Gaming Software Market Size by Purchase Type, Type, Technology, Application, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

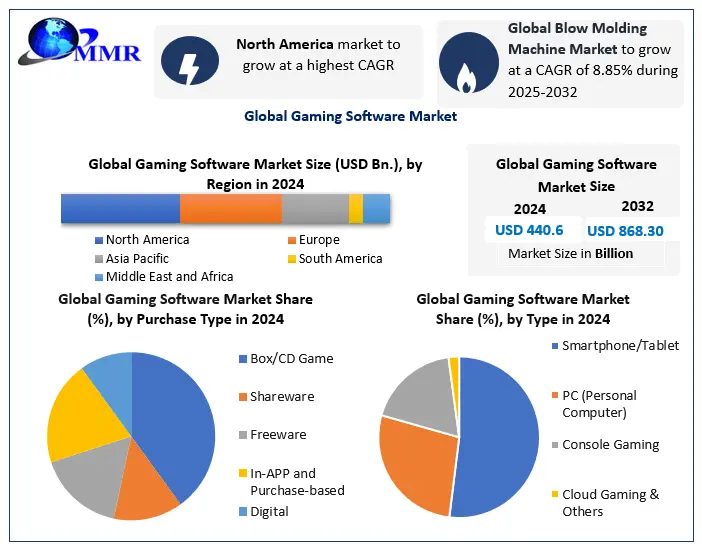

The Gaming Software market size was valued at USD 440.6 Bn. in 2024, and the Global Gaming Software Market revenue is expected to grow at a CAGR of 8.85% from 2025 to 2032, reaching nearly USD 868.30 Bn.

Overview

Gaming Software refers to computer programs and applications designated for playing video games on different platforms such as personal tablets, computers, mobile devices, gaming consoles and online platforms. These applications facilitate industry growth by providing developers with versatile game engines, development tools, and graphics software that streamline game creation, allowing for increasingly sophisticated and visually stunning experiences. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Gaming software applications are key driving factors for the growth of the gaming industry. The online distribution platforms and multiplayer services offered by gaming software expand accessibility, connecting gamers globally and fostering community engagement. Also, the rise of game streaming software has transformed gaming into a spectator sport, contributing to industry growth by attracting audiences beyond active players.

The increasing use of smartphones and the growing affordability of mobile data is a key driver for the Gaming Software Market growth. Mobile games now attract a massive user base spanning different age groups and demographics. This growth has led to a surge in demand for mobile gaming software that is optimized for various operating systems and devices.

Gaming Software Market Dynamics

Rise in E-Sports and Competitive Gaming to Drive the Market Growth

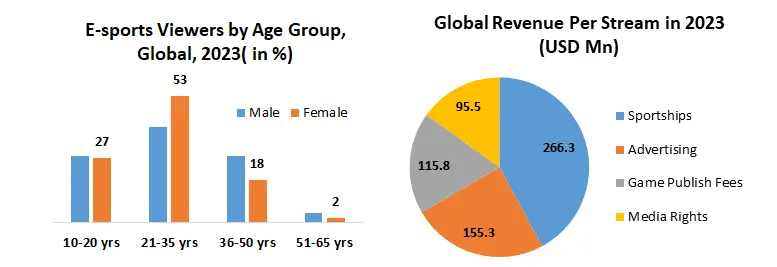

The surge in e-sports and competitive gaming has emerged as a significant growth driver for the global Gaming Software Market. It is a booming global industry where skilled video gamers play competitively. In fact, over 380 million people watch e-sports worldwide both online and in person. Gamers who live stream themselves as they play video games are referred to as "streamers." YouTube has made its biggest investment into e-sports to date, signing an exclusive multi-year broadcasting deal with gaming platform Faceit. Sony is partnering with gaming tournament organizer ESL to power Sony Playstation Vue, a 24-hour TV network dedicated to e-sports.

E-sports tournaments, where professional gamers compete on platforms such as League of Legends, Dota 2, and Counter-Strike, have gained popularity around the world. This growth is expected to increase viewership on platforms such as Twitch and YouTube Gaming, attracting sponsorships, advertising revenue, and even traditional sports investments. Also, as this sports ecosystem expands, demand for sophisticated gaming software increases. Developers are pushed to create cutting-edge titles with advanced graphics, seamless multiplayer capabilities, and spectator-friendly features, driving the demand for high-quality gaming software.

For Example, Meta announced that Oculus Publishing is now the largest publisher of virtual reality content in the gaming industry. Visitors to their booth learned that there are now over 500 titles in the Meta Quest Store and that 40 of those titles have grossed more than $10 million in revenue. In 2023, the most popular streaming services for listening to music, comedy, and podcasts are all around the world. Amazon Music, Spotify, Apple Music, Pandora, Tidal, Deezer, YouTube Music, Soundcloud, Sirius XM and iHeartRadio. According to Statista spotify was the most popular streaming platform accounting for 32% of streaming service users. Apple Music came second with 16% of the Gaming Software Market share.

Technological Advancements in Gaming Software to Boost the Market Growth

New technology emerges every day, and technology innovations such as augmented reality (AR), virtual reality (VR) and cloud gaming create lucrative opportunities for market growth. Developers are integrating augmented and virtual reality technologies into mobile and wearable games. Companies are blurring the line between gaming and experiences, adding in-game concerts, special events, and digital goods. The metaverse is a significant trend in this Gaming Software Market, influencing video game development. Facebook changing its name to Meta has brought this concept center stage, investing in more immersive virtual experiences. The AR/VR gaming market is expected to grow to $11B by 2030. For instance, the global Metaverse revenue opportunity could approach $800 billion in 2024 vs. about $500 billion in 2020, based on our analysis and Newzoo, IDC, PWC.

Metaverse Competitive Landscape

| Online Game Makers | Design Software Vendors | Social Networking | Gaming, AR & VR Hardware | Live Entertainment |

| Roblox | Unity | Live Nation | ||

| Epic Games | Epic Games | Tencent | Lenovo | Themo Parks |

| Microsoft | Adobe | - | HP | Sports Team |

| Activision Blizzard | Autodesk | - | Logitech | - |

| Electronic Arts | Ansys | - | Acer | - |

Cloud-based gaming, or gaming as a service (GaaS), refers to gaming content being delivered to users over the cloud and is expected to drive the Gaming Software Market growth across the world. Through this method, streaming services deliver game content to an app or web browser rather than installing games on a PC or console. All that's required is a secure internet connection. While this type of gaming has been around for a while, it has plagued infrastructure issues. Major players such as Microsoft, Google, and Amazon have stepped in and provided solutions for faster deployment and wider reach. Cloud gaming services allow players to stream games directly to their devices without the need for high-end hardware, broadening the market's reach to a wider audience. This shift towards cloud-based gaming requires sophisticated software to ensure smooth streaming, minimal latency, and high-quality visuals. As these technologies mature and become more accessible, the demand for innovative gaming software is set to rise.

Hardware Limitations and Upgrades to Restrain the Market Growth

High-quality gaming requires different advanced graphics cards, processors and sufficient memory. Evaluation of gaming software has sometimes outpaced the development of affordable hardware capable of running the latest games optimally. As a result, this creates a potential barrier for some gamers who may not be able to afford frequent hardware upgrades. The cost of staying up-to-date with the latest gaming hardware limits the market's growth potential, especially in regions where disposable income is limited. Also, established game publishers and developers often dominate the Gaming Software industry, making it difficult for newer entrants to gain a foothold. Such factors are responsible for the Gaming Software Market growth throughout the forecast period.

Gaming Software Market Segment Analysis

Based on Type, the smartphone/tablet segment dominated the largest Gaming Software Market share in 2024. Mobile gaming has grown exponentially, giving rise to a segment dedicated to mobile and casual gaming software. These applications encompass game development frameworks, user interface tools, and mobile-specific optimization solutions. The proliferation of smartphones has created a diverse market, ranging from simple puzzle games to complex mobile MMOs. However, PC (Personal Computer) Gaming: This segment encompasses gaming software developed for desktop and laptop computers. PC gaming offers high graphics quality and a wide variety of gaming genres, attracting hardcore gamers and esports enthusiasts.

Gaming Software Market Regional Analysis

North America held the largest market share in 2023 and is expected to sustain its position the in global market during the forecast period. The regional market growth is driven by the strong gaming culture, high disposable income and advanced technological infrastructure are key drivers responsible for growth. This region is majorly known for technological innovation and the key development of cutting-edge gaming software. For instance, Silicon Valley and various technology hubs help to create new gaming experiences such as virtual reality (VR), augmented reality (AR), and e-sports powerhouse. E-sports is the biggest tournament and league, attracting a massive audience and generating significant revenue.

The diverse gaming landscape in Europe is expected to boost gaming software market growth. Also, the UK, France, and Germany are major players, while Eastern Europe is also experiencing growth. However, stringent regulations related to loot boxes, microtransactions, and age ratings in some European countries impact the way gaming companies operate and monetize their products.

The Asia-Pacific region, especially countries including China, South Korea, and Japan, is at the forefront of the gaming software market. These nations have a rich gaming heritage, strong e-sports scenes, and a massive player base. Another mobile gaming is particularly prevalent in Asia, with a significant portion of the population engaging in mobile games. The region's embrace of smartphones and affordable data plans fuels this trend.

Competitive Analysis

The global gaming software market's competitive landscape is shaped by industry leaders including EA, Activision Blizzard, and Tencent Games, wielding extensive resources and diverse game portfolios to dominate the market. Innovators such as Epic Games and CD Projekt Red disrupt with ground breaking technologies and storytelling, while mobile gaming thrives through companies like NetEase Games and Niantic. Asia-Pacific powerhouses, indie developers, and strategic partnerships further enrich the landscape, while the evolution of esports and the emergence of new players underscore the market's dynamic nature. Success hinges on technological innovation, market understanding, and the delivery of captivating gaming experiences tailored to the diverse preferences of a global player base.

Gaming Software Market Scope Table: Inquire Before Buying

| Gaming Software Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 440.6 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 8.85% | Market Size in 2032: | USD 868.30 Bn. |

| Segments Covered: | by Purchase Type | Box/CD Game Shareware Freeware In-App and Purchase Based Digital |

|

| by Type | Smartphone/Tablet PC (Personal Computer) Console Gaming Cloud Gaming & Others |

||

| by Technology | Cloud Gaming Artificial Intelligence (AI) Augmented Reality (AR) & Virtual Reality (VR) |

||

| by Application | Action & Adventure Games Role-Playing Games (RPG) Sports Games Racing Games Simulation Games Others |

||

Gaming Software Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&A)

Gaming Software Key Players are:

1. Nvidia Computer Game Company

2. Valve Corporation, Nexon Co, Ltd.

3. Bethesda Softworks LLC

4. Ubisoft Entertainment S.A.

5. Nintendo Co., Ltd.

6. Electronic Arts Inc.

7. Rockstar Games Inc.

8. Gameloft

9. Activision Blizzard

10. Tencent Games

11. Sony Interactive Entertainment

12. Microsoft Game Studios

13. NetEase Games

14. Take-Two Interactive Software

15. Square Enix

16. Niantic

17. Epic Games

18. CD Projekt Red

19. Konami

20. Capcom

Frequently Asked Questions:

1] What is the growth rate of the Global Gaming Software Market?

Ans. The Global Gaming Software Market is growing at a significant rate of 8.85% during the forecast period.

2] Which region is expected to dominate the Global Gaming Software Market?

Ans. North America is expected to dominate the Gaming Software Market during the forecast period.

3] What is the expected Global Gaming Software Market size by 2032?

Ans. The Gaming Software Market size is expected to reach USD 868.30 Bn by 2032.

4] Which are the top players in the Global Gaming Software Market?

Ans. The major top players in the Global Gaming Software Market are Niantic, Epic Games, CD Projekt Red, Konami, and others

5] What are the factors driving the Global Gaming Software Market growth?

Ans. The increasing technology development in gaming software is driving the Gaming Software market.