Sensor Market by Type, Technology, End Use Industry – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

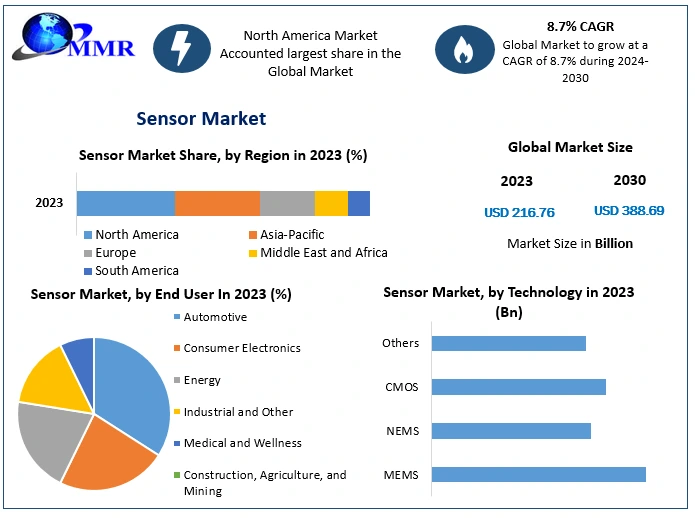

Global Sensor Market size was valued at USD 216.76 Bn in 2023 and is expected to reach USD 388.69 Bn by 2030, at a CAGR of 8.7 %.

Sensor Market Overview:

A sensor is a device that measures and detects physical or environmental characteristics and converts them into electrical signals. Sensors are designed to abduct and quantify specific aspects of the surrounding environment, allowing the detection and monitoring of several phenomena. Sensors work based on different principles and technologies depending on their intended purpose. They are composed of a sensing element, a transduction mechanism, and an output interface. Sensors are used in various fields such as technology, science, industry, and everyday applications.

They play a vital role in collecting data, monitoring systems, and enabling automation. Sensors are employed in various fields such as technology, science, industry, and other applications.They are also used to collect data, monitor systems, and enable automation. The report includes historical data, present and future trends, competitive environment of the Sensor industry. The bottom-up approach was used to estimate the market size. For a deeper knowledge of Sensor market penetration, competitive structure, pricing and demand analysis are included in the report.  To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Sensor Market Dynamics

Drivers

Technological Advancements to Boost the Sensor Market Growth

The emergence of new advanced techniques develops sophisticated and more advanced sensors. These advancements has been improve the performance and accuracy of sensors, allowing them to measure the data with greater correctness. Higher accuracy enables more reliable data collection, which is important in several applications including medical diagnostics, autonomous vehicles and industrial automation. The Advancements in sensor technology have promoted the miniaturization of sensors, to make them smaller in size during maintain their performance.

Miniaturization enables the integration of sensors into compact devices and systems where space is limited. This has opened up new possibilities for sensor integration in areas such as consumer electronics and IoT devices, boosting the growth of the sensor market. Technological advancements help to reduce the cost of sensor manufacturing and production. With the evolution of new sensor technologies, manufacturing techniques becoming more reliable and efficient. This lead to minimized production costs. The decreasing cost makes sensors more affordable to a wide range of industries, stimulating their adoption and fuelling the Sensor industry.

Increasing Demand for Wearable Devices to Fuel Sensor Industry Growth

Wearable devices including smart watches, fitness trackers and healthcare monitors, depend on heavily on sensor technologies. These devices associate several sensors to track and monitor user activities, health parameters, and biometric data. Sensors such as accelerometers, heart rate sensors and GPS modules are generally integrated into wearables. Wearable devices are more popular Due to the increasing focus on personal health and fitness. Users have been more conscious about monitoring their activity levels, heart rate, sleep patterns and intake of calories. Sensors in wearables implement the collection of real-time data, offering users insights into their health and fitness.

The accessibility of wearable devices has driven their adoption, resulting in the growth of the Sensor industry. Wearable devices play an important role in remote patient monitoring, enabling healthcare professionals to monitor patients’ vital signs and health conditions remotely. Sensors integrated into wearables have been transmitting data including blood pressure, blood glucose levels, and oxygen saturation. Remote patient monitoring improves patient care, minimizes hospital visits, and enhances early detection of health issues. The growing adoption of remote patient monitoring solutions increases the growth of the Sensor market.

Sensor Market Trend

Edge Computing and Sensor Fusion

Edge computing delivers data processing and analysis closer to the source of data generation, minimizing latency and improving response time. Sensors produce a large amount of data, particularly in industrial automation, autonomous vehicles, and smart city applications. By performing data processing and analytics at the edge, near the sensors, real-time insights have been obtained without the requirement to send data to a centralized cloud. This capability is crucial for time-sensitive applications that need immediate decision-making based on sensor data.

Edge computing support optimizes bandwidth usage by processing data locally and sending only relevant information to the cloud or central servers. This access minimizes the amount of data that needs to be transmitted over the network, reducing bandwidth needs and associated costs. By processing data at the edge, latency is reduced. This data does not need to travel to a remote location for analysis. This is more important for applications where low latency is difficult, including autonomous vehicles, robotics, and real-time monitoring systems.

Sensor Market Restraints

High Cost of Sensor

The Sensor Cost has been a significant barrier to the adoption of sensors, particularly for certain advanced sensor technologies. Sensors with advanced features, high precision, or specific need has been involve complex manufacturing processes or the use of expensive materials, resulting in higher production costs. The high cost of sensors has been limiting their adoption in price-sensitive markets.

Data Privacy and Security Concerns

Sensors generate vast amounts of data and the collection and storage of this data increase privacy and security concerns. Data privacy regulations and the potential risk of data breaches or unauthorized access to sensitive information have hindered the adoption of certain sensor technologies, particularly in sensitive data handling industries including healthcare or finance. Ensuring robust security measures and approving privacy regulations is vital to building trust and mitigating concerns related to data privacy and security and hampering the Sensor Market growth.

Sensor Market segment analysis

Based on Type: On the basis of the Type, the market is segmented into Physical Sensors,Chemical Sensors and Biological Sensors. Physical Sensors held the largest Sensor Market share in 2023 and are expected to grow at a significant CAGR for the market. Physical sensors are the most vital type in several industries such as consumer electronics, automotive, healthcare, and others. These sensors are employed to monitor and measure physical properties such as temperature, pressure, etc. They offer required data for control systems, safety applications, and environmental monitoring. Accelerometers and gyroscopes which are the types of physical sensors are used for motion sensing and orientation detection in the consumer electronics industry.

These sensors enable features including gaming control based on device movement. Temperature sensors are extensively used in industrial processes, HVAC systems and medical devices. They help in monitoring temperature to ensure optimal functioning and safety.Pressure sensors are largely useful in automotive and healthcare, where they are used to measure and monitor pressure levels in systems and devices. They enable correct pressure measurements applications such as tire pressure monitoring, medical monitoring equipment, and industrial processes. As a result, an increase in the use of physical sensors in several industries drives the Sensor Market growth.

Based on Technology: MEMS is expected to dominate the Sensor market with the highest CAGR during the forecast period. MEMS technology is the integration of mechanical elements, sensors and electronics on a single microchip. MEMS enables the miniaturization of sensors making them more cost-effective and suitable for many applications.This miniaturization grants compact designs of sensors and enables them in various devices and systems. The small size and integration capabilities of MEMS sensors make them suitable for applications in consumer electronics, wearables, and automotive systems.

MEMS technology offers high sensitivity, accuracy, and reliability in a compact form factor, to make it useful technology in the sensor market. MEMS technology has led to continuous advancements and innovations, resulting in improvement of sensor performance, increased functionality and expands use. MEMS technology developments have resulted in enhanced sensitivity, minimize power consumption, improve integration and the innovation of new advanced types of MEMS sensors. As a result, the increasing use of MEMS technology and developments in its technology drive the market growth.

Sensor Market Regional Insights

North America dominated the Sensor Market with the largest revenue and is expected to maintain its dominance over the forecast period. In North America, the automotive industry is a key consumer of sensors, with applications ranging from advanced driver assistance systems (ADAS) to engine control, safety systems, and environmental monitoring. The increasing adoption of sensors for compliance and improved vehicle performance due to the stringent safety and emission regulations and drive the regional Sensor market share.

The rising investment in sensor technologies to develop autonomous vehicles and enhance the overall driving experience by automakers and technology companies are also the boosting factor for regional market growth. The presence of prominent technology companies, growing research and development activities, and increasing demand for sensors in various industries are the influencing factors for the regional market.

Asia Pacific is expected to grow at the highest CAGR for the Sensor Market during the forecast period. Developing economies such as China, Japan, South Korea, and India are the significant market for the sensor due to increasing demand for the sensor from several industries. China is the major flourishing manufacturing sector, automotive industry, and consumer electronics market and thus it has a massive market for sensors. Technological advancements and innovations in sensors in South Korea especially in robotics, healthcare, and automotive applications and a strong presence in the semiconductor industry in Japan are the growth factors for the regional market. In India, the expansion of industrialization and rising investments in infrastructure development drive Sensor market growth.

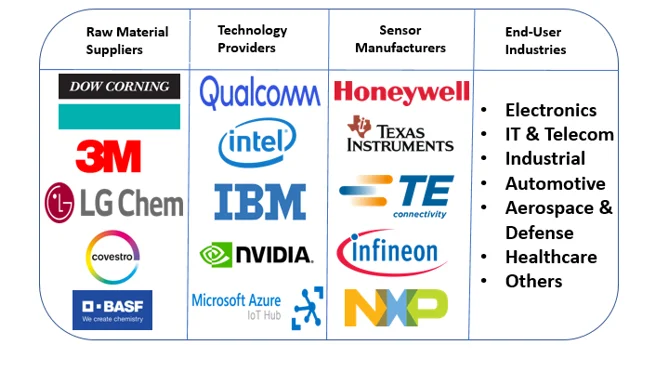

Sensor Industry Ecosystem Sensor Market Scope: Inquire before buying

Sensor Market Scope: Inquire before buying

| Global Sensor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 216.76 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 8.7% | Market Size in 2030: | US $ 388.69 Bn. |

| Segments Covered: | by Type | Radar Sensor Optical Sensor Biosensor Touch Sensor Image Sensor Pressure Sensor Temperature Sensor Proximity & Displacement Sensor Level Sensor Motion & Position Sensor Humidity Sensor Accelerometer & Speed Sensor Others |

|

| by Technology | MEMS NEMS CMOS Others |

||

| by End-User | Electronics IT & Telecom Industrial Automotive Aerospace & Defense Healthcare Others |

||

Sensor Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Sensor Key Player

1. Texas Instruments Incorporated

2. TE Connectivity Ltd

3. Omega Engineering Inc.

4. Honeywell International Inc.

5. Rockwell Automation Inc.

6. Atmel Corporation

7. Honeywell International Inc.

8. Infineon Technologies AG

9. Johnson Controls International PLC.

10. NXP Semiconductors N.V.

11. Qualcomm Technologies Inc.

12. Robert Bosch GmbH

13. Sony Corporation

14. STMicroelectronics

15. Texas Instruments Inc.

16. TE Connectivity

17. STMicroelectronics NV

18. Bosch Sensortec GmbH.

19. ABB Group

20. Siemens AG

21. OMRON Corporation

22. Samsung Electronics Co Ltd.

23. International Sensor Technology

24. DENSO Corporation

Frequently Asked Questions:

1] What is the growth rate of the Global Sensor Market?

Ans. The Global Sensor Market is growing at a significant rate of 8.7 % during the forecast period.

2] Which region is expected to dominate the Global Sensor Market?

Ans. North America is expected to dominate the Sensor Market during the forecast period.

3] What is the expected Global Sensor Market size by 2030?

Ans. The Sensor Market size is expected to reach USD 388.69 Bn. by 2030.

4] Which are the top players in the Global Sensor Market?

Ans. The major top players in the Global Sensor Market are Texas Instruments Incorporated, TE Connectivity Ltd, Omega Engineering Inc., Honeywell International Inc., Rockwell Automation Inc., Atmel Corporation, Honeywell International Inc., Infineon Technologies AG, Johnson, Controls International PLC., Robert Bosch GmbH and others.

5] What are the factors driving the Global Sensor Market growth?

Ans. Technological advancements and increasing demand for wearable devices are expected to drive market growth during the forecast period.