Hydrogen Market by Type, Production Process, Technology, Application and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

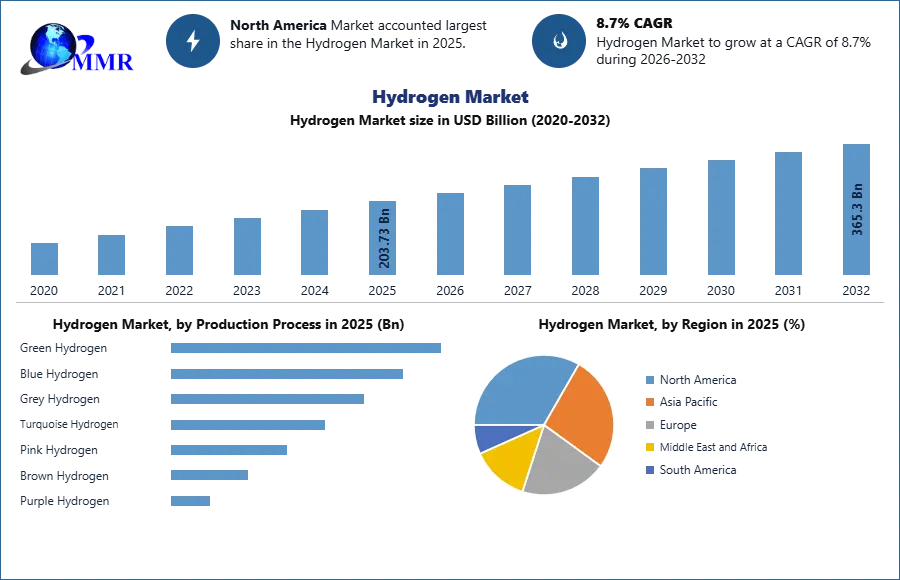

The Hydrogen Market size was valued at USD 203.73 Billion in 2025 and the total Hydrogen revenue is expected to grow at a CAGR of 8.7% from 2026 to 2032, reaching nearly USD 365.30 Billion.

Hydrogen is a lightweight chemical element. It exists in various forms but is most commonly found as a gas. As an energy carrier, hydrogen has significant attention for its potential in various industries, particularly as a clean and sustainable fuel source. Hydrogen in leading in decarbonizing sectors such as transportation, power generation, and industrial processes due to its high energy content and the fact that its combustion or reaction with oxygen produces water as the only by-product. With an increased focus on renewable energy and the transition towards a low-carbon economy, hydrogen has emerged as a key player in the quest for sustainable energy solutions. The hydrogen market relies on fossil fuel-based hydrogen production, but there's a growing emphasis on green hydrogen production methods using renewable energy sources. The hydrogen market driven by initiatives promoting clean energy, government policies supporting hydrogen adoption, and growing investments in hydrogen infrastructure.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The hydrogen market's current scenario is dynamic, with a shift towards green hydrogen production gaining traction due to environmental concerns and climate goals. Driving factors include the increasing demand for clean energy sources, advancements in hydrogen production technologies, and collaborations between industry players and governments to promote hydrogen as a viable energy solution. Growth is further propelled by rising investments in hydrogen infrastructure, the establishment of hydrogen corridors, and support for hydrogen-based transportation initiatives. Key trends encompass the expansion of hydrogen refueling infrastructure, integration of hydrogen in industries like transportation and power generation, and advancements in fuel cell technology. Opportunities lie in developing hydrogen ecosystems, scaling up production capacities, and fostering international cooperation for hydrogen trade. Recent developments include significant investments by key players like energy companies, automotive manufacturers, and technology firms in hydrogen-related projects, further bolstering the hydrogen market growth trajectory. The hydrogen market, with its potential to revolutionize the energy landscape, stands at the forefront of the transition towards a cleaner and more sustainable future, offering vast opportunities for technological advancements and global energy transformation.

Market Dynamics:

Increasing Global Focus on Decarbonization:

The urgent need to reduce greenhouse gas emissions and combat climate change is a key driver for the hydrogen market. Governments worldwide are adopting more stringent emission reduction targets and policies, creating a favorable environment for hydrogen as a clean energy carrier. For instance, the European Union's Green Deal and the Biden administration's clean energy agenda in the United States highlight the importance of hydrogen in achieving decarbonization goals.

Increasing international collaboration among governments, industry players, and research institutions is a significant driver for the hydrogen industry. For instance, the formation of international partnerships like the Hydrogen Council and the Clean Energy Ministerial's Hydrogen Initiative fosters knowledge-sharing, technology transfer, and collaborative research and development. Such collaborations facilitate the exchange of best practices, accelerate technological advancements, and create a supportive global ecosystem for hydrogen market.

High production costs restrain the market:

The hydrogen sector is the excessive expense of manufacturing, notably eco-friendly hydrogen. At present, electrolysis methods relying on renewable power can generate significant expenses when contrasted with traditional hydrogen generation approaches. However, ongoing research and development, along with economies of scale, are expected to drive down costs in the future for the hydrogen market.

The lack of a widespread hydrogen infrastructure network is a significant restraint for the industry. Establishing a comprehensive network of hydrogen production, storage, and distribution facilities requires substantial investment. Governments and industry players are actively addressing this challenge through initiatives such as Germany's National Hydrogen Strategy, which includes plans for the development of hydrogen corridors and a network of hydrogen refuelling stations.

Emerging Power-to-X Technologies:

The transportation sector sees great potential in hydrogen adoption, notably through hydrogen fuel cell vehicles poised to replace traditional internal combustion engine cars, thus curbing carbon emissions. Major players like Toyota, Hyundai, and Nikola Motors have achieved significant strides in fuel cell vehicle technology. Governments globally incentivize the development of hydrogen refueling stations to support these vehicles. Hydrogen finds application in diverse industries like ammonia production, steel manufacturing, and refineries, offering avenues to decarbonize these sectors. Thyssenkrupp, a German steel giant, plans to substitute coal for hydrogen in steel production, marking a substantial reduction in carbon emissions.

Moreover, Power-to-X technologies (P2H and P2A) are pivotal in the hydrogen market. These systems utilize surplus renewable energy to create hydrogen or ammonia, serving as energy carriers or raw materials. They facilitate renewable energy integration across power generation, heating, and industrial processes, and serve as sustainable alternatives in chemical and fertilizer production

Storage and Distribution Scaling Up Production:

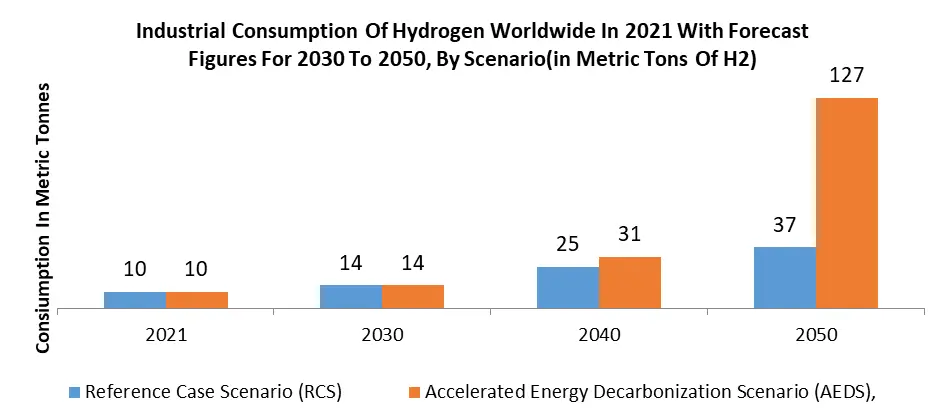

Scaling up hydrogen production to meet growing demand is a significant challenge. The main source of creating hydrogen involves the utilization of non-renewable sources such as fossil fuels that lead to the release of carbon into the atmosphere. In order to move towards a society that relies heavily on green hydrogen production, significant investment into structures, including but not limited to renewable energy infrastructure, advanced electrolyzer technologies, and optimized supply chains, is required. Hydrogen has specific storage and distribution challenges due to its low energy density and potential leakage issues. Developing efficient storage and transportation solutions, such as hydrogen pipelines and liquid hydrogen carriers, is crucial for the widespread adoption of hydrogen. Safety concerns associated with hydrogen handling and storage pose a challenge for the hydrogen market. While hydrogen has excellent safety records and is regulated rigorously, public perception and awareness remain critical. Ensuring proper safety measures, implementing robust regulations, and conducting comprehensive risk assessments are essential for gaining public trust and acceptance.

Hydrogen Market Segment Analysis:

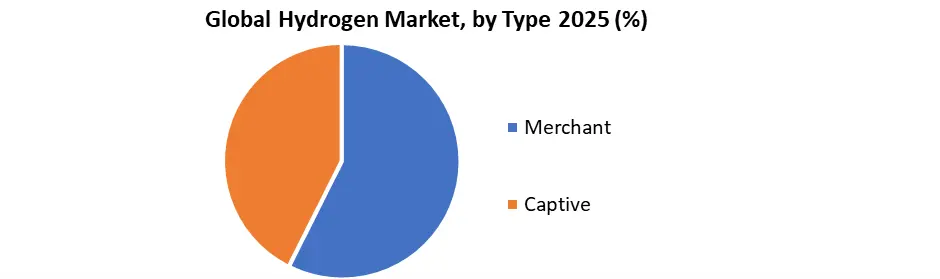

Based on type, the hydrogen market is categorized into merchant and captive. Merchant hydrogen is produced and sold to third-party customers while Captive hydrogen is produced and used by a single company or organization. While both merchant and captive hydrogen segments play a significant role in the hydrogen market, merchant hydrogen is widely used and has the potential for future growth. As the demand for hydrogen increases across various sectors, including transportation and power generation, merchant hydrogen production facilities scale up production and supply hydrogen to meet the growing hydrogen market requirements.

Based on the production process, The green hydrogen holds the dominance position in the market and expected to grow in the forecast period. With the increasing focus on decarbonization and renewable energy integration, the demand for green hydrogen as a clean energy carrier is expected to surge the hydrogen market. The declining costs of renewable energy technologies and supportive government policies further bolster the growth prospects of green hydrogen, positioning it as a key driver in the transition towards a sustainable and low-carbon economy.

Based on the application, the hydrogen market is categorized into transportation, power generation, industrial processes, residential heating, and others. Among these, transportation stands out as a widely used application with substantial growth potential for the hydrogen market. The transportation sector's shift towards decarbonization and the increasing availability of hydrogen refueling infrastructure is driving the adoption of FCVs. Hydrogen has considerable potential to perform a significant role in balancing the power grid and stockpiling energy, leading to the incorporation of renewable energy while supporting the alteration to a durable and solid power generation system. Furthermore, hydrogen has extensive uses in manufacturing processes. It acts as an essential piece of input for the creation of chemicals like ammonia, methanol, and others, and also for refining procedures like hydro cracking, desulfurization, and heat treatment of metals.

Based on technology, the hydrogen market is categorized into steam methane reforming (SMR), electrolysis, coal and biomass gasification, pyrolysis, and other emerging technologies. Among these, electrolysis stands out as a widely used technology with significant growth potential for the hydrogen market. By utilizing renewable energy sources, electrolysis functions to divide water molecules into hydrogen and oxygen, therefore allowing the generation of eco-friendly hydrogen. It represents a possible route to decarbonization and a clean energy shift, enabling hydrogen production without carbon emissions.

Hydrogen Market Regional Insights:

The hydrogen market in the North American region is expected to grow during the forecast period because of the well-established infrastructure, advanced technology, and strong commitment to sustainable energy solutions. Both the US and Canada have witnessed a significant increase in hydrogen-related investments. The US government, for instance, has launched the Hydrogen Energy Earthshot program, aimed at diminishing the cost of environmentally friendly hydrogen energy by 80% before 2032. Conversely, the Asia Pacific region is expected to experience the highest growth potential in the hydrogen market. Countries such as Japan, South Korea, and China have acknowledged the considerable role that hydrogen energy plays in achieving their long-term sustainability targets which drive the hydrogen market. Japan's Hydrogen Society vision, South Korea's hydrogen roadmap, and China's hydrogen industry development plans demonstrate their commitment to promoting the hydrogen sector.

These countries possess robust manufacturing capabilities, large-scale industrial demand, and strong renewable energy capacity, making them well-positioned to drive the growth of the hydrogen market in the Asia Pacific region. South America and MEA regions are also recognizing the potential of hydrogen in their respective energy landscapes. Countries like Chile and Saudi Arabia are exploring opportunities for green hydrogen production, leveraging their renewable energy resources. South Africa is investing in hydrogen as a way to diversify its energy mix and promote clean energy technologies. These areas possess the capacity to emerge as key leaders in the hydrogen sphere, fueled by their ability to tap into renewable energy potential, satisfy local needs, and mitigate carbon emissions.

Competitive Landscape

A mix of established players and emerging companies characterize the competitive landscape of the hydrogen market, each striving to position themselves in this rapidly growing sector. Air Liquide, a global leader in industrial gases and hydrogen, has established a strong presence in the hydrogen market. Air Liquide has been involved in numerous high-profile hydrogen projects worldwide, such as H2 Mobility in Germany and the HyBalance facility in Denmark. Another major player is Linde plc, formed by the merger of Linde AG and Praxair, Inc. Linde plc is a leading industrial gases and engineering company and has a strong focus on hydrogen production, distribution, and fuel cell technologies. Linde has a significant global presence and has been involved in projects like the world's largest PEM (Proton Exchange Membrane) electrolyzer plant in Canada.

Companies like Plug Power and Ballard Power Systems have established themselves as key players in the hydrogen fuel cell market, particularly in applications such as material handling equipment and transportation. In terms of recent mergers and acquisitions, a notable example is the merger between Plug Power and SK Group's subsidiary, SK Group, a South Korean conglomerate. This strategic partnership aims to accelerate the deployment of hydrogen fuel cell systems in South Korea and other Asian hydrogen markets. In terms of technological advancements, companies like Nel ASA, a leading hydrogen production solutions provider, have made significant progress in advancing electrolyzer technologies for large-scale green hydrogen production. Nel ASA's Proton PEM electrolyzers have demonstrated high efficiency and scalability, contributing to the growth of the green hydrogen sector.

Companies such as Hyundai and Toyota have been actively developing fuel-cell electric vehicles (FCEVs) and have made advancements in hydrogen fuel cell technology, including increased power output and extended driving ranges for the hydrogen market. These technological advancements and collaborations among established players and new entrants highlight the dynamic nature of the competitive landscape in the hydrogen market.

Hydrogen Industry Ecosystem

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 12 March 2026 | Argus Media / Gas TSOs | European Gas Transmission System Operators urged for uniform EU standards and de-risking of cross-border hydrogen pipelines to enable future flows. | This development aims to standardize infrastructure across the continent, facilitating a more integrated and competitive European hydrogen market. |

| 09 March 2026 | Copenhagen Infrastructure Partners (CIP) | CIP and Hy2gen officially cancelled a planned 240 MW renewable hydrogen and ammonia project in Norway. | The cancellation highlights ongoing market volatility and the challenges of securing final investment decisions (FID) for large-scale green projects. |

| 15 December 2025 | Hystar AS | Hystar announced a strategic collaboration with McDermott to develop a standardized 100 MW green hydrogen plant design using PEM electrolyzers. | Standardizing plant designs is expected to lower capital expenditure and accelerate the deployment of gigawatt-scale hydrogen hubs globally. |

| 25 July 2025 | Hy24 | Hy24 and Shanghai REFIRE signed a Memorandum of Understanding to scale green hydrogen production and fuel cell mobility solutions. | The partnership creates a bridge between European investment and Chinese manufacturing, boosting the commercialization of hydrogen-electric heavy transport. |

| 01 July 2025 | Envision Energy | Envision Energy commissioned a massive 500 MW electrolysis project in China, currently ranked as the world's largest operational site. | Setting a new benchmark for industrial-scale production, this project demonstrates the feasibility of high-volume green hydrogen for industrial decarbonization. |

Hydrogen Market Scope: Inquire before buying

| Hydrogen Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 203.73 USD Billion |

| Forecast Period 2026-2032 CAGR: | 8.7% | Market Size in 2032: | 365.3 USD Billion |

| Segments Covered: | by Type | Merchant Captive |

|

| by Production Process | Green Hydrogen Blue Hydrogen Grey Hydrogen Turquoise Hydrogen Pink Hydrogen Brown Hydrogen Purple Hydrogen |

||

| by Technology | Steam Methane Reforming (SMR) Electrolysis Gasification Pyrolysis Other emerging technologies |

||

| by Application | Transportation Power Generation Industrial Energy & Heating Others |

||

Hydrogen Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Hydrogen Market key players

- Reliance Industries Limited

- Air Liquide International S.A.

- Aker Asa

- Ballard Power Systems

- Bayotech

- Caloric Anlagenbau GmbH

- Chevron Corporation

- Enapter AG

- Engie SA

- Repsol

- ExxonMobil Corporation

- FuelCell Energy, Inc.

- Green Hydrogen Systems

- Hiringa Energy Ltd.

- Hygear

- Aurora Hydrogen

- Iberdrola, SA

- Idroenergy

- INOX Air Products Ltd.

- Johnson Matthey PLC

- Lhyfe

- Linde plc

- LNI Swissgas

- Messer Group GmbH

- Adani Green Energy

- Advanced Ionics

- Agfa-Gevaert

- Alchemr

- AlGalCo

- BASF

- Evolve Hydrogen

- Shell PLC