Digital Payment Market Size by Component, Payment Type, Deployment, Technology, Transaction Size, Enterprise Size, End Use, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

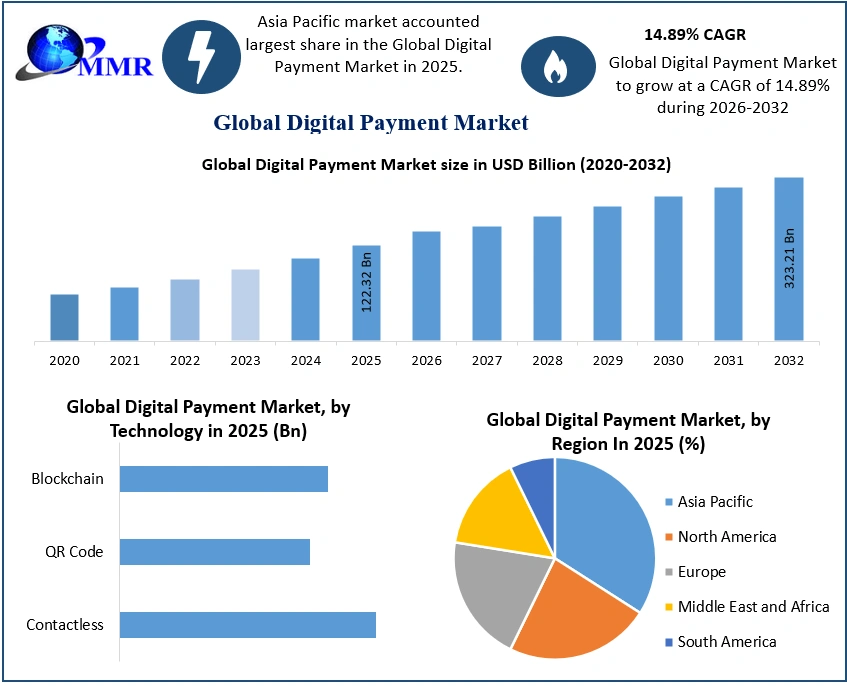

The Digital Payment Market size was valued at USD 122.32 Billion in 2025 and the total Digital Payment revenue is expected to grow at a CAGR of 14.89% from 2025 to 2032, reaching nearly USD 323.21 Billion by 2032.

The MMR report provides an extensive overview of innovation and future trends shaping the Digital Payment Market, covering emerging technologies such as AI-powered conversational payments, blockchain-based DeFi solutions, biometric and voice authentication, digital ID, eKYC advancements, and open banking integrations within IoT ecosystems. It also includes a detailed pricing and revenue analysis, examining interchange fees, MDR, regional pricing variations, and evolving SaaS-based monetization models of digital wallets and super apps. Additionally, the report analyzes consumer and merchant behavior, highlighting key user demographics, motivators, retention trends, and operational challenges. Furthermore, it evaluates ESG and financial inclusion impacts, focusing on digital payment adoption in rural and underserved regions, environmental sustainability through paperless transactions, and gender inclusion metrics in digital access.

Digital Payment Market Overview:

Digital payments are payments made through digital or online channels that do not entail the exchange of actual currency. This type of payment, also known as an electronic payment (e-payment), is the transfer of value from one payment account to another in which both the payer and the payee utilize a digital device such as a mobile phone, computer, or credit, debit, or prepaid card. A firm or an individual might be the payer and payee. This means that in order for digital payments to take place, both the payer and the payee must have a bank account, an online banking method, a device from which to make the payment, and a medium of transmission, which means they must have signed up to a payment provider or an intermediary such as a bank or a service provider. UPI, NEFT, AEPS, mobile wallets, and PoS terminals are all examples of digital payment methods. UPI is the most popular method in digital payment market, with transactions exceeding USD 1 trillion in value.

The switch to digital payments and receipts offers some obvious advantages, particularly for small enterprises. Consumers and companies are now expecting digital payments to be accessible for faster and more secure payments with no risk or fees. The payer possesses a mobile phone, which allows for further validation by fingerprint or other verification or biometric approach, so reducing risk. Going cashless has various advantages for commercial transactions as well. Cash management is no longer required, lowering the danger of theft and lowering the expense of security and storage majorly drives the growth of digital payment market. Digital payments are frequently faster transactions, resulting in shorter lines and boosting the customer's in-store experience. Thus, customer convenience drives purchases. A clear trail is accessible for easy accounting, assisting in the simplification of operations and tax compliance.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Digital Payment Market Dynamics

Initiatives for the Promotion of Digital Payments:

Countries worldwide are leveraging ICT technology to enhance the Digital Payment Market, with governments actively pursuing initiatives to automate payment processes. The Digital Payment Market stands out as a crucial driver for economic growth in nations, offering the potential to elevate productivity, enhance transparency, and boost tax revenue, foster financial inclusion, and present users with expanded economic choices. In India, the government has taken several steps to incentivize Digital Payments, including the Digital India initiative, the introduction of the Unified Payments Interface (UPI), and the establishment of the 14444-helpline number, all serving as catalysts for the shift towards the market.

These endeavours play a pivotal role in advancing Digitalization and spreading awareness regarding the advantages of embracing new technologies in the market. Similarly, countries such as Singapore and Australia have embarked on diverse Digital Payment projects. The Monetary Authority of Singapore (MAS) actively encourages consumers and businesses to embrace Digital Financial Services and ePayments in the Digital Payment Market. This recommendation gained prominence in response to the COVID-19 pandemic, aiming to implement heightened safety measures, including limiting visits to Financial Institutions' premises and further driving the market forward. Rapid Decline in Unbanked Population:

Rapid Decline in Unbanked Population:

A significant portion of the global population resides in rural and remote areas, facing challenges related to connectivity and digital literacy, particularly in the underserved Digital Payment Market. Recognizing the value of extending financial services to this vast population, governments, development organizations, and private-sector entities are now focusing on bridging this gap within the market. Consequently, more individuals in rural and isolated areas are gaining access to financial services, marking a notable expansion within the market.

Governments initiated various projects to connect these populations, aiming to promote financial inclusion within the Digital Payment Market. In India, for example, the World Bank's 2018 data showed that approximately 190 million individuals lacked bank accounts, highlighting the existing gaps within the Digital Payment Market. However, due to concerted efforts and initiatives by the Indian government, the percentage of people with bank accounts increased from 53% in 2014 to 80% in 2017, showcasing a positive transformation within the market.

Moreover, according to the MMR findings, the global percentage of adults with bank accounts rose from 61% in 2014 to 69% in 2018, indicating a broader reach within the Digital Payment Market. Digital payments played a crucial role in expanding the reach of bank accounts within the market, as the payment bank feature enabled individuals to create and operate accounts using mobile phones, even in remote areas. The adoption of digital wallets significantly impacted financial inclusion within the market, contributing to a decline in the number of unbanked individuals worldwide. This trend created an opportune environment for digital payment companies to expand their client base within the evolving Digital Payment Market.

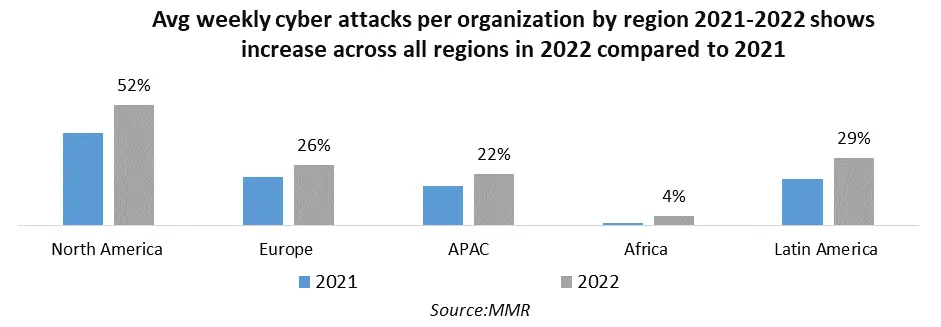

Evolving Cyber Attacks on Digital Payments

Cyber-attacks present a substantial obstacle to the growth of the Digital Payment Market, constituting the most severe challenges faced by the payment sector in an extended period. The escalating use of Digital Payment Systems also introduces cybersecurity threats such as cyber theft and fraud within the market. The acceptance of payment technologies and their integration into enterprises has sparked concerns regarding privacy, theft, and regulatory compliance within the market. Businesses grapple with the impact of emerging cyber assaults utilizing mobile malware to infiltrate Digital Payment Systems and pilfer cardholder data. Evolving scams, including friendly fraud, affiliate fraud, botnets, phishing, velocity attacks, and triangulation, further compound the risks within the Digital Payment Market.

As per the Central Statistics Office (CSO), the annual loss from cyber assaults is expected to reach USD six trillion by 2022, a significant increase from USD three trillion in 2015, indicating potential financial ramifications for the Digital Payment Market. Additionally, the Association for Financial Professionals (AFP) Payments Fraud and Control Survey Report for 2020 revealed that over 81% of global firms experienced cyber assaults in 2019, highlighting the pervasive nature of these threats within the Digital Payment Market. Consequently, the heightened frequency of cyber assaults is expected to impede the widespread adoption of Digital Payment Systems. Furthermore, in line with the 2018 AFP Payments Fraud and Control Survey Report, more than 86% of firms encountered cyber-attacks, underscoring the persistent challenges faced by the market. Thus, the escalating instances of cyber assaults are foreseen to hinder the adoption of Digital Payment Systems and services.

Lack of Global Standards for Cross-Border Payments:

Year after year (YoY), the volume of cross-border commerce has been on the rise, with more companies engaging in the purchase of products and services from around the world. Despite this growth, digital payment providers within the Digital Payment Market face challenges in capitalizing on this potential, primarily due to the absence of global payment systems that offer user-friendly simplicity within the Digital Payment Market, the lack of standardized global practices within the market, and varying government restrictions in different nations affecting the market. Cross-border payments within the Digital Payment Market are hindered by diverse payment rules and data storage requirements that vary from country to country, leading to inefficiencies within the market. Moreover, the domestic payment infrastructure is ill-suited for handling cross-border transactions in the market.

Over the past few decades, several countries within the Digital Payment Market have developed both high- and low-value payment systems, each based on proprietary communication and security standards within the Digital Payment Market. However, as these payment systems evolve independently within the market, there is a growing need for standardization and automation across inter-bank and intra-bank networks spanning different nations within the Digital Payment Market. This lack of standardization and automation has adverse effects on banks and businesses within the Digital Payment Market, often requiring direct intervention for the collection and restoration of data within the market. Intra-bank transactions within the Digital Payment Market enable major banks with subsidiaries and branches to transfer funds to destination nations within the market, where beneficiaries are either promptly credited in their foreign operation accounts within the market, or payments are routed to their banks through bilateral transfers or national clearing and settlement procedures within the Digital Payment Market.

Digital Payment Market Segment Analysis

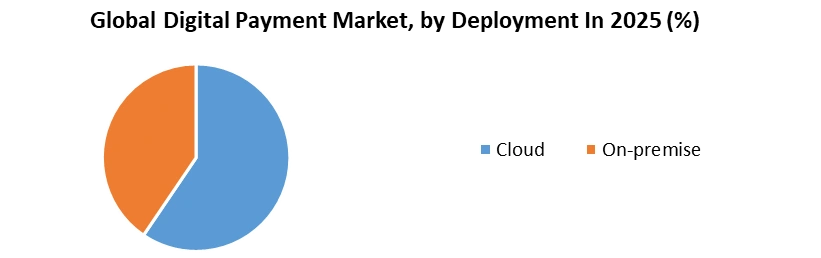

Based on Deployment, in 2025, the Digital Payment Market is segmented into Cloud and On-premise. The Cloud segment holds the dominant Digital Payment Market share, driven by its scalability, cost efficiency, and ability to support real-time payment processing and data analytics. Increasing adoption of SaaS-based payment platforms and integration with AI and API-driven ecosystems further enhance its growth. The On-premise segment continues to serve organizations prioritizing data security, regulatory compliance, and full control over infrastructure—particularly in large financial institutions and government bodies with stringent data governance requirements.

Based on End Use, in 2025, the Digital Payment Market is segmented into BFSI, Healthcare, IT & Telecom, Media & Entertainment, Retail & E-commerce, Transportation, and Others. The BFSI sector dominates the market due to widespread integration of digital banking, mobile wallets, and instant payment systems. Retail & E-commerce follows closely, driven by booming online shopping and consumer preference for secure, seamless payment gateways. IT & Telecom leverage digital payments for subscription models and service automation, while the Healthcare sector is increasingly adopting online billing and telemedicine payment platforms. Media & Entertainment benefit from the rise in digital content subscriptions and in-app purchases, whereas Transportation sees growing use of contactless and mobile ticketing systems. The Others segment, including education and government services, is expanding steadily with ongoing digitization initiatives.

Based on End Use, in 2025, the Digital Payment Market is segmented into BFSI, Healthcare, IT & Telecom, Media & Entertainment, Retail & E-commerce, Transportation, and Others. The BFSI sector dominates the market due to widespread integration of digital banking, mobile wallets, and instant payment systems. Retail & E-commerce follows closely, driven by booming online shopping and consumer preference for secure, seamless payment gateways. IT & Telecom leverage digital payments for subscription models and service automation, while the Healthcare sector is increasingly adopting online billing and telemedicine payment platforms. Media & Entertainment benefit from the rise in digital content subscriptions and in-app purchases, whereas Transportation sees growing use of contactless and mobile ticketing systems. The Others segment, including education and government services, is expanding steadily with ongoing digitization initiatives.

Digital Payment Market Regional Analysis

In 2025, North America asserted its dominance in the global Digital Payment Market, commanding over 34.0% of total sales. The regional Digital Payment Market experienced a surge, driven by factors like increased deployment and technological advancements in smart parking meters. An illustrative example is the collaboration between ParkMobile, a market parking solution provider, and EasyPark, a facilities service provider, in July 2020. This partnership facilitated contactless payments across Vancouver, contributing to the regional Digital Payment Market boost. Additionally, the United States witnessed a rise in unmanned establishments, further fueling the demand for Digital Payment Market solutions.

Ahold Delhaize, a Dutch supermarket chain, exemplified this trend in November 2019 by establishing a cashier-less shop in the United States, contributing to the diversification of the Digital Payment Market. Europe is poised for significant growth throughout the forecast period, with banks in the region actively working on a European Digital Payment Market initiative to establish a unified payments system for retailers and customers across the area. Such initiatives are expected to create new development prospects for the market in the coming years. Moreover, the Italian government's digital drive to expand electronic payments is acting as a catalyst for regional Digital Payment Market growth.

In the Asia-Pacific region, digital wallets have emerged as the most popular payment option for both e-commerce and point-of-sale (POS) transactions within the Market. During the forecast period, it is expected that digital wallet payments will constitute three-quarters of e-commerce payment methods and over half of POS payments in the Asia-Pacific market. Although the transaction value of e-commerce payments currently surpasses that of POS payments within the market, this discrepancy is projected to narrow in the future years. Additionally, digital remittances, while a relatively small portion of market transactions, hold significance for many Asian customers who value the ability to send money to family and friends. The Asia-Pacific Digital Payment Market area is predicted to experience rapid growth during the forecast period, showcasing diverse markets in terms of Market usage rate, user demographics, and preferred payment methods.

China stands out in the Asia-Pacific Digital Payment Market region, boasting the highest number of digital payment users and the greatest mobile proximity payment penetration rate. In the last year, China recorded over 3,000 billion US dollars in Market transactions, with digital wallets dominating both e-commerce and POS payments. Other notable contributors to the market in the Asia-Pacific region include Japan, South Korea, and India. In Japan and South Korea, credit cards lead as the most popular payment method for both e-commerce and POS purchases within the market. In contrast, India predominantly relies on cash for POS transactions, while digital wallets take precedence in e-commerce transactions within the Market. Notably, more mature markets such as South Korea, Japan, and New Zealand have witnessed a higher adoption of digital payments among their older population, showcasing the evolving landscape across diverse Market economies.

Digital Payment Market Scope: Inquiry Before Buying

| Global Digital Payment Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 122.32 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 14.89% | Market Size in 2032: | USD 323.21 Bn. |

| Segments Covered: | by Component | Solution Payment Gateway Solutions Payment Processing Solutions Payment Wallet Solutions Payment Security & Fraud Management Solutions Point of Sale (POS) Solutions Services Professional Services Consulting Implementation Support and Maintenance Managed Services |

|

| by Payment Type | Mobile Payment Proximity Payment Remote Payment Online Banking Point of Sale Debit Card @POS Credit Card @POS NFC Card Digital wallet |

||

| by Deployment | Cloud On-premise |

||

| by Technology | Contactless QR Code Blockchain |

||

| by Transaction Size | Domestic Cross-Border |

||

| by Enterprise Size | Large Enterprises Small & Medium Enterprises |

||

| by End Use | BFSI Healthcare IT & Telecom Media & Entertainment Retail & E-commerce Transportation Others |

||

Digital Payment Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Digital Payment Market, Key Players:

1. Google LLC

2. Samsung Electronics

3. Alipay

4. WeChat Pay

5. Apple Inc.

6. PayPal

7. Venmo

8. Cash App

9. Amazon

10. Paytm

11. PhonePe

12. Google Payment

13. Mercado PagoGCash

14. TWINT

15. KakaoPay

16. PicPay

17. Revolut Ltd.

18. N26 GmbH

19. Monzo

20. Grab

21. Gojek

22. LINE Corporation

23. Ascend Group

24. Adyen

25. PayMaya

26. GCash

27. MoMo

28. bKash

29. MTN Group Management Services

30. Orange

31. Others

FAQs:

1] What segments are covered in the Market report?

Ans. The segments covered in the Market report are based on Component, Payment Type, Deployment, Technology, Transaction Size, Enterprise size, End Use and region

2] Which region is expected to hold the highest share of the Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Market.

3] What is the market size of the Market by 2032?

Ans. The market size of the Market by 2032 is USD 323.21 Bn.

4] What is the growth rate of the Market?

Ans. The Global Market is growing at a CAGR of 14.89% during the forecasting period 2026-2032.

5] What was the market size of the Market in 2025?

Ans. The market size of the Market in 2025 was USD 122.32 Bn.