Coal to Liquid Market Size by Product, Technology, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2029

Overview

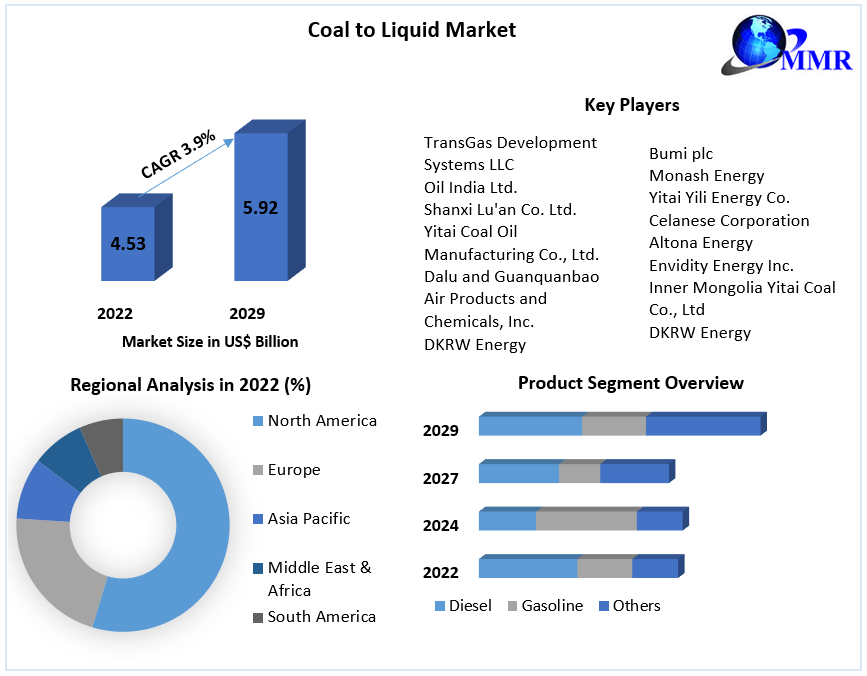

Coal-to-liquid Fuels Market size is expected to reach US$ 5.92 Bn by 2029, growing at a CAGR of 3.9% during the forecast period.

Transformation of coal to liquid to obtain liquid hydrocarbon products is called coal liquefaction. Liquid fuels from coal provide a feasible alternative to conventional fuels and coal-derived fuels are low in particulates, ultra-clean, and have low nitrogen level.

The report study has analyzed revenue impact of covid-19 pandemic on the sales revenue of market leaders, market followers and disrupters in the report and same is reflected in our analysis.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The objective of the report is to present a comprehensive assessment of the market and contains thoughtful insights, facts, historical data, industry-validated market data and projections with a suitable set of assumptions and methodology. The report also helps in understanding coal to liquid market dynamics, structure by identifying and analyzing the market segments and project the global market size. Further, report also focuses on competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence. The report also provides PEST analysis, PORTER’s analysis, SWOT analysis to address questions of shareholders to prioritizing the efforts and investment in near future to emerging segment in coal to liquid market.

Increasing demand for liquid fuel in transportation sector across the globe is a major factor for growing the global coal to liquid market. Moreover, presence of plentiful coal reserves globally, coupled with rising demand for low carbon-emitting fuels are some other factors projected to propel growth of the target market. Technological advancements coupled with sustained growth of the liquid fuels demand for transportation are the factor driving the global coal to liquid market. High capital expenditure associated with liquefaction process equipment and plants, and stringent government regulations imposed on emission of greenhouse gases and carbon, are estimated to hamper growth of the market over the forecast period.

Diesel has the leading product segment in 2022. Diesel produced from coal to liquid processes has several potential advantages. Diesel produced from crude oil contains aromatics, which on combustion produces particals. But, diesel produced form liquefaction of coal do not contain aromatics and hence it burns much cleaner and overcome one of the major objection of diesel combustion.

Indirect coal liquefaction is the most used process and is the largest technology segment. In this technology, solid coal is passed into a gas phase process before it is converted into a raw liquid form. Direct coal liquefaction is widely used in different applications in a lot of coal to liquid plants. The products produced using this process can be polished to meet most of the current specifications of the transportation fuels.

North America is estimated to the highest market share in the global coal to liquid market owing to technological advancements and geological characteristics. Its dominance can be attributed to occurrence of large coal reserves in the region. The market for coal liquefaction in the Asia Pacific is expected to expand significantly in the forecast period.

Coal to Liquid Market Scope: Inquire before buying

| Coal to Liquid Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2022 | Forecast Period: | 2023-2029 |

| Historical Data: | 2017 to 2022 | Market Size in 2022: | US $ 4.53 Bn. |

| Forecast Period 2023 to 2029 CAGR: | 3.9% | Market Size in 2029: | US $ 5.92 Bn. |

| Segments Covered: | by Product | • Diesel • Gasoline • Others |

|

| by Technology | • Direct Coal Liquefaction • Indirect Coal Liquefaction |

||

Coal to Liquid Market, by Region

• North America (United States, Canada and Mexico)

• Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

• Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

• Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

• South America (Brazil, Argentina Rest of South America)

Coal to Liquid Market Key Players:

• Chevron Corporation

• Pall Corporation

• Shenhua Group

• Yankuang Company

• Jincheng Anthracite Mining Group

• Sasol Limited

• Linc Energy

• DKRW Energy

• Bumi plc

• Monash Energy

• Yitai Yili Energy Co.

• Celanese Corporation

• Altona Energy

• Envidity Energy Inc.

• Inner Mongolia Yitai Coal Co., Ltd

• TransGas Development Systems LLC

• Oil India Ltd.

• Shanxi Lu'an Co. Ltd.

• Yitai Coal Oil Manufacturing Co., Ltd.

• Dalu and Guanquanbao

• Air Products and Chemicals, Inc.

• DKRW Energy

Frequently Asked Questions:

1. Which region has the largest share in Global Coal to Liquid Market?

Ans: North America region held the highest share in 2022.

2. What is the growth rate of Global Coal to Liquid Market?

Ans: The Global Coal to Liquid Market is growing at a CAGR of 3.9% during forecasting period 2023-2029.

3. What is scope of the Global Coal to Liquid Market report?

Ans: Global Coal to Liquid Market report helps with the PESTEL, PORTER, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in Global Coal to Liquid Market?

Ans: The important key players in the Global Coal to Liquid Market are – Chevron Corporation, Pall Corporation, Shenhua Group, Yankuang Company, Jincheng Anthracite Mining Group, Sasol Limited, Linc Energy, DKRW Energy, Bumi plc, Monash Energy, Yitai Yili Energy Co., Celanese Corporation, Altona Energy, Envidity Energy Inc., Inner Mongolia Yitai Coal Co., Ltd, TransGas Development Systems LLC, Oil India Ltd., Shanxi Lu'an Co. Ltd., Yitai Coal Oil Manufacturing Co., Ltd., Dalu and Guanquanbao, Air Products and Chemicals, Inc., DKRW Energy.

5. What is the study period of this Market?

Ans: The Global Coal to Liquid Market is studied from 2022 to 2029.