Industrial Gases Market Size by Type, End Use Industry and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

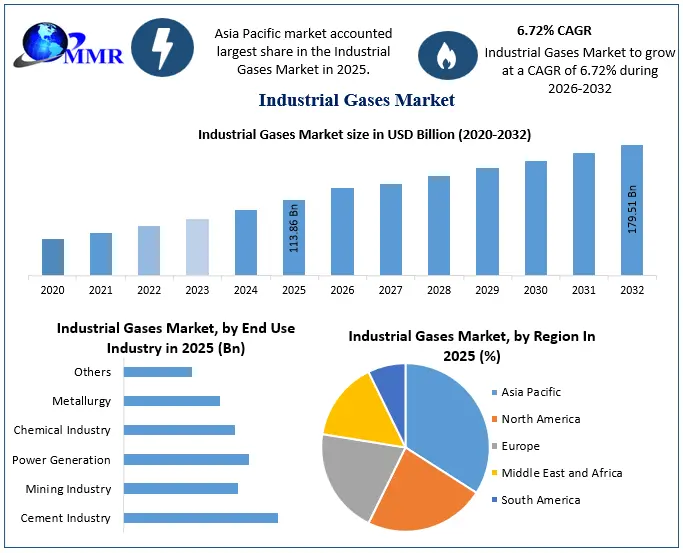

The Industrial Gases Market size was valued at USD 113.86 Billion in 2025 and the total ABC revenue is expected to grow at a CAGR of 6.72% from 2026 to 2032, reaching nearly USD 179.51 Billion.

To know about the Research Methodology :- Request Free Sample Report

Industrial Gases Market Dynamics:

Expanding Industrial Manufacturing and Healthcare Sectors Drive Market Growth

The growing demand from manufacturing industries, including steel, chemicals, electronics, food & beverage, and healthcare, is a major factor driving the global Industrial Gases Market. Industrial gases such as oxygen, nitrogen, hydrogen, argon, and carbon dioxide are indispensable for metal fabrication, chemical processing, semiconductor manufacturing, medical treatments, food preservation, and pharmaceutical production. Rapid industrialization, increasing healthcare expenditure, expanding hospital infrastructure, and rising demand for high-purity gases in electronics manufacturing are further accelerating market growth. In addition, the transition toward cleaner industrial processes and increasing adoption of hydrogen in energy applications continue to strengthen market demand.

High Energy Costs and Supply Chain Volatility Restrain Market Expansion

Despite robust growth prospects, the market faces challenges due to the energy-intensive nature of industrial gas production. Fluctuations in electricity and natural gas prices significantly impact manufacturing costs, particularly for cryogenic air separation and hydrogen production processes. Furthermore, supply chain disruptions, transportation costs, and stringent environmental regulations related to carbon emissions increase operational complexities for manufacturers. These factors can affect profitability and limit capacity expansion, especially in regions with volatile energy markets.

Growth in Clean Hydrogen, Carbon Capture, and Electronics Manufacturing Creates New Opportunities

The increasing focus on clean hydrogen, carbon capture, utilization and storage (CCUS), and sustainable industrial operations is creating significant opportunities for the global Industrial Gases Market. Governments and private companies are investing in hydrogen production, renewable energy integration, and low-carbon industrial infrastructure to support decarbonization goals. At the same time, the rapid expansion of semiconductor manufacturing, electric vehicle battery production, and advanced electronics is driving demand for ultra-high-purity industrial gases. Continuous advancements in air separation technologies, on-site gas generation systems, and digital monitoring solutions are expected to further improve production efficiency and support long-term market growth

Industrial Gases Market Trends:

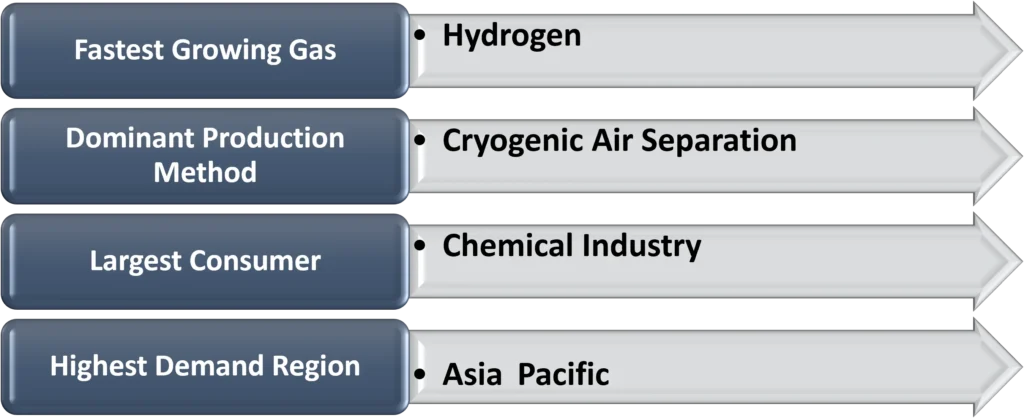

- Growing investments in clean hydrogen production: Governments and industrial gas companies are increasing investments in green hydrogen and blue hydrogen projects to support decarbonization initiatives across the energy, transportation, and manufacturing sectors. Hydrogen is emerging as a key industrial gas for low-carbon industrial processes and clean energy applications.

- Expansion of semiconductor and electronics manufacturing: The rapid growth of semiconductor fabrication, consumer electronics, and electric vehicle production is driving demand for ultra-high-purity nitrogen, argon, helium, and specialty gases. Increasing investments in advanced chip manufacturing facilities are further supporting market expansion.

- Rising adoption of on-site gas generation systems: Industries are increasingly deploying on-site oxygen and nitrogen generation systems to improve supply reliability, reduce transportation costs, and enhance operational efficiency. This trend is particularly strong in healthcare, food processing, chemicals, and metal fabrication industries.

- Increasing focus on carbon capture, utilization, and storage (CCUS): Industrial gas manufacturers are investing in carbon capture technologies and CO₂ recovery systems to help industries reduce greenhouse gas emissions and comply with stringent environmental regulations. The integration of CCUS with industrial gas production is becoming an important sustainability strategy.

- Technological advancements in air separation and digitalization: Companies are implementing advanced cryogenic air separation technologies, automation, IoT-enabled monitoring systems, and predictive maintenance solutions to optimize gas production, improve energy efficiency, and minimize operational downtime.

- Strategic capacity expansions and long-term supply agreements: Leading industrial gas companies are expanding production facilities and entering long-term supply contracts with steel manufacturers, chemical producers, semiconductor fabs, and healthcare providers to ensure stable gas supply and strengthen their global market presence.

Industrial Gases Market:Quick Snapshot

Global Industrial Gases Market Scope: Inquire before buyin

| Global Industrial Gases Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 113.86 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 6.72% | Market Size in 2032: | USD 179.51 Bn. |

| Segments Covered: | By Gas Type | Oxygen Carbon Dioxide Nitrogen Hydrogen Noble Gas Helium Argon Others (Neon, Krypton, Xenon, and Radon) |

|

| By Production Process | Cryogenic Air Separation Non-Cryogenic Air Separation Steam Methane Reforming (SMR) Electrolysis Others |

||

| By Distribution Mode | Merchant (Bulk & Cylinder) Tonnage (On-site Supply) Packaged Gases |

||

| By End Use Industry | Cement Industry Mining Industry Power Generation Chemical Industry Metallurgy Others |

||

Industrial Gases Market, by region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Leading Industrial Gases Market, Key Players:

The competitive landscape of the industrial gases industry is characterized by established Industry leaders, emerging players, and new entrants. Leading companies in the Industrial Gases industry such as Air Liquide, Linde, and Praxair dominate the Industry, leveraging their extensive distribution networks, advanced technologies, and comprehensive product portfolios. Air Liquide’s focus on innovation and sustainability has solidified its position, while Linde’s strategic mergers and acquisitions have enhanced its global reach. Praxair, now part of Linde, has maintained a strong foothold through its customer-centric approach and operational efficiency. Industry followers, including Messer Group and Air Products, are capitalizing on niche segments and regional industries, often offering competitive pricing and tailored solutions. New entrants, driven by technological advancements and a growing emphasis on eco-friendly solutions, are challenging established players by introducing innovative products and services. The presence of these new competitors has prompted leaders to enhance their R&D investments and diversify offerings to maintain their Industry share. The industrial gases Industry is dynamic, with leaders focusing on innovation and sustainability, followers leveraging local insights, and new entrants disrupting traditional models, thereby fostering a competitive environment that drives growth and adaptation.

1. AGA AB

2. Airgas

3. Air Liquide

4. Air Products and Chemicals

5. BASF SE

6. BOC

7. Gulf Cryo

8. The Linde Group

9. Messer Group

10. MOX-Linde Gases

11. Praxair

12. Nippon Gases

13. Matheson Tri-Gas

14. Rotarex

15. Universal Industrial Gases

16. Dubai Industrial Gases

17. Bristol Gases

18. INOX-Air Products Inc.

19. Iwatani Corp.

20. SOL Group

FAQs:

1. What are the growth drivers for the Industrial Gases market?

Ans. The rising demand from manufacturing industries, advancements in technology, and increased use in healthcare and energy sectors are expected to be the major drivers for the Industrial Gases market.

2. What are the factors restraining the global Industrial Gases market growth during the forecast period?

Ans. The high operational costs, regulatory challenges, and fluctuating raw material prices are expected to be the major factors restraining the global Industrial Gases market growth during the forecast period.

3. Which region is expected to lead the global Industrial Gases market during the forecast period?

Ans. Asia Pacific is expected to lead the global Industrial Gases market during the forecast period.

4. What was the Global Industrial Gases Market size in 2025?

Ans: The Global Industrial Gases Market size was USD 113.86 Billion in 2025.

5. What segments are covered in the Industrial Gases Market report?

Ans. The segments covered in the Industrial Gases market report are Type, End-use Industry, and Region.