Hydrogen Valve Market Size by Valve Type, Material, Size, Application, End User, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

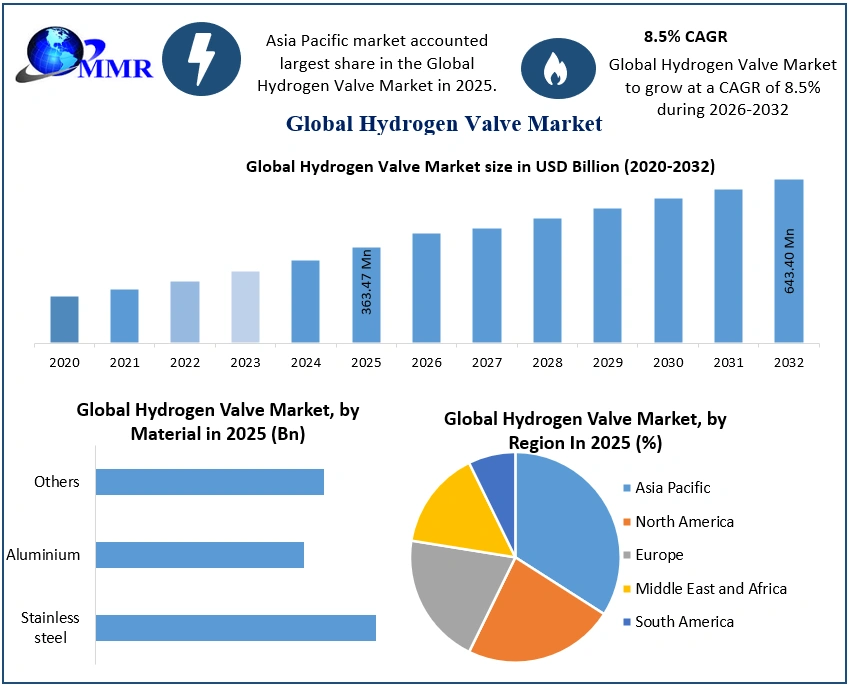

The Hydrogen Valve Market size was valued at USD 363.47 Million in 2025 and the total Hydrogen Valve revenue is expected to grow at a CAGR of 8.5% from 2026 to 2032, reaching nearly USD 643.40 Million by 2032.

Hydrogen Valve Market Overview

A hydrogen valve is a high-performance valve designed to safely control hydrogen gas or liquid hydrogen flow in applications such as fuel space, fueling stations, and aerospace. It must mitigate leaks, withstand extreme pressure, and oppose hydrogen embrittlement. Mainly made from stainless steel, coated brass, or polymers, these valves often feature cryogenic compatibility with liquid hydrogen. They complywith stringent standards like ISO 19880-3 ans SAE J2600 to ensure safety inhydrogen systems.

Global hydrogen valve market is experiencing robust growth, driven by the clean energy transition, government policies like the U.S. Inflation Reduction Act and the EU’s hydrogen strategy, and rising applications in mobility, industry, and power generation. Important growth factors include increasing oil and gas decarbonisation efforts and technological advancements in hydrogen-compatible materials and smart valves. Recent trends highlight surging demand for cryogenic valves for liquid hydrogen in space and transport applications, high-pressure valves that are 700+ bar for fuel vehicles.

Air Liquide's new liquid hydrogen plant in Nevada (2024) uses Emerson's cryogenic valves to handle -253°C hydrogen for space and trucking applications. Asia Pacific dominance is led by China, Japan, and South Korea’s hydrogen infrastructure projects. Hydrogen Valve Market opportunities are expanding in greenhouse hydrogen production, aviation applications, and advanced leak detection technologies. Recent developments impacting the market include U.S. DOE’s $7 Bn hydrogen hub funding, EU Hydrogen bank auctions, and major industry partnerships like Hyundai-Bosch in fuel cells.

Emerson Electric dominates in automated valves for large-scale hydrogen plants, emphasizing smart control sysytems. Sewagelok specializes in precision high-pressure valves for fueling stations and aerospace. Emerson has broader industrial reach, while Swagelok excels in customization and aftermarket support. Both compete in Asia-Pacific’s boosting market, advancing hydrogen-resistant materials and energy partnership.

To know about the Research Methodology :- Request Free Sample Report

Global Hydrogen Valve Market Dynamics

Growing Adoption of Fuel Cell Vehicles (FCVs) to Drive the Market Growth

The increasing need for hydrogen fuel vehicles is the key driver for the hydrogen valve market. Governments all over the world are encouraging fuel cell cars to minimize carbon emissions, resulting in greater production of hydrogen valves for fuel cell systems, storage tanks, and refuelling stations. Toyota Mirai and Hyundai Nexo employ high-pressure hydrogen valves for the safe supply of gas. Global stock of fuel cell vehicles exceeded 72000 units, with South Korea, China, and the U.S. as the leaders in implementation. Such a trend enhances the need for pneumatic and electric hydrogen valves in vehicle use.

Expansion of Hydrogen Refueling Infrastructure to Drive the Hydrogen Valve Market Growth

The deployment of hydrogen fueling stations is gaining momentum, particularly in Europe, North America, and Asia, necessitating the need for dedicated hydrogen valves. The valves facilitate hydrogen compression, storage, and dispensing. Germany's H2 mobility program plans to install 1000 hydrogen stations by 2032, needing thousands of high-pressure valves per station. Companies such as Nel Hydrogen and Air Liquide depend on automated pneumatic and electric valves to ensure maintenance or control efficiency, and safety in HRS networks.

Rising Industrial Applications in Oil & Gas and Chemicals to Drive the Hydrogen Valve Market Growth

Hydrogen valves find considerable industrial applications in the production of ammonia, petroleum refining, and methanol. Hydrogen valves are used most by the oil and gas industry in hydroprocessing equipment for fuel desulfurization, while hydrogenation operations use them in the chemical industry. High-pressure and corrosive conditions are regulated by high-performance hydrogen valves in Shell's Pernis refinery in the Netherlands. Industrial applications represent more than 40% of the hydrogen valve market, fueled by strict environmental regulations that bring in cleaner refining methods. The hydrogen valve market is controlled by several challenges that will determine its growth and development.

However, one of the major challenges is the cost of production of hydrogen valves because of the requirement of high-technology materials like stainless steels and nickel alloys, which resist hydrogen special properties, particularly its ability to embrittle metals. Embrittlement leads chiefly to valve failure, calling for strict material selection and design practices for reliability and safety. The Hypothetical nature of global standards for hydrogen valves introduces uncertainty and complicates manufacturing production, since companies must address differences in regional needs and conditions. Another significant aspect is safety concerns; hydrogen's high flammability and sensitivity to leakage in case of slight defects necessitate sophisticated sealing technologies and heavy engineering.

Expansion of Hydrogen Refueling Infrastructure and Green Hydrogen Integration Creates lucrative opportunity for Hydrogen Valve Market Market Growth

Its maximum future value is coupled with the production of green hydrogen, which is initiated by the global renewable energy transition and decarbonization. Green hydrogen from electrolysis by wind, solar, or hydro power necessitates high-technology and reliable valve systems to possess the ability to handle high-pressure gas streams, prevent leakage, and provide protection for production, storage, and transportation. As governments and industry bet on green hydrogen projects such as the European Union's REPowerEU plan of 10 million tonnes of local green hydrogen production by 2032, there will be greater demand for high-performance hydrogen valves.

Saudi Arabia's NEOM Green hydrogen project targets 1.2 million tonnes/year, while the Australian Asian Renewable Energy Hub depends on high-performance valves to employ hydrogen in electrolyzers, compressors, and pipe networks.

| Rise of Smart Valves | IoT-enabled hydrogen valves with real-time monitoring and predictive maintenance are gaining traction. | ||

| Material Innovations | Increased use of Inconel 718 & duplex stainless steel to combat hydrogen embrittlement. | ||

| Cryogenic Valve Demand | Growing need for valves in liquid hydrogen (LH2) storage (-253°C) for transport and export. | ||

| Government Subsidies Driving Growth | Policies like the U.S. IRA tax credits and the EU Hydrogen Bank boost valve demand. | ||

| Modular Electrolyzer Valves | Compact, pre-assembled valve systems for containerized electrolyzers (e.g., Siemens Energy’s solutions). | ||

| Hydrogen Refueling Station Boom | Over 1,000 new H2 stations are planned globally by 2025, requiring high-pressure valves. | ||

| Asia-Pacific Dominance | China, Japan, and South Korea account for 60% of hydrogen valve demand due to FCV adoption. | ||

| Leak-Proof Valve Standards | Stricter ISO 19880-3:2023 safety norms for hydrogen valves in refueling infrastructure | ||

| M&A Activity in the Valve Sector | Companies like Baker Hughes and Flowserve are acquiring niche hydrogen valve manufacturers. | ||

| 3D-Printed Valve Components | Additive manufacturing reduces lead times for custom hydrogen valve parts. | ||

Global Hydrogen Valve Market Segment Analysis

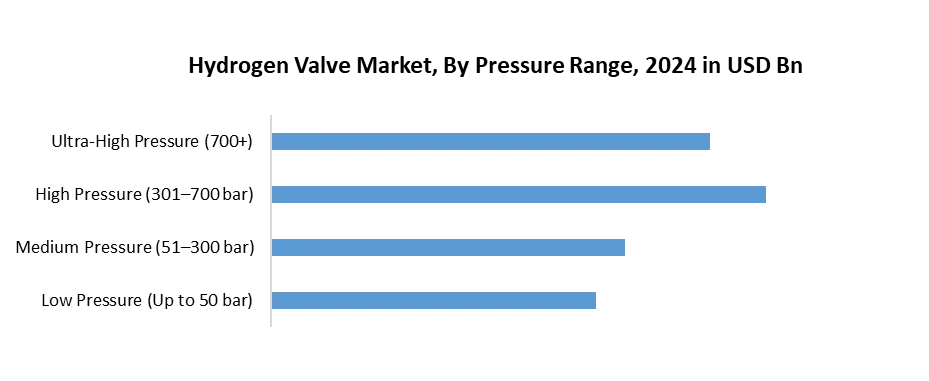

By Pressure Range, the high-pressure segment (301–700 bar) holds the largest market share in the Global Hydrogen Valve Market. According to MMR analysis, the segment is further expected to grow at a CAGR of 8.6 % during the forecast period. This dominance is primarily due to the rapid growth of hydrogen mobility and fueling infrastructure, where storage and dispensing at 350 bar and 700 bar are industry standards. Hydrogen fuel cell vehicles, including cars, buses, and trucks, rely on these pressure ranges to ensure longer driving ranges and efficient fueling times. The demand for high-pressure hydrogen valves has surged, making them the backbone of the hydrogen transportation ecosystem.

The adoption of high-pressure valves is further supported by the global growth of hydrogen refueling stations, which require reliable and durable valve solutions that can withstand extreme pressure levels. Governments in regions such as Europe, North America, and Asia-Pacific are investing heavily in hydrogen mobility as part of clean energy and net-zero emission initiatives. This has accelerated the need for high-pressure systems, directly boosting the market share of valves within this range.

Compared to low- and medium-pressure valves, which are used in industrial, laboratory, and storage applications, high-pressure valves hold greater commercial importance because they are directly tied to end-user applications in transportation and large-scale energy storage. Ultra-high-pressure valves (above 700 bar) remain niche, limited to research, aerospace, and specialized industrial use, and thus contribute only a small portion of the market.

Hydrogen Valve Market Regional Insights

The Asia-Pacific region dominates the global hydrogen valve market, accounting for around 45 to 50% of demand. Driven by government-led hydrogen strategies, rapid industrialization, and rising fuel cell vehicles. China, Japan, and South Korea are the important contributor countries, with China alone projected to invest $20 billion in hydrogen infrastructure by the end of 2025. China’s Sinopac operates the world’s biggest green hydrogen plant in Xinjiang, requiring thousands of high-pressure valves for electrolysis and storage. Japan’s basic hydrogen strategies mandate 800 hydrogen refueling stations by 2032, with companies like Toyota and Kawasaki Heavy Industries driving or motivating demands for FCV-compatible valves. South Korea’s Hyundai NEXO and Doosan Fuel Cell rely on pneumatic and solenoid valves for hydrogen systems.

The Asian Development Bank also funds multiple hydrogen projects, including india’s green hydrogen mission, further boosting or enhancing valve demand. APAC will remain the largest hydrogen valve market because of strong policy support, low electrolyzer costs, and expanding industrial applications.

Hydrogen Valve Market Competitive Landscape

Emerson Electric and Swagelok are two key players shaping the long-duration energy storage markets. Emerson Electric has established itself as a technology leader in hydrogen valves through its Fisher pressure management valves and ASCO solenoid valves, which are deployed in leading projects like Saudi Arabia’s NEOM green hydrogen project. And company’s 30% industrial valve sales now come from hydrogen applications, with a strong focus on IoT-enabled smart valves for electrolyzer monitoring. Emerson holds upto28% market share in electrolyzer valves, supported by a partnership with Siemens Energy and IMT Power. In comparison, Swagelok dominates in precision fluid control, with its 316L stainless steel and Inconel valves being the preferred choice for high-pressure hydrogen refuelling stations. The company’s 40% energy sector revenue comes from hydrogen valves, particularly in oil and gas applications like BP’s blue hydrogen projects. Emerson leads in digital valve solutions.

In comparison, Swagelok dominates in precision fluid control, with its 316L stainless steel and Inconel valves being the preferred choice for high-pressure hydrogen refuelling stations. The company’s 40% energy sector revenue comes from hydrogen valves, particularly in oil and gas applications like BP’s blue hydrogen projects. Emerson leads in digital valve solutions.

Swagelok excels in cryogenic valve technology for liquid hydrogen storage, as seen in NASA’s Kennedy Space Center applications. Emerson’s revenue from hydrogen valves grew by 22% YOY, compared to Swagelok’s 15%, reflecting their differing focus areas. Emerson in large-scale renewable hydrogen and Swagelok in industrial and aerospace applications. Both companies are aggressively extending in Asia-Pacific, with Emerson supplying China’s Sinopec and Swagelok providing valves for Hyundai’s fuel cell production.

Hydrogen Valve Market Scope: Inquire before buying

| Global Hydrogen Valve Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 363.47 Mn. |

| Forecast Period 2026 to 2032 CAGR: | 8.5% | Market Size in 2032: | USD 643.40 Mn. |

| Segments Covered: | by Valve Type | Needle Valves Check Valves Ball Valves Gate Valves Globe Valves Flow Control Others |

|

| by Material | Stainless steel Aluminium Others |

||

| by Size | Up to 1 inches Over 1 to 4 inches Over 4 inches |

||

| by Application | Fuel Cell Vehicles Hydrogen Refueling Stations Energy Storage Systems Power Generation Others |

||

| by End User | Oil & Gas Energy & Power Pharmaceutical Metals & Mining Automotive Others |

||

Hydrogen Valve Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Hydrogen Valve Market, Key Players

1. Emerson Electric Co.

2. Crane Company

3. Parker Hannifin Corp

4. Baker Hughes Company

5. Swagelok Company

6. KITZ Corporation

7. Velan Inc.

8. Westport Fuel Systems Inc.

9. Kevin Steel

10. GSR Ventiltechnik GmbH

11. Adams Armaturen GmbH

12. Hartmann Valves GmbH

13. GEFA Processtecchnik GmbH

14. Maximator GmbH

15. HABONIM

16. OMB Saleri S.P.A.

17. CAM S.p.A.

18. Oliver Valves Ltd

19. Rotarex

20. Valmet

21. Vexve Oy

22. Schrader Pacific

23. Furui Va

24. Shanghai Hanqing Hydropower S&T

25. Baitu Cryogenic Valve

26. Jiangsu Shentong

27. Zhejiang Hongsheng Mobile Parts

28. Flowserve Corporation

29. Honeywell International Inc.

30. CIRCOR International, Inc.

Frequently Asked Questions:

1. Which region has the largest share in the Global Hydrogen Valve Market?

Ans: The Asia Pacific region held the highest share in 2025.

2. What is the growth rate of the Global Hydrogen Valve Market?

Ans: The Global Market is expected to grow at a CAGR of 8.5% during the forecast period 2026-2032.

3. What is the scope of the Global Hydrogen Valve Market report?

Ans: The Global Hydrogen Valve Market report helps with the PESTEL, Porter's, Recommendations for Investors and leaders, and market estimation for the forecast period.

4. Who are the key players in the Global Hydrogen Valve Market?

Ans: The important key players in the Global Hydrogen Valve Market are Emerson Electric, Swagelok, Parker Hannifin, KITZ Corporation, KSB Group, WEH GmbH, GF Piping Systems, Baker Hughes, Neles (Valmet), and GEMÜ Group.

5. What is the study period of this market?

Ans: The Global Hydrogen Valve Market is studied from 2025 to 2032.