LiDAR Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2034

Overview

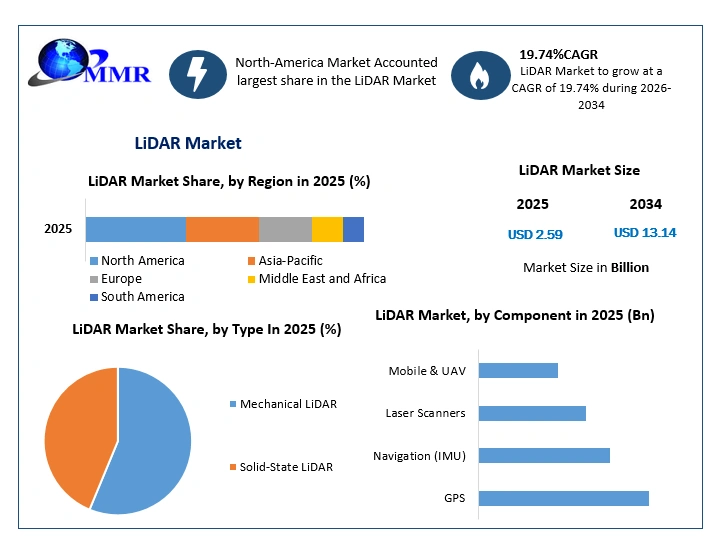

The LiDAR Market size was valued at USD 2.59 Billion in 2025 and the total LiDAR revenue is expected to grow at a CAGR of 19.74% from 2026 to 2034, reaching nearly USD 13.14 Billion.

LiDAR Market Overview:

Light Detection and Ranging (LiDAR) technology utilizes laser tools, micro-electro-mechanical systems (MEMS), and GPS transmitters to create high-quality 3D visual images. Widely employed across automotive, healthcare, aerospace, and defense sectors, LiDAR's diverse applications fuel LiDAR market growth. Enhanced spatial resolution enables precise distance measurement, benefiting operations like mining water runoff analysis and hillside change detection. However, challenges such as cost and data accessibility hinder market expansion. Nonetheless, increasing automation and demand for high-quality 3D imagery, particularly in sectors like military, civil engineering, and corridor mapping, are expected to propel LiDAR market growth, promising advancements and innovation in the field.

LiDAR Market Size, Growth & Share Analysis

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

LiDAR Market Dynamics

The incorporation of increasing automation into LiDAR technologies is profoundly influencing the LiDAR market.

The advancements in spatial resolution within LiDAR-based digital terrain models are yielding superior accuracy in various applications, including change detection on hillsides, water runoff analysis for agriculture or mining sites, and monitoring inland waterways. This progress is fueling the growth of the LiDAR market, propelled by increasing automation to streamline operations and boost efficiency. The rising demand for high-quality 3D imagery, particularly in sectors such as military & defense, topographical surveys, civil engineering, and corridor mapping, is expected to drive LiDAR market growth during the forecast period. Textured 3D imagery finds application in diverse fields like urban planning, 3D mapping, and corridor mapping. The adoption of advanced safety features, including LiDAR integration, is experiencing exponential growth, mainly in regions like the U.S., where government approval for self-driving cars equipped with LiDAR for GPS and navigation purposes has been granted.

LiDAR technology is also instrumental in weather monitoring and environmental surveillance. For instance, Canadian environmental monitoring stations leverage LiDAR to track tropospheric pollution levels. LiDAR installations play a critical role in monitoring volcanic ash emissions that can disrupt air travel routes. Moreover, LiDAR technology is employed in mapping oil sand monitoring systems. These diverse applications, leveraging LiDAR's enhanced precision, are poised to propel LiDAR market growth in the coming years.

However, a significant hindrance to LiDAR market growth is the lack of informed customers. Addressing the need for customer education is crucial to minimizing the costs associated with implementing and designing awareness programs. Enhancing customer knowledge and awareness are essential not only for effectively addressing development and environmental concerns but also for fostering sustainable development. Consequently, strategic efforts to educate customers about LiDAR technology and its applications are imperative for unlocking the full potential of the LiDAR market.

The high cost of LiDAR services and the shortage of geospatial data are significant barriers impeding LiDAR market growth.

The raised expenses associated with LiDAR services and the limited availability of geospatial data present substantial obstacles to LiDAR market growth. These factors hinder the accessibility of LiDAR technology for businesses and organizations, particularly those operating under budgetary constraints. Moreover, the scarcity of geospatial data impedes the development and deployment of LiDAR-based applications, as comprehensive and accurate data is essential for maximizing the technology's effectiveness. Consequently, these challenges restrain LiDAR market growth by constraining adoption across diverse industries and geographical regions. When compared to traditional surveying methods, using LiDAR for surveying is more expensive. A LiDAR system costs around USD 75,000 in total, including high-end electronics, sensors, scanners, and other components. Processing software should ideally be free; however, post-processing software, such as point-cloud categorization, may require third-party software, which can cost anywhere from USD 20,000 to 30,000 per licence. Despite the fact that the cost of LiDAR systems is expected to drop in the next few years as more competitors enter the market, the current cost of surveying with LiDAR is considerable, especially for small-scale projects. Overcoming these barriers will require concerted efforts, such as cost reduction initiatives and initiatives to enhance data accessibility, to unlock the full potential of the LiDAR market.

The Road Ahead for LiDAR market

1. LiDAR technology is a leading trend in engineering and data science, driving significant momentum in the LiDAR market.

2. Surging demand for LiDAR finds roots in diverse applications across emerging sectors like autonomous vehicles and established domains such as construction and mining.

3. This robust demand fuels ongoing research and development efforts within the LiDAR market, aimed at delivering future enhancements in resolution, range, and accuracy.

4. Breakthroughs in solid-state technology and the emergence of spectrum-scan LiDAR are catalysts propelling innovation and broadening the scope of LiDAR applications, further energizing the market.

5. Integration of LiDAR solutions with unmanned aerial vehicles (UAVs) is revolutionizing fields like mapping, surveying, and inspection, reshaping the technological landscape.

6. LiDAR's integration into geographical information systems (GIS) enables meticulous mapping and terrain analysis at high resolutions, expanding the market's scope.

7. Its pervasive use across sectors like autonomous vehicles, agriculture, forestry, and land management underscores its versatility and efficacy in tackling real-world challenges.

8. Future advancements in Artificial Intelligence and Machine Learning promise to enhance LiDAR's capabilities in 3D mapping, object recognition, and scene interpretation.

9. The proliferation of LiDAR technology across industries necessitates robust security protocols, encryption measures, and data authentication mechanisms to safeguard integrity and privacy.

10. Overall, the future outlook for LiDAR technology is promising, empowering both machines and humans with precise and efficient perception capabilities, driving further growth within the market.

LiDAR Technology Gaining Traction in the Automotive Industry

The LiDAR market is poised for significant growth, with shipments expected to surpass 100 million units by 2030, largely propelled by the automotive sector. This surge in demand for LiDAR correlates with the rising adoption of Advanced Driver Assistance Systems (ADAS) and automated driving in both passenger vehicles and robotaxis. Companies like Tesla and Wayve pursue autonomous driving solutions without LiDAR, the majority of automotive manufacturers, including Mercedes-Benz, Nissan, BMW, Stellantis, Volkswagen, and Volvo, have announced plans to incorporate LiDAR into their sensor suites for upcoming vehicle models.

LiDAR faces competition from alternative technologies such as cameras and machine vision, with some entities arguing that vision-based systems alone are adequate for autonomous driving. This presents a potential obstacle to LiDAR's growth, given the relatively low switching costs associated with adopting cheaper vision-based solutions. In the automotive LiDAR market, intense competition prevails, with over 70-80 companies operating globally, targeting various industries and geographic regions. Since , nine companies, namely Velodyne, Luminar, Aeva, Ouster, Innoviz, Aeye, Indie Semiconductor, Quanergy, and Cepton, have announced stock listings through Special Purpose Acquisition Company (SPAC) mergers.

Valeo's Scala stands out as the world's first mass-produced LiDAR for automobiles. In , Mercedes-Benz and Honda introduced Level 3 models, the S-Class and Legend respectively, both equipped with Scala LiDAR. Valeo has shipped over 170,000 LiDAR units since 2017. According to a MMR study, the automotive LiDAR market was valued at approximately $100 million in , driven by the introduction of LiDAR-equipped models by major car manufacturers such as Toyota, Honda, and Chinese companies like Xpeng. Numerous Original Equipment Manufacturers (OEMs) have forged partnerships with LiDAR suppliers for their forthcoming vehicle models, with Chinese automakers taking a lead in such collaborations.

LiDAR Market Segment Analysis

Based on Installation, the LiDAR market is sub-segmented into airborne and Ground-Based. The airborne segment is expected to hold for the largest proportion of the market, which is expected to grow at a CAGR of xx% during the forecast years as more aerial mapping equipment are adopted. Aerial LiDAR replaces photogrammetry as an accurate and thorough way of constructing digital elevation models. In comparison to its terrestrial counterparts, this technology provides improved accuracy and a greater coverage area. It allows for more detailed area mapping in a shorter amount of time. LiDAR systems on the ground are either stationary or mobile. With the assistance of a tripod and balancing assembly, they are mounted on moving platforms such as SUVs or all-terrain vehicles (ATVs). The cost of ground-based LiDAR systems is lower than that of airborne LiDAR systems. The automotive industry is gaining traction as a potential application for mobile ground-based LiDAR systems, with the number of high-end vehicles equipped with advanced driver assistance systems (ADAS) increasing year after year.

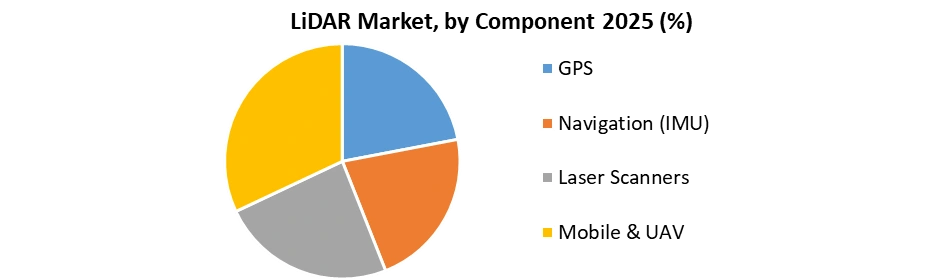

Based on Component, the LiDAR market is sub-segmented into GPS, Navigation (IMU), Laser Scanners and Mobile & UAV. Laser scanners are used to record an intensity value in order to generate a return signal strength that can aid differentiate objects with different reflectivities. LiDAR data from a laser scanner produces a 2D point cloud that can be used for localization, mapping, and modelling of objects and environments. During the projection period, demand for laser scanners is expected to grow significantly, with a CAGR of 15.2 %. Reduced laser technology prices are expected to enable 3D scanning to discover new applications, resulting in significant LiDAR market growth potential during the forecast period.

LiDAR Market Regional Analysis:

In 2025, North America asserted its dominance in the LiDAR market, commanding a significant revenue share of XX%. This was primarily driven by the region's increasing adherence to regulatory mandates mandating the incorporation of specific automotive safety technologies across both light and heavy vehicles.

Asia Pacific is poised to emerge as the swiftest-growing region, with a projected Compound Annual Growth Rate (CAGR) of 14.4% from 2026 to 2034. Asia-Pacific region experienced notable growth opportunities within the automotive sector, fueled by the escalating adoption of technologies such as Advanced Driver Assistance Systems (ADAS) and Autonomous Emergency Braking (AEB). China and India are expected to retain their appeal as lucrative markets, buoyed by significant investments from domestic and international players.

Companies are strategically expanding their presence in Europe and Asia Pacific regions to bolster customer support. For instance, in August 2019, Ouster LiDAR extended its reach into Asia Pacific and Europe by establishing new offices in Shanghai, Paris, and Hong Kong. Additionally, in November, Outer LiDAR forged a collaboration with Kudan Inc. to bolster its footprint in Japan.

LiDAR Industry Ecosystem

LiDAR Market Recent Industry Developments

| Date | Company | Development | Impact |

|---|---|---|---|

| 07 January 2025 | Luminar Technologies | Luminar unveiled its next-generation Halo LiDAR platform at CES 2025, delivering higher resolution, longer range, and lower power consumption for automotive applications. | The launch strengthens ADAS and autonomous driving capabilities while accelerating commercialization of advanced automotive LiDAR systems. |

| 07 January 2025 | Hesai Technology | Hesai introduced the AT1440 automotive LiDAR, featuring 1,440-channel architecture and ultra-high-definition perception for intelligent vehicles. | The innovation significantly improves object detection accuracy and sensing performance, reinforcing competition in the automotive LiDAR market. |

| 18 March 2025 | Ouster | Ouster announced that its REV7 digital LiDAR sensors entered high-volume production, offering improved range, reliability, and perception performance. | The production milestone expands the availability of high-performance digital LiDAR for automotive, industrial, robotics, and smart infrastructure applications. |

| 23 April 2025 | Cepton | Cepton announced an expanded collaboration with Koito Manufacturing to accelerate the mass production of automotive LiDAR systems for global OEM programs. | The partnership enhances manufacturing scalability and OEM adoption, supporting broader deployment of LiDAR-enabled vehicles. |

LiDAR Market Scope: Inquire before buying

| Global LiDAR Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD2.59 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 19.74% | Market Size in 2034: | USD 13.14 Bn. |

| Segments Covered: | by Component | GPS Navigation (IMU) Laser Scanners Mobile & UAV |

|

| by Type | Mechanical LiDAR Solid-State LiDAR |

||

| by Installation | Airborne Ground-Based |

||

| by End-User | Defense and Aerospace Civil Engineering Archaeology Forestry and Agriculture Mining Industry Transportation |

||

Global LiDAR Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

LiDAR Market Key Players:

LiDAR Manufacturers in North America

1. Leica Geosystems Holdings AG (Switzerland)

2. Teledyne Optech Inc. (Canada)

3. Quantum Spatial, Inc. (United States)

4. Faro Technologies, Inc. (United States)

5. Velodyne LiDAR, Inc. (United States)

6. Trimble, Inc. (United States)

7. RIEGL USA (United States)

8. Optech Inc. (Canada)

9. Geodigital (Canada)

10. Topcon Positioning Systems Inc. (United States)

11. Waymo LLC (United States)

12. Lumibird Canada (Canada)

13. Ouster, Inc. (United States)

14. LeddarTech Inc. (Canada)

15. Trimble, Inc. (US)

LiDAR Manufacturers in Europe:

16. YellowScan (France,)

17.Sick AG(Germany)

18. HEXAGON (Sweden)

19. Phoenix LiDAR Systems (Germany)

20. Valeo (France)

21. ZX Lidars (United Kingdom)

22. Vaisala (Finland)

LiDAR Manufacturers in Asia-Pacific:

23. Beijing Surestar Technology (China)

24. Denso (Japan)

Frequently Asked Questions:

1. Which region has the largest share in Global LiDAR Market?

Ans: North America region holds the highest share in 2025.

2. What is the growth rate of Global LiDAR Market?

Ans: The Global LiDAR Market is growing at a CAGR of 19.74% during forecasting period 2026-2034.

3. What segments are covered in Global LiDAR market?

Ans: Global LiDAR Market is segmented into Type, Installation, End-User, Component and region.

4. Who are the key players in Global LiDAR market?

Ans: The important key players in the Global LiDAR Market are – Leica Geosystems Holdings AG (Switzerland), Teledyne Optech Inc. (Canada), Quantum Spatial, Inc. (United States), Faro Technologies, Inc. (United States), Velodyne LiDAR, Inc. (United States), Trimble, Inc. (United States), RIEGL USA (United States).

5. What was the Global LiDAR Market size in 2025?

Ans: The Global LiDAR Market size was USD2.59 Billion in 2025.