Medical Sensors Market Size by Product, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

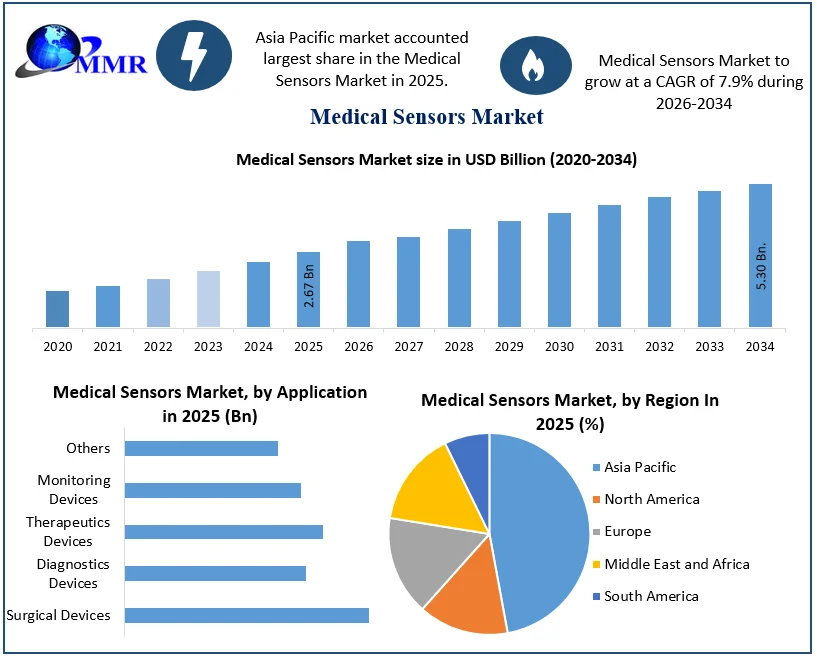

The Medical Sensors Market size was valued at USD 2.67 Billion in 2025 and the total Medical Sensors revenue is expected to grow at a CAGR of 7.9% from 2026 to 2034, reaching nearly USD 5.30 Billion.

Medical Sensors Market Overview

Medical sensors are devices that detect and monitor physiological signals from the human body, such as heart rate, temperature, blood pressure, or glucose levels. These sensors convert biological data into electrical signals for real-time analysis, diagnosis, and monitoring, enabling more accurate and non-invasive healthcare solutions. They are widely used in medical devices, wearables, and diagnostic tools which significantly boosts the Medical Sensors Market .

In April , the Centre cleared the National Medical Devices Policy, targeting the expansion of India's medical devices sector from USD 11 billion in to USD 50 billion by , requiring an annual growth rate of over 15%. The policy has sparked increased global interest and investment in the sector. Foreign direct investment (FDI) in medical devices surged to USD 3.4 million in the first three-quarters of FY23, up from USD 1.9 million in FY22. Notably, Medtronic announced a USD 350 million investment to expand its R&D center in Hyderabad, while Omron Healthcare committed USD 15.5 million to build a manufacturing facility in Tamil Nadu.

Medical Sensors Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

Medical Sensors Market Dynamics

Growing Demand for Technological Devices Fuels Medical Sensor Market Growth

The rapid adoption of technological devices in the medical industry is driving significant growth in the medical sensors market. As healthcare shifts towards more data-driven and patient-centric care, advanced medical sensors have become essential in providing real-time, accurate physiological data. Devices like wearable health monitors, smart implants, diagnostic tools, and remote patient monitoring systems rely heavily on these sensors to track vital parameters such as heart rate, body temperature, blood pressure, oxygen levels, and glucose concentration. This growing demand for medical sensors is closely tied to advancements in telemedicine, the Internet of Things (IoT), and AI-based healthcare solutions. With an increasing focus on remote healthcare delivery and personalized medicine, healthcare providers are utilizing connected medical devices that enable continuous patient monitoring, even outside clinical settings. Medical sensors play a pivotal role in making these devices functional, efficient, and reliable, thus directly impacting the quality of patient care.

Additionally, the rise in chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions, along with the global aging population, has heightened the need for constant health monitoring. Patients with chronic conditions require ongoing assessments, which are now more efficiently done through wearable devices equipped with cutting-edge sensors. These technologies allow for early diagnosis, timely intervention, and improved outcomes, further boosting the demand for sophisticated sensors in the medical sector. The healthcare industry’s increasing emphasis on automation, minimally invasive treatments, and real-time patient data management has also accelerated the integration of medical sensors into next-generation medical devices. For instance, smart surgical tools and robotic surgery systems now rely on sensors for precise navigation and enhanced control, further showcasing the critical role of sensor technology in improving medical outcomes.

In , a survey revealed that Singapore led all surveyed countries in the adoption of predictive analytics within healthcare organizations, with a reported adoption rate of 92%. Predictive analytics in healthcare involves using data, statistical algorithms, and machine learning techniques to identify the likelihood of future outcomes based on historical data. This can help in various ways, such as predicting patient outcomes, streamlining operations, and personalizing patient care. China was the second highest, showing a significant adoption rate of 79% in the for medical sensors Market. Following China, both Brazil and the United States reported an adoption rate of 66%. This illustrates a growing global trend towards leveraging advanced data analytics to improve healthcare efficiency and patient outcomes.

Growing Adoption of Software as a Medical Device (SaMD) for Enhanced Healthcare Systems

A significant trend in the medical sensors market is the rise of Software as a Medical Device (SaMD) solutions aimed at transforming healthcare systems. Innovations such as digital medications and sensor-enabled pills are gaining traction, allowing patients to administer treatments more safely and efficiently, ultimately improving health outcomes. Sensor-embedded pills, for example, provide real-time data on medication adherence and effectiveness, facilitating more personalized care. As the demand for cost-effective outpatient treatments increases, the adoption of such digital solutions is expected to grow, driving the need for advanced medical sensors.

These sensors enable the monitoring of medication impact, missed doses, and overall patient health data. Additionally, advancements in sensor technology are broadening their application across various medical devices, including surgery-specific sensors, diabetes management tools, orthopedic care devices, and wearable tech like smartwatches for heart rate and sleep apnea monitoring. This trend is set to enhance the role of medical sensors in improving the accuracy and functionality of medical equipment, leading to greater demand in the healthcare sector.

Medical Sensors Market Segment Analysis

Based on Product, in the medical sensors market, products are segmented by the types of sensors utilized in healthcare applications. In the medical sensors market, biosensors are currently the dominant segment. This is primarily due to their versatility and critical role in a wide range of diagnostic and therapeutic applications. Biosensors are integral to glucose monitoring, disease diagnostics, and various point-of-care testing solutions, making them highly sought after in the healthcare industry. Their ability to provide real-time, accurate data on biological processes drives their widespread adoption and market dominance. Pressure sensors are widely used for monitoring blood pressure, respiratory systems, and fluid levels in medical devices.

Temperature sensors play a crucial role in monitoring patient body temperature and are integrated into various wearable and diagnostic devices. Image sensors are used in medical imaging technologies such as X-rays, MRIs, and endoscopies to capture high-resolution visuals for diagnostics. Accelerometers are commonly found in devices that monitor patient movement and activity, essential for rehabilitation and physical therapy applications. Biosensors are highly versatile and used to detect biological elements, often in glucose monitors, cholesterol testing, and disease diagnostics. Flow sensors help in controlling and monitoring fluid dynamics in devices such as ventilators and infusion pumps. Squid sensors (Superconducting Quantum Interference Devices) offer extremely sensitive magnetic field detection, used in advanced medical diagnostics such as MRI systems. Other sensors also contribute to the medical field, providing various capabilities that enhance diagnostic and therapeutic outcomes in the for medical sensors Market.

Based on Application, medical sensors are utilized across several applications in healthcare. In terms of application, monitoring devices hold the dominant position in the for medical sensors Market. The demand for continuous monitoring of vital signs, such as heart rate, blood pressure, and oxygen levels, is growing rapidly due to the increasing prevalence of chronic diseases and the need for remote patient management. Monitoring devices are crucial in various settings, including hospitals, home care, and wearable health technologies, driving their dominance in the market. Surgical devices rely on sensors to ensure precision and safety during procedures, assisting in minimally invasive surgeries and robotic-assisted surgeries.

Diagnostic devices use sensors to detect and analyze physiological data, such as heart rate, blood glucose levels, and organ imaging, to aid in accurate diagnoses. Therapeutic devices incorporate sensors to deliver targeted treatments, such as in drug delivery systems, physiotherapy tools, and wearable devices for managing chronic conditions. Monitoring devices continuously track vital signs like heart rate, oxygen levels, and blood pressure, making them essential in intensive care units, wearable health monitors, and telemedicine applications. Other areas also benefit from sensor integration, offering more advanced and patient-centric healthcare solutions in the for medical sensors Market.

Medical Sensors Market Regional Analysis

The Asia Pacific region is expected to experience the highest growth rate in the medical sensors market during the forecast period. This region includes countries like China, India, Australia, New Zealand, and other Southeast Asian nations. Market players are actively expanding their presence in these emerging economies, where the increasing awareness of advanced medical systems is expected to drive for medical sensors market growth.

China accounted for the largest share of the global medical sensors market in 2025, and this trend is likely to continue. Factors contributing to China's growth include a growing elderly population, government support for healthcare services, and rising discretionary income. Meanwhile, India's medical sensors industry is being driven by the demand for diagnostic imaging and patient monitoring devices. The country's need for advanced, connected devices is growing, especially for patient monitoring, as it helps reduce hospital expenses. The adoption of remote monitoring systems is also increasing, contributing to the rising demand for medical sensors across the region.

The steady growth of the medical Sensors market in the Asia-Pacific region from. In 2025, the market generated about 96.4 billion U.S. dollars, with cardiology devices contributing the largest share of over 13.5 billion dollars. Other prominent segments include diagnostic imaging devices, orthopedic devices, and general and plastic surgery devices, with significant contributions from diabetes care and dental devices. This surge in demand for medical devices is closely linked to advancements in healthcare infrastructure and the increasing adoption of diagnostic imaging and patient monitoring technologies. This, in turn, is driving the growth of the medical sensors market in the region. The rising demand for connected medical devices, particularly in areas such as cardiology and diagnostic imaging, necessitates the use of advanced sensors for monitoring, diagnosis, and treatment. Moreover, the growing elderly population, along with increased healthcare expenditure, further propels the adoption of medical sensors for remote patient monitoring, diagnostic tools, and other healthcare services across the Asia-Pacific region. This upward trend in the medical devices market creates a favorable environment for the continued development of the medical sensors market.

Medical Sensors Market Competitive Landscape

In August 2023, NXP Medical Sensors (Netherlands), Taiwan Medical Sensors Manufacturing Company (Taiwan), Robert Bosch GmbH (Germany), and Infineon Technologies AG (Germany) invested in European Medical Sensors manufacturing Company (ESMC) GmbH. This collaboration focuses on building a 300mm Medical Sensors fabrication plant that will support the automotive and industrial sectors. This move positions these companies as dominant players in the Medical Sensors manufacturing field, increasing their competitive edge in sensor technologies that rely on advanced Medical Sensors components. The introduction of FinFET transistor technology and high production capacity (40,000 wafers) enhances their ability to serve the rapidly boosting demand for Medical Sensors in high-demand sectors, which will increase competitive pressure on other sensor manufacturers.

In July 2023, Tekscan, Inc. (US) announced partnerships with DigiKey (US) and Mouser Electronics (US) to increase the availability of its FlexiForce sensors in the electronics marketplace. This partnership directly impacts competition by enhancing Tekscan’s distribution network and product visibility, allowing the company to tap into a larger market of electronics and sensor buyers. By expanding their reach, Tekscan directly compete with companies offering similar force and pressure sensors, making the medical sensors market more competitive for smaller players and new entrants.

In March 2023, Sensirion AG (Switzerland) joined the ST Partner Program by STMicroelectronics, integrating its humidity and temperature sensors into ST’s product portfolio. This partnership allows Sensirion to leverage STMicroelectronics’ global distribution channels, thereby expanding its market reach and gaining access to a wider customer base. The partnership enhances both companies' competitiveness by combining Sensirion’s sensor technology with ST’s established market presence, creating a stronger offering in the medical sensors markets. This collaboration presents a challenge for rivals who may not have such strategic alliances or the ability to offer comprehensive solutions to end-users.

Medical Sensors Market Recent Development

| Date | Company | Development | Impact |

|---|---|---|---|

| 21 August 2025 | Abbott | Abbott officially launched its next-generation FreeStyle Libre 2 Plus continuous glucose monitoring sensor in India to provide real-time blood glucose data directly to smartphones. | This expansion enhances accessibility to advanced wearable biosensors in high-prevalence regions, driving patient self-management and mitigating severe glycemic risks. |

| 02 September 2025 | Medtronic | The U.S. FDA cleared Medtronic's MiniMed 780G system to integrate with the partner-developed Instinct sensor and approved its clinical use for Type 2 diabetes patients. | This regulatory milestone widens the total addressable consumer base for automated sensor-driven medical systems into a major new therapeutic segment. |

| 02 December 2025 | Medtronic | Medtronic initiated the full commercial rollout of its updated MiniMed 780G system embedded with the high-precision Instinct sensor across the United States. | The launch introduces cross-vendor hardware flexibility, expanding market commercialization and options in the continuous patient monitoring sector. |

| 12 January 2026 | Medtronic | Medtronic Diabetes secured U.S. FDA clearance for the MiniMed Go Smart MDI system, which seamlessly pairs with Abbott's Instinct sensor to centralize dosing and tracking data. | The approval delivers an integrated tracking architecture that boosts clinical utility and modernizes remote data integration for multiple daily injection (MDI) therapy. |

| 25 February 2026 | Medtronic | Medtronic launched the regional commercial rollout of its MiniMed Go Smart MDI system featuring the Simplera sensor across the EMEA geography. | This geographical expansion scales up the deployment of smart wearable diagnostic infrastructure and broadens international patient access to digital therapeutics. |

Medical Sensors Market Scope: Inquire before buying

| Medical Sensors Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 2.67 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 7.9% | Market Size in 2034: | USD 5.30 Bn. |

| Segments Covered: | by Product | Pressure Sensor Temperature Sensor Image Sensor Accelerometer Biosensor Flow Sensor Squid Sensor Others |

|

| by Application | Surgical Devices Diagnostics Devices Therapeutics Devices Monitoring Devices Others |

||

Medical Sensors Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Medical Sensors Key Players

North America

1. Honeywell International Inc.(Charlotte, North Carolina, USA)

2. General Electric Healthcare (Chicago, Illinois, USA)

3. Texas Instruments Incorporated (Dallas, Texas, USA)

4. Medtronic PLC (Dublin, Ireland; operational headquarters in Minneapolis, Minnesota, USA)

5. Amphenol Advanced Sensors (Wallingford, Connecticut, USA)

Europe

6. Siemens Healthineers (Erlangen, Germany)

7. STMicroelectronics (Geneva, Switzerland)

8. Sensirion AG (Stäfa, Switzerland)

9. NXP Semiconductors (Eindhoven, Netherlands)

10. TE Connectivity (Schaffhausen, Switzerland)

Asia Pacific

11. Omron Corporation (Kyoto, Japan)

12. Panasonic Corporation (Osaka, Japan)

13. Sensata Technologies (Attleboro, Massachusetts, USA; significant operations in Asia)

14. Fuji Electric Co., Ltd. (Tokyo, Japan)

15. AMS AG (Premstaetten, Austria; strong presence in the Asia-Pacific region)

Middle East & Africa

16. Bosch Sensortec GmbH (Reutlingen, Germany; presence in the Middle East and Africa)

17. Masimo Corporation (Irvine, California, USA; active presence in the Middle East)

18. Althen Sensors & Controls (Heerlen, Netherlands; Middle East market presence)

South America

19. Smiths Group PLC (Smiths Medical) (London, UK; South American market focus)

20. Analog Devices, Inc. (Norwood, Massachusetts, USA; operations extending to South America)

21. Others

Frequently Asked Questions:

1. What is the growth rate of the Global Medical Sensors Market?

Ans. The Global Medical Sensors Market is growing at a significant rate of 7.9% during the forecast period.

2. Which region is expected to dominate the Global Medical Sensors Market?

Ans. Asia Pacific is expected to dominate the Medical Sensors Market during the forecast period.

3. Which factors are expected to create opportunities for the Global Medical Sensors Market size by 2034?

Ans. Continuous advancements in Medical Sensors manufacturing techniques, such as the development of new materials, novel deposition methods, and innovative lithography technologies, create opportunities for the Medical Sensors market.

4. Which are the top players in the Global Medical Sensors Market?

Ans. The major top players in the Global Medical Sensors Market are Honeywell International Inc., General Electric Healthcare, Texas Instruments Incorporated, Medtronic PLC (Dublin, Ireland; operational headquarters in Minneapolis, Minnesota, USA), Amphenol Advanced Sensors (Wallingford, Connecticut, USA), and Others.

5. What are the factors driving the Global Medical Sensors Market growth?

Ans. The growing emphasis on renewable energy sources such as solar power is driving the demand for Medical sensors used in solar panel manufacturing. Specialty gases are essential in processes like chemical vapor deposition (CVD) for thin-film deposition in solar cell fabrication.

6. What was the Global Medical Sensors Market size in 2025?

Ans: The Global Medical Sensors Market size was USD 2.67 Billion in 2025.