COVID-19, from the huge group of coronaviruses (CoV), has now become a threat to people and the worldwide economy. China is the largest manufacturer of a semiconductor component in the world and also the largest exporter. Most of the provinces and hubs of semiconductor component production in China went into lockdown after the virus outbreak. China’s GDP is estimated to drop by 1-1.25 due to lower production. This will hit the global economy as China accounts for approximately 19.71 % of global GDP at buying power equality. Therefore, the global GDP will drop by around 0.5 % during this pandemic. We expect that the virus outbreak will also impact the Indian electronics industry on a massive scale.

In parallel, efforts are underway to relieve the devastating economic consequences of COVID-19, which contain business shutdowns, unemployment, and extraordinary drops in the gross domestic product (GDP) across several economies. The semiconductor industry, which has historically been a major source of high-tech jobs, is among the many sectors that have had to adjust their production planning and tasks as COVID-19 shifts demand for major semiconductor end applications.

Impact of COVID-19 on global semiconductor demand

The COVID-19 crisis is unprecedented in the current time. While the recession during the financial crisis from 2007 to 2008 was driven by stagnating consumer demand, the COVID-19 situation induced a shock to both global demand and supply, creating a dual challenge. This unique phenomenon makes it difficult to extrapolate from past crises to make forecasts.

Global GDP projections are based on two scenario

• Global GDP recovers in the fourth quarter of 2020

• Global GDP recovery is delayed until late 2022

Based on the two scenarios we calculated, we anticipatethe demand to drop by 6 to 14% for the semiconductor industry in 2020 compared to 2019. Breaking down this projection by major end markets—PC or server, consumer electronics, wireless communication, wired communication, industrial applications, and automotive.

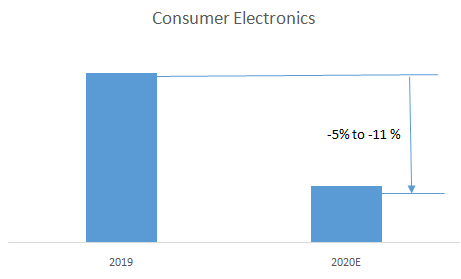

Consumer electronics

Semiconductor companies provide components to numerous consumer-electronics products such as televisions, video games, watches, etc. Consumers utilize optional assets to purchase most products in this category, so demand has highly corresponded with local GDP. The expected demand for consumer-electronics semiconductors to drop by 5 to 11 % in 2020.

Consumer electronics are faring better way due to a current rise in demand for audio equipment, video games, and some kitchen appliance. A trend is likely occurring because people are spending more time at home. While this increase has halfway balanced an important declines reported for other consumer-electronics products, it likely comes from one-off purchases and thus will not continue after some time. As a result, the reduced demand for consumer-electronic semiconductors will extend beyond 2020

Many of the electronics manufacturers based on North America and Europe depend on certain components built by suppliers in China. IPC, electronics equipment, ran a survey in February in which 65% of 150 participating electronics manufacturers and suppliers reported delays from suppliers due to the spread of coronavirus.

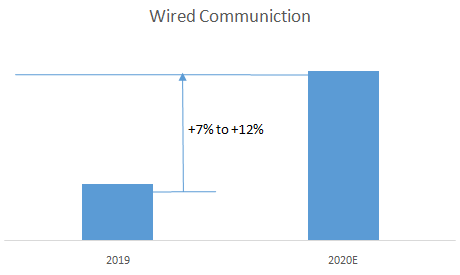

Wired communication

Demand for semiconductors utilized in wired communication applications is expected to increase by 7 to 12% in 2020 because of a few pandemic-related factors such as:

• The necessity of security advancements for existing enterprise infrastructures because more employees are working from home

• A more than 50 % increase in fixed broadband utilization in certain economies, prominent to more purchases of link/DSL and remote switches as employees upgrade internet connections in private home workplaces

• Higher internet traffic that will impetus the demand for switches and routers

• Notable demand for cloud services and related computing nodes, which will build the requirement for optoelectronics in data center fiber connections

• A more than 40 % increase in video streaming across many networks

Even if the economic downturn persists after 2020, demand for semiconductors used in wired communication will still grow. Annual growth may not remain as high as the 7 to 12 % seen in 2020. But, many of the declared investments are one-time purchases that will reduce future replacement needs.

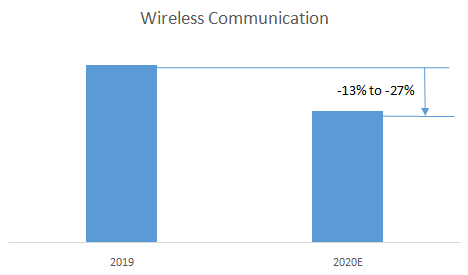

Wireless communication

Demand for semiconductors used in wireless communication

applications will see perhaps the keenest drop in 2020, which is almost a drop of 13 to 27 %. The level of mobile-phone sales is the primary demand driver in this category, has historically been well corresponded with GDP, and therefore is expected to drop significantly over the coming months. Sharp declines have just been reported in the region where COVID-19 is predominant, particularly in China. We also expect consumer inclinations should move to more affordable phones that will also negatively affect demand for semiconductors. The recovery of mobile-phone sales will fluctuate by geography, with China prone to see an uptick before Europe and the United States, since its economy is closer to recovery.

For 5G wireless communication, infrastructure has two different demand patterns. In regions that have not launched 5G networks, telecom providers will expect to postpone investments and instead focus on improving their current networks to accommodate growing data traffic. By contrast, some telecom providers in the region that already have 5G will double down on their investments, particularly if governments offer subsidies trying to fuel the local GDP.

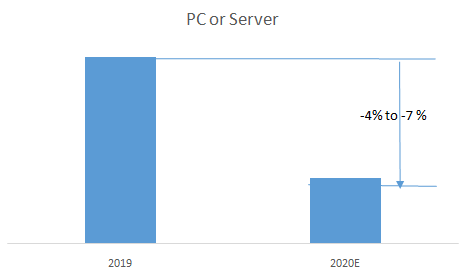

PC or server

Demand for PC semiconductors will decrease by an expected 4 to 7% in 2020 due to companies will postpone scheduled hardware upgrades and other long-term migration projects. Stable laptop and tablet demand will incompletely balance this drop since numerous buyers are upgrading their private IT infrastructure to help their homeschooling activities or work. These one-time IT equipment upgrades won’t be repeated similarly in later years if the downturn continues and consumers cut back spending even further. This reality joined with enterprises decreasing PC substitutions to deal with their liquidity, could additionally dissolve semiconductor deals after 2020 if the crisis continues.

We expect chip demand for the PC and server end market to decline by 4 to 7 % this year, with results fluctuating by product.

In the third and fourth quarters of 2020, the semiconductor market for servers could increase by 4 to 7%, driven by a solid boost in video streaming and conferencing as more people work from home. Demand for enterprise cloud solutions and enterprise IT are required to stay stable or show a minor decrease as certain organizations cut IT financial plans while others accelerate their cloud-migration plans. Augmented server requests may not persist past 2020. But, if the global economy endures struggling after the fourth quarter of 2020, various firms will cut IT spending plans, a trend that will exceed any additional increases in video streaming.

Hence, the depressed end-market demand due to widening quarantine orders in major countries is considerably decreasing pressure on the electronics components supply chain. Market players in the electronics components industry are now faced with the challenge of balancing the supply/demand environment in a world plagued with uncertainty and fear.