Companion Diagnostics Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

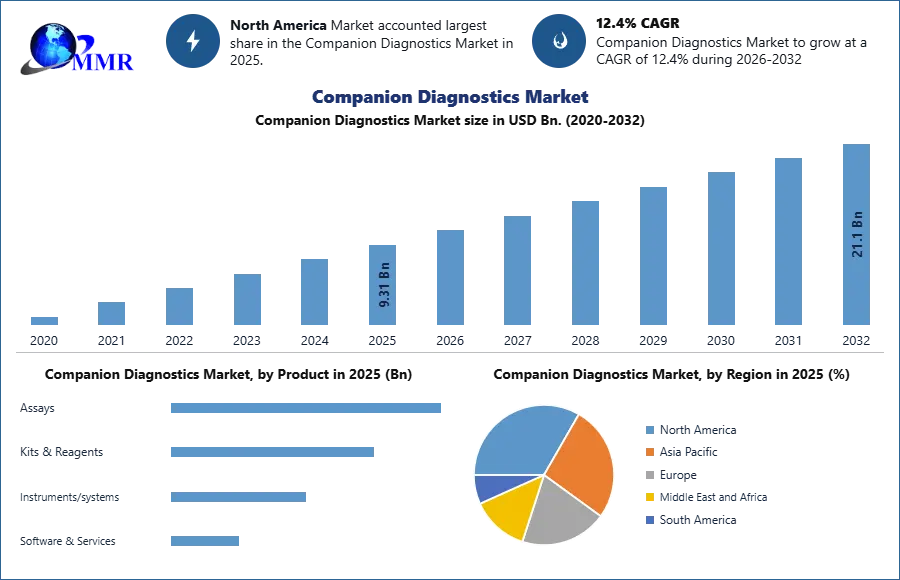

Companion Diagnostics Market size was valued at USD 9.31 Billion in 2025 and the total Companion Diagnostics Market revenue is expected to grow at a CAGR of 12.4% from 2026 to 2032, reaching nearly USD 21.1 Billion by 2032.

Companion Diagnostics Market Overview

The companion diagnostics for oncology market is witnessing significant growth and transformation driven by advancements in personalized medicine and the development of companion diagnostic tools. This market segment plays a crucial role in the era of precision medicine, where healthcare is increasingly tailored to individual patients based on their unique genetic and molecular profiles. The companion diagnostics market for oncology is characterized by ongoing innovation and development. These diagnostic tools are continually evolving to identify specific biomarkers, genetic mutations, or other molecular characteristics in cancer patients. These advancements are crucial for ensuring that the right patients receive the most suitable targeted therapies, optimizing treatment outcomes. The market is particularly focused on oncology, where companion diagnostics have made significant inroads. The oncology sector benefits immensely from these diagnostic tools, which help oncologists determine the most appropriate treatment strategies, especially in the case of targeted cancer therapies. Collaboration between pharmaceutical companies, diagnostic developers, healthcare institutions, and regulatory agencies is instrumental in the successful development and adoption of companion diagnostics. These partnerships are key drivers for advancing personalized medicine and expanding the market.

To know about the Research Methodology :- Request Free Sample Report

Companion Diagnostics Market Dynamics

Increase in number of companion Diagnostic Testing Laboratories to boost the Market growth

The growth of companion diagnostic testing laboratories is another driver for the market. Specialized laboratories that conduct companion diagnostic tests are expanding their capabilities and capacity to meet the rising demand, which is expected to boost Companion Diagnostics. These laboratories are equipped with the necessary technology and expertise to perform complex molecular analyses, ensuring accurate and timely results for healthcare providers. The approval of new companion diagnostics by regulatory agencies, such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), drives market growth. When companion diagnostics receive regulatory approval, it provides confidence in their accuracy and clinical utility. As more companion diagnostics gain approval for use with specific therapies, healthcare providers are more likely to incorporate these tests into their clinical practice, boosting market demand. The increasing development and availability of targeted therapies in various disease areas, including oncology, create a strong driver for companion diagnostics. These therapies are designed to act specifically on the molecular targets identified by companion diagnostics. As more targeted therapies are developed, the demand for companion diagnostics to identify suitable patients for these treatments grows.

Regulatory Hurdles to restraint the Companion Diagnostics Market growth

The regulatory complexities associated with companion diagnostics pose a significant restraint. Navigating the approval processes required for these tests, which often involve coordination with drug approvals, can be time-consuming and resource-intensive. Stringent regulatory requirements can delay market entry and add to development costs. The development of companion diagnostics requires substantial investments in research, validation studies, and clinical trials. The high development costs deter smaller companies and laboratories from entering the market and limit the availability of companion diagnostics Market for some diseases or conditions. Identifying relevant biomarkers for certain diseases can be a significant constraint. Biomarker discovery is essential for developing effective companion diagnostics, and in some cases, the lack of well-defined biomarkers can limit the development of corresponding tests and therapies. Companion diagnostics often involve the collection and analysis of sensitive patient data. Ensuring data privacy and security while complying with relevant regulations can be a significant restraint, particularly with the increasing focus on data protection and privacy laws. The lack of standardized practices and guidelines for companion diagnostics can hinder their widespread adoption. Standardization is crucial for ensuring consistency, accuracy, and comparability of test results across different laboratories and healthcare settings.

Companion Diagnostics Market Segment Analysis:

Based on Technology, Polymerase Chain Reaction Segment is expected to dominate the market over the forecast period. Polymerase Chain Reaction technology is widely utilized in the development of companion diagnostics for oncology, which is expected to boost the Companion Diagnostics Market growth. These diagnostics are specifically designed to identify specific genetic mutations or alterations associated with cancer. They play a critical role in guiding the treatment decisions for cancer patients. Polymerase Chain Reaction allows for the precise and sensitive detection of genetic markers, such as mutations in cancer-associated genes, which is crucial for tailoring personalized treatment plans. Polymerase Chain Reaction is an essential technology for the development of companion diagnostics. As researchers and pharmaceutical companies work to identify biomarkers and genetic variations linked to cancer, PCR provides a reliable and efficient method for detecting these specific genetic changes. This technology is used to validate and refine diagnostic assays, ensuring their accuracy and clinical relevance.

Companion Diagnostics Market Regional Insight:

North America to hold the largest Companion Diagnostics Market share over the forecast period

In 2025, North America, and particularly the United States, dominated the companion diagnostics market. Companion diagnostic tests are considered a significant tool for treatment decisions, especially for many oncology drugs, a classification aligned with the FDA's risk assessment approach. The rising affordability of treatment and well-established healthcare infrastructure are driving the global market for companion diagnostics in the region. The increasing prevalence of chronic diseases all over the world demands companion diagnostics procedures. A large number of ongoing clinical trials, outsourcing services, research activities, and increasing healthcare investment by governments are some of the factors responsible for the growth of the market in North America.

The rising cancer burden in the United States is expected to be a key driver for market growth. In 2024, the country reported approximately 1.8 million new cancer cases and 606,520 cancer-related deaths, according to a study by MMR. Additionally, favorable reimbursement policies for breast cancer diagnostic solutions in the U.S. are projected to facilitate their adoption. The Centers for Medicare and Medicaid Services (CMS) expanded its coverage to include next-generation sequencing as a diagnostic tool for patients with hereditary breast cancer. The growing role of oncology companion diagnostics in the era of next-generation omics is set to propel the market further. For example, in 2022, Guardant Health, Inc. received United States FDA approval for Guardant360 CDx, a companion diagnostic test designed to detect genetic mutations present in cfDNA to assist physicians in identifying patients with non-small cell lung cancer (NSCLC) who would benefit from TAGRISSO treatment. Companion diagnostic tests in the U.S. are categorized as in vitro diagnostic (IVD) class III products, signifying a high-risk classification and therefore the highest level of regulatory oversight. As a result, given the high adoption rates of healthcare expertise and the growing demand for personalized medicine, the United States companion diagnostics market is expected to register significant growth over the forecast period.

Companion Diagnostics Market Competitive Landscape

Companies in the companion diagnostics market continually strive to develop and implement innovative technologies for diagnostic testing, improving accuracy, efficiency, and the range of applications. Strategic collaborations and partnerships are common within the industry. These alliances often involve diagnostic testing laboratories, healthcare providers, and pharmaceutical companies working together to advance companion diagnostics. Companies with a global presence have a competitive advantage. They can leverage their diagnostic tests across multiple markets, serving a broader patient population. To gain a competitive edge, companies focus on expanding their market presence, targeting regions with growing demand for companion diagnostic tests, such as North America.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 15 February 2026 | Agilent Technologies | The company obtained FDA clearance for its PD-L1 IHC 22C3 pharmDx assay as a companion diagnostic for epithelial ovarian and fallopian tube cancers. | This development expands precision medicine access for ovarian cancer patients needing targeted immunotherapy. |

| 19 January 2026 | Roots Analysis | Industry tracking confirmed a six-fold increase in clinical trial success rates when using biomarker-data for patient recruitment. | The finding validates companion diagnostics as a critical financial driver for reducing drug development costs. |

| 22 December 2025 | Foundation Medicine | The company reached a milestone of 100 approved CDx indications globally across its tissue and liquid biopsy platforms. | This cements their position as a market leader in comprehensive genomic profiling for diverse oncological therapies. |

| 14 November 2025 | Thermo Fisher Scientific | The Oncomine Dx Target Test received FDA approval as a companion diagnostic for Bayer’s sevabertinib in treating HER2-mutant NSCLC. | The approval secures broad reimbursement across the US and Europe, removing accessibility barriers for lung cancer testing. |

| 12 September 2025 | Illumina | Illumina entered a strategic partnership with global pharma firms to develop tumor-agnostic KRAS companion diagnostics using the TruSight Oncology test. | This initiative advances standardized precision oncology by enabling broad patient identification for KRAS-targeted drugs. |

| 28 April 2025 | Roche Diagnostics | The VENTANA TROP2 RxDx assay received FDA Breakthrough Device Designation for its use in non-small cell lung cancer (NSCLC). | Integrating AI-driven digital pathology provides superior diagnostic precision over traditional manual scoring methods. |

Companion Diagnostics Industry Ecosystem

Companion Diagnostics Market Scope: Inquiry Before Buying

| Companion Diagnostics Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 9.31 USD Bn. |

| Forecast Period 2026-2032 CAGR: | 12.4% | Market Size in 2032: | 21.1 USD Bn. |

| Segments Covered: | by Product | Assays, Kits & Reagents Instruments/systems Software & Services |

|

| by Technology | Polymerase Chain Reaction Immunohistochemistry In-situ Hybridization Next Generation Gene Sequencing Other |

||

| by Indication | Cancer Neurological Diseases Infectious Diseases Others |

||

| by End User | Hospitals & Clinics Diagnostic Laboratories Research Institutions Pharmaceutical Companies |

||

Companion Diagnostics Market, by region:

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Companion Diagnostics Market Report in Strategic Perspective:

- Roche Diagnostics

- Thermo Fisher Scientific

- Agilent Technologies

- Abbott Laboratories

- Qiagen

- Myriad Genetics, Inc,

- Illumina

- Danaher Corporation

- Biomérieux

- Icon plc

- Sysmex Corporation

- Guardant Health

- Foundation Medicine

- Bio-Rad Laboratories

- Siemens Healthineers

- Almac Group

- ARUP Laboratories

- Abnova Corporation

- Invivoscribe

- Amoy Diagnostics

- Labcorp

- Natera

- Hologic

- Becton, Dickinson and Company

- Quest Diagnostics