics aim to offer cutting-edge diagnostic services to attract patients, driving the adoption of state-of-the-art imaging equipment. Efforts to raise awareness about the importance of early diagnosis and preventive healthcare drive the demand for Middle East Medical Imaging Market. Educational initiatives targeting healthcare professionals and the general public promote the utilization of advanced imaging technologies for better healthcare outcomes. The integration of telemedicine platforms with medical imaging technologies expands access to diagnostic services, especially in remote areas. Teleimaging services enable healthcare providers to remotely interpret imaging studies, facilitating timely diagnoses and treatment decisions.

Continued advancements in medical imaging technologies, such as AI-driven solutions and 3D imaging, present significant growth opportunities. For example, the Middle East MRI market is expected to be driven by technological innovations. The rising demand for personalized healthcare solutions drives the need for precision medical imaging technologies. The Middle East & Africa Precision Medical Imaging Market is expected to exhibit substantial growth during 2020-2025, reflecting the demand for precise diagnostic tools. Government initiatives to enhance healthcare infrastructure, including the installation of advanced imaging equipment, fuel Middle East Medical Imaging Market growth. For instance, partnerships between healthcare facilities and imaging technology providers, like United Imaging's agreements in the Middle East, boost access to advanced imaging services.

Efforts to raise awareness about the benefits of AI-driven medical imaging technologies and provide training opportunities for healthcare professionals to stimulate market growth. For example, collaborations between United Imaging and research facilities in Saudi Arabia aim to establish research academies for advanced imaging, fostering knowledge exchange and skill development. Efforts to promote medical tourism in the region drive investments in state-of-the-art medical imaging facilities. These investments aim to attract international patients seeking high-quality diagnostic and therapeutic procedures, contributing to Middle East Medical Imaging Market growth. The increasing prevalence of chronic diseases necessitates advanced diagnostic imaging technologies for early detection and treatment. This trend underscores the importance of AI-driven solutions and high-resolution imaging modalities to improve disease management and patient outcomes. Challenges in Access to Advanced Medical Imaging Technology in the Middle East:

Challenges in Access to Advanced Medical Imaging Technology in the Middle East:

Some regions in the Middle East lack access to advanced medical imaging technology due to inadequate infrastructure and resources, hindering the adoption of cutting-edge diagnostic tools. For instance, rural areas face challenges accessing high-resolution MRI or CT scanners, leading to disparities in healthcare quality. Stringent regulations and bureaucratic processes in some Middle Eastern countries delay the approval and deployment of new medical imaging technologies. Complex regulatory frameworks impede Middle East Medical Imaging Market entry for innovative imaging solutions, prolonging the time to market and hindering industry growth. The Middle East faces a shortage of skilled radiologists and imaging technicians, limiting their capacity to operate and interpret medical imaging equipment effectively. This shortage results in longer wait times for imaging procedures and delays in diagnosis and treatment.

The initial capital investment required for purchasing and maintaining advanced medical imaging equipment, such as MRI and PET scanners, poses a significant financial barrier for healthcare facilities in the Middle East. High equipment costs deter hospitals and clinics from upgrading their imaging capabilities, restricting access to state-of-the-art diagnostic tools. Many Middle Eastern countries allocate limited budgets to healthcare, which prioritize other areas over medical imaging technology investments. Budget constraints limit the growth of imaging services, restrict up Equipment Sizes to existing infrastructure, and inhibit the adoption of innovative imaging solutions.

The adoption of AI-driven medical imaging technologies in the Middle East faces obstacles such as skepticism, lack of awareness, and concerns about data privacy and security. Slow adoption rates limit the integration of AI solutions into existing healthcare workflows and hinder advancements in diagnostic accuracy and efficiency. While telemedicine holds promise for expanding access to medical imaging services, the Middle East Medical Imaging Market lacks the necessary infrastructure and connectivity to support widespread teleimaging initiatives. Poor internet connectivity, especially in rural areas, and insufficient telemedicine regulations impede the development and implementation of teleimaging solutions.

Middle East Medical Imaging Market Segment Analysis:

Based on Procedure, Magnetic Resonance Imaging (MRI) and Computed Tomography (CT) Scan are the dominant segments, with MRI holding a slight edge due to its extensive applications in neuroimaging, musculoskeletal imaging, and oncology. CT SCAN, known for its rapid image acquisition and high-resolution imaging capabilities, follows closely, particularly in emergency medicine and trauma cases. X-ray imaging maintains its significance as a widely used and cost-effective imaging modality for various diagnostic purposes, especially in orthopedics and pulmonary imaging.

Ultrasound, favored for its non-invasive nature and real-time imaging capabilities, is rapidly gaining traction in obstetrics, cardiology, and abdominal imaging. Nuclear imaging (SPECT/PET) plays a crucial role in oncology and cardiology, although its adoption is relatively low due to equipment costs and specialized expertise requirements. Other emerging imaging technologies, such as optical imaging and elastography, show promise in niche applications but have yet to achieve widespread adoption. MRI is expected to continue dominating the Middle East Medical Imaging Market, driven by advancements in technology, expanding clinical indications, and increasing demand for non-invasive diagnostic imaging.

Middle East Medical Imaging Market Regional Insights:

The Middle East Medical Imaging Market exhibits variations in regional dominance and growth trajectories. Currently, the Gulf Cooperation Council (GCC) countries, including Saudi Arabia, the United Arab Emirates (UAE), and Qatar, dominate the market due to their robust healthcare infrastructure and substantial investments in advanced medical imaging technologies. For example, Saudi Arabia has witnessed significant growth in MRI installations. Additionally, the UAE is a key player, with initiatives like the Dubai Health Strategy 2018-2022 focusing on enhancing healthcare services, including medical imaging. However, other regions, such as Egypt and Turkey, are also emerging as prominent players, driven by increasing healthcare investments and infrastructure development.

For instance, Egypt's medical imaging market is expected to grow at a considerable CAGR during 2023-2030, reflecting the region's growing demand for advanced diagnostic tools. Moreover, Turkey has witnessed substantial growth in medical tourism, attracting patients seeking high-quality diagnostic and therapeutic procedures, thereby stimulating investments in state-of-the-art medical imaging facilities. As the region continues to focus on improving healthcare access and quality, countries like Egypt and Turkey are expected to witness significant growth in their medical imaging markets, further diversifying the regional landscape and contributing to the overall growth of the Middle East Medical Imaging Market.

Competitive Landscape

These developments signify a significant shift towards AI-driven healthcare solutions in the Middle East. Lunit's partnership with HMG and Cloud Solutions promises to enhance diagnostic capabilities, leading to better patient outcomes. Medlab Middle East's focus on AI underscores its growing importance in healthcare, fostering innovation and efficiency. United Imaging's collaborations introduce advanced imaging technologies, meeting the region's rising healthcare demands. These advancements are poised to drive Middle East Medical Imaging Market growth by improving healthcare accessibility, efficiency, and accuracy, ultimately benefiting patients and healthcare providers across the Middle East.

On July 26, 2023, Lunit expanded its presence in the Middle East by partnering with Dr. Sulaiman Al Habib Medical Group (HMG), the largest healthcare provider in the region. This collaboration involves supplying Lunit INSIGHT MMG, an AI solution for mammography analysis, to HMG for three years. HMG plans to integrate the solution into medical institutions across the Middle East, processing numerous mammography images annually. Additionally, Lunit and HMG's subsidiary, Cloud Solutions, will collaborate to enhance Lunit's AI-powered solutions using Cloud Solution's advanced cloud AI platform, aiming to offer an improved healthcare experience.

On December 27, 2023, Medlab Middle East convened experts to explore AI's transformative impact on laboratories and healthcare. AI accelerates diagnostics and decision-making, revolutionizing healthcare systems worldwide. In the UAE, AI-based medical imaging is gaining momentum, supported by government initiatives. Saudi Arabia introduced AI-powered eye screening tests, enhancing diabetic retinopathy diagnosis.

On February 14, 2023, United Imaging formed key partnerships at Arab Health 2023. Collaborating with I-ONE Nuclear Medicine & Oncology Center, they introduced the first PET/MR uPMR 790 in the Gulf countries, focusing on advanced PET/MR imaging. Additionally, agreements were signed with My Doctor Medical Center in Qatar for advanced imaging solutions and Health Garden Clinic in Morocco for the installation of the first uMR680 MRI system. United Imaging also expanded cooperation with top medical suppliers in Saudi Arabia and Kazakhstan to boost its presence in the Middle East and Central Asia.

Global Middle East Medical Imaging Market Scope: Inquire before buying

| Global Middle East Medical Imaging Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 1.76 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 3.46% | Market Size in 2030: | US $ 2.23 Bn. |

| Segments Covered: | by Procedure | Computed Tomography (CT) Scan X-Ray Imaging Magnetic Resonance Imaging (MRI) Ultrasound, Nuclear Imaging (SPECT/PET) Others |

|

| by Technology | Direct Digital Radiology Computed Radiology |

||

| by Equipment Size | Bulky-Stationary-cart wheel Handheld or Portable |

||

| by Application | Cardiology Pelvic And Abdominal Oncology Mammography Gynecology Neurology Urology Musculoskeletal Dental Others |

||

| by End Users | Hospitals Diagnostic Centers Imaging Centers Specialty Clinics Ambulatory Surgical Centers Academic and Research Institutes Others |

||

Middle East Medical Imaging Market Key Players:

1. Diagnostic Imaging Equipment Manufacturers

These companies develop and supply X-ray, CT, MRI, ultrasound, and other diagnostic imaging systems used in hospitals and diagnostic centers.

North America

1. GE HealthCare Technologies Inc. – United States

2. Hologic, Inc. – United States

Europe

1. Siemens Healthineers AG – Germany

2. Philips Healthcare – Netherlands

Asia Pacific

1. Canon Medical Systems Corporation – Japan

2. Fujifilm Healthcare Corporation – Japan

3. Samsung Medison Co., Ltd. – South Korea

Middle East

1. Gulf Medical Co. Ltd. – Saudi Arabia

2. Advanced Electronics Company (AEC) – Saudi Arabia

2. MRI & CT Imaging Solution Providers

These companies provide advanced MRI and CT technologies for neurological, cardiovascular, oncology, and general diagnostic applications.

North America

1. GE HealthCare Technologies Inc. – United States

Europe

1. Siemens Healthineers AG – Germany

2. Philips Healthcare – Netherlands

Asia Pacific

1. Canon Medical Systems Corporation – Japan

2. Fujifilm Healthcare Corporation – Japan

Middle East

1. Gulf Medical Co. Ltd. – Saudi Arabia

3. Ultrasound & Women's Health Imaging Companies

These companies develop ultrasound systems and specialized imaging solutions for obstetrics, gynecology, cardiology, and general imaging.

North America

1. GE HealthCare Technologies Inc. – United States

2. Hologic, Inc. – United States

Europe

1. Philips Healthcare – Netherlands

Asia Pacific

1. Samsung Medison Co., Ltd. – South Korea

2. Canon Medical Systems Corporation – Japan

Middle East

1. Al Faisaliah Medical Systems – Saudi Arabia

4. Nuclear Imaging & Molecular Imaging Companies

These companies provide PET, SPECT, and molecular imaging systems used in oncology, cardiology, and neurology diagnostics.

North America

1. GE HealthCare Technologies Inc. – United States

Europe

1. Siemens Healthineers AG – Germany

Asia Pacific

1. Canon Medical Systems Corporation – Japan

Middle East

1. King Faisal Specialist Hospital & Research Centre – Saudi Arabia

5. Medical Imaging Informatics & Enterprise Imaging Providers

These companies provide PACS, RIS, AI-powered imaging software, and enterprise imaging management solutions.

North America

1. GE HealthCare Technologies Inc. – United States

Europe

1. Siemens Healthineers AG – Germany

2. Philips Healthcare – Netherlands

Asia Pacific

1. Fujifilm Healthcare Corporation – Japan

Middle East

1. InterSystems Middle East – United Arab Emirates

2. Malaffi Health Information Exchange – United Arab Emirates

FAQs:

1. What are the growth drivers for the Middle East Medical Imaging Market?

Ans. AI-Powered Medical Imaging Solutions Driving Market Growth and expected to be the major driver for the Middle East Medical Imaging Market.

2. What is the major Opportunity for the Middle East Medical Imaging Market growth?

Ans. Private Healthcare Sector Driving Investments in Advanced Imaging Technologies are the major opportunity for the Middle East Medical Imaging market.

3. Which country is expected to lead the Middle East Medical Imaging Market during the forecast period?

Ans. Gulf Cooperation Council (GCC) is expected to lead the Middle East Medical Imaging Market during the forecast period.

4. What is the projected market size and growth rate of the Middle East Medical Imaging Market?

Ans. The Middle East Medical Imaging Market size was valued at USD 1.76 Billion in 2023 and the total Middle East Medical Imaging Market revenue is expected to grow at a CAGR of 3.46% from 2023 to 2030, reaching nearly USD 2.23 Billion.

5. What segments are covered in the Middle East Medical Imaging Market report?

Ans. The segments covered in the Middle East Medical Imaging Market report are by Procedure, Technology, Equipment Size, Application, End Users, and Region.