Polyethylene Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

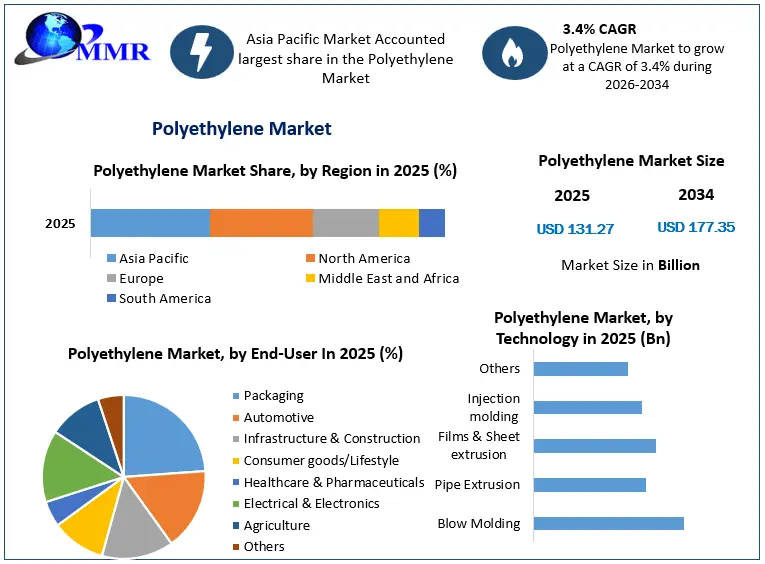

The Polyethylene Market size was valued at USD 131.27 Billion in 2025 and the total Polyethylene revenue is expected to grow at a CAGR of 3.4% from 2026 to 2034, reaching nearly USD 177.35 Billion.

Polyethylene Market Overview:

Polyethylene is a type of plastic that is made up of a long chain of carbon atoms with two hydrogen atoms connected to each one. Packaging film, garbage and grocery bags, agricultural mulch, wire, and cable insulation, squeeze bottles, toys, and housewares are some of the most common applications. Nylon, polyethylene, polyester, Teflon, and epoxy are examples of synthetic polymers. Natural polymers extracted from nature. They are frequently made of water. Silk, wool, DNA, cellulose, and proteins are examples of naturally occurring polymers. Blow Molding, Pipe Extrusion, Films and sheet extrusion, and Injection molding are some of the types of polyethylene technology.

Polyethylene Market Growth and Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Polyethylene Market Dynamics:

The global polyethylene market is experiencing robust demand growth across diverse industries such as automotive, food and beverage, electrical and electronics, and consumer products. This surge in demand is a major driving factor for the overall expansion of the polyethylene industry. Furthermore, the automotive industry's emphasis on enhancing vehicle economy by reducing weight is contributing significantly to the market's growth trajectory.

The burgeoning demand for polyethylene in various industries is primarily propelled by its versatile properties. Polyethylene is valued for its impact resistance, flexibility, moldability, and cost-effectiveness. In particular, the automotive sector's quest for lightweight materials to improve fuel efficiency has intensified the demand for polyethylene. This trend aligns with the industry's commitment to sustainability and environmental consciousness

However, the polyethylene market is not without its challenges. The presence of alternative products, such as polyethylene terephthalate and polypropylene, which share similar characteristics such as impact resistance, flexibility, moldability, and cost advantages, poses a limitation on the unbridled growth of the global market. The competition from these alternative materials necessitates strategic considerations for market players.

Polyethylene terephthalate pet is widely used in the packaging industry, particularly for the production of bottles and containers. The PET market's growth is fueled by the increasing demand for convenient and sustainable packaging solutions. Innovations in PET technology, such as the development of recycled PET, contribute to the market's environmental sustainability and appeal. The recycled polyethylene terephthalate (rPET) market addresses the growing concern for environmental sustainability. The recycling of PET contributes to reducing plastic waste and promoting a circular economy. Market players are investing in advanced recycling technologies to meet the demand for recycled materials across various industries, including packaging and textiles. Polyethylene Wax provides diverse applications, including in the production of adhesives, coatings, and plastics. The polyethylene wax market benefits from its lubricating and binding properties. As industries seek alternatives to traditional waxes, polyethylene wax emerges as a versatile and cost-effective solution.

Polyethylene Renaissance: Unveiling Opportunities across HDPE, PET, Polycaprolactone, and More

The High Density Polyethylene market is witnessing significant growth driven by its versatile applications, particularly in the packaging sector. As consumer preferences shift towards sustainable and efficient packaging solutions, HDPE stands out for its durability and cost-effectiveness. Similarly, the Polyethylene Terephthalate (PET) market is experiencing a surge in demand, especially in the beverage and textile industries. The lightweight and recyclable nature of PET makes it a preferred choice for bottling and packaging applications. In the realm of specialty plastics, the Polycaprolactone market is gaining traction. Its biodegradability and biocompatibility make it an attractive option in the medical and agricultural sectors.

Meanwhile, the Chlorinated Polyethylene market is witnessing increased demand, particularly in the manufacturing of impact-resistant and weather-resistant products. Its applications extend to cables, hoses, and industrial rubber. A noteworthy player in the polyethylene landscape is the Cross-Linked Polyethylene industry, which is crucial in sectors requiring high-performance and durable materials, such as plumbing and automotive industries. Additionally, the Metallocene Polyethylene market is making strides with advancements in polymerization technology and also offers enhanced properties, making it valuable in film production and pipe manufacturing.

Market Challenges:

Fluctuations in raw material prices further complicate the market landscape. The polyethylene market is susceptible to variations in the prices of raw materials, impacting production costs and, consequently, product pricing. These fluctuations pose a challenge for market players in maintaining stability and profitability. Strategies such as hedging and diversification become crucial in navigating these market dynamics. Despite the challenges, polyethylene continues to find new application areas, presenting avenues for market growth. Its use in fashion apparel, sports goods, and toys is expanding, driven by its desirable qualities such as physical stress resistance, durability, flexibility, and ease of product molding. This diversification of applications enhances the resilience of the polyethylene pet market by tapping into emerging consumer trends and preferences.

Major companies play a pivotal role in shaping the polyethylene market landscape. Initiatives and investments by industry giants contribute significantly to market growth. For instance, ExxonMobil, a key player in the market, commenced operations of a new 650,000 ton/year polyethylene line at its Texas site in July 2021. Such expansions and investments underscore the industry's commitment to meeting the growing demand for polyethylene. The ultra high molecular weight polyethylene (UHMWPE) market represents a specialized segment characterized by exceptionally high molecular weight, resulting in unique properties such as high impact strength and abrasion resistance. Applications in medical devices, defense, and industrial components drive the demand for UHMWPE. Market players are actively innovating to capitalize on the specific requirements of these industries.

Polyethylene Market Segment Analysis:

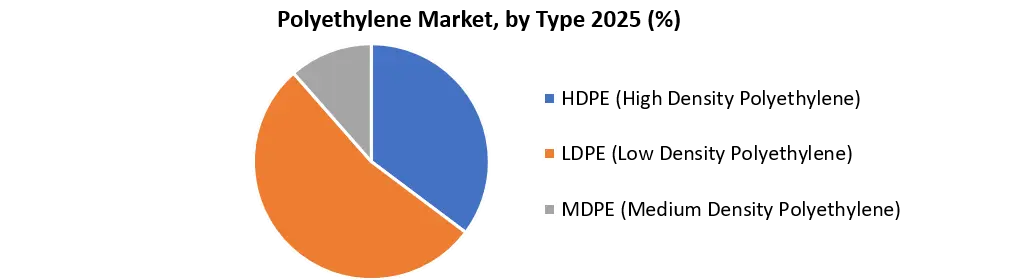

Based on the Type, the Polyethylene Market is segmented into HDPE (High-Density Polyethylene), LDPE (Low-Density Polyethylene), and MDPE (Medium Density Polyethylene). The HDPE (High-Density Polyethylene) segment is expected to hold the largest market share of xx% by 2034. HDPE, or high-density polyethylene, has various advantages over low and medium-density polyethylene. It's a petroleum-based thermoplastic polymer that's easy to work with, low in cost, has a high moisture barrier, and used to make opaque packaging. Household cleaning bottles, shampoo bottles, flowerpots, and blown mold drums are just a few examples of popular products. These are the key drivers that are expected to boost the growth of this segment in the global market during the forecast period 2026-2034.

Based on the End-User, the Polyethylene Market is segmented into Packaging, Automotive, Infrastructure and construction, Consumer goods/Lifestyle, Healthcare and Pharmaceuticals, Electrical and Electronics, Agriculture, and Others. The infrastructure and construction segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. Polyethylene films or sheets are widely used in construction and provide water protection for under-construction structures. Flooring, vapor retarders, countertop protection, window films, and roofing all utilize it. These sheets can be used to cover building materials, shut off rooms, and protect people from lead poisoning. During oil drilling or landfills, HDPE plastic sheeting protects groundwater from harmful pollutants.

The packaging segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2026-2034. PET (Polyethylene Terephthalate) is a moisture-resistant plastic developed from polyethylene that provides a solid protective structure for packaging. It's found in a variety of places, including cooking oil bottles, PET bottles, and milk cartons. Polyethylene packaging is cost-effective and attracts substantially less dust, dirt, or other foreign elements.

Polyethylene Market Regional Insights:

The Asia Pacific dominates the Polyethylene market during the forecast period 2026-2034. The Asia Pacific is expected to hold the largest market share of xx% by 2034. Several key factors supporting the current growth of the Asia Pacific market are the rapid adoption of industrial automation to increase output and the rising electronics, packaging, and automotive sectors in the region. Due to lower personnel costs and government assistance, China accounted for the highest revenue share in the Asia Pacific in 2025. China has emerged as a significant production and export base for more cost-effective plastic items. These are the major factors that drive the growth of this region in the market during the forecast period 2026-2034.

The global HDPE market faced significant challenges in H1 2024, with estimates revealing approximately $1.1 billion in losses for major exporters to China. The downturn, attributed to the worst the polyolefins industry has experienced, prompted a shift in market dynamics. The US and Canada emerged as sales winners, gaining $ 423 million in estimated sales. However, Iran, South Korea, Saudi Arabia, and the UAE witnessed notable drops in HDPE imports. The crisis is linked to miscalculations concerning China's economic factors and demographics, underscoring the need for capacity rationalization in the face of oversupply.

Polyethylene Market Recent Industry Developments:

| Date | Company | Development | Impact |

|---|---|---|---|

| 01 April 2026 | Dow | The company implemented a 30 cents per pound price increase for polyethylene in U.S. and Canadian markets. | This aggressive pricing strategy is passing upstream cost pressures to downstream packaging and consumer goods manufacturers. |

| 05 May 2026 | SABIC | The company launched ULTEM™ reactive oligomer technology for use in high-performance, lightweight aerospace composites. | This innovation enhances structural durability and reduces weight, strengthening the company's position in specialized high-value plastic markets. |

| 01 November 2024 | BASF | The firm launched the new Easiplas™ HDPE brand and reached major construction milestones at its Zhanjiang Verbund site. | This expands production capacity and supply of high-quality plastics for the growing Chinese infrastructure and packaging markets. |

| 01 September 2024 | Indian Oil Corporation Limited (IOCL) | IOCL adopted Univation’s UNIPOL™ PE Process Technology for a new 650,000-ton capacity polyethylene facility. | This deployment enables the large-scale production of LLDPE and HDPE to support regional demand for flexible and rigid packaging. |

| 01 October 2024 | KPS (OPW/Dover) | The company introduced a 3" conductive HDPE double-wall piping system featuring a zero-permeation EVOH layer. | The technology provides superior environmental protection and safety for high-flow fuel applications in critical infrastructure. |

Polyethylene Market Scope: Inquiry Before Buying

| Polyethylene Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 131.27 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 3.4% | Market Size in 2034: | USD 177.35 Bn. |

| Segments Covered: | by Type | HDPE (High Density Polyethylene) LDPE (Low Density Polyethylene) MDPE (Medium Density Polyethylene) |

|

| by Technology | Blow Molding Pipe Extrusion Films & Sheet extrusion Injection molding Others |

||

| by End-User | Packaging Automotive Infrastructure & Construction Consumer goods/Lifestyle Healthcare & Pharmaceuticals Electrical & Electronics Agriculture Others |

||

Polyethylene Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Polyethylene Key Players

1. Reliance Industries Limited (India)

2. Formosa Plastic Group (Taiwan)

3. Braskem (Brazil)

4. Repsol (Spain)

5. China International Petroleum Corporation (China)

6. INEOS (UK)

7. Ducor Petrochemicals (Netherland)

8. SABIC (Saudi Arabia)

9. China Petroleum & Chemical Corporation (China)

10. Borouge (UAE)

11. Borealis AG (Austria)

12. MOL Group (Hungary)

13. Beaulieu International Group (Belgium)

14. Chevron Phillips Chemical Company (US)

15. Sasol Ltd. (South Africa)

16. DowDuPont (US)

Frequently Asked Questions:

1] What is the growth rate of the Global Polyethylene Market?

Ans. The Global Polyethylene Market is growing at a significant rate of 3.4 % during the forecast period.

2] Which region is expected to dominate the Global Polyethylene Market?

Ans. Asia Pacific region is expected to dominate the Polyethylene Market growth potential during the forecast period.

3] What is the expected Global Polyethylene Market size by 2034?

Ans. The Polyethylene Market size is expected to reach USD 177.35 Bn by 2034.

4] Which are the top players in the Global Polyethylene Market?

Ans. The top players in the market include Reliance Industries Limited (India), Formosa Plastic Group (Taiwan) and others.

5] What are the factors driving the Global Polyethylene Market growth?

Ans. Polyethylene demand growth is robust across industries such as automotive, food and beverage, electrical and electronics, and consumer products, which is a major driving factor for the global polyethylene market's growth.

6] Which Country dominated the largest Polyethylene Market Growth?

Ans. China held the largest market share in the Asia-Pacific region.