Polyether Polyols Market by Type, Application, End User, and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

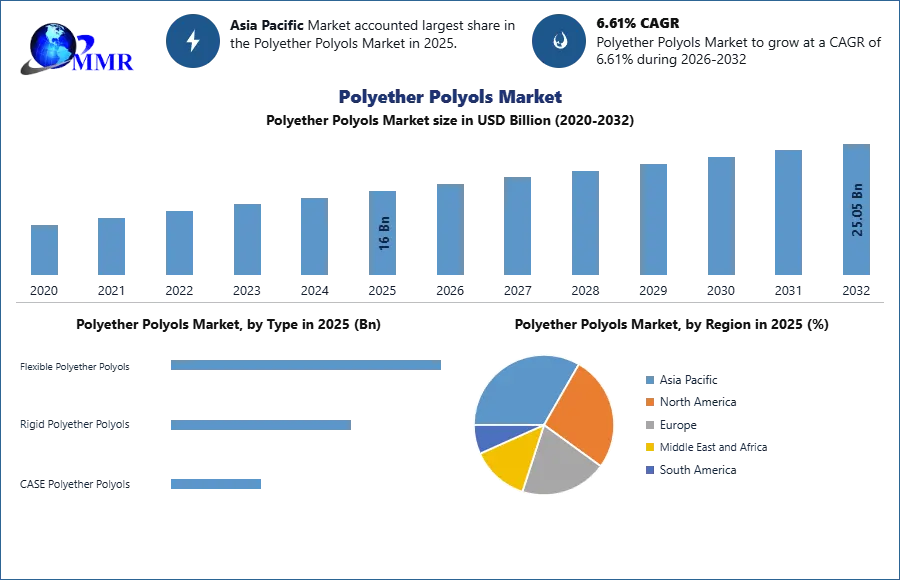

The Polyether Polyols Market size was valued at USD 16 Billion in 2025 and the total Polyether Polyols revenue is expected to grow at a CAGR of 6.61% from 2026 to 2032, reaching nearly USD 25.05 Billion.

Polyether Polyols Market Dynamics

A Polyether polyols are key components used in the production of polyurethanes. Polyether-based polyurethanes exhibit enhanced hydrolytic stability and excellent resistance to weak acids and bases compared to polyester-based polyurethanes. Various factors such as growth of automotive and construction industries, growing demand from refrigerator and freezer manufacturers in APAC, increasing demand for bio-based Polyols are mainly driving the global polyether polyols market over forecast period.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The report covers an in depth analysis of COVID 19 pandemic impact on Global Polyether Polyols Market by region and on the key players revenue affected till April 2020 and expected short term and long term impact on the market.

Rising efforts for energy conservation are propelling demand for polyether polyols with high insulation, lightweight, durability, comfort, and resilience properties, particularly in the building and construction, furnishing, flooring, automobile, and packaging industries. This is expected to create lucrative opportunities for global market over the forecast period.

However, factors such as stringent environmental regulations on the manufacturing of polyurethane polyols and volatile prices of raw materials are restraining the market growth over forecast period.

Global Polyether Polyols Market is segmented by type, by application, by end user and by region. By type, rigid polyether polyols held 67.45% of market share in 2025 and is expected to keep its dominance over forecast period. Rigid polyether polyols is manufactured using various starters such as sucrose, sorbitol, glycols, pentaerythritol, ethylene diamine, triethylamine and their mixtures. These polyether polyols are marketed under the brand various brand names. These are short chain polyethers being used in rigid polyurethane foam formulations. Rigid polyols are used in foamed and solid applications or in combination with polyols with a higher molecular weight to increase hardness of the final product.

By End user, construction end user held 34.54% of market share in 2025 and is expected to keep its dominance over forecast period owing to increasing use of polyether polyols in the building and construction industry as it possesses good insulating properties and provides uniform temperature stability. Moreover, the growing preference for energy-efficient buildings to reduce carbon emissions is expected to create lucrative opportunities over forecast period.

Construction end user is followed by Automotive and furnishing. Polyether Polyols are increasingly used in the automotive industry in vehicle interiors such as acoustic parts, seats, steering wheels, and back-foam instrument panels and doors. An increase in automobile production, especially in North America, APAC and Europe regions are expected to create lucrative opportunities for market over forecast period.

By geography, APAC dominated the global market with xx% of market share in 2025 and is expected to keep its dominance over forecast period. Factors such as growing automotive industry, increasing polymer consumption and the increasing residential and commercial construction as a result of urbanization are mainly driving the market in this region. China is leading the APAC market. Wanhua Chemical Group co. ltd. is leading player in china. A Wanhua Chemical has 3 main plants in china, one is Yantai (North China), and one is in Foshan (South China), one is in Ningbo (East China), with production capacities 210KT of Polyether Polyols. The Wanhua Chemical mainly supplies rigid polyols in 7 countries with more than 17 series and 100 grades. APAC is followed by Europe and North America.

The European market is expected to hold xx% of market share over forecast period owing to expanding automotive industry with the surge in demand for energy-efficient and lightweight vehicles. The expansion of Polyether Polyols capacities by the manufacturers such as BASF SE (Germany), Solvay (Belgium) and Covestro AG (Germany) to meet the surging demand in the automotive and furniture industries is expected to boost the demand for Polyether Polyols in this region.

Report covers in depth analysis of key development, marketing strategies, value chain, supply chain and company profiles of market leaders, potential players and new entrants. Key players operating in this market are adopting various organic and inorganic growth strategies such as merger& acquisitions, collaborations, strategic alliances, expansion, joint ventures, new product launches, patent and diversification to increase regional presence and business opeartions. BASF SE (Germany) is a leading player in global polyether polyols market.

BASF offers a series of reactive and non-reactive polyols for numerous applications. All reactive polyols have an ethylene oxide (EO) end-cap, creating a primary hydroxyl group. BASF’s non-reactive polyether polyols are suitable for the continuous production of flexible polyurethane foam by means of the slabstock process. With BASF, customers benefit from a strong partner with a global and local advantage. Their large-scale plants and international presence including our six “Verbund” sites and around 380 production facilities allow us to offer reliable, competitive products to our customers. BASF is dedicated to ensure a competitive & reliable supply and to support local needs by leveraging technologies.

The objective of the report is to present a comprehensive analysis of the Global Polyether Polyols Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that includes market leaders, followers and new entrants. PORTER, SVOR, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report.

External as well as internal factors that are supposed to affect the business positively or negatively have been analysed, which will give a clear futuristic view of the industry to the decision-makers. The report also helps in understanding Global Polyether Polyols Market dynamics, structure by analyzing the market segments and project Global Polyether Polyols Market. Clear representation of competitive analysis of key players by price, financial position, Product portfolio, growth strategies, and regional presence in the Global Polyether Polyols Market make the report investor’s guide.

Recent Industry Developments

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 11 March 2026 | ADNOC / Covestro | Completed the landmark acquisition of Covestro for approximately €14.7 billion, integrating its vast polyol and polyurethane portfolio into ADNOC's chemical division. | This merger creates a vertically integrated energy-to-chemicals giant, significantly altering the competitive landscape for global polyether polyol supply. |

| 25 January 2026 | BASF / Wanhua Chemical | Formed a strategic joint venture for polyols production in China, specifically targeting the expansion of capacity for high-performance rigid foam materials. | The partnership strengthens the strategic footprint in Asia, optimizing production costs for the world's largest regional polyether polyols market. |

| 12 January 2026 | Dow | Commercialized the VORANOL™ WK 5750, a next-generation polyether polyol optimized for hypersoft flexible foams in automotive and furniture seating. | This product launch sets a new industry benchmark for low-VOC emissions and improved comfort in consumer-facing polyurethane applications. |

| 15 November 2025 | Stepan Company | Finalized the acquisition of INVISTA's aromatic polyester polyol business, including key manufacturing plants and intellectual property. | This consolidation broadens Stepan's global polyol footprint and enhances its ability to supply hybrid polyether-polyester systems for rigid insulation. |

| 04 July 2025 | Cargill / BASF | Launched a comprehensive Bio-Polyol Market Initiative aimed at replacing 20% of petroleum-based precursors with renewable agricultural feedstocks by 2030. | The initiative drives decarbonization across the value chain, meeting stringent new EU and North American environmental mandates for sustainable chemistry. |

| 23 March 2025 | Covestro / Shell plc | Signed a multi-year supply agreement for bio-circular polyols utilizing ISCC PLUS certified mass-balance accounting. | The collaboration establishes a scalable supply of circular materials, allowing downstream customers to reduce their Scope 3 emissions without retooling production. |

Scope of Polyether Polyols Market: Inquire before buying

| Polyether Polyols Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 16 USD Billion |

| Forecast Period 2026-2032 CAGR: | 6.61% | Market Size in 2032: | 25.05 USD Billion |

| Segments Covered: | by Type | Flexible Polyether Polyols Rigid Polyether Polyols CASE Polyether Polyols |

|

| by Application | Polyurethane Foams Flexible Rigid Adhesives Sealants Coatings Elastomers Insulation Others |

||

| by End User | Construction Automotive Furniture & Bedding Packaging Electrical & Electronics Footwear Healthcare Others |

||

| by Functionality | Low Functionality High Functionality |

||

Polyether Polyols Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest)

Key Players / Competitors Profiles Covered in Brief in Global Polyether Polyols Market Report in Strategic Perspective:

- Bayer AG

- BASF SE

- Covestro AG

- Dow Chemical Company

- Huntsman International LLC

- Shell plc

- Wanhua Chemical Group Co., Ltd.

- Repsol

- SABIC

- MOL Hungarian Oil and Gas PLC

- Sadara Chemical Company

- Mitsui Chemicals, Inc.

- KPX Chemical

- Tosoh Corporation

- Stepan Company

- COIM Group

- Manali Petrochemicals Limited

- AGC Inc.

- Sanyo Chemical Industries, Ltd.

- Indorama Ventures Public Company Limited

- Carpenter Co.

- Inov Polyurethanes

- Shandong Bluestar Dongda Co., Ltd.

- Jining Huakai Resin Co., Ltd.

- Limin Chemical Co., Ltd.