Live Cell Encapsulation Market by Polymer Type, Method, Application, Manufacturing Technique, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2029

Overview

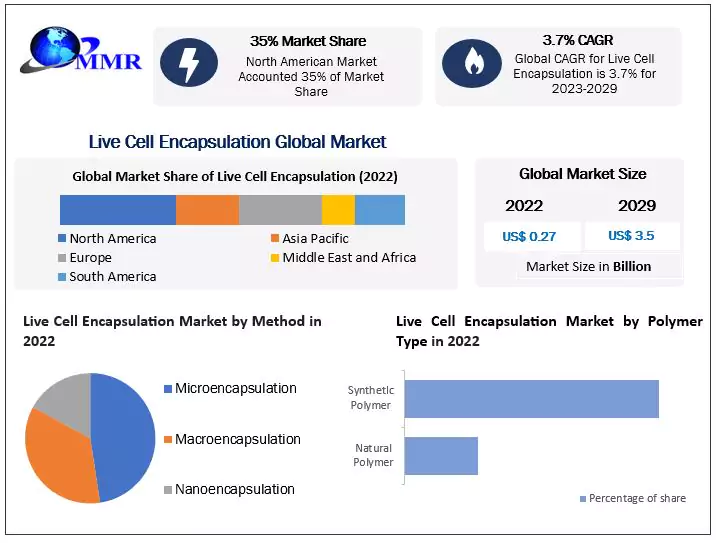

Live Cell Encapsulation Market is worth USD 0.27 Billion and is estimated to grow at a CAGR of 3.7% in the forecasted period. The forecasted revenue hints at a growth of around 0.35 billion USD by 2029.

Live Cell Encapsulation Market is a small but has shown signs of its progression because of researchers and biotechnologists who have opened new opportunities for the Live cell encapsulation market. Live Cell encapsulation is a technique that traps living cells within membranes or beads that are selectively permeable to certain polymeric compounds, making them a potential tool for treating a variety of human diseases. Live cell encapsulation market has applications in various fields like regenerative medicine, tissue engineering, drug delivery, biotechnology, prolonged cell survival, enhanced therapeutic efficacy, targeted delivery, and immune response. These various applications have brought in huge investments and interest in the Live cell encapsulation market which has resulted in a CAGR of 3.7%. North America leads the market and has a share of over 35% in Live cell encapsulation market. Asia Pacific is rising high and is expecting a CAGR of 8.5%.

To know about the Research Methodology :- Request Free Sample Report

Market Drivers in Live Cell Encapsulation Market

The capabilities and applications of live cell encapsulation market have been significantly broadened by significant breakthroughs in encapsulation technologies. The effectiveness and compatibility of Live cell encapsulation market have been increased through advances in materials science, biocompatible polymers, and microfabrication processes, enabling improved cell viability and function. Regenerative medicine and cell-based therapies are in more demand due to diseases like diabetes, cardiovascular problems, and neurological diseases. A method for delivering therapeutic cells, shielding them from immunological rejection, and enhancing their survival and usefulness is live cell encapsulation. Encapsulating live cells have the potential to help cell-based therapeutics overcome obstacles including immunogenicity and immunorejection. A physical barrier is also present between the transplanted cells and the host immune system which is created by encapsulating live cells. The government and other large corporations have been investing in Live cell encapsulation market and providing both financial and technical support. For instance, Johnson & Johnson invested $100 million in Cell Medica, a business that is creating cancer medicines via live cell encapsulation. A firm called Humacyte, which is creating live cell encapsulation therapy for cardiovascular illness, received $50 million from Novartis. GSK made a $30 million investment in CellSeed, a firm that is working on live cell encapsulation therapy for diabetes.

Challenges in Live Cell Encapsulation Market

Live cell encapsulation market technologies can be costly, which can limit their widespread adoption. The development and production of encapsulation materials, manufacturing processes, and quality control measures can contribute to the overall cost of encapsulated cell therapies. Overcoming cost barriers and improving cost-effectiveness through advancements in manufacturing techniques, materials, and process optimization is a significant challenge in Live cell encapsulation market. Also maintaining the same level of consistency of encapsulation quality, maintaining cell viability, and achieving high production volumes are critical factors that need to be addressed in order to gain a larger share in Live encapsulation market. One of the biggest IP challenges is the fact that the technology is still in its early stages of development. This means that there is a lot of uncertainty about what is patentable and what is not, in Live cell encapsulation market. As a result, companies need to be careful about disclosing their IP to others, as they may inadvertently give away their competitive advantage. Another IP challenge is the fact that there are a number of different technologies that can be used in live cell encapsulation industry. This means that companies need to be careful about infringing on the IP of other companies. As a result, it is important to conduct a thorough IP search before developing or commercializing a live cell encapsulation product. Also, the IP landscape for live cell encapsulation market is constantly changing. This is due to the fact that new technologies are being developed all the time. As a result, companies need to stay up-to-date on the latest IP development to sustain in live cell encapsulation market.

Live Cell Encapsulation Market Trend

Researchers are developing new materials that can be more biocompatible and allow for better cell growth and function. These new materials could lead to the development of more effective and safer cell-based therapies.

New methods for cell encapsulation are been developed that can make new cell encapsulation more efficient and scalable. These new methods could lead to the production of cell-based therapies at a lower cost. With each new technology, each application is widening the field, such as use of encapsulated cells to deliver drugs or to regenerate tissues. Researchers are exploring the use of encapsulated cells for biosensing, bioelectronics, biocatalysis, and other biotechnological applications. This expansion of the application scope of live cell encapsulation broadens its potential impact and opens up new avenues for innovation and commercialization. Increasing awareness has helped the Live cell encapsulation market

Increasing Adoption of 3D Cell Culture Techniques, including scaffold-based and scaffold-free systems, are gaining popularity in the live cell encapsulation market. These techniques better mimic the physiological environment and cell-cell interactions, leading to improved cell viability, functionality, and relevance in drug discovery, tissue engineering, and regenerative medicine applications. These adoptions have also gained huge interest in drug delivery processes and also helped the live cell encapsulation market grow.

Encapsulation systems are being designed to incorporate bioactive molecules, such as growth factors, cytokines, and small molecules, to regulate cell behaviour, differentiation, and tissue regeneration. These molecules can be released in a controlled manner from the encapsulation matrix to enhance therapeutic outcomes and improve tissue engineering applications. Thus, these bioactive molecules also help regulate host cell migration, proliferation, and differentiation and allow cells to interact via specific receptors.

Live Cell Encapsulation Market Segmentation

Live Cell Encapsulation Market Segmentation by Polymer type

Natural polymer and Synthetic Polymer are two types of polymers in Live cell encapsulation market. Syntenic polymer nearly controls 80% of the polymer segment leaving only 20% for natural polymer. Synthetic polymer has good flexibility, strength and resistivity and thus is preferred over natural polymers. Synthetic polymers may overcome the problems related to purification, immunogenicity, and pathogen transmission of some natural polymers and may also provide a greater reproducibility and control over the material properties.

Live Cell Encapsulation Market Segmentation by Method

Microencapsulation, Microencapsulation & Nanoencapsulation are the three methods in live cell encapsulation market. Microencapsulation holds the highest market share and dominates on more than half of this segment. The reason for using microencapsulation is that the core material is completely coated and isolated from external environment. More importantly, microencapsulation would not affect the properties of core materials which acts as a huge positive in live cell encapsulation industry. Macroencapsulation enjoys a lesser share and with upcoming new technologies like nanoencapsulation, the market share is further declining.

Live Cell Encapsulation Market Segmentation by Application

Drug Delivery holds the highest share in the application segment of live cell encapsulation market. It nearly holds around 45% of the market and leads the industry as demand for cell-based therapies for the treatment of a variety of diseases, such as cancer, diabetes, and heart disease are increasing offering more opportunities in the field. Regenerative Medicine is also an important application as treatment of spinal cord injuries, heart injuries are readily using regenerative medicines. Cell transplantation is a risky segment and thus have lesser share than regenerative medicine.

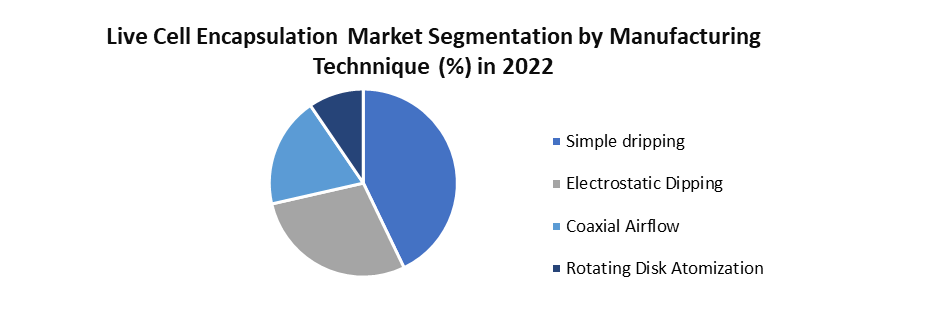

Live Cell Encapsulation Market Segmentation by Manufacturing technique

Live Cell Encapsulation Market Segmentation by Manufacturing technique

Simple dripping holds the highest market as it is easy and simplifies the process to a large extent. This industry nearly holds half of the segment in live cell encapsulation market. The polymer forms a barrier around the cells, protecting them from the immune system. The electrostatic dipping is also a favourable technique as its more advanced method that uses an electric field to attract cells to a surface. Coaxial airflow holds a lower percent of market and is a relatively newer in Live cell encapsulation. A rotating disk atomization manufacturing technique is the most advanced method for encapsulating cells. It involves rotating a disk that is coated with a polymer

Live Cell Encapsulation Market Segmentation by Region

Live Cell Encapsulation Market Segmentation by Region

Global

The creation of high-performance capsules, improvements in molecular technology, and the growth of the biopharmaceutical sector in emerging economies are all factors that have an impact on the market. Thus, the global economy of the Live Cell Encapsulation has started rising steadily. Asia Pacific recorded the highest CAGR amongst the 5 regions. North America emerged as market leader with nearly 35% of the total Live Cell Encapsulation market. The market has huge scope in global market due to its increasing applications and thus many companies are willing to place a bet on live cell encapsulation market.

North America

North America leads the Live Cell Encapsulation market and occupies around 35% of the total Live cell encapsulation market. US leads the way with highest market share amongst the other countries.US big players have contributed thoroughly in this market growth. BioTime, Viacyte are some of the companies with highest contributions. Also, high investments in research and analysis have already increased growth potential of the industry.

Asia Pacific

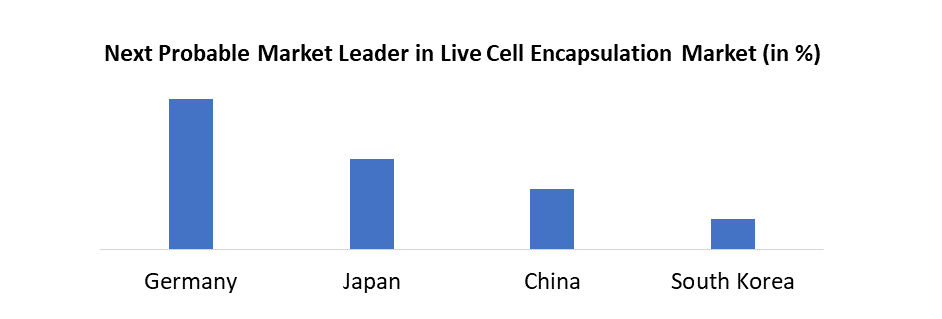

Asia Pacific is currently having a decent share of the market and is forecasted to grow at a rapid rate which is because of increased population, higher demand and well-developed technology. The increased healthcare sector has directly improved the investments and also the internal structure of the pharma and healthcare market has developed in last few years. Countries such as China, Japan, South Korea, India, and Singapore are key contributors to the market. China leads the market and is one of the largest markets in the world for Live cell encapsulation market.

Europe

Europe has a significant market share in Live Cell Encapsulation industry and falls just behind North America. The region has a well-established pharmaceutical and biotechnology industry, stringent regulatory frameworks, and a strong emphasis on product quality and safety. Germany leads the manufacturing capabilities, while UK and France have well developed healthcare infrastructure. Europe offers a favourable market environment for gene therapy and live cell encapsulation and thus attract foreign investments into its research

Middle East and Africa

The Middle East is an emerging sector with many opportunities and risk. Saudi Arabia, UAE, Qatar have made significant investments to build a sustainable place for biotechnology and research. In Saudi Arabia, the government's Vision 2030 plan aims to diversify the economy and develop the healthcare sector. Other regions of UAE like Dubai, Qatar have also started making healthcare and biotechnology hub, attracting international pharmaceutical companies and research organizations.

South America

South America expresses a steady market share and is mainly constricted to bigger countries like Brazil, Argentina. Argentina has focused on innovation, research and development, and quality manufacturing process and ensured that they expand their Live Cell Encapsulation market share. Columbia has been investing in healthcare from past decade, which gives it an opportunity to have similar market share as of that of Brazil and Argentina. Other countries like Peru, Chile are also slowly making footsteps in Live cell encapsulation market.

Live Cell Encapsulation Market: Competitive Landscape

The market is very constricted and is focused on future and its futuristic applications. US holds a dominant share of the live cell encapsulation market and companies like Blackstone Labs and Mikrocops which have a suitable influence on the live cell encapsulation market. Investments from Sernova Corp, Viacyte have made sure that the market flourishes. Acquisitions have made the market open and entry of new entrants have increased significantly. Example - Viacyte acquired Semma Therapeutics, Langer Biotechnologies acquired Althea Technologies. Also, collaborations and partnerships have helped the live cell encapsulation market grow and new recent findings are the result of the same. In 2022, Sernova Corp. and Just Biotherapeutics announced a collaboration to develop a live cell encapsulation therapy for the treatment of diabetes. But the market is still in its early stages and has humongous potential to be one of the leading markets in biotechnology in future.

Live Cell Encapsulation Market Scope: Inquire before buying

| Live Cell Encapsulation Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2017 to 2022 | Market Size in 2022: | US $ 0.27 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 3.7% | Market Size in 2029: | US $ 0.35 Bn. |

| Segments Covered: | by Method | • Microencapsulation • Macroencapsulation • Nanoencapsulation |

|

| by Type | • Drug Delivery • Regenerative Medicine • Cell Transplantation |

||

| by Manufacturing Technique | • Simple dripping • Electrostatic dripping • Coaxial airflow • Rotating disk atomization |

||

| by Polymer Type | • Natural polymer • Synthetic Polymer |

||

Live Cell Encapsulation Market: Key Players

The players mentioned are top companies working in the Live Cell Encapsulation Market. All these companies have shown tremendous market strategy and have showed huge potential to maximize the Live cell encapsulation market.

• Austrianova (United States)

• Sernova Corp. (Canada)

• Thermo Fisher Scientific Inc. (United States)

• Balchem Corporation (United States)

• Blackstone Labs (United States)

• mikrocops (United States)

• Xencor, Inc. (United States)

• Organovo Holdings, Inc. (United States)

• Encaptra Cell Delivery Solutions (United States)

• TissueGen Inc. (United States)

• Prellis Biologics (United States)

• Danaher Corporation (United States)

• Corning Incorporated (United States)

• Becton, Dickinson and Company (United States)

• 3D Biotek, LLC (United States)

• Cellencor (United States)

• ReNeuron Group plc (United Kingdom)

• CellCoTec (Netherlands)

• Lonza Group Ltd. (Switzerland)

• Evonik Industries AG (Germany)

• Merck KGaA (Germany)

• CELLINK AB (Sweden)

• Living Cell Technologies Ltd. (New Zealand)

• OrbusNeich Medical (Hong Kong)

• Nipro Corporation (Japan)

FAQ

Q.1) What is the CAGR of Live Cell Encapsulation market?

Ans: The CAGR for Live Cell Encapsulation market is 3.7%

Q.2) Which are the leading companies in Live Cell Encapsulation market?

Ans: Austrianova and Sernova Corp are some of the leading companies in the Live Cell Encapsulation Market.

Q.3) Which region shows maximum potential in Live Cell Encapsulation Market

Ans: Asia Pacific is expected to grow exponentially and is likely to dominate Live Cell Encapsulation Market in future

Q,4) Which is the leading region in Live Cell Encapsulation market?

Ans: North America leads the market of Live Cell Encapsulation market significantly

Q.5) What was the forecasted period of the Live Cell Encapsulation Market report?

Ans: The forecasted period for the Live Cell Encapsulation market research was 2023 – 2029