Stainless Steel Market Size by Type, Application, Product Form, Series, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2034

Overview

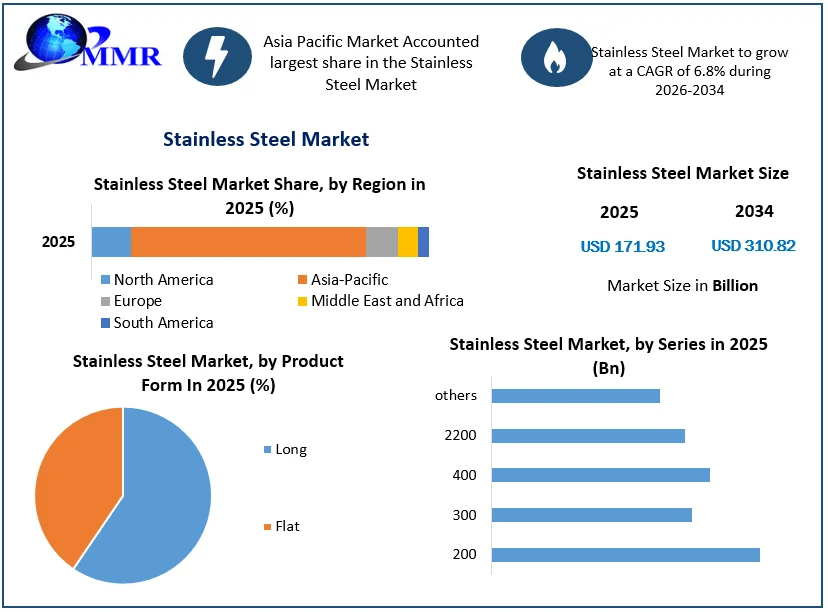

The Stainless Steel Market size was valued at USD 171.93 Billion in 2025 and the total Stainless Steel Market revenue is expected to grow at a CAGR of 6.8 % from 2026 to 2034, reaching nearly USD 310.82 Billion.

Stainless Steel Market Overview

Stainless steel is a type of steel alloy that contains at least 10.5% chromium, which makes it resistant to corrosion and staining. the chromium, stainless steel may also contain other elements such as nickel, molybdenum, and titanium. It is widely used in various applications due to its corrosion resistance, strength, and durability. It is commonly used in kitchen appliances, cutlery, medical instruments, chemical processing equipment, and construction materials. There are several types of stainless steel available, each with different properties and characteristics, but all of them share the common characteristic of being highly resistant to corrosion and staining. Stainless steel is produced through a variety of manufacturing processes, including melting, rolling, and annealing, to achieve the desired properties and characteristics.

Stainless Steel Market Snapshot

To know about the Research Methodology :- Request Free Sample Report

Stainless Steel Market Dynamics

Increasing usage and production of stainless steel in the automobiles sector driving market revenue growth

The increasing usage and production of stainless steel in the automobile sector is key drivers of revenue growth in the stainless steel market. The growing demand for lightweight, durable, and corrosion-resistant materials in the automotive industry has led to increased use of stainless steel. Stainless steel is widely used in the automotive sector for manufacturing various components such as exhaust systems, fuel tanks, bumpers, and other structural parts due to its superior corrosion resistance, durability, and strength-to-weight ratio.

Additionally, the increasing adoption of electric vehicles (EVs) is also driving the demand for stainless steel in the automotive industry, as it is used in the manufacturing of battery casings and charging stations. The growing trend towards vehicle customization and aesthetics is also driving the demand for stainless steel in the automotive industry, as it is commonly used in manufacturing decorative trim, grilles, and other interior and exterior components. Therefore, the increase in usage and production of stainless steel in the automobiles sector is expected to continue to drive revenue growth in the stainless steel market during the forecasting period.

Stainless Steel Market is increasing urbanization and infrastructure development to boost the market growth

Increasing urbanization and infrastructure development are drivers of the stainless steel market, as stainless steel is widely used in various construction applications such as building structures, bridges, and tunnels. As urban populations grow, the demand for new infrastructure and buildings increases, which in turn drives demand for stainless steel products. Stainless steel is used extensively in the construction of buildings, bridges, tunnels, and other infrastructure projects, as well as in the manufacturing of construction machinery and equipment.

In addition to its strength and durability, stainless steel's resistance to corrosion and staining makes it an ideal material for use in harsh outdoor environments. The demand for stainless steel in construction and infrastructure development is expected to grow during the forecasted period, as urbanization continues to drive the need for new buildings, roads, bridges, and other infrastructure projects. According to a report by Maximize market research, the global stainless steel market size is expected to reach USD 223.7 billion by 2030, growing at a CAGR of 6.8% from 2024 to 2030

According to a report by the United Nations, the global urban population is expected to reach 68% by 2050, up from 55% in 2023. This growth in urbanization is expected to drive significant demand for infrastructure development and construction activities, which in turn will drive demand for stainless steel products. The construction industry is the largest consumer of stainless steel products, accounting for approximately 50% of total stainless steel demand. Stainless steel is widely used in construction due to its strength, durability, and resistance to corrosion, which makes it ideal for use in building structures and other applications. In forecasting period, there have been several major infrastructure development projects around the world that have driven demand for stainless steel products.

For example, in the United States, the construction of the One World Trade Center in New York City required more than 35,000 tons of stainless steel, according to the International Stainless Steel Forum. In China, the construction of the Hong Kong-Zhuhai-Macau Bridge, the world's longest sea bridge, required more than 10,000 tons of stainless steel.

In addition, to infrastructure development, increasing urbanization also drives demand for stainless steel products in other applications such as household appliances, transportation, and consumer goods. For example, the growing middle class in developing countries is driving demand for stainless steel kitchen appliances such as refrigerators and ovens. According to a report by MMR, the global market for stainless steel kitchen appliances is expected to reach USD 23.3 billion by 2030, growing at a CAGR of 4.6% from 2024 to 2030

Increasing demand for energy and power generation infrastructure

The increasing demand for energy and power generation infrastructure is driven by the need to meet growing energy needs due to population growth, urbanization, and economic development. This demand is expected to continue to grow during the forecasting period, particularly in the developing Stainless Steel Industry globally, where access to reliable and affordable energy is still limited. Stainless steel is widely used in the manufacturing of power plants, pipelines, and other energy-related infrastructure due to its strength, durability, and resistance to high temperatures and corrosion.

In power generation, stainless steel is used in various applications, including turbine blades, heat exchangers, and other components in nuclear, thermal, and hydroelectric power plants. Stainless steel is also used in the construction of wind turbines, which are increasingly being used as a source of renewable energy. The use of stainless steel in wind turbines is driven by its durability, corrosion resistance, and ability to withstand extreme weather conditions. As the demand for renewable energy continues to grow, the demand for stainless steel in the manufacturing of wind turbines is also expected to increase.

In addition, to its use in power generation, stainless steel is used in the manufacturing of pipelines and other energy-related infrastructure. The oil and gas industry is a major consumer of stainless steel products, particularly in the construction of offshore platforms and subsea pipelines. The increasing demand for oil and gas in developing countries is expected to drive significant investment in new production projects, which in turn will drive demand for stainless steel products. Stainless steel is also used in a wide range of other energy-related applications, including energy storage systems, solar panel frames, and fuel cells. The growing demand for these applications is expected to drive further growth in the stainless steel market.

The Stainless Steel Market rise in the volume of recycled steel

The rise in the volume of recycled steel is an important trend in the stainless steel market. Stainless steel is highly recyclable, with most stainless steel products containing around 60% recycled content. The increasing adoption of recycling processes in the steel industry is expected to have a positive impact on the stainless steel market.

The key benefit of recycling steel is the reduction in the use of raw materials, which can help to conserve natural resources and reduce the environmental impact of steel production. Moreover, recycling steel can also reduce energy consumption and emissions, as the recycling process requires less energy than the production of virgin steel. The rise in the volume of recycled steel is also expected to have a positive impact on the cost of stainless steel products. Recycled steel is often cheaper than virgin steel, as it requires less processing and uses fewer resources.

As a result, the increased use of recycled steel in the production of stainless steel products can make them more affordable and accessible to customers. Furthermore, the increasing demand for sustainable and eco-friendly materials is also driving the adoption of recycled steel in the stainless steel market. Customers are becoming more aware of the environmental impact of materials and are looking for sustainable options. The use of recycled steel in stainless steel products can help to meet this demand and improve the sustainability of the industry.

Stainless Steel Market Growing availability of alternative materials

The growing availability of alternative materials is becoming a restraint for the stainless steel market. While stainless steel has been a popular material for various industries due to its properties like corrosion resistance, durability, and aesthetic appeal, the increasing availability of alternative materials has led to a shift in consumer preferences. Alternative material is aluminium, which is lightweight, corrosion-resistant, and relatively cheaper compared to stainless steel. The use of aluminium has increased in industries such as aerospace, automotive, and construction, which were traditionally dominated by stainless steel. Moreover, the increasing use of advanced composites and carbon fiber in industries such as aviation and defense is also posing a threat to the stainless steel market.

The availability of alternative materials is also leading to intense competition in the market, as manufacturers are continuously looking for ways to improve their materials and reduce costs. This competition can lead to a decrease in profit margins for stainless steel manufacturers and make it challenging for them to maintain their market position. However, stainless steel manufacturers are also innovating and investing in research and development to improve their products and stay competitive in the market. For instance, the development of duplex stainless steel, which offers higher strength and corrosion resistance, has helped the market stay relevant and competitive.

Volatile Prices of Raw Materials

Stainless steel is made from several raw materials such as iron ore, nickel, and chromium. The prices of these raw materials can vary significantly based on market conditions and supply and demand dynamics, which can have a significant impact on the production costs of stainless steel. Fluctuations in the prices of raw materials can cause a ripple effect throughout the supply chain, from the manufacturers to the end-users.

The volatile prices of raw materials are a significant restraint in the stainless steel market, as they can cause instability in the market and affect the profit margins of manufacturers. The stainless steel market is highly competitive, and manufacturers are continuously looking for ways to reduce their production costs to remain competitive. the increasing demand for the stainless steel industry has put pressure on the availability of raw materials, leading to price fluctuations.

The demand for stainless steel is expected to continue to grow in the coming years, which could exacerbate the problem of volatile raw material prices. In response, stainless steel manufacturers are looking for alternative raw materials or investing in vertical integration to mitigate the risk of volatile raw material prices. However, the volatile prices of raw materials remain a significant challenge for the stainless steel market and need to be addressed for the market to continue to grow in the future.

Stainless Steel Market Regionals insights

Asia Pacific is the largest market for stainless steel, with a significant revenue share of the global market. The region is expected to experience significant growth in the forecasting period due to the increasing demand for stainless steel products in various industries, chemical/petrochemical products, consumer goods, and heavy and vehicle transportation, medical items, energy is driving market revenue growth. According to the United Nations Comtrad database on international trade, India imported stainless steel wire worth USD 5 million from China in 2022.

The World Steel Association reports that in 2022, India's crude steel production climbed by roughly 19% to 121 Million Tonnes (MT), while the world's top producer, China, saw a 3.9 % decline to 1 038.8 MT. The second-largest producer of steel in the world, India, produced 128.7 MT in 2022, compared to China's 1 064.7 MT. The report states that in 2022, Japan produced 98.5 MT of steel as opposed to 85.6 MT in 2022. According to a report by Maximize Market Research, the Asia Pacific stainless steel market size was valued at USD 132.7 billion in 2022 and is expected to reach USD 223.7 billion by 2029, growing at a CAGR of 6.8% from 2022 to 2029.

Europe market is expected to register a moderate revenue growth rate during the forecast period. Europe had a leading large number of automotive component manufacturers and aerospace sector around 45%- 50% of steel is used in automotive exhaust systems. The region is expected to experience moderate growth in the forecasting period, driven by the increasing demand for stainless steel products in the automotive and construction industries. Such factors will fuel the market growth is majorly attributed to the increasing demand for duplex series of steel in electronic and engineering applications, owing to its cost-effective property.

Segments Covered in the Report

This Report covers the analysis of market trends in each sub-segment from 2022 to 2029, as well as historical data and estimates for revenue growth at the global, regional, and national levels. Reports and Data have segmented the stainless steel market based on grade, product, application, and region.

Stainless Steel Market Segmentations

Based on Product Form, the stainless steel market is segmented based on the form of the product. The flat products segment is anticipated to dominate the global market for stainless steel this accounted for over 74% of revenue share in the year 2025, CRC dominated the market in 2025, with over 40% of the global revenue share. The demand for CRC is primarily driven by the automotive industry due to its high strength and durability. HRC and plate segments grew during the forecast period, owing to their increasing use in construction and infrastructure development projects.

Overall, the stainless steel market offers a range of products with different properties and applications, catering to the needs of diverse industries. The long products segment includes a cold-finished bar, forged bar, hot rolled bar, profile, wire rod, and wire. The hot rolled bar segment dominated the market in 2025, with over 30% of the global revenue share. The report further states that the demand for hot rolled bars is primarily driven by the construction and automotive industries. The cold-finished bar and wire rod segments also witnessed significant growth during the forecast period, owing to their increasing use in the construction and infrastructure development sectors

Based on Application,

The stainless steel market is segmented based on Application industries. The automotive and

transportation segment is a major Application industry, driven by the increasing demand for lightweight and durable materials in the automotive sector. According to a market report by Maximize market research, the automotive and transportation segment dominated the Stainless Steel market share in 2025, accounting for over 25% of the global revenue share. The building and construction segment is also a significant Stainless Steel industry, driven by the increasing demand for stainless steel in infrastructure and construction projects. The heavy industries segment includes sectors such as oil and gas, power generation, and mining, which require stainless steel products with high corrosion resistance and durability. The consumer goods segment includes applications such as kitchen appliances, cutlery, and furniture, where stainless steel is used for its aesthetic appeal and corrosion resistance.

Based on Series, the global stainless steel market has been segmented in 200 series, 300 series, 400 series, and others. The 200 series segment expected a moderate revenue growth rate over the forecast period. The 200 series is a group of austenitic stainless steels that are extremely corrosion-resistant and have a low nickel content.200 series are generally harder and stronger than 300 series steels owing to increased nitrogen content.

Based on types the stainless steel market is segmented based on the types of stainless steel. Austenitic Stainless Steel is the most commonly used type, accounting for over 70% of the global stainless steel market. This type is widely used in applications such as automotive components, kitchenware, and chemical processing equipment, due to its excellent corrosion resistance, formability. Martensitic Stainless Steel is characterized by its high strength, hardness, and wear resistance, making it ideal for applications such as knives, turbine blades, and dental and surgical equipment.

Ferritic Stainless Steel is known for its high corrosion resistance, particularly against stress corrosion cracking, making it ideal for applications in the automotive and industrial sectors. Precipitation Hard Stainless Steel is a type of stainless steel that can be hardened by heat treatment, making it suitable for applications in the aerospace and nuclear industries. Duplex Stainless Steel, on the other hand, has a mixed microstructure of both austenitic and ferritic stainless steels, making it highly resistant to corrosion and ideal for applications in the chemical and petrochemical industries.

Stainless Steel Market Competitive landscape

The competitiveness of the Stainless Steel industry is increasing due to the ultimate innovations and productions, in order to remain competitive and maintain market share, companies must continually innovate and adapt to changing industry trends and consumer demands. Companies are focusing on improving their product offerings and increasing their distribution networks through partnerships and collaboration to get a larger portion of the market growing start-ups, mergers, and increasing trends of organic and inorganic growth is being witnessed.

The key players in the market such as Acerinox S.A., Aperam Stainless, POSCO, Outokumpu, and Momentive Performance Materials this major key players are using strategies such as acquisition and mergers, partnerships, and investment and divestment, fueling industry growth. Furthermore, large and medium-scale companies are offering highly improved product-type portfolios and customer services. The company uses both hot and cold rolled processes to manufacture steel-based products for customers. Moreover, the company is also involved in acquisition, R&D activity, and steel innovation to meet customer’s demand this trend is projected to positively impact the global market during the forecast period

Stainless Steel Market Recent development

| Date | Company | Development | Impact |

|---|---|---|---|

| 27 March 2025 | Jindal Stainless | The company acquired a 9.62% strategic stake in the RBI-licensed digital platform M1xchange to strengthen its supply chain ecosystem. | This partnership enables seamless access to affordable working capital for MSMEs and significantly reduces the overall working capital cycle. |

| 20 May 2025 | Outokumpu | The company expanded its commercial phase into the aerospace industry by delivering its first batch of a specialized spherical stainless steel metal powder for 3D printing. | The high-performance austenitic grade acts as a sustainable alternative to nickel-based alloys, shortening component development cycles for demanding aerospace applications. |

| 21 January 2026 | Acerinox | The manufacturer officially obtained the prestigious ISO 20400 certification for Sustainable Procurement. | This global milestone integrates verifiable environmental criteria and strict operational excellence throughout the company's entire raw material sourcing network. |

| 05 March 2026 | Acerinox | The firm partnered with Jeremias to commercialize the world’s first low-emission chimney line engineered with more than 90% recycled material. | The rollout successfully achieves a 50% reduction in carbon footprint, establishing a milestone for circular economy initiatives in sustainable construction. |

| 12 June 2026 | Acerinox | The company established a collaboration with Alfa Laval to integrate its low-emission EcoACX® steel range into gasketed plate heat exchangers. | Deploying stainless steel produced with 90% recycled content accelerates industrial decarbonization across global thermal management systems. |

Stainless Steel Market Scope: Inquire before buying

| Stainless Steel Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 171.93 Bn |

| Forecast Period 2026 to 2034 CAGR: | 6.8 % | Market Size in 2034: | USD 310.82 Bn |

| Segments Covered: | by Type | Austenitic Stainless Steel Martensitic Stainless Steel Ferritic Stainless Steel Precipitation Hard Stainless Steel Duplex Series |

|

| by Application | Automotive and Transportation Building and Construction Consumer Goods Heavy Industries Metal Products Other |

||

| by Product Form | Long Flat |

||

| by Series | 200 300 400 2200 others |

||

Stainless Steel Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan the and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

Stainless Steel Market Key players

1.Acerinox S.A.

2.Aperam Stainless,

3.POSCO,

4.Outokumpu,

5.Arcleor Mittal,

6.Thysssenkrupp Stainless GmbH,

7.Yieh United Steel Corp,

8.Nippon Steel Corporation,

9.Baosteel Group,

10.Jindal Stainless

11.Outokumpu

Frequently Asked Questions:

1] What is the growth rate of the Global stainless steel Market?

Ans. The Global Stainless Steel Market is growing at a significant rate of 6.8 % during the forecast period.

2] Which region is expected to dominate the Global Stainless Steel Market?

Ans. Asia Pacific is expected to dominate the Stainless Steel Market during the forecast period.

3] What is the expected Global Stainless Steel Market size by 2034?

Ans. The Stainless Steel Market size is expected to reach USD 310.82 Bn by 2034.

4] Which are the top players in the Global Stainless Steel Market?

Ans. Some of the top players operating in the stainless steel market include Acerinox S.A, Jindal Stainless, Nippon Steel Corporation, Aperam Stainless, Arcelor Mittal, Baosteel Group, Outokumpu, POSCO, ThyssenKrupp Stainless GmbH, and Yieh United Steel Corp.

5] Which sector is the key driver in the Stainless Steel Market?

Ans. The automotive industry sector is the key driver in the stainless steel market.