Lightweight Materials Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2034

Overview

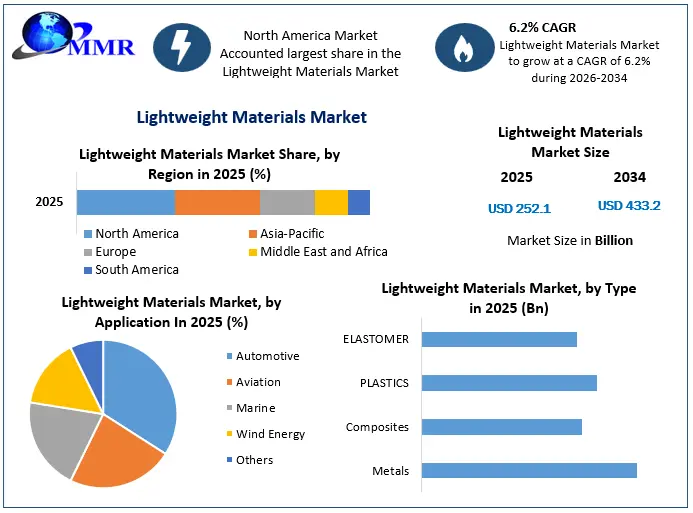

Lightweight Materials Market size was valued at USD 252.1 Bn. in 2025 and the total Lightweight Materials revenue is expected to grow at a CAGR of 6.2% from 2026 to 2034, reaching nearly USD 433.2 Bn.

Lightweight Materials Market Overview:

Lightweight materials are metal alloys and composites that are used to reduce the weight of automobiles, airplanes, and windmills while maintaining structural strength and efficiency. Lightweight materials offer a high strength-to-weight ratio, strong corrosion resistance, and greater design flexibility.

The increasing adoption of electric vehicles (EVs) to minimize hazardous air pollution is driving the growth of the lightweight materials industry. In addition, the growing utilization of lightweight materials in the wind energy industry for manufacturing windmills is positively impacting market growth across the world. Besides that, the growing use of lightweight materials in the aviation industry to reduce fuel consumption provides attractive growth opportunities for Lightweight materials industry investors. Likewise, the usage of aluminum alloys in the food and beverage (F&B) sector for the production of foils, beverage cans, and cooking and food processing tools is rapidly increasing. As a result, these factors increase the demand for lightweight materials market in Food and beverage industry.

The implementation of emission-reduction legislation in both developed and developing countries has increased the adoption of lightweight materials across various industries, due to their capacity to lower emissions by 20-30%. This factor is expected to increase the demand for lightweight materials during the forecast period. Besides that, increased awareness of renewable energy sources has increased the windmills plants, where lightweight materials-based wind turbines are frequently used due to their lower overall weight and improved system efficiency. This helps the lightweight materials industry to thrive in the increasing renewable energy sector.

A large number of automotive manufacturers are switching to products that reduce the weight of the vehicles owing to the increased awareness pertaining to fuel emissions, which in turn is anticipated to drive the global market. The increased demand for vehicles in North America is expected to augment the market growth over the forecast period. The growth in this region is driven on account of the strong presence of major auto manufacturers in countries such as the U.S. and Canada. Furthermore, the presence of renewable energy equipment manufacturers is expected to drive the lightweight materials market in this region.

Lightweight Materials Market Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Lightweight Materials Market Dynamics:

Increasing penetration of lightweight components

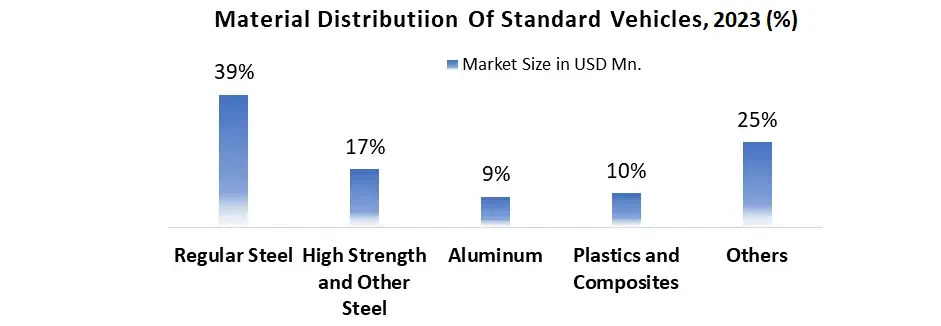

Lightweight materials have several advantageous qualities such as high tensile strength and increased design flexibility, making them a favored alternative for producers that produce different automotive components such as door modules, chassis, and bumper beams. These vehicle interior and exterior components are not only used by OEMs (original equipment manufacturers) but also have a high volumetric demand in the global market. Passenger vehicles are one of the main segments in the automotive industry, accounting for two-thirds of all vehicles produced. Lightweight materials (regular steel, high-strength steel, plastics, and composites) account for 75% of standard vehicle material distribution, making automotive the largest application category of the global lightweight materials market.

Trends toward achieving environmental sustainability through the reduction of carbon dioxide (CO2) emissions from vehicles are encouraged by various governmental and nongovernmental organizations globally. For example, as of 2016, the fuel efficiency benchmark in the United States for fleet-wide average is set at 33.3 MPG, with similar trends being followed in Mexico, Canada, and other European countries. This is placing OEMs under pressure to enhance the overall fuel economy of cars, which includes adopting lightweight components to lower overall curb weight. An increase in automotive production, stringent government norms for emission control, and increasing penetration of lightweight materials are expected to drive the demand for lightweight materials and drive the lightweight materials market revenue during the forecast period.

Additionally, it is observed that using lightweight components in the vehicle will not be able to match the CO2 emissions target alone, pushing hybrid and electric vehicles in the market to contribute to fulfilling the regulations. Electric and hybrid vehicle production is expected to grow to 11 million units by the end of the forecast period, up from 3.5 million units in 2016. This is attributed to unfolding the multiple opportunities for stakeholders across the lightweight material market value chain.

Stringent emission and fuel economy regulations

Stringent emission and fuel economy regulations

Governments across the world have introduced stringent emission and fuel economy regulations for vehicles. These requirements have driven manufacturers to utilize more lightweight materials, such as lightweight metals, composites, and polymers. Advanced lightweight materials improve a vehicle's fuel efficiency while maintaining safety and performance. A 10% decrease in vehicle mass can increase fuel economy by 6 to 8%. The use of lightweight materials reduces fuel consumption in a vehicle because less weight requires less energy to accelerate.

Engine components can withstand high pressure and temperature with the use of advanced materials, which in turn helps increase efficiency and lowers emissions. The multi-material designs use a system of approach that keeps the best features of materials at an appropriate position by combining HSS, magnesium, composites, aluminum, and other materials. Lightweighting can be achieved by efficient design, material selection, production, and assembly.

High cost of carbon fiber

The automotive industry is the dominant end-user of lightweight materials and the industry is continuously investigating every possible solution to reduce the overall weight of the vehicle. Although carbon fiber is one of the potential materials for the manufacture of automotive components, it is not widely used owing to its expensive cost, which affects the entire cost of the finished product. In addition to the substantial cost, additional constraints that restrict the utilization of carbon fiber include the high cost of maintenance and repairs, as well as recycling. As of 2016, only premium and luxury category cars have more carbon fiber components, although production of midrange vehicles is higher, which do not utilize as many carbon fiber components owing to the high cost. This is the major restraining factor for the lightweight materials market growth.

Fluctuating prices of highly traded commodities

Aluminum, steel, and other lightweight materials are hot commodities with volatile pricing. However, as of 2016, steel accounts for around half of the total material distribution of a conventional automobile. Due to increased competition from high-strength steel and composite materials, this share is expected to decrease. However, by the end of the forecast period, next-generation cars such as electric and hybrid vehicles are expected to account for around 22% to 25% of global automotive manufacturing. This is directly related to the rising share of aluminum and other sophisticated composite materials in comparison to steel. Reserves for these metals are declining in some places, causing final product costs to rise while threatening the capacity to satisfy obligations. Material price inflation, smaller pricing margins, long-term fixed price contracts, and commodity hedging may have an adverse effect on the players involved in the lightweight material value chain. As a result, these factors restrict the lightweight materials market growth.

Lightweight Materials Market Segment Analysis:

Based on Application, the automotive segment held the largest market share of about 35% and dominated the Lightweight Materials market in 2025. The segment is further expected to grow at a CAGR of about 6.1% throughout the forecast period. The growth of lightweight material in the automotive industry is attributed to industrialization, rising living standards, new product development, and growing penetration of electric vehicles, especially in emerging countries. Additionally, growing concern about gas emissions has resulted in the increased use of lightweight components such as high-strength steel, aluminum, and composites, which add efficiency to vehicles, reduce CO2 emissions, and increase automotive efficiency when compared to heavier cars. As a result, fuel consumption is reduced by 6-8% and acceleration requires less power than in larger vehicles.

The aviation segment is expected to hold a high share of about 30% in the Lightweight Materials market during the forecast period. Airframes, overhead bins, lavatory interiors, passenger doors, and cargo doors are among the aircraft components made from lightweight materials. A standard aircraft contains approximately 70% to 80% lightweight materials, and aircraft manufacturers are investing in every possible space to increase the usage of lightweight materials in the construction of the components to improve fuel efficiency, reduce related costs, and increase passenger/cargo load per flight. Aluminum is currently the most common material used in different structural sections such as airframes and door frames, accounting for around 40%-50% of the total material utilized. One of the global lightweight materials market trends is the rising usage of composite structures, which is gaining substantial pace.

The aviation segment is expected to hold a high share of about 30% in the Lightweight Materials market during the forecast period. Airframes, overhead bins, lavatory interiors, passenger doors, and cargo doors are among the aircraft components made from lightweight materials. A standard aircraft contains approximately 70% to 80% lightweight materials, and aircraft manufacturers are investing in every possible space to increase the usage of lightweight materials in the construction of the components to improve fuel efficiency, reduce related costs, and increase passenger/cargo load per flight. Aluminum is currently the most common material used in different structural sections such as airframes and door frames, accounting for around 40%-50% of the total material utilized. One of the global lightweight materials market trends is the rising usage of composite structures, which is gaining substantial pace.

The composite structure has several advantages over traditional lightweight materials, including lower fatigue and corrosion risk, superior aesthetic and aerodynamic finish, and greater design freedom. Recent examples are the Boeing 787 Dreamliner and the Airbus A340, both of which utilized advanced composite materials instead of conventional materials to lower total aircraft weight. Additionally, components constructed of composite materials require less maintenance than non-composite ones. A thriving retrofit industry, an increasing number of aircraft orders, rising fuel prices, and stringent regulations are all expected to contribute to increased demand for composites and other lightweight materials during the forecast period.

The Windmill segment is expected to grow at a CAGR of 5.2% and hold a significant share at the end of the forecast period. A growing number of wind energy power plants all across the world is expected to contribute significantly to the growth of the lightweight materials industry. Wind energy is the leading conventional energy source in North America and Europe, with China dominating the capacity addition competition. A rise in wind power investments for capacity increases and new projects around the world is driving up demand for windmills, which is connected to an increase in demand for lightweight materials during the forecast period.

The Windmill segment is expected to grow at a CAGR of 5.2% and hold a significant share at the end of the forecast period. A growing number of wind energy power plants all across the world is expected to contribute significantly to the growth of the lightweight materials industry. Wind energy is the leading conventional energy source in North America and Europe, with China dominating the capacity addition competition. A rise in wind power investments for capacity increases and new projects around the world is driving up demand for windmills, which is connected to an increase in demand for lightweight materials during the forecast period.

Lightweight materials are also utilized in the production of various products, including mountain bikes and hiking equipment. This is gaining popularity in developing countries and is expected to increase the demand for lightweight materials during the forecast period. Besides that, the massive growth of the manufacturing base in various developing economies such as India, China, and Brazil, which is also experiencing an expansion in the customer landscape as a demographic dividend, is expected to play a significant role in the growth of the lightweight materials market.

Lightweight Materials Market Regional Insights:

The global lightweight materials market has grown significantly in recent years as a result of stringent government CO2 emission control rules and a rising preference among automotive manufacturers for lightweight vehicles. Increasing global car production, rapid increase in the industrial base, changing demographics, and a good global economic outlook are just a few of the important factors driving the global lightweight materials market.

North America is one of the leading automotive industries, and it is expected to drive the lightweight material market during the forecast period. The region has enacted severe government initiatives to reduce CO2 emissions. The United States announced corporate average fuel economy (CAFE) guidelines in 2012, with an average requirement of 54.5 miles per gallon of gasoline from 2017 to 2025. Investment in new car manufacturing in Mexico is also increasing, with capacity set to increase by 50% over the next five years. Aerospace manufacturing provides for a significant portion of the US economy, accounting for around 1.4% of GDP. Meanwhile, the replacement of aging aircraft with lightweight, fuel-efficient aircraft, together with military aircraft inventions and advances, is expected to increase the North American lightweight materials market during the forecast period.

The Asia-Pacific regional lightweight materials market is expected to grow at a CAGR of about 5.4% during the forecast period. The rising demand for fuel-efficient heavy commercial vehicles and huge investments made by manufacturers in the R&D process in the region are some of the major factors driving the growth of the Asia-Pacific lightweight materials market during the forecast period. The increasing adoption of electric vehicles in emerging markets such as India, Thailand, China, and Indonesia, is positively impacting the regional industry growth. China is the Asia Pacific region's largest market for electric cars. Rising income levels increased worries about fuel pollution, and government plans to increase electric auto manufacturing are expected to drive the Chinese demand for electric vehicles even higher during the forecast period.

The Asia-Pacific regional lightweight materials market is expected to grow at a CAGR of about 5.4% during the forecast period. The rising demand for fuel-efficient heavy commercial vehicles and huge investments made by manufacturers in the R&D process in the region are some of the major factors driving the growth of the Asia-Pacific lightweight materials market during the forecast period. The increasing adoption of electric vehicles in emerging markets such as India, Thailand, China, and Indonesia, is positively impacting the regional industry growth. China is the Asia Pacific region's largest market for electric cars. Rising income levels increased worries about fuel pollution, and government plans to increase electric auto manufacturing are expected to drive the Chinese demand for electric vehicles even higher during the forecast period.

Rising foreign direct investment in the automotive industry is increasing revenue in the region. The fast-growing automotive industries in Japan, South Korea, and Vietnam, as well as rising consumer demand for lightweight and fuel-efficient automobiles, are expected to increase the Asia Pacific market size during the forecast period. Foreign investment is expected to be driven by favorable labor regulations and low labor costs. Stringent fuel pollution laws in the Asia Pacific are expected to continue to force firms to create and manufacture lightweight vehicles. These factors further enhance the industry's revenue growth.

MEA is expected to be the fastest-growing region for the lightweight materials market during the forecast period. Rapid industrialization and the establishment of manufacturing facilities by major conglomerates such as Cytec Solvay Group are driving growth in this region. The ease of access to natural resources, along with the rising application industry, is expected to increase market demand. Additionally, market demand in Latin America is rapidly increasing due to a rise in the number of manufacturers of lightweight materials. Likewise, the presence of aviation and wind energy equipment manufacturers in Europe is expected to increase European lightweight materials market growth.

Lightweight Materials Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 15 January 2025 | Toray Industries, Inc. | Launched a new high-modulus carbon fiber series optimized for next-generation electric vehicle (EV) chassis components. | Enables a 15% weight reduction in vehicle structures while significantly improving crash safety performance. |

| 22 February 2025 | ArcelorMittal | Commissioned a new green steel production facility specifically for automotive-grade advanced high-strength steel (AHSS). | Supplies low-carbon materials to European automakers to meet strict emission reduction compliance standards. |

| 10 March 2026 | BASF SE | Entered a strategic partnership to supply bio-based engineering plastics for lightweight interior aircraft modules. | Reduces cabin weight by 8%, directly improving fuel efficiency and sustainability for commercial aviation. |

| 05 May 2026 | Novelis Inc. | Opened a state-of-the-art aluminum recycling center focused on closed-loop automotive sheet supply. | Increases circularity by processing 300,000 tons of scrap aluminum annually with 95% lower energy usage. |

Lightweight Materials Market Scope: Inquire before buying

| Lightweight Materials Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | US $ 252.1 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 6.2% | Market Size in 2034: | US $ 433.2 Bn. |

| Segments Covered: | by Type | Metals Aluminum High Strength Steel Magnesium Titanium Composites Carbon-fiber reinforced plastic (CFRP) Glass-fiber reinforced plastic (GFRP) Natural Fibre-Reinforced Polymer (NFRP) Others PLASTICS PC ABS PA PP PU Others ELASTOMER EPDM NR SBR Others |

|

| by Application | Automotive Aviation Marine Wind Energy Others (Transportation, Packaging, and Other Engineered Goods) |

||

Lightweight Materials Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Lightweight Materials Market Key Players

1. Alcoa Corporation

2. ArcelorMittal

3. BASF SE

4. Covestro AG

5. DuPont de Nemours, Inc.

6. Hexcel Corporation

7. Novelis Inc.

8. Owens Corning

9. Solvay S.A.

10. Toray Industries, Inc.

11. Mitsubishi Chemical Group Corporation

12. Teijin Limited

13. SGL Carbon

14. Royal DSM

15. TATA Steel

16. Constellium SE

17. Rio Tinto

18. Norsk Hydro ASA

19. UACJ Corporation

20. POSCO Holdings

21. General Electric

22. Boeing

23. Airbus SE

24. Hexagon Composites ASA

25. Toray Composite Materials America, Inc.

26. Aditya Birla Group

27. Saudi Basic Industries Corporation (SABIC)

28. Evonik Industries AG

29. Cytec Solvay Group

30. Toyota Motor Corporation

Frequently Asked Questions:

1. What are the growth drivers for the Lightweight Materials market?

Ans. The increasing adoption of electric vehicles (EVs) to minimize hazardous air pollution, the growing utilization of lightweight materials in the wind energy industry for manufacturing windmills, and the growing use of lightweight materials in the aviation industry to reduce fuel consumption, are expected to be the major driver for the Lightweight Materials market.

2. What is the major restraint for the Lightweight Materials market growth?

Ans. The High cost of carbon fiber and Fluctuating prices of highly traded commodities are expected to be the major restraining factor for the Lightweight Materials market growth.

3. Which region is expected to lead the global Lightweight Materials market during the forecast period?

Ans. The North American market is expected to lead the global Lightweight Materials market during the forecast period due to the Increasing global car production, rapid increase in the industrial base, changing demographics, government initiatives to reduce CO2 emissions, and Investment in new car manufacturing in Mexico.

4. What is the projected market size & growth rate of the Lightweight Materials Market?

Ans. Lightweight Materials Market size was valued at USD 252.1 Bn. in 2025 and the total Lightweight Materials revenue is expected to grow at a CAGR of 6.2% from 2026 to 2034, reaching nearly USD 433.2 Bn.

5. What segments are covered in the Lightweight Materials Market report?

Ans. The segments covered in the Lightweight Materials market report are Type, Application, and Region.