Orthopedic Devices Marke32t Size by Devices Type, End-User and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

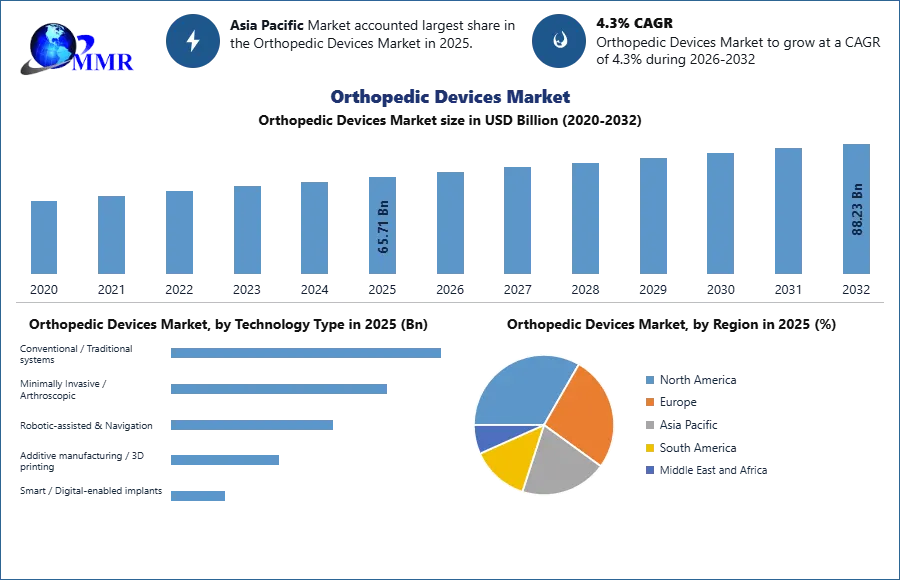

Orthopedic Devices Market was valued at USD 60.84 Billion in 2025, and it is expected to reach USD 88.23 Billion by 2032, exhibiting a CAGR of 4.3% during the forecast period (2025-2032)

Orthopedic Devices are medical devices and accessories used to treat orthopaedic problems, such as joint reconstruction, spinal devices, trauma fixation devices, arthroscopic devices, and so on. The global orthopaedic devices market is rapidly developing, owing to an apparent increase in the number of orthopaedic surgical procedures conducted globally. Because of the huge increase in orthopaedic treatments, there is a large need for orthopaedic equipment. Globally, 22.3 million orthopaedic surgical operations were conducted in 2017. Orthopaedic devices are critical in providing pain relief, improving quality of life, and increasing mobility for patients suffering from musculoskeletal illnesses and abnormalities. These orthopaedic medical equipment and methods are constantly evolving in response to changing customer demands. Technological improvements and the incorporation of digital technology are now the primary drivers of the orthopaedic devices market's revenue growth.

Maintaining a trained and experienced team of specialists is becoming increasingly important for healthcare organisations dealing with rapid technology changes. When building prototype medical equipment, inventors and producers must keep the comfort, safety, and convenience of the consumers in mind. Incorporating cutting-edge ideas, such as wearable medical gadgets and medical textiles, has undoubtedly revolutionised the field of orthopaedics in recent years. The Orthopedic Devices market is expected to expand significantly in various areas during the world. During the forecast period, the market size in the North America area is expected to reach USD 14,820 million in the United States. The market size in Germany and the United Kingdom in Europe is predicted to be USD 3,223 million and USD 1,700 million, respectively. In the Asia Pacific area, Japan and China are estimated to have market sizes of USD 4,194 million and USD 2,235 million, respectively.

Research Methodology

The research report highly depends on both primary and secondary data sources. The research process involves the investigation of various factors affecting the industry, such as government policy, market environment, competitive landscape, historical data, current market trends, technological innovation, upcoming technologies, and technical progress in related industries, as well as market risks, opportunities, market barriers, and challenges. All conceivable elements influencing the markets included in this research study have been considered, examined in depth, validated through primary research, and evaluated to provide the final quantitative and qualitative data. The market size for top-level markets and sub-segments is normalised, and the impact of inflation, economic downturns, regulatory & policy changes, and other variables is factored into the market forecast.

This data is combined and added with detailed inputs and analysis, and presented in the report. Extensive primary research was conducted to acquire information and verify and confirm the crucial numbers arrived at after comprehensive market engineering and calculations for market statistics; and data triangulation. Bottom-up technique is widely employed in the whole market engineering process, along with multiple data triangulation methodologies, to perform market estimation and forecasting for the overall market segments and sub-segments covered in this research.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Orthopedic Devices Market Dynamics

Reshaping the Future of Orthopaedic Healthcare with Wearable Technology

Wearable technology stands out as an interesting endeavour that has garnered significant popularity during the world in recent years. This technology, which allows numerous industry specialists and individuals to measure personal fitness and health criteria, is growing more exact with each modern innovation. As these devices improve in accuracy and gain more applications in health monitoring, their potential to impact orthopaedic treatment is expected to skyrocket in the near future. Orthopaedic professionals may utilise this technology to analyse and assess their patients' pre-operative course, allowing them to explain many aspects of treatment without having to personally attend to them.

Various device makers have gone to great lengths to provide fresh developments in the orthopaedic business area, speculating on the devices' future usage in orthopaedic treatment. Exactech, a joint replacement solutions provider, acquired Muvr Labs, one of the best patient wearable device makers, for an undisclosed sum in December 2020. The portfolio of the latter firm is intended to facilitate surgeons' contact with joint replacement patients during the treatment process. Furthermore, Muvr's platform includes mobile device apps, wearables, and chatbot texting to enable remote patient monitoring while healthcare professionals receive real-time data for the patients' recovery and experience.

Growing Use of Robotics, Computer-aided Surgery, and 3D Printing

The growing usage of technologically sophisticated items in the minimally invasive surgery area, such as robots and computer-aided surgical instruments, has led in an increase in demand for minimally invasive orthopaedic operations. Minimally invasive procedures have been shown to be cost-effective and accurate, with the added benefit of speedy recovery and shorter hospital stays. A growing number of orthopaedic firms are expanding their product offerings to incorporate robots to aid surgeons during knee, hip, or spine surgeries. Medtronic completed the acquisition of Mazor Robotics in December 2018, which was engaged in the development of the Mazor X guidance system and the Renaissance robot-assisted spine surgery equipment, with the goal of expanding into the robot-assisted spine surgery area.

High Investment in Research & Development

Due to a lack of effective surgical equipment, available trauma care procedures cannot entirely replace bodily components. As a result, manufacturers are investing much in research and development to create creative and efficient equipment. This rise in R&D activity is expected to result in rapid market expansion in the near future. A growth in the number of additional bone-related ailments, as well as technology developments, are likely to drive the market even further. Obesity is one of the key risk factors for arthritis. Being overweight or obese raised the incidence of knee osteoarthritis (OA) by 2.5 to 4.6 times when compared to being of normal weight, according to research published in the BMJ Journal in 2020. The global market is oligopolistic, with a few international firms controlling more than 80% of the market share.

Companies concentrate on product development and providing orthopaedic equipment at reasonable rates, particularly in emerging nations. The development of minimally invasive orthopaedic devices for single treatments is expected to increase the number of procedures performed in both developed and emerging nations. Partnerships, product approvals, acquisitions, and new launches are examples of important developments that might have a favourable influence on the industry in the coming years. Medtronic PLC, for example, will debut the Adaptix Interbody System, a titanium spinal implant, in November 2020. In 2019, Medtronic also acquired Titan Spine, a privately held surface technology and titanium spine interbody implant company. Such measures might help the market flourish even further.

Increasing Prevalence of Orthopedic Disorders and Traumatic Injuries

The high frequency of orthopaedic problems, such as degenerative bone disease, as well as the expanding ageing population and the rising number of traffic accidents, all contribute to market growth. Furthermore, the early development of musculoskeletal problems, mostly caused by sedentary lifestyles and obesity, is predicted to drive market expansion. The key driver driving demand for these devices during the forecast period will be a significant rise in the frequency of musculoskeletal illnesses and orthopaedic injuries, which will result in limited mobility and terrible physical discomfort. Musculoskeletal diseases affect around 1.71 billion people worldwide, according to data published by the Global Burden of Disease in 2021. As a result, an increase in musculoskeletal problems is expected to drive the market between 2022 and 2030.

According to the American Academy of Orthopedic Surgeons, over 6.8 million individuals with orthopaedic injuries seek medical assistance in the United States alone each year. Furthermore, a significant increase in the prevalence of osteoporosis (brittle bone), which is defined by a low bone to mass density ratio and physical weakening of bone structures, is predicted to drive demand for orthopaedic surgical devices in the near future. According to the National Institute of Health (NIH), more than 53 million persons in the United States are expected to have osteoporosis and are at a higher risk of developing the condition due to a poor bone to mass ratio.

Rise in the Elderly population to Increase the Volume of Surgical Procedures

Because senior persons are more prone to hip fractures, an obvious increase in the geriatric population base is complementing the orthopaedic device market expansion. According to a 2015 United Health Foundation estimate, more than 300,000 seniors aged 65 and over are hospitalised each year for hip fractures. Furthermore, around 30% of seniors fall each year, increasing the frequency of orthopaedic injuries and boosting demand for these devices.

The development of orthopaedic research and technology advancements, the expanding obese population, and inactive & sedentary lifestyles are all expected to contribute to increased demand for these devices in the future years. Furthermore, increased research investment by major players in the development of beneficial and less invasive orthopaedic devices is expected to boost the orthopaedic devices market during the expected period.

High Cost of Surgical Implantation and Post-Surgical Complications

The development of modern orthopaedic devices is expected to considerably cut the cost of existing ones. This contributes to greater acceptance of the latter in emerging economies such as Asia Pacific and the Middle East, where medical reimbursement is scarce. These actions are expected to have a positive impact on procedure volume and market growth in the near future. However, despite an increase in the senior population and an increase in the prevalence of orthopaedic injuries worldwide, the high cost of the surgery and post-surgical problems are restricting market growth. Postoperative infections, neuroparalysis, and a loss of full range of motion are some of the risks and problems associated with orthopaedic surgical treatments that may limit market growth.

Orthopedic Devices Market Segment Analysis

Based on End User, Hospitals is estimated to be a dominating end user segment during the forecast period. Orthopedic devices are mostly used in hospitals because they are surgically implanted. Hospitals treat a high number of patients who have suffered orthopaedic injuries. Aside from therapy, effective reimbursement policies given by hospitals are a crucial element contributing to the increasing proportion of patients being treated in hospitals. However, growing the use of minimally invasive treatments is expected to result in a preference for outpatient surgical centres.

As people become more aware of the availability of innovative items, hospitals are being pushed to continuously improve their technology and services. Furthermore, payment coverage for orthopaedic therapies has boosted the use of orthopaedic procedures. These characteristics enable clients to choose more complex and expensive treatment choices, increasing overall revenue produced.

Based on Devices Type, the market is segmented into joint reconstruction devices, spinal devices, trauma devices, arthroscopy devices, orthobiologics, and others. In 2019, the joint reconstruction category had the lion's share of the market. The segment is expanding because to an increase in surgeries such as knee and hip replacements, shoulder and extremity reconstructions, and other musculoskeletal procedures involving these joints. The arthroscopy devices (sports medicine/soft tissue repair) sector is expected to develop at a substantial rate during the forecast period, owing to an increase in sports-related soft tissue injuries and the increased launch of innovative products in this field.

In 2025, the knee orthopaedic devices category held the biggest market share of more than 28.2%. This category is likely to continue its dominance from 2025 to 2032, thanks to an increase in the number of knee procedures. However, high expenses and lengthy follow-up periods are significant barriers to sector expansion. Furthermore, onerous regulatory standards for the clearance of class III medical devices are impeding their approval. Total knee replacement surgeries are expected to increase to 3.5 million per year by 2029. Almost half of all Americans will get knee osteoarthritis in at least one knee over their lives. Approximately 80% of osteoarthritis patients have some degree of mobility impairment.

Regional Insights

North America dominated the global orthopedic device market in 2022, with a revenue share of more than 46%. High demand for modern healthcare services is likely to boost the regional market, owing to the presence of well-developed healthcare infrastructure, industry heavyweights, and reimbursement coverage. The region's orthopaedic surgery volume is being fueled by an ever-increasing target patient population as a result of ageing and increased vehicle accidents. The increasing frequency of orthopaedic disorders, along with the use of improved treatment technologies, is expected to drive market expansion in the United States.

Europe is the second-largest market due to a rise in operations, increased knowledge of technologically sophisticated orthopaedic equipment, and an increase in healthcare expenditure by the region's population. However, Asia Pacific is expected to grow at a faster rate during the forecast period. Factors such as a big patient pool and rising healthcare spending in the region are complementing Asia Pacific market expansion. Furthermore, the rising purchasing power of the public in emerging nations such as India and China will affect market growth.

During the forecast period, Asia Pacific is estimated to have the fastest CAGR. China and India are estimated to have the world's largest senior population pools. As a result, demand from these countries is expected to skyrocket in the near future. Furthermore, the thriving medical tourism business, owing to the provision of modern healthcare treatments at cost-effective prices, is likely to attract an increasing number of patients from the target patient group. Japan has a significant number of implant producers and spends more money on healthcare than most other nations in the area. Furthermore, rapid adoption of new technologies is estimated to promote regional market expansion.

Orthopedic Devices Market Recent Development

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2026 | MTF Biologics and Kolosis BIO | The companies launched Summit Matrix, a sophisticated synthetic bone graft designed to enhance bone regeneration. | The development addresses the growing demand for biologics in spinal fusion and trauma surgeries to improve patient recovery times. |

| 05 January 2026 | Spineology Inc. | The company rolled out OptiMesh HA Nano, integrating expandable implant technology with a specialized hydroxyapatite (HA) surface. | This innovation aims to transform spinal fusion surgeries by facilitating osteoconduction and ensuring more stable interbody fixation. |

| 10 October 2025 | University of Utah Orthopaedic Innovation Center | The center launched the Dynamic Compression Implant System to revolutionize fracture fixation and joint fusion. | This system provides continuous active compression, which is expected to reduce implant failure rates and improve osteotomy stabilization. |

| 12 August 2025 | OIC International & AddUp | The firms collaborated to establish a state-of-the-art 3D-printed orthopedic implant manufacturing facility in the AMTZ hub. | The facility will scale the production of customized implants, significantly reducing costs for knee and hip replacements in emerging markets. |

| 15 July 2025 | Straits Orthopaedics | The company acquired Medin Technologies, a U.S.-based manufacturer of sterilization cases and trays for orthopedics. | The acquisition strengthens the company’s contract manufacturing capabilities and vertical integration within the surgical instrument supply chain. |

| 28 January 2025 | Zimmer Biomet | Zimmer Biomet entered into a definitive agreement to acquire Paragon 28 for an enterprise value of $1.2 billion. | This strategic move dramatically expands the company's portfolio in the high-growth foot and ankle surgical market. |

Report Scope:

The Orthopedic Devices Market research report includes product categorization, product application, development trend, product technology, competitive landscape, industrial chain structure, industry overview, national policy and planning analysis of the industry, and the most recent dynamic analysis, among other things. The study discusses the worldwide market's drivers, opportunities, and limitations. It discusses the influence of various drivers, trends, and constraints on market demand during the forecast period. The research also outlines market potential on a global scale. The research includes the production time, base distribution, technical characteristics, research and development trends, technology sources, and raw material sources of significant Orthopedic Devices Market firms in terms of production bases and technologies. The more precise research also contains the key application areas of market and consumption, significant regions and consumption, major producers, distributors, raw material suppliers, equipment providers, and their contact information, as well as an analysis of the industry chain relationship. This report's study also contains product specifications, manufacturing processes, cost structure, and data information organised by area, technology, and application.

Orthopedic Devices Market Scope: Inquire before buying

| Orthopedic Devices Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 65.71 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.3% | Market Size in 2032: | 88.23 USD Billion |

| Segments Covered: | by Technology Type | Conventional / Traditional systems Minimally Invasive / Arthroscopic Robotic-assisted & Navigation Additive manufacturing / 3D printing Smart / Digital-enabled implants |

|

| by Material Type | Metal (e.g., titanium, stainless steel, cobalt-chromium) Polymers (e.g., UHMWPE, PMMA) Ceramics Composite Materials Others |

||

| by Devices Type | Joint Reconstruction Devices Knee Hip Extremities Spinal Devices Spinal Fusion Devices Spinal Non-Fusion Devices Trauma Devices Arthroscopy Devices Orthobiologic Devices Others |

||

| by End-User | Hospitals Orthopedic Clinic Ambulatory Surgical Centers Others |

||

Orthopedic Devices Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (razil, Argentina Rest of South America)

Key Players:

1. Johnson & Johnson

2. Medtronic

3. Smith & Nephew Plc.

4. Aap Implantate Ag

5. Aesculap Inc.

6. Alphatec Spine

7. Amedica Corporation

8. Apatech Ltd.

9. Arthrocare Corporation

10. Biomet Inc.

11. Conmed Corporation

12. Depuy Inc.

13. Donjoy Inc.

14. Exatech Inc.

15. Globus Medical Inc.

16. Integra Lifesciences Holding Corporation

17. Medtronic Inc.

18. Nuvasive Inc.

19. Stryker Corporation

20. Synthes Inc.

21. Zimmer Holding Inc.