Europe Virtual Data Room Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Country-wise Growth Analysis and Identification, Competitive Positioning Review & Market Size Forecast to 2030

Overview

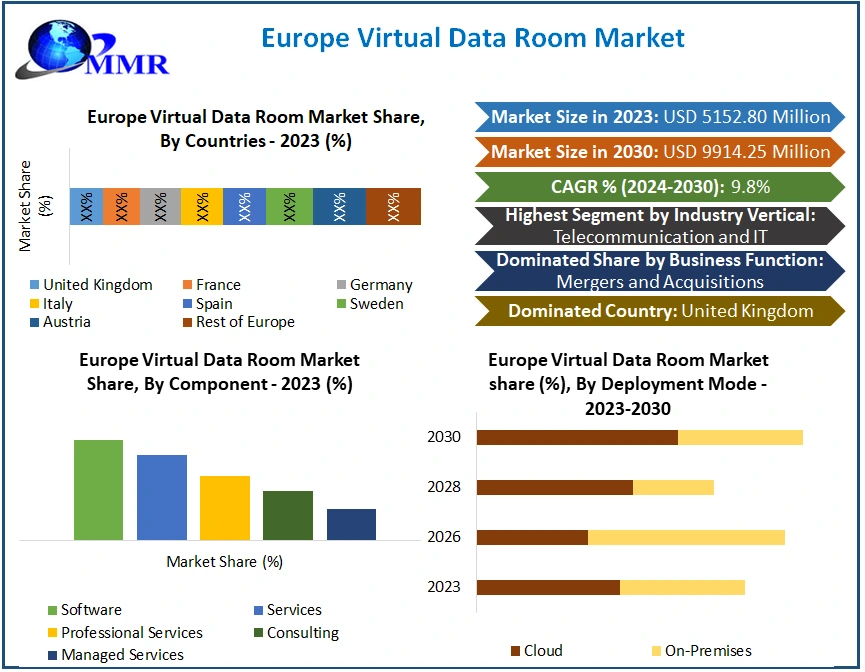

The Europe Virtual Data Room Market size was valued at USD 5152.80 Million in 2023 and the total Europe Virtual Data Room revenue is expected to grow at a CAGR of 9.8% from 2024 to 2030, reaching nearly USD 9914.25 Million by 2030.

The Europe Virtual Data Room market is experiencing robust growth driven by increasing demand for secure and efficient data management solutions across various industries. A virtual data room is an online repository used for storing and sharing sensitive documents and information securely, particularly during mergers, acquisitions, and other corporate transactions. In Europe, the adoption of VDRs is on the rise, particularly in key sectors such as finance, legal, and real estate, where confidentiality and compliance are vital. The market in Europe is characterized by stringent data protection regulations, including the General Data Protection Regulation (GDPR), which mandates organizations to ensure the secure handling of personal data. As a result, businesses are increasingly turning to VDR solutions that comply with these regulations to safeguard sensitive information and mitigate risks of data breaches and non-compliance fines. This factor positively benefits the Europe virtual data room market.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

In addition, the surge in mergers, acquisitions, and corporate transactions across the region necessitates the need for secure platforms like VDRs to facilitate due diligence, negotiations, and deal completion. This factor further drives the Europe virtual room market growth. Besides that, the increasing trend towards remote work and virtual collaboration, accelerated by the COVID-19 pandemic, has heightened the demand for digital solutions for document sharing and collaboration, further influencing the Europe virtual data room market. VDRs enable remote teams to access and collaborate on documents securely from anywhere, thereby enhancing efficiency and productivity. Additionally, the emphasis on data security and compliance with regulatory requirements, such as GDPR, is driving organizations to invest in VDR solutions with robust security features, including encryption, access controls, and audit trails. The growing awareness of the importance of data privacy among businesses and consumers alike is further fueling the adoption of VDRs as a trusted solution for protecting sensitive information, thereby supporting the virtual room market in Europe region.

Europe offers a diverse landscape with varying regulatory environments, industry sectors, and technological advancements. Countries such as the United Kingdom, Germany, France, etc. are key markets for VDR providers, given their strong economies, thriving M&A activity, and emphasis on data security and privacy. The Europe virtual room market is characterized by the presence of established VDR providers as well as emerging players offering innovative solutions to cater to the evolving needs of businesses. Hence, the Europe Virtual Data Room market is poised for continued growth, driven by ongoing digital transformation initiatives, increasing regulatory scrutiny, and the need for secure and compliant data management solutions in an increasingly interconnected world.

Europe Virtual Data Room Market Dynamics:

Increasing Mergers and Acquisitions Activity in Europe

Europe has been witnessing a steady rise in mergers, acquisitions, and other corporate transactions across various industries. The surge in mergers, acquisitions, and corporate transactions across diverse industries in Europe has rapidly increased demand for secure, efficient, and compliant data-sharing platforms like Virtual Data Rooms (VDRs), thereby this factor is expected to be the major factor driving the Europe virtual data room market growth. These transactions involve intricate processes such as due diligence, negotiations, and deal finalization, necessitating the seamless exchange of sensitive information among involved parties.

Top M&A Deals By Value In The European Power Industry Since 2022

| Target | Acquirer | Deal value | Date Announced | Deal Type |

| Power Grid Unit | Government of Germany | $21000m | February, 2023 | Asset Transaction |

| ContourGlobal | Cretaceous Bidco | $6140m | May, 2022 | Acquisition |

| Hornsea 2 Wind Project | AXA Investment Managers; Credit Agricole Assurances | $3953m | March, 2022 | Asset Transaction |

| Siemens Gamesa Renewable Energy | Siemens Energy | $3331m | May, 2022 | Acquisition |

| Nature Energy Stovring | Shell Petroleum | $2000m | November, 2022 | Acquisition |

Traditional methods of document sharing and collaboration are often inadequate to meet the stringent security and compliance requirements associated with these transactions. Hence, companies increasingly turn to VDRs as a reliable solution to facilitate these processes while ensuring confidentiality, integrity, and regulatory compliance of the shared data. This factor significantly impacts the Europe virtual data room market by driving a surge in demand for VDR solutions tailored to the unique needs of mergers, acquisitions, and corporate transactions. Businesses seek VDR providers that offer robust security features, such as encryption, access controls, and audit trails, to safeguard sensitive information throughout the deal lifecycle.

As the frequency and complexity of corporate transactions continue to escalate in Europe, the role of VDRs in facilitating secure and efficient data sharing becomes increasingly pivotal. Europe VDR market players are compelled to innovate and enhance their offerings to meet the evolving needs of businesses engaged in mergers, acquisitions, and other transactions. This dynamic landscape presents opportunities for VDR providers to differentiate themselves by delivering cutting-edge features, superior user experience, and robust compliance capabilities. Ultimately, the rising demand for VDRs driven by the surge in corporate transactions underscores their indispensable role in the European business ecosystem, propelling growth and innovation in the Europe virtual data room market.

Stringent Data Privacy Regulations In Europe

The stringent data privacy regulations such as the General Data Protection Regulation (GDPR) in Europe significantly impact the Europe virtual data room market. Companies operating or dealing with European data are obligated to comply with GDPR's strict requirements regarding the handling and protection of personally identifiable information (PII). Failure to adhere to these regulations results in severe penalties, including fines amounting to €20 million or 4% of the company's global annual revenue, whichever is higher. This potential financial risk serves as a significant deterrent for businesses, regardless of their size, compelling them to ensure that their VDR solutions are GDPR-compliant.

Data Protection Regulations Governing Virtual Data Rooms In Europe

| Regulation | Description | Applicability |

| General Data Protection Regulation (GDPR) | Comprehensive EU regulation governing the protection and privacy of personal data. It imposes strict requirements on data handling, security, and compliance. | Applies to all EU member states and any organization processing the personal data of EU residents. |

| Data Protection Act 2018 (UK) | UK legislation aligned with GDPR, regulating the processing and protection of personal data. | Applicable to organizations operating in the UK. |

| Federal Data Protection Act (BDSG) (Germany) | German law implementing GDPR and setting additional requirements for data processing within the country. | Applicable to organizations operating in Germany. |

| French Data Protection Act (France) | French legislation governing the processing and protection of personal data, in alignment with GDPR principles. | Applicable to organizations operating in France. |

| Dutch Data Protection Act (Netherlands) | Dutch law implementing GDPR and setting specific provisions for data protection and privacy within the Netherlands. | Applicable to organizations operating in the Netherlands. |

Moreover, non-compliance with GDPR and other data privacy regulations leads to a loss of trust and credibility among stakeholders, including shareholders, clients, and the general public. Shareholders perceive non-compliance as a threat to the company's profitability and sustainability, potentially impacting investment decisions. Clients, on the other hand, hesitate to engage with businesses that demonstrate a disregard for data privacy regulations, fearing potential breaches of their sensitive information. In the Europe virtual data room market, any suggestion of failing to comply with data privacy and security standards leads to substantial harm to a company's reputation, given the heightened importance of these concerns in the current landscape. Therefore, ensuring regulatory compliance is not just a legal obligation but also a crucial business requirement for virtual data room providers in Europe.

Europe Virtual Data Room Market Country Analysis:

As a leading financial center in Europe, the United Kingdom witnessed a robust demand for VDR solutions, particularly in the finance, legal, and real estate sectors. As a result, the U.K. dominated the Europe virtual data room market with the highest market share of 33.45% in 2023 and is expected to maintain its dominance by 2030. The implementation of stringent data protection laws, particularly the Data Protection Act 2018 and adherence to GDPR standards, has propelled the adoption of VDRs that ensure the safe handling of sensitive information. Additionally, Brexit has catalyzed shifts in data management strategies, prompting businesses to prioritize VDR solutions capable of facilitating seamless cross-border data exchange amid evolving regulatory landscapes.

Germany, renowned for its robust industrial base and staunch commitment to data security, is expected to offer lucrative potential for virtual data room service providers in Europe. The country's stringent regulatory framework, including the Federal Data Protection Act (BDSG) and GDPR compliance requirements, drives businesses to seek VDR solutions equipped with advanced encryption, access controls, and audit capabilities. Germany's thriving M&A activity, particularly within the manufacturing and technology sectors, further amplifies the demand for VDRs tailored to support due diligence processes and secure deal negotiations. Thus, all of these factors positively support the German virtual data room market and increase the Europe virtual data room market size.

With a diverse economic landscape spanning industries such as automotive, aerospace, and luxury goods in France, is further influencing the Europe virtual data room market. The French Data Protection Act underscores the country's commitment to data privacy, incentivizing businesses to adopt secure VDR solutions for document management and collaboration. Moreover, the increasing digitization of administrative processes and government initiatives aimed at fostering entrepreneurship contribute to the growth of the VDR market in France, as organizations seek efficient and compliant data-sharing platforms.

Scope of the Europe Virtual Data Room Market :Inquire before buying

| Europe Virtual Data Room Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 5152.80 Mn. |

| Forecast Period 2024 to 2030 CAGR: | 9.8% | Market Size in 2030: | US $ 9914.25 Mn. |

| Segments Covered: | by Component | Software Services Professional Services Consulting Managed Services |

|

| by Deployment Mode | Cloud On-premises |

||

| by Organization Size | Large Enterprises Small and Medium-Sized Enterprises (SMEs) |

||

| by Business Function | Mergers and Acquisitions Marketing and Sales Compliance and Legal Finance Workforce Management Others |

||

| by Industry Vertical | Telecommunication and IT BFSI Retail and E-commerce Government Healthcare and Life Sciences Real Estate Others |

||

Europe Virtual Data Room Market by European Countries:

1. United Kingdom

2. France

3. Germany

4. Italy

5. Spain

6. Sweden

7. Austria

8. Rest of Europe

Leading Europe Virtual Data Room Market Key Players:

1. Drooms GmbH (Germany)

2. Ethos Data Room (United Kingdom)

3. Datasite France S.A.R.L. (France)

4. Trusted-Colo GmbH & Co. KG c

5. Uniscon GmbH 2024 Uniscon GmbH 2024

6. Drooms(Munich)

7. Circana (United Kingdom)

8. Ansarada (London)

9. SecureDocs (United Kingdom)

10. Dealroom. co (Netherlands)

FAQs:

1. What are the growth drivers for the Europe Virtual Data Room market?

Ans. Increasing mergers and acquisitions activity, rising demand for secure data-sharing solutions, and stringent data protection regulations such as GDPR are expected to be the major drivers for the Europe Virtual Data Room market.

2. What are the major restraints for the Europe Virtual Data Room market growth?

Ans. Rising concerns about data security, compliance challenges with evolving regulations, and potential resistance to adopting new technologies among certain industries are major restraints for the Europe Virtual Data Room market growth.

3. Which Country is expected to lead the Europe Virtual Data Room market during the forecast period?

Ans. The United Kingdom is expected to lead the Europe Virtual Data Room market during the forecast period.

4. What is the projected market size and growth rate of the Europe Virtual Data Room Market?

Ans. The Europe Virtual Data Room Market size was valued at USD 5152.80 Million in 2023 and the total Europe Virtual Data Room revenue is expected to grow at a CAGR of 9.8% from 2024 to 2030, reaching nearly USD 9914.25 Million by 2030.

5. What segments are covered in the Europe Virtual Data Room Market report?

Ans. The segments covered in the Europe Virtual Data Room market report are Component, Deployment Mode, Organization Size, Distribution Channel, Business Function, Industry Vertical, and Region.