Data Center Cooling Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

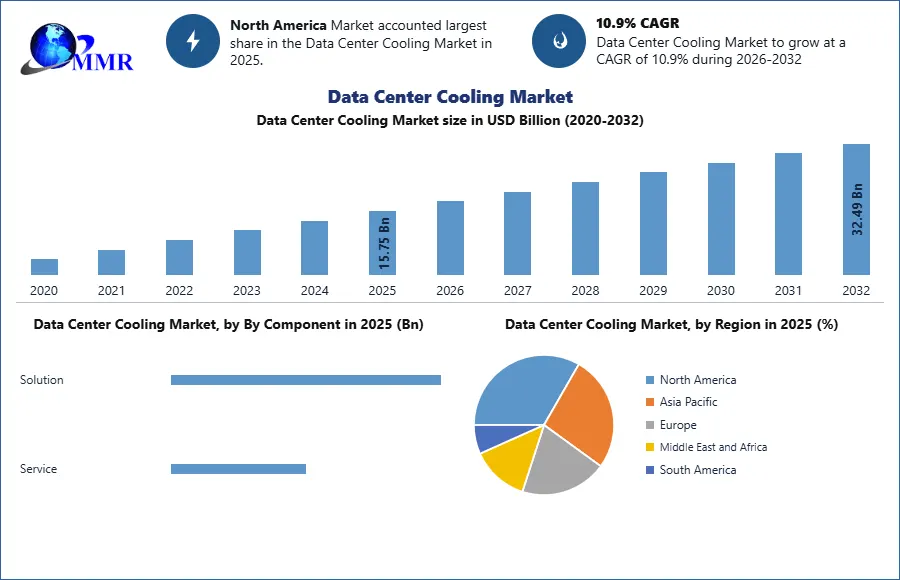

Data Center Cooling Market size was valued at USD 15.75 Bn. in 2025 and the total revenue is expected to grow at a CAGR of 10.9% through 2026 to 2034, reaching nearly USD 39.96 Bn.

Data Center Cooling Market Overview:

Free cooling can also aid in the energy efficiency of data centres. Thermal reservoirs, low-temperature ambient air, and evaporating water are only a few examples of free cooling. The sole objective of data centre cooling is to keep the environment suitable for the operation of information technology equipment (ITE). To achieve this purpose, the heat generated by the ITE must be removed and transferred to a heat sink.

To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

Data Center Cooling Market Segment Analysis:

The data center cooling market is segmented by cooling type, component, data center type, and end-user industry, with each segment contributing significantly to market expansion. By cooling type, liquid-based cooling systems are rapidly gaining dominance, accounting for approximately 45–47% market share in 2025, driven by the rising heat density of AI and high-performance computing workloads. Traditional air-based cooling systems continue to hold a significant share due to their widespread deployment in legacy infrastructure; however, their efficiency limitations are accelerating the shift toward liquid cooling technologies such as direct-to-chip and immersion cooling.

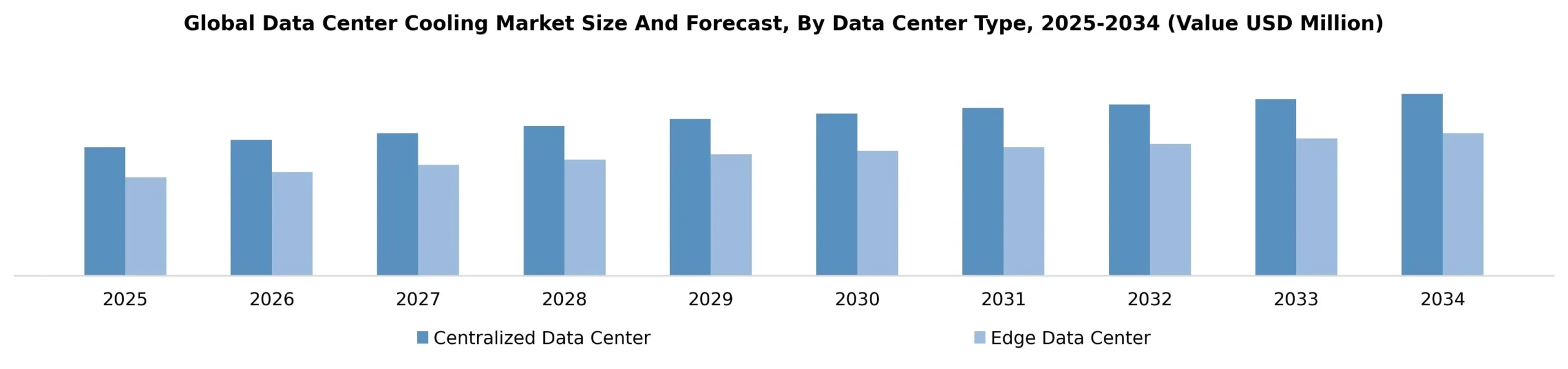

In terms of data center type, hyperscale data centers dominate the market with over 35% share, owing to increasing investments by cloud service providers and tech giants. Meanwhile, edge data centers are expected to witness the fastest growth during the forecast period due to 5G deployment and decentralized computing needs.

Based on Component, the Data Center Cooling Market is segmented into Solutions and Services. The Solutions segment held the largest market share in 2025. The segment dominates because cooling hardware represents the highest capital expenditure in data center infrastructure, encompassing air conditioning units, chillers, cooling towers, control systems, and increasingly, liquid cooling solutions. Rising rack power densities, accelerated deployment of AI servers, and continuous expansion of hyperscale and colocation facilities have significantly increased investments in advanced cooling equipment. Furthermore, the growing emphasis on reducing Power Usage Effectiveness (PUE), improving operational reliability, and complying with sustainability targets has accelerated the replacement of conventional cooling systems with energy-efficient technologies, reinforcing the leadership of the Solutions segment.

Overall, the market is transitioning toward energy-efficient, high-density, and sustainable cooling solutions, with liquid cooling emerging as the key growth driver through 2034.

Based on Organization Size, the Data Center Cooling Market is segmented into Large Organizations and Small & Medium Organizations. Large Organizations held the largest market share in 2025. The dominance of this segment is driven by substantial investments from hyperscale cloud providers, colocation operators, financial institutions, telecommunications companies, and multinational enterprises in expanding high-capacity data center infrastructure. Large organizations operate mission-critical IT environments with stringent uptime requirements, making investments in advanced cooling technologies essential for ensuring operational continuity, energy efficiency, and regulatory compliance. Their greater capital availability and long-term digital transformation strategies continue to support sustained demand for high-performance cooling systems.

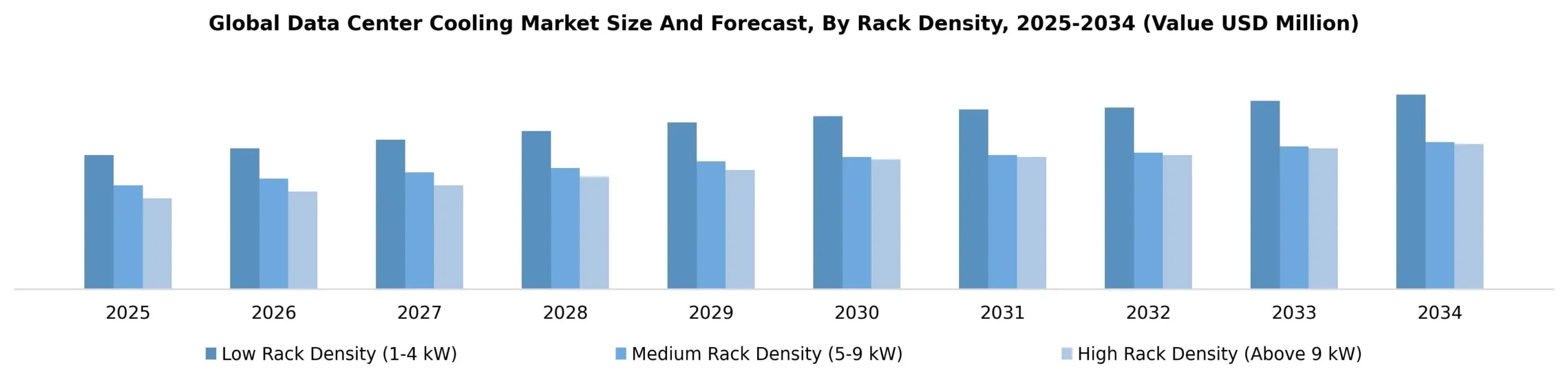

Based on Rack Density, the Data Center Cooling Market is segmented into Low Rack Density (1–4 kW), Medium Rack Density (5–9 kW), and High Rack Density (Above 9 kW). Medium Rack Density held the largest market share in 2025. This segment remains the industry standard across enterprise, colocation, and commercial data centers, offering an optimal balance between computing performance, energy efficiency, and cooling requirements. Medium-density racks support a broad range of conventional enterprise applications while minimizing infrastructure complexity and operational costs. Nevertheless, High Rack Density is anticipated to witness the fastest growth through the forecast period, driven by increasing deployment of AI servers, GPU clusters, and high-performance computing systems that demand advanced liquid cooling and precision thermal management solutions.

Based on End-Use Industry, the Data Center Cooling Market is segmented into BFSI, IT & Telecom, Research & Academic, Government & Defense, Retail, Energy, Manufacturing, Healthcare, and Others. IT & Telecom held the largest market share in 2025. The segment's leadership is attributed to rapid expansion of cloud computing infrastructure, increasing internet traffic, large-scale deployment of artificial intelligence applications, and continuous investments in hyperscale and colocation data centers. Telecommunications operators and cloud service providers continue to expand network infrastructure to support 5G, edge computing, streaming services, and enterprise digitalization, significantly increasing demand for high-efficiency cooling systems. Additionally, the industry's strong focus on minimizing operational costs, improving energy efficiency, and maintaining uninterrupted service availability further reinforces its dominant position in the global Data Center Cooling Market.

Regional Insights:

North America dominates the global data center cooling market, accounting for approximately 38–40% market share in 2025, driven by the presence of leading hyperscale data center operators and strong investments in AI infrastructure. The United States leads the region due to rapid deployment of high-density data centers and increasing adoption of advanced cooling technologies such as liquid and hybrid cooling systems.

Asia-Pacific is the fastest-growing region, supported by rapid digitalization, expanding cloud ecosystems, and increasing data center construction in countries such as China, India, Japan, and Singapore. Government initiatives, rising internet penetration, and cost advantages further contribute to regional growth.

Europe is emerging as a key innovation hub, driven by stringent environmental regulations and a strong focus on sustainable and energy-efficient cooling solutions. Countries such as Germany, the UK, and the Nordic region are leading in adopting green data center technologies.

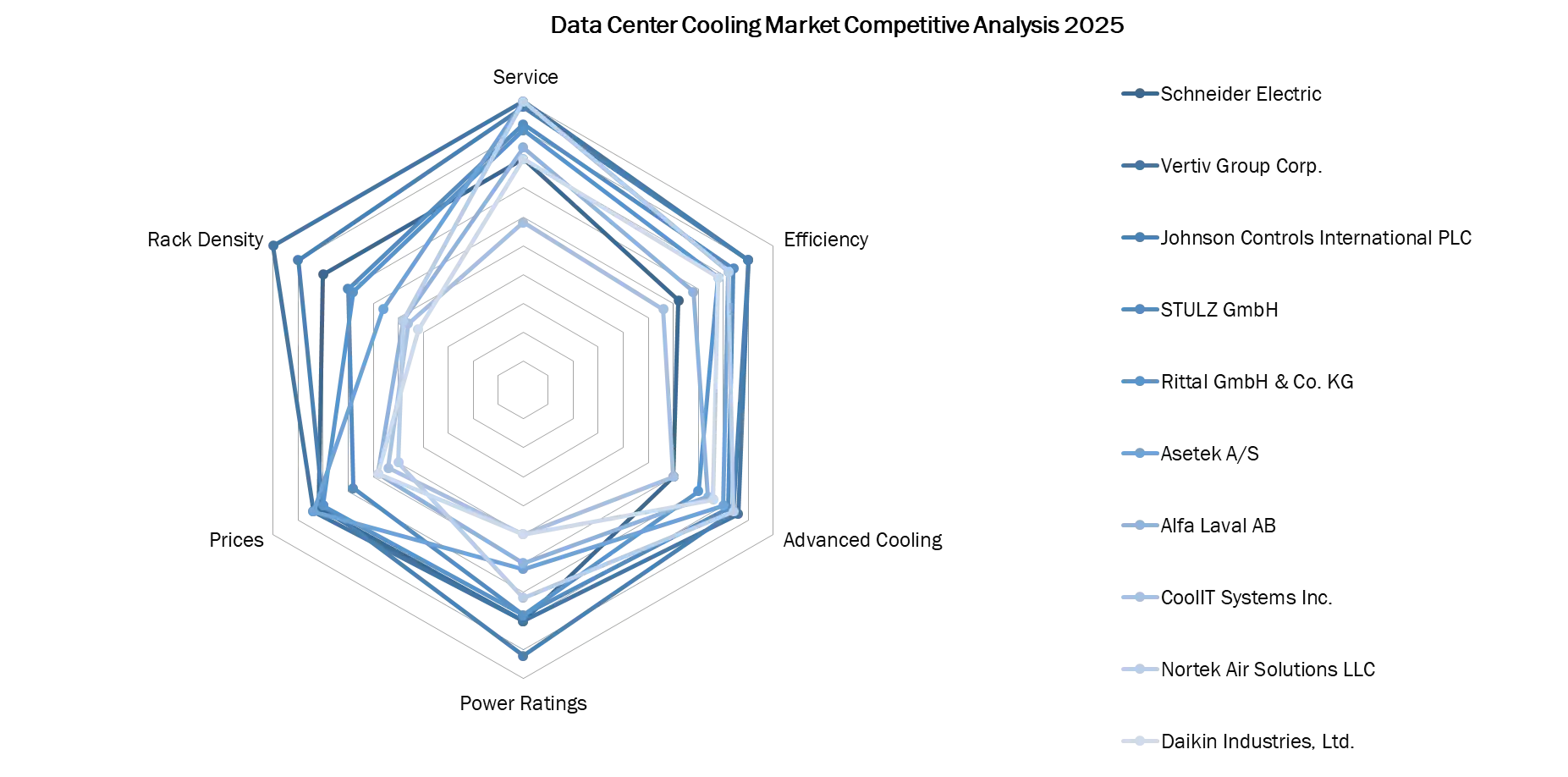

Competitive Analysis:

The data center cooling market is becoming highly competitive as AI, HPC, and high-density rack deployments force operators to shift from conventional air cooling toward hybrid and liquid-based thermal architectures. Vertiv, Schneider Electric, Johnson Controls, STULZ, Rittal, Trane Technologies, Carrier, Daikin, Mitsubishi Electric, Delta Electronics, Munters, Nortek Air Solutions, Eaton, Emerson, Hitachi and Fujitsu compete strongly in facility-scale cooling, power, enclosure, controls, chillers, CRAH/CRAC systems, prefabricated modules and service networks. Vertiv is positioned as one of the strongest AI infrastructure players because it is combining power, cooling and rack ecosystems for OCP-compliant high-density deployments and is also collaborating with NVIDIA on 800 VDC platform designs for next-generation AI factories. Johnson Controls is strengthening its liquid cooling position through a 2025 strategic investment in Accelsius, a two-phase direct-to-chip liquid cooling company, while Trane Technologies moved further into full-stack data center thermal management with its 2026 agreement to acquire LiquidStack. These developments show that large infrastructure providers are no longer treating cooling as a standalone HVAC category; they are building integrated thermal-management platforms around AI servers, power density, water efficiency and lifecycle services.

Specialist liquid cooling and immersion players such as CoolIT Systems, Asetek, Alfa Laval, GRC, Coolcentric, Chilldyne, LiquidCool Solutions, LiquidStack, AireSys/AIREASYS, DCX, Submer and Asperitas compete on direct-to-chip cold plates, coolant distribution units, immersion tanks, pumps, heat exchangers, leak-free operation, retrofit capability and high-density AI workload support. CoolIT gained major strategic relevance after Ecolab announced in 2026 that it would acquire CoolIT Systems, positioning Ecolab as a broader cooling-solutions provider for next-generation AI data centers. Alfa Laval competes through heat exchangers and liquid-cooling support for high-capacity data centers and launched FreeWaterLoop in 2026 as an integrated external cooling system for facility loops. Submer is expanding internationally with sustainable liquid cooling solutions for India’s AI data center ecosystem, while LiquidStack launched a modular coolant distribution unit with up to 10 MW cooling capacity in 2025. Overall, competitive advantage is shifting toward vendors that can offer scalable liquid cooling, low water usage, heat reuse, fast deployment, integration with power infrastructure, and proven service capability for hyperscale and AI factories.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 06 August 2025 | Daikin Industries, Ltd. | The company announced a definitive agreement to acquire DDC Solutions, a specialist in advanced cooling systems for AI data centers. | This acquisition integrates server-rack cooling equipment into the Daikin Applied Americas portfolio to address high-density thermal management needs. |

| 31 December 2025 | Munters Group | The business area Data Center Technologies (DCT) secured record orders valued at 2.1 billion SEK for chilled water infrastructure. | The order provides a colocation provider with custom CRAHs, CDUs, and chillers to support large-scale US-based facilities through 2028. |

| 15 February 2025 | Submer | The firm announced the expansion of its SmartPod immersion cooling systems across AI-focused data centers throughout Europe. | This strategic rollout enhances Power Usage Effectiveness (PUE) for operators managing next-generation GPU clusters. |

| 14 June 2025 | Shell | The multinational launched the Shell DLC Fluid S3, a new propylene glycol-based Direct Liquid Cooling (DLC) solution. | The fluid is specifically engineered to handle the thermal demands of High-Performance Computing (HPC) and Artificial Intelligence (AI) workloads. |

| 25 June 2025 | Castrol | The company introduced a dedicated fluid management service for data center liquid cooling operations. | The service facilitates the transition from air cooling to liquid-based setups, optimizing cooling efficiency and equipment longevity. |

Data Center Cooling Market Scope: Inquire before buying

| Data Center Cooling Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 15.75 USD Billion |

| Forecast Period 2026-2034 CAGR: | 10.9% | Market Size in 2032: | 39.96USD Billion |

| Segments Covered: | By Component | Solution Air conditioner Air handling units Split air conditioning systems Packaged air conditioning units (PAC) Others Chilling unit Air-cooled chillers Water-cooled chillers Glycol-cooled chillers Cooling tower Evaporative cooling Dry Others Control system Economizer system Condensing Non-condensing Liquid cooling system Direct to chip Immersive Single phase Two phase Others Service Consulting Maintenance and support Installation and deployment |

|

| By Data Center Type | Centralized Data Center Hyperscale Colocation Enterprise Edge Data Center |

||

| By Type of Cooling | Room-based Cooling Row/Rack-based Cooling |

||

| By Rack Density | Low Rack Density (1-4 kW) Medium Rack Density (5-9 kW) High Rack Density (Above 9 kW) |

||

| By Organization Size | Large Organization Size Small and Medium Organization |

||

| By End Use Industry | BFSI IT & Telecom Research & Academic Government & Defense Retail Energy Manufacturing Healthcare Others |

||

Data Center Cooling Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

Data Center Cooling Market, Key Players:

- Vertiv Group Corp.

- Johnson Controls International PLC

- STULZ GmbH

- Rittal GmbH & Co. KG

- Asetek A/S

- Alfa Laval AB

- CoolIT Systems Inc.

- Nortek Air Solutions LLC

- Daikin Industries, Ltd.

- Mitsubishi Electric Corporation

- Delta Electronics, Inc.

- Munters Group AB

- Green Revolution Cooling (GRC)

- Coolcentric

- Fujitsu Ltd.

- Carrier Global Corp.

- Eaton Corporation plc

- Emerson Electric Co.

- Hitachi, Ltd.

- Trane Technologies plc

- Black Box Corporation

- Chilldyne, Inc.

- Bitfury

- LiquidCool Solutions, Inc.

- LiquidStack

- AireSys / AIREASYS Technologies

- DCX The Liquid Cooling Company

- Submer Technologies

- Asperitas

Others