Agricultural Drone Market Size by Type, Component, Payload Capacity, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

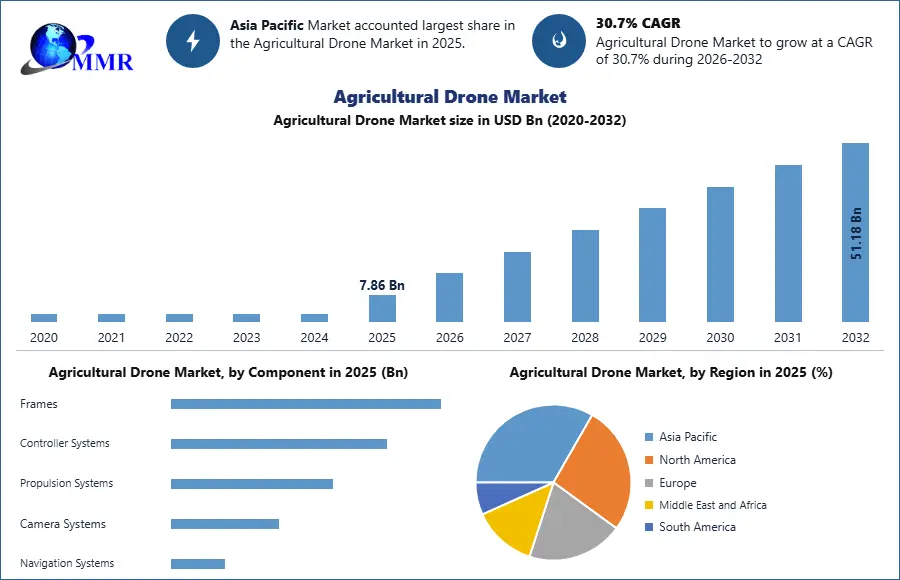

Agricultural Drone Market size was valued at USD 7.86 Bn in 2025, and the total Agricultural Drone Market revenue is expected to grow at a CAGR of 30.70% from 2026 to 2032, reaching nearly USD 51.18 Bn by 2032.

Agricultural Drone Market Overview

An agricultural drone is an unmanned aerial vehicle (UAV) equipped with advanced sensors, cameras, and spraying systems designed to optimize farming operations. It enables precision agriculture by monitoring crop health, spraying fertilizers/pesticides, mapping fields, and analyzing soil conditions, improving efficiency, yield, and sustainability. The demand for agricultural drones is rising due to their ability to enhance farm productivity, reduce labor costs, and support precision farming. Meanwhile, supply is increasing as manufacturers develop more advanced, affordable, and regulatory-compliant drones to meet growing farmer needs.

The Asia-Pacific dominated the agricultural drone market in 2025, driven by large-scale farming in China, Japan, and India. Key players include DJI (China), XAG (China), Parrot (France), AgEagle (U.S.), and Yamaha Motor (Japan), leading in innovation and market share. The report covered the Agricultural Drone Market's segments (Type, Component, Payload Capacity, Application, and Region). Data has been provided by market participants, and regions (North America, Asia Pacific, Europe, Middle East & Africa, and South America). It provides a thorough analysis of the rapid advances that are currently taking place across all industry sectors.

To know about the Research Methodology:-Request Free Sample Report

Agricultural Drone Market Dynamics

Agricultural Drone Market Trends

1. Rising Adoption of Precision Farming

• Drones equipped with multispectral, thermal, and hyperspectral sensors help farmers monitor crop health, soil conditions, and irrigation needs.

• AI-powered analytics enable data-driven decision-making, optimizing pesticide, fertilizer, and water usage.

2. Government Support & Subsidies

• Countries like India, China, and the U.S. are promoting drone use in agriculture through subsidies and training programs.

• Example: India’s “Kisan Drone” scheme provides financial aid to farmers for drone purchases.

3. Shift Toward Autonomous & AI-Integrated Drones

• AI and machine learning are being used for real-time crop disease detection, yield prediction, and automated spraying.

• Companies like DJI, AgEagle, and Parrot are launching fully autonomous drones for field mapping and spraying.

4. Increased Use of Spraying Drones

• LiDAR and GPS-enabled drones are improving spraying accuracy, reducing chemical wastage by up to 30%.

• China leads in spraying drone adoption, with companies like XAG and DJI dominating the market.

Precision Farming Demand and AI Integration to Boost Agricultural Drone Market Growth

The agricultural drone market is driven by the increasing need for precision farming, enabling efficient crop monitoring, soil analysis, and targeted spraying. AI-managed drones provide real time data analytics, improve yield adaptation and reduce input costs. Government subsidy (e.g., India’s Kisan Drone Scheme) and labor shortages further accelerate adoption. Advanced sensors (multispectral, LiDAR) enhance field mapping accuracy, while autonomous drone streamlines operations. Along with prominent players such as DJI and XAG leading innovation, permanent farming and smart agricultural fuel demand. Demand and climate challenges of global food push farmers towards drone-based solutions, making them essential for modern agriculture.

High Costs and Regulatory Hurdles to Hamper Widespread Drone to Restrain Agricultural Drone Market

Despite the development, the agricultural drone market faces restrictions including high early investment (drone, sensor, software) and operating costs. Limited battery life (20–40 minutes) restrictions massive use, while complex rules (BVLOS restriction, pilot licensing) delayed deployment. Data security concerns and obstructing adopting lack of technical expertise among farmers. In developing areas, poor connectivity and infrastructure limit. Additionally, resistance to new technologies in traditional agricultural communities slows down the market. These challenges should be addressed to unlock the full capacity of agricultural drones.

Drone-as-a-Service (DaaS) and Emerging Markets to Create Agricultural Drone Market Opportunity

The Drone-as-a-Service (DaaS) model presents a major opportunity, allowing small farmers to access drone technology affordably. Emerging markets (Africa, Latin America) offer untapped potential due to increasing agritech investments. Advances in swarm drone technology and solar-powered drones could enhance efficiency. AI and 5G integration will enable real-time data processing, while government initiatives (e.g., FAA/EASA approvals) will expand commercial use. Partnerships between agritech firms and drone manufacturers (e.g., John Deere & Blue River) will drive innovation. Sustainable farming trends and carbon credit incentives may further boost adoption, positioning drones as a key tool in future agriculture.

Agricultural Drone Market Segment Analysis

Based on Payload Capacity, the Agricultural Drone Market is segmented into Lightweight drones (up to 2kg), Medium-weight drones (2 to 10kg), and Heavy-weight drones (Above 10kg –up to 25kg). Medium-weight drones (2 to 10kg) segment dominated the Agricultural Drone Market in 2024 and is expected to hold the largest market share over the forecast period. Dominance is due to an optimal balance between payload capacity, strength, and operational efficiency. These drones are versatile enough to handle key farming tasks like crop spraying, multispectral imaging, and field mapping, while remaining cost-effective for small to mid-sized farms.

Unlike lightweight drones (limited to basic scouting) or heavy-weight drones (expensive and complex), medium-weight models offer longer flight times, higher spray capacity (5–10L), and compatibility with advanced sensors, making them ideal for precision agriculture. Prominent players like DJI (Agras T30/T40) and XAG (P Series) dominate this segment, with automatic spraying and adoption through AI-operated analytics. Their widespread use in Asia (China, India) and North America strengthens their market dominance.

Based on Application, Agricultural Drone Market is segmented into Precision Farming, Field Mapping, Livestock Monitoring, Crop Scouting and Others. Precision Farming segment dominated the Agricultural Drone Market in 2024 and is expected to hold the largest market share over the forecast period. The precision farming segment leads the agricultural drone market, as drones equipped with multispectral sensors, AI analytics, and variable-rate spraying systems enable data-driven decisions to maximize crop yields while minimizing input costs.

Unlike standalone applications like field mapping or livestock monitoring, precision farming integrates real-time crop health analysis, targeted pesticide/fertilizer application, and irrigation management into a unified system – delivering measurable ROI for farmers. Key players like DJI, XAG, and AgEagle focus on this segment through smart spraying drones and farm management software, with adoption strongest in row-crop farms (corn, soybeans) and orchards. Government subsidies for precision agriculture further accelerate growth, making it the core application driving drone demand globally.

Agricultural Drone Market Regional Analysis

Asia-Pacific (APAC) Region Dominate the Agricultural Drone Market

Dominance by China, India, and Japan led the global agricultural drone market in 2025, which is the largest stake for accurate agricultural technologies, government subsidies, and acute labor deficiency in agriculture. China stands as the world's largest market, with companies such as DJI and Zag Pioneering have a cost -effective spray drones used in millions of hectares. India accelerates adoption among small farmers for crop monitoring and chemical spraying with its peasant drone subsidy scheme. Japan's aging population is a demand for further fuel. APAC is required by favorable rules, expansion of agritech startups, and durable farming practices, as the fastest-growing area. North America and Europe remain important markets, but high drone costs and more mechanized APAC in volume due to the current form of infrastructure. The region's dominance is expected to be strong with AI-managed drone and herd technology.

Recent Development

29 April 2026 – DJI (China)

DJI Agriculture released its 2025/2026 Agricultural Drone Industry Insight Report highlighting rapid global adoption of agricultural drones for precision farming and crop protection. The company reported that more than 600,000 DJI agricultural drones are operating globally across over 100 countries with support from 3,500 service and repair centers. DJI’s agricultural drones have helped reduce water consumption by nearly 410 million tons and lowered carbon emissions by approximately 51 million tons through precision spraying and intelligent farm management. The development strengthens DJI’s leadership in the Agricultural Drones Market by accelerating sustainable farming practices, autonomous spraying, and AI-driven agricultural automation worldwide.

12 November 2025 – XAG (China)

XAG unveiled its next-generation P-series agricultural drones and smart farming ecosystem technologies during its annual technology conference in Guangzhou. The company introduced upgraded agricultural drones featuring autonomous swarm operation, AI-powered navigation, precision spraying, and smart IoT integration for large-scale farming operations. XAG also launched intelligent agricultural autopilot systems and digital farm management platforms aimed at improving crop monitoring and reducing operational costs. The development supports increasing adoption of precision agriculture and autonomous farming technologies globally. Rising demand for efficient crop spraying, seeding, and field mapping solutions continues to strengthen XAG’s position in the Agricultural Drones Market.

Agricultural Drone Market Scope: Inquire before buying

| Agricultural Drone Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 7.86 USD Bn |

| Forecast Period 2026-2032 CAGR: | 30.7% | Market Size in 2032: | 51.18 USD Bn |

| Segments Covered: | by Type | Fixed Wing Drones Rotary Drone Blades Hybrid Drones |

|

| by Component | Frames Controller Systems Propulsion Systems Camera Systems Navigation Systems |

||

| by Payload Capacity | Lightweight drones (up to 2kg) Medium-weight drones (2 to 10kg) Heavy-weight drones (Above 10kg –up to 25kg) |

||

| by Application | Precision Farming Field Mapping Livestock Monitoring Crop Scouting Others |

||

Agricultural Drone Market Key Region

North America (United States, Canada and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam, Indonesia, Philippines, Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America)

Key players/Competitors profiles covered in the Agricultural Drone Market report in strategic perspective

North America

1. AgEagle Aerial Systems Inc. – USA (Wichita, Kansas)

2. PrecisionHawk – USA (Raleigh, North Carolina)

3. Trimble Inc. – USA (Sunnyvale, California)

4. Sentera LLC – USA (Minneapolis, Minnesota)

5. John Deere-USA

6. Harris Aerial – USA (Fort Pierce, Florida)

Europe

1. Parrot Drone SAS (France)

2. senseFly (Switzerland, now part of AgEagle – but EU-developed)

3. Delair (France)

4. Aerones (Latvia)

Asia Pacific

1. DJI (China)

2. XAG (China)

3. TTA (Thailand)

4. Nileworks (Japan)

5. Kray Technologies (Russia)

6. Flying Labs (India)

Middle East and Africa

1. FlySight (UAE)

2. Aerial Vision (South Africa)

3. DroneScan (South Africa)

South America

1. AGX Drones (Brazil)

2. XMobots (Brazil)

Frequently Asked Questions:

1. What are agricultural drones?

Ans: Agricultural drones are unmanned aerial vehicles designed for farming tasks such as crop monitoring, soil analysis, and precise application of fertilizers and pesticides.

2. What are the main types of agricultural drones?

Ans: The market is segmented into fixed-wing drones, rotary drone blades, and hybrid drones, with fixed-wing drones dominating due to their ability to cover large areas efficiently.

3. What are the top manufacturers of agricultural drones?

Ans: Major manufacturers include DJI, XAG, Garuda Aerospace, Yamaha, IO TechWorld, and others, with a focus on advancing technology for precision agriculture.

4. What recent developments are there in the agricultural drone market?

Ans: Recent advancements include the introduction of new drones, government initiatives promoting drone usage, and the establishment of standard operating procedures for pesticide application via drones.