Data Center Market - Industry Structure Evaluation, Demand Drivers Analysis, Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2032

Overview

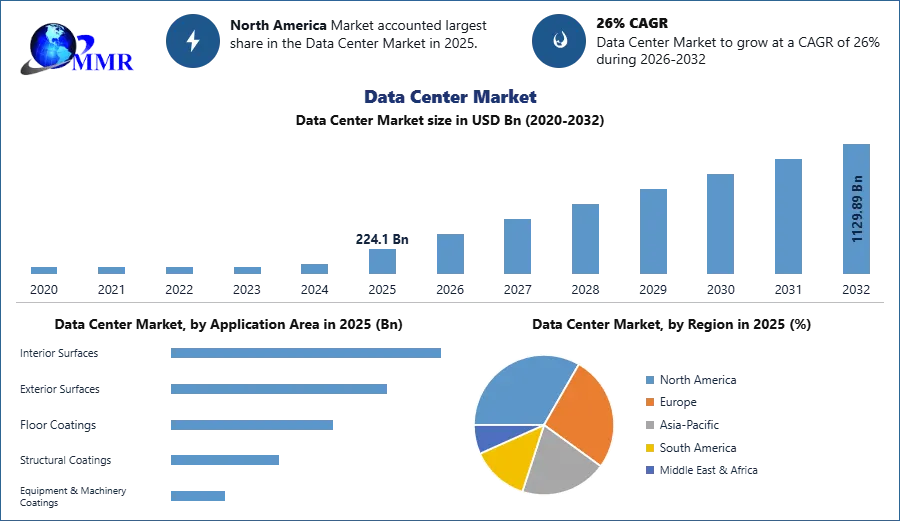

The Data Center Market size was valued at USD 224.10 Billion in 2025 and the total Data Center revenue is expected to grow at a CAGR of 26% from 2025 to 2032, reaching nearly USD 1129.91 Billion by 2032.

Data Center Market Overview:

Data Center is a physical facility used to house the critical application and data that organizations implement. The design of the data center is based on a network of computing and storage resources that enable the delivery of shared applications and data. Routers, switches, firewalls, storage systems, servers, and application delivery controllers are key components of data center design. Organizations are outsourcing their data operations to third-party providers that specialize in data center operations.

To know about the Research Methodology :- Request Free Sample Report

Data Center Market Dynamics:

In the data center market, more extensive capacity markets benefit from established connections with local governments and utilities throughout the planning, approval, construction, and power provisioning stages of new data center developments. This measure serves as an indicator of one aspect of the relative risk profile of a market, with larger data center markets indicating lower risk, while smaller, emerging data center markets tend to present higher risk. The substantial size of larger data center markets also guarantees the presence of on-site staff, sales teams, and other essential human capital to facilitate upcoming data center developments. As a result, the most significant data center markets are strategically positioned for sustained growth, at least until potential challenges arise, such as capacity strain on the local power grid or shifts in political imperatives.

Over the past decade, the data center market has witnessed a substantial influx of over $100 billion, attracting investment from various entities such as pension funds, private equity firms, infrastructure funds, and sovereign wealth organizations. Recognizing the data center market's growth potential, these diverse entities have facilitated the industry's expansion more economically, often taking ownership positions in new companies instead of acquiring data centers asset by asset. This investment approach has proven highly advantageous for the data center market, with these organizations expressing intent to deploy similar capital amounts if appealing opportunities arise.

Simultaneously, a significant technological shift has unfolded, with enterprises opting to move workloads off-premises initially to colocation facilities and more recently to a blend of colocation, public, and private cloud computing. This transition has elevated major cloud platform providers to crucial roles in various data center markets, signing increasingly substantial leases that have reshaped data center sizing, rendering a 10-megawatt (MW) data center, once impressive, significantly smaller than the now more common 30 MW leases. As cloud computing has given rise to extensive data center campuses, the demand for edge computing has emerged from end-user needs. Factors such as IoT devices, imminent 5G wireless networks, and the potential for self-driving vehicles necessitate substantial infrastructure investment, particularly in densely populated urban areas. Industry leaders in the data center market are strategically constructing platforms capable of supporting a wide spectrum of use cases, recognizing the crucial importance of minimizing latency for the optimal functionality of these new applications.

Valuations Insights

Investors in the data center market maintain their strategic focus on top-tier data centers, emphasizing attributes such as robust tenancy, substantial remaining lease terms, and the capability to meet evolving customer demands for optimal connectivity, cloud on-ramps, and density. This targeted emphasis is expected to persist amid the current economic landscape marked by rising inflation and interest rates. However, the limited sales activity observed during H1 poses challenges in determining the average cap rate movement and the precise impact of escalating interest rates and inflation on asset pricing.

Various factors, including supply chain disruptions, inflationary pressures, and supply-and-demand dynamics, are exerting influence on the underwriting assumptions for rental rates and concessions. This has led to increased scrutiny of non-recurring costs and rental rates in specific markets. The evaluation of vacant and second-generation enterprise data center valuations has become more intricate, with heightened importance placed on physical attributes and market fundamentals at the time of sale. Considerations such as speed-to-market and power availability are crucial in this assessment. Enterprise facilities designed for specific purposes, with limited regard for their appeal in the second-generation market, often trade at a notable discount to replacement cost. However, assets with higher capacity or fiber-rich networks can effectively mitigate this discount to replacement cost.

The Rise of XaaS

The escalating demand for "Everything as a Service" (XaaS) has a profound impact on data centers, manifesting in an extraordinary 42% year-over-year surge in H1 2022. This substantial growth is intricately linked to the persistent adoption of hybrid work models, where the diversity of cloud-based tools and technologies plays a critical role. As companies increasingly embrace virtual collaboration and flexible work-from-anywhere models, the robust demand for "Software as a Service" (SaaS) applications is anticipated to endure. The data center landscape, with its capacity to provide the infrastructure backbone for seamless XaaS delivery, becomes pivotal in accommodating the evolving demands of modern work environments. The 2021 survey, revealing that companies are leveraging over 100 distinct SaaS applications on average, signifies a 38% increase from 2020 figures, reinforcing the data center market's central role in supporting the transformative shift toward XaaS solutions.

Data Center Market Segment Analysis

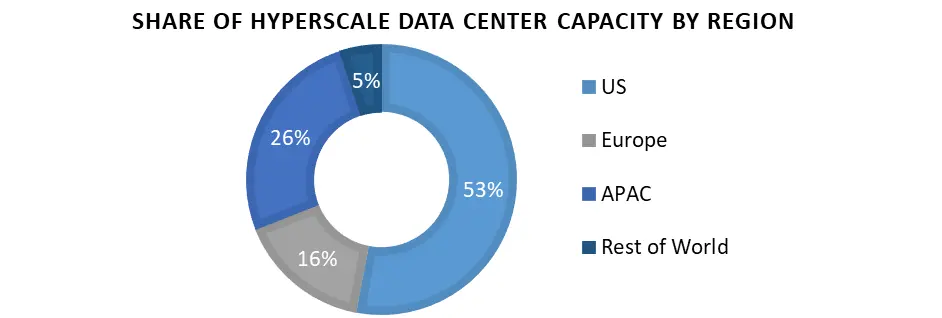

By Type, Hyperscale data center dominated the market with a 40 % share in 2025. Maximizing cooling efficiency, balanced workload, and automated facility are the major factors driving the growth of the market. Reducing the cost of data interruptions, minimizing downtime due to excessive demands, etc., ability to scale up when demand is great and scale down when demand is low are factors. Hyperscale data center offers a wide array of applications in various industries, namely IT & telecom, BFSI, government utilities, healthcare, energy, manufacturing, and others. The cloud segment is expected to grow at a CAGR of 5.4 % through the forecast period. The emerging cloud technology is driving market growth. It is more flexible because it can be accessed with different devices and it is easy to recover the lost data and high speed, which helps the other businesses to grow.

By Application, the BFSI sector dominated the market with a 26% share in 2025. It has become the backbone of the BFSI sector. It provides IT Service Management (ITSM) that manages the IT tools and applications, inventory, service lifecycle, and monitoring performance, of all assets in the DC; Datacenter Facility Management (DCFM), managing the Interdependent electrical network along with HVAC, UPS's, DGSET's, Rack's, iPDU's, etc. effortlessly.

IT & Telecom is expected to grow at a CAGR of 7 % through the CAGR period. Modern data centers have become a crucial part of the IT infrastructure. Storage, data centers are being designed to cover the demands of the clientele. It is important to re-architect the traditional data center infrastructure because any form of interruption in a data center can lead to a tremendous loss for the constitution of an organization. These factors are expected to drive the market growth through the forecast period.

By Deployment, On-Premise dominated the market with a 56.4% share in 2025. On-premises captures data from sensors across the data center infrastructure. An on-premises solution offers consistent and secure data collection, reporting, and alerting for an individual environment. The data gives administrators information related to infrastructure availability, airflow, power consumption, temperature, humidity, and security. These are the factors driving the market growth of the segment. Flexibility, Accessibility with different devices, unlimited computing power, lower IT expenditure, and easy access to data and application are the factors expected to drive the market growth through the forecast period.

Data Center Market Regional Analysis

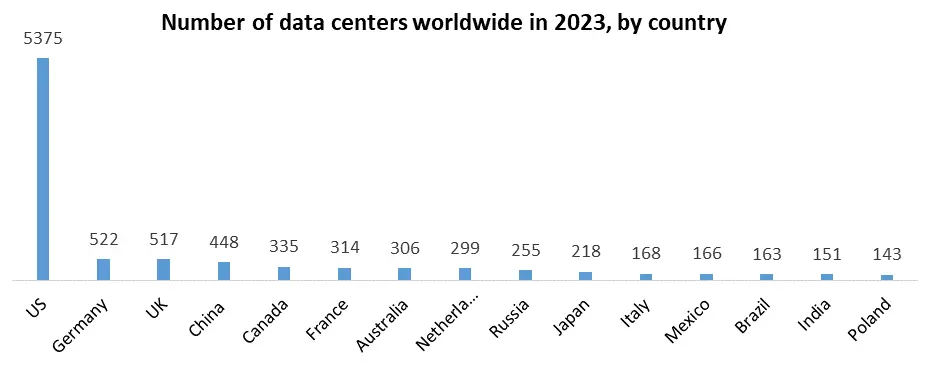

North America Dominated the data center market with a 35 % share in 2025. Owing to the huge presence of leading modular data center providers and the flourishing IT & telecom industry and surge in investments by key players as well as the government for developing the innovative are key factors for the growth of the data center market in this region. The increasing adoption of cloud services by enterprises across industries in the US and Canada will facilitate the data center market growth in North America over the forecast period.

In 2025, the well-established core data center markets in North America grappled with escalating pressures stemming from constrained power and land resources. Northern Virginia, recognized as the world's largest data center market, faced an unprecedented multi-year pause on development in specific submarkets. This hiatus was initiated to allow utility companies to address the challenges posed by an extensive development pipeline. Consequently, there has been a noticeable surge in interest directed towards secondary markets like Portland, Phoenix, Columbus, and various Canadian markets within the data center market landscape. Operators are actively seeking larger sites endowed with cost-effective power solutions in response to these emerging constraints in the data center market. While more established markets like Northern Virginia, Silicon Valley, Chicago, Dallas, and Atlanta continue to exhibit robust momentum, attention is increasingly shifting towards untapped submarkets where the availability of land and power resources appears to be more feasible in the data center market.

Asia Pacific is expected to grow at a GAGR of 6.7 % through the forecast period. Extensive development of 5G network infrastructure in the region and rise in the number of start-ups in the developing economies such as India, China, and South Korea are contributing the market growth. Major factors contributing to the market growth are rapid development in the banking sector of the major economies and growing demand for cloud service from small-, medium-, and large-segment enterprises and increased adoption of data center architecture and technologies.

Data Center Market Competitive Landscape

In the first half of 2022, the data center market in key U.S. regions, encompassing Northern Virginia, Dallas, Silicon Valley, Chicago, Phoenix, New York Tri-State, and Atlanta, witnessed a substantial surge, recording 453.4 megawatts (MW) of positive net absorption—more than triple the levels observed in H1 2021. The total inventory across these primary data center markets saw remarkable year-over-year growth, reaching 3,711.0 MW, indicating the sector's robust expansion. Construction activities were particularly pronounced, with over 1,600 MW under development, surpassing the previous year's figures and with Northern Virginia contributing significantly to this growth. Data center user requirements exhibited notable expansion, with leases for more than 60 MW, some exceeding 100 MW. The overall vacancy rate hit a record low of 3.8%, with Silicon Valley registering a nationwide-low at 1.3%. The surge in preleasing activity was fueled by concerns about potential supply chain disruptions, prompting hyperscalers to proactively secure space for planned growth over the next five years.

Additionally, the average monthly asking rate for a 250- to 500-kW requirement increased by 5.9% year-over-year to $127.50 per kW, underscoring the market's vitality. With the escalating demand from hyperscale entities, the data center industry expects an increase in partial-interest trades, forward sales of new constructions, and sale-leasebacks, driven by rising interest rates and enterprises seeking capital. However, the market is not without challenges; supply chain disruptions are impacting the timely delivery of new constructions, particularly concerning essential data center equipment like network switches. These challenges contribute to delays that can extend over a year, intensifying the existing supply/demand imbalance and driving an upward trend in pricing within the data center market.

Investor Impact

Despite challenges in capital markets pricing, which have led to decreasing volumes across various sectors, data centers continue to attract significant interest from investors.

Data Center Market Recent Industry Developments (2025–2026)

| Date | Company | Development | Impact |

|---|---|---|---|

| 16 March 2026 | STT GDC India | Commenced construction of the Palava hyperscale campus in Maharashtra with an initial 50 MW IT load capacity. | Scales to 400 MW, positioning it as one of India's largest AI-ready data center regions. |

| 02 March 2026 | AMD | Announced a $100 billion agreement to supply up to 6 GW of AI capacity to Meta. | Facilitates the deployment of Helios rack-scale servers and MI450 architecture for advanced AI workloads. |

| 19 February 2026 | Larsen & Toubro | Announced multiple contract wins for L&T-Cloudfiniti to expand data center and cloud services. | Strengthens its position in the $200 billion investment inflow expected for Indian digital infrastructure. |

| 03 January 2026 | Yotta Data Services | Pledged to scale investments to bring nearly 500 MW of AI factories online throughout the year. | Supports the surge in sovereign cloud platforms and high-performance AI infrastructure demand. |

| 14 October 2025 | Partnered with AdaniConneX to develop a $15 billion AI data center hub in Visakhapatnam. | Establishes gigawatt-scale operations supported by subsea cables and green energy infrastructure. | |

| 21 April 2025 | Core AI | Filed SEC Form 20-F highlighting the transition to AI-native infrastructure and new campus joint ventures. | Signals a strategic pivot toward energy-optimized campuses specifically for high-performance computing. |

Data Center Market Scope: Inquiry Before Buying

| Data Center Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 224.1 USD Bn |

| Forecast Period 2026-2032 CAGR: | 26% | Market Size in 2032: | 1129.89 USD Bn |

| Segments Covered: | by Type | Traditional Cloud Hyperscale |

|

| by Deployment | Cloud On-premise |

||

| by Industry | IT & Telecom BFSI Energy Manufacturing Others |

||

| by Paint Type | Water-based Paints Solvent-based Paints Powder Coatings UV-cured Coatings Anti-corrosive Coatings |

||

| by End-use Component | Server Racks Cooling Systems Power Equipment Walls & Ceilings Flooring Systems |

||

Data Center Market, by Region:

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Data Center Market Key Players:

| Sr. No | Company | Data Center Footprint | Total Capacity | AI Infrastructure | Listed Entity | Service Scope |

| Asia Pacific | ||||||

| 1 | Sify Technologies Limited | 14 operational data centers across India | 188 MW+ installed capacity | India's first NVIDIA DGX-Ready AI campus certified for liquid cooling | NASDAQ-listed (Ticker: SIFY) | End-to-end digital ICT solutions including cloud, network, cybersecurity, managed services and colocation |

| 2 | Fujitsu Ltd | *** | *** | *** | *** | *** |

| 3 | Reliance Group | Multiple hyperscale campuses in India, including Jamnagar and Navi Mumbai | 168 MW+ operational AI campus (Phase I); multi-GW pipeline | AI-enabled data centers, GPU clusters, sovereign AI infrastructure, Meta partnership | NSE: RELIANCE | Colocation, cloud, edge computing, AI infrastructure, connectivity, digital platforms |

| 4 | Capgemini SE | *** | *** | *** | *** | *** |

| 5 | HCL Technologies Limited | *** | *** | *** | *** | *** |

| 6 | Hitachi Ltd | *** | *** | *** | *** | *** |

| 7 | Huawei Technologies Co. Ltd | *** | *** | *** | *** | *** |

| North America | ||||||

| 9 | Digital Realty |

*** | *** | *** | *** | *** |

| 10 | Nvidia | *** | *** | *** | *** | *** |

| 11 | IBM Corporation | IBM Cloud data centers and AI infrastructure across APAC | Not publicly disclosed | IBM Vela AI supercomputing infrastructure, watsonx AI platform | NYSE: IBM | Hybrid cloud, AI, consulting, infrastructure services, cybersecurity |

| 12 | Oracle | *** | *** | *** | *** | *** |

| 13 | Alphabet Inc. |

*** | *** | *** | *** | *** |

| 14 | Equinix Inc. | 100+ IBX data centers | 725 MW+ (global) | AI-ready IBX, liquid cooling | NASDAQ: EQIX | Colocation, interconnection, cloud exchange |

| 15 | Cisco Systems Inc. |

*** | *** | *** | *** | *** |

| 16 | Hewlett Packard Enterprise Company |

*** | *** | *** | *** | *** |

| Europe | ||||||

| 17 | HCL Technologies Limited |

*** | *** | *** | *** | *** |

| 18 | Capgemini SE | Global delivery centers and managed infrastructure operations across India, Singapore, Australia, Japan, and China | N/A (No owned colocation capacity) | AI-driven cloud transformation and hybrid infrastructure solutions** | Euronext Paris: CAP | Cloud services, managed infrastructure cyber security,consulting, digital transformation |

| 19 | Schneider Electric SE |

*** | *** | *** | *** | *** |

| 20 | Vertiv Co. | *** | *** | *** | *** | *** |

| 21 | Equinix Inc. | *** | *** | *** | *** | *** |

| 22 | Hewlett Packard Enterprise Company | Regional presence across India, Singapore, Australia, Japan, China, South Korea, and Southeast Asia through customer deployments and service centers | N/A (No owned data center capacity disclosed) | HPE Private Cloud AI, Cray Supercomputing, NVIDIA AI Computing by HPE, GreenLake Hybrid Cloud Platform | NYSE: HPE | Hybrid cloud, AI infrastructure, HPC systems, storage, networking, edge computing, managed services, cybersecurity |

| 23 | IBM Corporation |

*** | *** | *** | *** | *** |

| 24 | Cisco Systems Inc. |

*** | *** | *** | *** | *** |

| 25 | Sify Technologies Limited |

*** | *** | *** | *** | *** |

FAQs:

1. What is the current trend in data center technology?

Ans: Data centers are increasingly leveraging artificial intelligence (AI) and machine learning (ML) for predictive analytics, automation, and optimization of operations. These technologies help in predictive maintenance, energy management, and overall efficiency improvements.

2. How do data centers ensure security and compliance?

Ans: Data centers employ a range of measures to ensure security and compliance with industry regulations. The nature and extent of these measures may vary based on the type of data center, the data they handle, and the regulatory environment.

3. What is the impact of cloud computing on traditional data centers?

Ans: cloud computing has transformed traditional data centers by offering unparalleled scalability, flexibility, and cost efficiency through on-demand resources and a pay-as-you-go model. This shift has redefined the role of traditional data centers, placing emphasis on agility, global reach, and outsourcing infrastructure management to cloud service providers.

4. How are data centers addressing energy efficiency and sustainability?

Ans: Data centers are actively addressing energy efficiency and sustainability concerns through a combination of technological advancements, operational strategies, and environmental initiatives.

5. Who are the top key players in the Data Center Market?

Ans. Digital Realty, Nvidia, Oracle, Alphabet Inc., Fujitsu Ltd, Reliance Group, Capgemini SE, HCL Technologies Limited, Sify Technologies Limited, IBM Corporation, Cisco Systems Inc., Hewlett Packard Enterprise Company, Hitachi Ltd, Equinix Inc., Huawei Technologies Co. Ltd, Schneider Electric SE, Vertiv Co.