Carbon Management Software Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

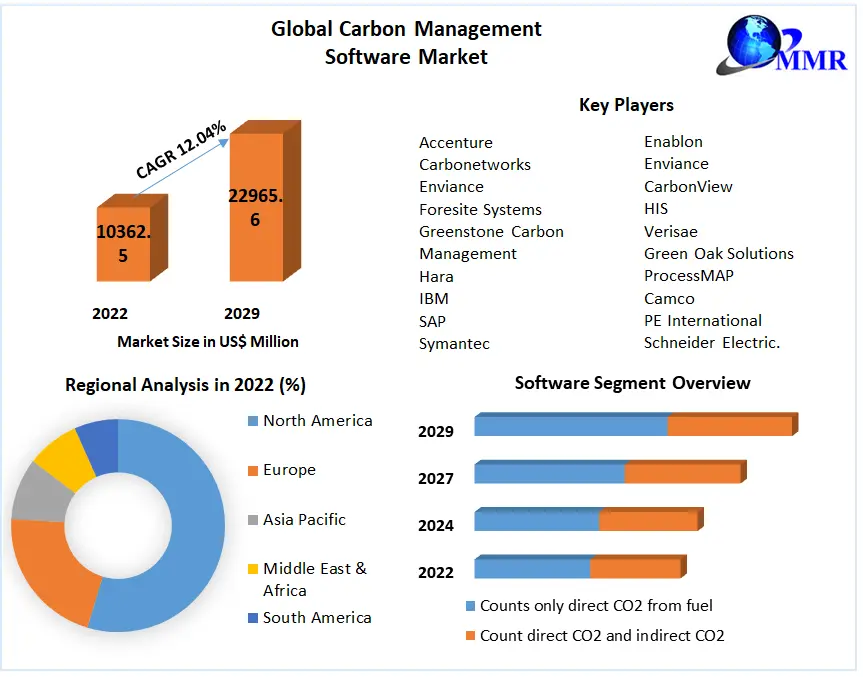

The Carbon Management Software Market size was valued at USD20.72 Billion in 2025, and the total Carbon Management Software Market revenue is expected to grow at a CAGR of 22.39% from 2026 to 2032, reaching nearly USD 85.24 Billion.

Carbon Management Software Market Introduction:

Carbon Management Software is specialized tool and platforms designed to help organizations measure, manage, & reduce their carbon emissions and environmental impact. These software solutions utilize advanced technologies such artificial intelligence, machine learning and data analytics to collect, analyse, and greenhouse gas (GHG) emissions data. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The Carbon Management Software Market is experiencing rapid growth as companies worldwide prioritize sustainability, regulatory compliance, and carbon footprint reduction. The above table offers insights into corporate perceptions of many carbon management software providers, highlighting brand awareness and capability gratitude.

Sphera, SAP and Schneider Electric emerge as the most preferred providers, with strong brand recognition and perceived leadership in carbon management capabilities. Other key players, for example Watershed, WayCarbon, and Benchmark Gensuite, also receive substantial acknowledgment for their capabilities. Nevertheless, a notable portion of respondents remnants unaware of offerings from several providers, indicating an opportunity for increased carbon management software market penetration and awareness-building.

Key Players with strong or market-leading capabilities, including IBM, Microsoft, and Persefoni, continue to gain traction owing to their robust reporting, analytics, and compliance solutions. Meanwhile, providers for example Normative, Sweep, and FigBytes/AMCS face challenges in brand recognition, with a significant share of respondents unfamiliar with their offerings. This analysis underscores the competitive landscape of the carbon management software market, where differentiation over advanced scalability, functionality, and seamless integration with corporate sustainability strategies remains crucial.

| Brand Perception Analysis of Carbon Management Software Vendors 2025 | |||||

| Software Provider | Market-leading | Strong Capabilities | Average Capabilities | Recognize the Name Only | Unaware of the Offering |

| Sphera | 11% | 29% | 11% | 20% | 29% |

| Schneider Electric | 13% | 25% | 11% | 26% | 24% |

| SAP | 6% | 28% | 11% | 28% | 27% |

| Watershed | 9% | 19% | 7% | 20% | 44% |

| Benchmark Gensuite | 7% | 20% | 8% | 27% | 37% |

| WayCarbon | 7% | 20% | 8% | 22% | 44% |

| Wolters Kluwer Enablon | 8% | 19% | 9% | 22% | 42% |

| Cority | 6% | 17% | 10% | 17% | 50% |

| Optera | 4% | 19% | 6% | 21% | 51% |

| Diligent | 5% | 15% | 11% | 35% | 34% |

| Microsoft | 5% | 14% | 10% | 40% | 30% |

| Persefoni | 6% | 13% | 9% | 17% | 55% |

| VelocityEHS | 5% | 14% | 9% | 25% | 46% |

| IBM | 4% | 12% | 13% | 37% | 35% |

| UL Solutions | 5% | 9% | 6% | 27% | 53% |

| Salesforce Net Zero Cloud | 3% | 10% | 9% | 27% | 51% |

| FigBytes/AMCS | 4% | 9% | 5% | 26% | 56% |

| Sweep | 3% | 8% | 5% | 20% | 65% |

| Normative | 3% | 5% | 8% | 18% | 65% |

Carbon Management Software Market Dynamics:

Increasing awareness of sustainability and the threat of a global 1.5°C temperature rise is prompting strategic shifts in government and organizations. Major players are adopting carbon management tools to address the probable 18% GDP loss from climate change by 2050. These tools, used to manage, calculate, monitor, and report emissions, help measure operational emissions during the supply chain. According to Maximize market Research, the carbon management software market is projected to grow at a CAGR of 22.39% reaching US$ 85.25 Billion by 2032. The carbon management system market is fragmented, as various companies are offering software for management and monitoring. This rise in numbers is being caused by greater approval of cloud services. Businesses that provide consultation services are expected to grow steadily and exhibit a similar pattern during 2025-2032.

Stringent regulations mandating emissions reporting & reduction goals, like as those set forth by government bodies like U.S. SEC & international climate agreements, drive demand for accurate Carbon Management Software Market. Increasing corporate commitments to sustainability and ESG (Environmental, Social, and Governance) goals propel organizations to adopt advanced carbon management technologies to monitor and mitigate their environmental impact. Integration of AI, ML, and IoT (Internet of Things) in Carbon Management Software enhances data accuracy, predictive analytics, and monitoring capabilities, enabling proactive emissions management strategies. Effective carbon management reduces environmental footprint and also optimizes resource use, lowers operational costs, enhances efficiency, making it economically beneficial for business. Shifting towards renewable energy sources and sustainable practices requires robust carbon management strategies to track & optimize carbon offset and renewable energy investments drive Carbon Management Software Market growth.

Introduced CERius, AI-powered carbon emissions management software, at Azito power plant in Cote D’Ivoire, enhancing accuracy in emissions reporting & supporting net-zero goal through data precision and AI-driven insights. Recognized as a leader in Sustainability Management Software by Forrester, highlighting its strength in carbon accounting, compliance, and decarbonization planning, leveraging AI for advanced financial modeling and ESG reporting. Release OpreX Carbon Footprint Tracer, cloud service in collaboration with SAP, tailored for process manufacturing industries to visualize and reduce CO2 emissions, emphasizing integrated data management & emissions reduction strategies. These development underscore Carbon Management Software Market commitment to innovation and sustainability, Carbon Management Software Market driving forward capabilities of Carbon Management Software to meet evolving environmental challenge ®ulatory requirement globally.

Carbon Capture's Potential Is Being Embraced By Heavy Industries.

Carbon capture reduce overall environmental footprints for heavy-emitting industries including electricity, steel, cement, oil & gas, and chemicals by removing more than 90% of carbon dioxide emissions. Thanks to these large companies, achieving net-zero emissions. According to an MMR analysis, carbon capture is expected to contribute 27% of the required emissions reductions in the cement, iron, steel, and chemicals sectors, which increases Carbon Management Software Market demand.

Carbon capture is being adopted by heavy sectors as feasible alternative to decarbonization, with over 100 new software installations planned in 2022. Heidelberg Cement, a major cement company, is working on eight carbon capture management software plants throughout world. Aramco, the world's largest oil firm, is building one of world largest carbon capture plants to help with hydrogen generation. ArcelorMittal, largest steelmaker in Americas and Europe is using carbon capture as one of levers in its multibillion-dollar investment agenda. All 3 companies committed to achieving net-zero emissions by 2050.

Governments Across The World Are Supporting The Carbon Management Software Market.

Globally Governments are pushing control of carbon emissions by introducing various methods, such as national climate change plans, national sustainable development strategies, & national green growth strategies, to preserve their sustainable goals. The National Green Growth Roadmap was published in 2009 in Cambodia, National Green Technology Policy was published in 2009 in Malaysia, and the National Framework Strategy on Climate Change was published in 2010 and 2011 respectively in Philippines. To control carbon emissions, several nations throughout world are pursuing environmental sustainability strategies, which drive Carbon Management Software Market. For example, Chinese government strives for environmental sustainability through several policies & initiatives as second-largest economy in world.

Chinese President Xi Jinping declared on September 22, 2020, that China enhance its Intended Nationally Determined Contributions by enacting more forceful policies & efforts during General Debate of United Nations General Assembly's 75 session. It hopes to become carbon neutral by 2060, with peak of CO2 emissions occurring in 2032. It is expected that during forecast period, demand for carbon management software will significantly increase.

New Technological Advancement Creates Opportunities In The Carbon Management Software Market.

The goal of Advanced Carbon Management is to help organizations satisfy regulatory requirements. Organizations are proactively controlling carbon emissions through the use of carbon management software from various industries to maximize operational and financial advantages, which drives the Carbon Management Software Market. Carbon management also helps the company enhance its reputation. Furthermore, carbon management software assists enterprises at every level of their energy transition, from capturing greenhouse gas emissions to setting GHG Scope 1, 2, and 3 targets and benchmarks to total GHG emissions automation and carbon management reporting, which drive the Carbon Management Software Market.

A new set of technology-based solutions is successful in reducing the carbon footprint of a wide range of users. Year after year, global warming sets new temperature records, and human activities that emit greenhouse gases (GHG) are directly to effects. Current GHG emissions must be cut in half by 2032 and net-zero by 2050 tent zero global warming at a sub-catastrophic level. Technology and service providers focusing on the underlying technologies that will enable long-term commercial sustainability will have new possibilities as they move toward a net-zero future.

Carbon Management Software Market Segment Analysis:

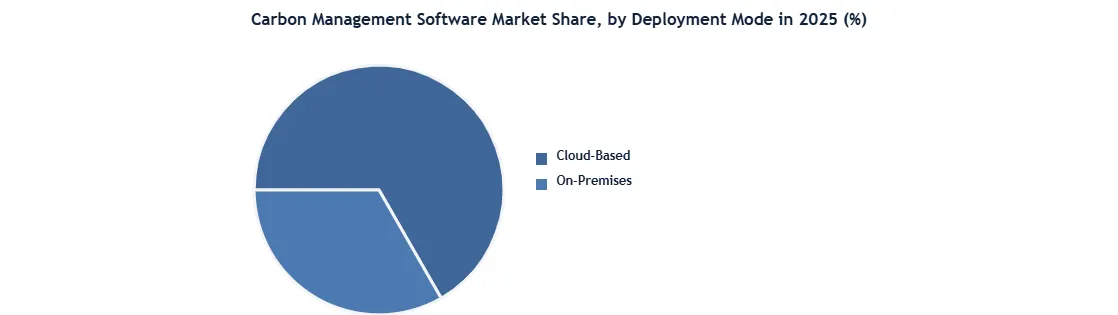

In 2025, Cloud-based deployment mode is dominant segment holding around 72.4% of the carbon management software market. This growth is attributed to cloud-based carbon accounting software offers scalability, flexibility, and remote access, permitting organizations to manage and track CO2 emissions from any location. This model is ideal for businesses looking for cost-effective solutions as it removes the need for extensive infrastructure investments. It allows real-time data updates and integrates easily with other cloud-based systems, improving collaboration across departments. Furthermore, the subscription-based pricing models related with cloud solutions lower initial expenses, making them affordable for small and medium-sized companies. The growing demand for carbon accounting software highlights the necessity for adaptable and scalable solutions, further helping the use of cloud-based platforms across various industries.

Furthermore, the subscription-based pricing models related with cloud solutions lower initial expenses, making them affordable for small and medium-sized companies. The growing demand for carbon accounting software highlights the necessity for adaptable and scalable solutions, further helping the use of cloud-based platforms across various industries.

Carbon Management Software Market Regional Insights:

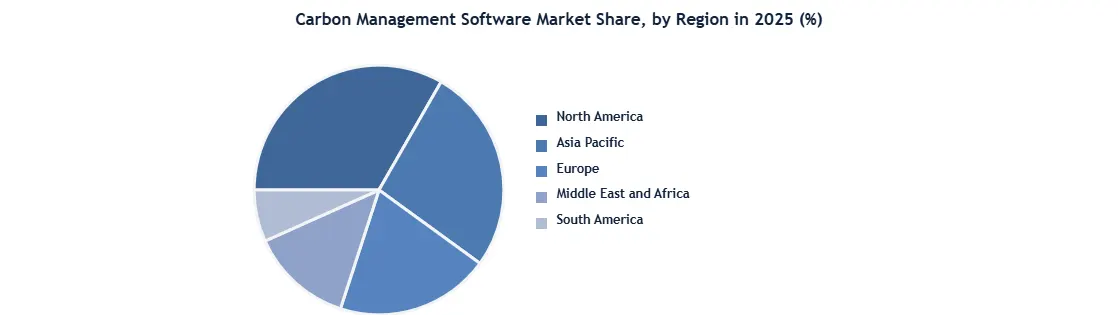

In the Carbon Management Software market, regional dynamics play a crucial role in shaping market trends and growth. As of 2025, North America held the largest Carbon Management Software Market share at 31.90%, driven by the robust adoption of carbon management solutions in the United States. The U.S. government's initiatives, such as those led by the Department of Energy's Office of Fossil Energy and Carbon Management (FECM), underscore a strong commitment to advancing carbon management technologies through substantial investments in research, development, and demonstration (RD&D). For instance, resources like the Carbon Matchmaker Tool and the Carbon Management Interactive Diagram are pivotal in fostering collaborations and accelerating the deployment of carbon management solutions nationwide under initiatives like the Bipartisan Infrastructure Law (BIL), which earmarks over $12 billion for carbon management RD&D over five years. These efforts are expected to significantly bolster demand for carbon management software in North America.

Asia Pacific, commanding a significant 27.40% market share in 2025, is witnessing rapid adoption of carbon management software driven by economic growth, industrialization, and increasing environmental awareness. Countries like China, Japan, and India are investing heavily in renewable energy and carbon reduction initiatives, spurred by both domestic policies and international commitments. For instance, China's commitment to peak carbon emissions by 2032 and achieve carbon neutrality by 2060 has catalyzed the adoption of advanced technologies, including carbon management software, to monitor and reduce emissions across industries. Japan's initiatives under its Green Growth Strategy and India's focus on sustainable development are driving the adoption of carbon management solutions to mitigate environmental impact and enhance competitiveness in global Carbon Management Software Market.

Competitive Landscape

Recent advancements in AI-powered carbon emissions management software by companies like GE Vernova, Persefoni, Sphera, and Yokogawa are poised to drive Carbon Management Software Market growth. These technologies enhanced capabilities in measuring, managing, and reducing carbon footprints in various industries. By leveraging AI & advanced data analytics, these solutions allow more accurate emissions reporting, scenario analysis, and compliance with regulations. This drive adoption among energy producer, manufacturing firms, and sector aiming for carbon neutrality. As businesses prioritize sustainability and ESG goals, demand for sophisticated carbon management software is expected to grow, fostering innovation and Carbon Management Software Market growth in environmental management technologies.

March 26, 2024, GE Vernova launched its AI-powered carbon emissions management software, CERius, at Azito, Cote D’Ivoire's largest gas power plant. This innovative software utilizes artificial intelligence and machine learning to enhance accuracy in emissions reporting and facilitate carbon reduction strategies. CERius™ aims to assist energy companies, like Azito, in achieving net-zero goals by automating greenhouse gas data collection, providing scenario analysis, promoting team collaboration, and ensuring compliance with global emissions regulations, including recent mandates from the U.S. Securities and Exchange Commission (SEC). This deployment marks a significant step towards leveraging technology for sustainable energy practices and environmental stewardship.

Apr 02, 2024, Persefoni is recognized as leader in sustainability management software by Forrester, achieving highest scores in categories such as Audit & Compliance, Innovation, Market Presence, ROI calculation, Supplier engagement, Sustainability intelligence, & Vision. Platform, known for its Climate Management & Accounting capabilities, caters to enterprises and financial institutions seeking robust solutions for sustainability. Forrester's evaluation highlighted Persefoni's expertise in carbon accounting, data management, compliance, and decarbonization planning, emphasizing its strong vision for incorporating broader ESG reporting and enhancing financial modeling. This acknowledgment underscores Persefoni's pivotal role in advancing corporate sustainability initiatives worldwide.

Jun 14, 2024, Sphera has been recognized as a leader in carbon accounting and management software by IDC MarketScape's latest report. The assessment highlights Sphera's robust capabilities in providing granular carbon footprinting, including regional, building, asset, and product-level data. This acknowledgment underscores Sphera's commitment to offering comprehensive environmental, social, and governance (ESG) performance solutions, alongside risk management software and consulting services. The report's evaluation criteria encompassed six capability and strategy categories, incorporating vendor demonstrations, extensive questionnaire responses, and customer interviews, aiming to illuminate the evolving landscape of carbon accounting and management applications.

February 26, 2024. Yokogawa Electric Corporation launched OpreX Carbon Footprint Tracer, new solution under its OpreX Transformation lineup aimed at addressing carbon footprint management in process & manufacturing industries. This cloud-based service calculates CO2 emissions using data from instrumentation systems and power monitors, offering consultancy to devise strategies for emission calculation and reduction. Yokogawa's initiative provides comprehensive solution for visualizing and minimizing CO2 emissions, supporting companies in meeting their sustainability goals. Collaboration with SAP enhances capability to manage and mitigate environmental impacts effectively, marking significant step towards decarbonization in industrial sector.

Carbon Management Software Market Scope: Inquiry Before Buying

| Carbon Management Software Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 20.72 USD Billion |

| Forecast Period 2026-2032 CAGR: | 22.39% | Market Size in 2032: | 85.24 USD Billion |

| Segments Covered: | by Component | Software Services |

|

| by Deployment Mode | Cloud-Based On-Premises |

||

| by Enterprise Size | Small & Medium Enterprises (SMEs) Large Enterprises |

||

| by Application | Energy Management Greenhouse Gas Management Air Quality Management Sustainability Reporting Others |

||

| by End-User Industry | Power and Utilities Manufacturing Oil and Gas Transportation & Logistics Construction & Infrastructure IT & Telecommunications Others |

||

Carbon Management Software Market, by Region

North America (United States, Canada, Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (India, China, Japan, South Korea, Australia, ASEAN, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and Rest of ME & A)

South America (Brazil, Argentina, Columbia, and Rest of South America)

Carbon Management Software Market Key players:

- Intelex Technologies

- Persefoni

- Watershed Technology, Inc.

- Sinai Technologies

- Sphera

- ENGIE Impact

- IBM

- Microsoft

- Schneider Electric

- SAP

- Wolters Kluwer Enablon

- Ideagen EHS

- Normative (Denmark)

- Emitwise

- Vaayu Tech

- Workiva Carbon

- Net0

- Evalue8 Sustainability

- CarbonView

- Cority

- Greenly

- Plan A

- Sweep (France)

- GE Vernova (CERius)

- Pledge Earth Technologies Ltd

- Dakota Software Corporation

- Locus Technologies, Inc.

- EcoChain Technologies B.V.

- Trimble Inc.Other Key Players