Logistics Market by Transportation Mode, Logistics Type, End Use and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

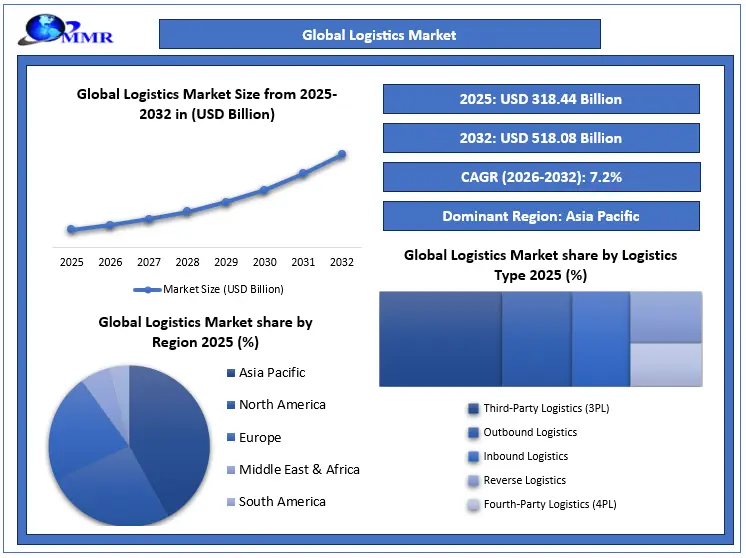

The Global Logistics Market is expected to grow from USD 318.44 Billion in 2025 to USD 518.08 Billion by 2032, at a CAGR of 7.2%, driven by e-commerce expansion, IoT-enabled tracking, automation, AI-driven supply chain management, and smart multimodal transport solutions.

Global Logistics Market Key Highlights:

• E-commerce Growth: Global e-commerce sales surged from USD 4.98 trillion in 2021 to USD 6.86 trillion in 2025, driving demand for last-mile and cross-border logistics.

• Parcel Volume: China leads with over 900 million parcels annually, followed by the USA with 500 million and Germany at 400 million, emphasizing concentrated logistics activity.

• Automation Adoption: 53% of OECD logistics firms use robotics in warehouses, improving operational efficiency and handling over 1.2 million shipments daily in high-volume regions.

• Delivery Efficiency: Average urban delivery time decreased from 2.36 days in 2022 to 2.15 days in 2023, reflecting enhanced performance through micro-fulfilment centers and regional hubs.

• Dominating Region – Asia Pacific: Asia Pacific leads global logistics, handling over 1.8 billion e-commerce parcels annually, driven by China, India, and Southeast Asia’s rapid digital commerce expansion.

• IoT & Digital Logistics: 48% of advanced economy logistics firms leverage IoT tracking, while 67% of cross-border operators utilize digital documentation for predictive delivery and supply chain transparency.

To know about the Research Methodology :- Request Free Sample Report

Logistics Market Trends – Consumer Demand for Faster Last-Mile Delivery

The global logistics market is increasingly shaped by consumer demand for faster last-mile delivery, driven by the surge in e-commerce and urban online shopping. Last-mile deliveries are projected to grow 78% globally by 2030, while delivery vehicles may increase 36% in the 100 busiest cities, contributing up to 13% of urban emissions. Average urban delivery time decreased from 2.36 days (2022) to 2.15 days (2023), reflecting operational responsiveness.

• Micro-fulfilment centres and regional hubs for faster e-commerce logistics.

• KPIs aligned with World Bank LPI to monitor efficiency and consumer satisfaction.

• Collaboration with municipalities to manage congestion and optimize freight and cargo transportation.

• Adoption of green logistics and low-emission vehicles to reduce environmental impact.

Logistics Market Drivers – E-Commerce & Online Shopping Expansion

The global logistics market growth is significantly driven by the rapid expansion of e commerce and online shopping, which increases demand for transportation, warehousing, fulfilment, and last mile delivery services. Global e commerce sales rose from nearly USD 4.98 trillion in 2021 to nearly USD 6.86 trillion in 2025, with forecasts exceeding USD 8 trillion by 2027, reflecting sustained expansion of digital commerce. The number of online shoppers grew from 2.37 billion in 2020 to nearly 2.77 billion in 2025, with online retail accounting for around 21–22.5% of global retail sales by 2025. This structural shift drives higher volumes requiring third party logistics (3PL), enhanced supply chain management, digital logistics, and real time logistics tracking solutions to support cross border fulfilment and delivery optimization.

Logistics Market Opportunities – Technology-Enabled & Personalized Logistics

• Digital Infrastructure Adoption: High-income and 32% of developing countries’ logistics firms leverage cloud-based logistics platforms for real-time shipment visibility and coordination.

• Automation & Robotics: 53% of OECD logistics companies use robotics for warehousing, enhancing operational efficiency and throughput.

• IoT-Enabled Tracking: 48% adoption in advanced economies enables precise cargo monitoring, predictive delivery, and smart logistics solutions.

• Digital Documentation: 67% of cross-border operators implement electronic workflows for streamlined supply chain management.

• Blockchain & AI Integration: 45% exploring blockchain for transparency and AI-driven analytics for predictive insights, creating strategic differentiation.

Logistics Market Restraints – Rising Logistics & Transportation Costs

Rising logistics and transportation costs are constraining the global logistics market, impacting supply chain efficiency, delivery pricing, and consumer satisfaction. In India, total logistics expenditure accounted for 7.97% of GDP in 2024 and 9.09% of non-services output, with freight costs exceeding 80% of total logistics spending. Transport mode costs range from ₹1.96/tonne km (rail) to ₹72/tonne km in air, while labor and warehousing costs add further financial pressures, highlighting the need for smart logistics solutions, automation, and digital logistics platforms.

• Operational Optimization: Optimize multimodal transport for cost, speed, and service, and implement IoT- and AI-enabled supply chain management to enhance efficiency.

• Technology & Sustainability Investment: Invest in automated warehousing, handling technologies, and adopt green logistics solutions for cost-effective and eco-friendly last-mile delivery.

Logistics Market Technology Impact Matrix

| Technology | Warehousing Efficiency | Transportation Visibility | Route Optimization | Coordination & Control | Emissions Management |

| Automation & Robotics | High | Low | Low | Medium | Medium |

| IoT Tracking | Low | High | Medium | Medium | Medium |

| AI-Based Planning | Medium | Medium | High | High | Medium |

| Cloud Platforms | Medium | Medium | Medium | High | Low |

| Green Logistics | Low | Low | Medium | Low | High |

Global Logistics Market Analysis by Segments

The Global Logistics Market segmentation reveals how transportation modes, service types, logistics types, and end use industries drive operational strategy, cost efficiency, and growth forecasts. Asia Pacific dominates volume and segment demand within the global supply chain and logistics market outlook.

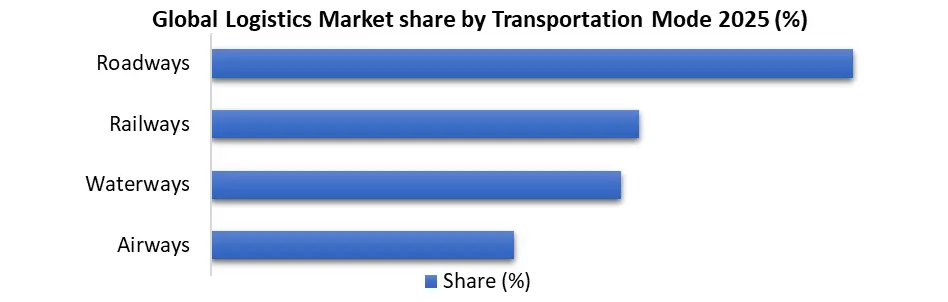

By Transportation Mode: Rail, road, waterways, and air define cost speed trade offs and service reach. In 2025, road and air transport together held nearly 45% share of intermodal freight value, while rail remains cost efficient for bulk freight and essential to multimodal logistics strategies within global supply chains.

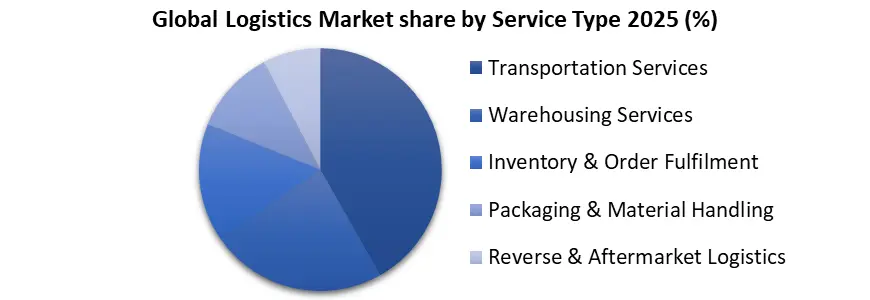

By Service Type: Core logistics functions encompass transportation, warehousing, inventory management, order fulfilment, packaging, material handling, reverse logistics, and solutions that improve delivery performance and supply chain responsiveness across industries.

Logistics Market Regional Insights

The global logistics market is increasingly driven by high-volume parcel flows, with Asia Pacific dominating last-mile delivery and supply chain operations. China leads with over 900 million parcels annually, followed by the USA with 500 million parcels and Germany at 400 million parcels, highlighting concentrated e-commerce logistics activity. This surge underscores demand for digital logistics, IoT-enabled shipment tracking, AI in supply chain management, and smart logistics solutions to improve operational efficiency, predictive delivery, and personalized services. These regions represent strategic hubs for optimizing transportation, warehousing, and third-party logistics capabilities across global supply chains.

• Invest in automation and robotics to manage 1.2 million daily shipments in Europe and 850,000 parcels per day in India, enhancing efficiency.

• Expand cloud-based and IoT-enabled logistics platforms to track 1.8 billion e-commerce parcels across top markets, optimize multi-modal transport, and enable predictive analytics for faster, reliable deliveries.

Logistics Market Competitive Landscape

• Global and regional logistics integrators such as DHL, Kuehne + Nagel, DSV, UPS, and Sinotrans leverage multimodal transportation, cross-border logistics compliance, and digital logistics tracking to serve high-volume international supply chains. North America specialists and emerging regional players focus on last-mile delivery, domestic freight, and e-commerce logistics, optimizing transportation, warehousing, and third-party logistics capabilities.

• Specialized providers such as Lineage Logistics and Americold operate over 120 temperature-controlled warehouses globally, serving 400 million cold chain shipments annually, differentiating through IoT-enabled monitoring, predictive analytics, and AI-driven supply chain management to strengthen last-mile delivery efficiency.

Logistics Market Recent Developments

| Company | Year | Development | Business Implication |

| DHL Group | 2025 | Opened Europe Innovation Center (5,360 m²) for AI, robotics, IoT, sustainability | Strengthens innovation and digital/logistics automation across Europe & global network |

| DHL Group | 2025 | EUR 500 million investment in Middle East logistics (2024–2030) | Enhances express delivery, freight, warehousing & regional trade connectivity |

| Kuehne + Nagel | 2025 | Launched air logistics gateway in Bengaluru, India | Increases cross-border capacity & service reliability for healthcare, tech, and automotive logistics |

| CEVA Logistics | 2026 | Opened eCommerce warehouse in Dubai | Expands regional fulfillment & contract logistics for Middle East e-commerce market |

| CEVA Logistics | 2025 | Tested 100% electric heavy-duty truck in Spain | Advances sustainable logistics and reduces road freight emissions |

Logistics Market Scope: Inquiry Before Buying

| Logistics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 318.44 USD Billion |

| Forecast Period 2026-2032 CAGR: | 7.2% | Market Size in 2032: | 518.07 USD Billion |

| Segments Covered: | By Services | Transportation Services Warehousing and Distribution Services Freight Forwarding Services Inventory Management Services Value-Added Logistics Services Integration & Consulting Services |

|

| By Type | Forward Logistics Reverse Logistics |

||

| By Model | 1PL 2PL 3PL 4PL 5PL |

||

| By Operation | Domestic International |

||

| By Mode of Transport | Railways Airways Roadways Waterways |

||

| By Category | Conventional Logistics E-Commerce Logistics |

||

| By Usage | B2B (Business-to-Business) B2C (Business-to-Consumer) |

||

| By End Use | Healthcare Manufacturing Aerospace Telecommunication Government and Public Utilities Banking and Financial Services Retail |

||

Logistics Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Global Logistics Market Key players:

1) DHL

2) Kuehne + Nagel

3) DSV A/S

4) DB Schenker

5) CEVA Logistics

6) A.P. Moller – Maersk

7) C.H. Robinson Worldwide

8) UPS Supply Chain Solutions

9) Expeditors International

10) Sinotrans Limited

11) GXO Logistics

12) J.B. Hunt Transport Services

13) Rhenus Logistics

14) DACHSER

15) DP World Logistics

16) Ryder Supply Chain Solutions

17) Nippon Express

18) Kintetsu World Express

19) CJ Logistics

20) Lineage Logistics

21) Delhivery

22) Blue Dart Express

23) Mahindra Logistics

24) Allcargo Logistics

25) Safexpress

26) Gati-Kintetsu Express

27) Hellmann Worldwide Logistics

28) Penske Logistics

29) Americold Logistics

30) Imperial Logistics

FAQs of Global Logistics Market:

Q1: What is driving the growth of the global logistics market?

A1: The growth is driven by e-commerce expansion, IoT-enabled tracking, automation, AI-driven supply chain management, and smart multimodal transport solutions.

Q2: Which region dominates the global logistics market?

A2: Asia Pacific dominates, handling over 1.8 billion e-commerce parcels annually, led by China, India, and Southeast Asia.

Q3: How is technology transforming logistics operations?

A3: Adoption of robotics, IoT-enabled tracking, cloud platforms, and AI enhances operational efficiency, predictive delivery, and supply chain transparency.

Q4: What are the main challenges in logistics?

A4: Rising transportation, labor, and warehousing costs, along with freight expenditure exceeding 80% of logistics spending, constrain efficiency and pricing.

Q5: What are the major opportunities in the logistics market?

A5: Opportunities include cloud-based platforms, automation & robotics, IoT-enabled tracking, digital documentation, blockchain, and AI-driven predictive analytics for supply chain optimization.